|

市場調查報告書

商品編碼

2065518

用於人工智慧推理的GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)AI Inference GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

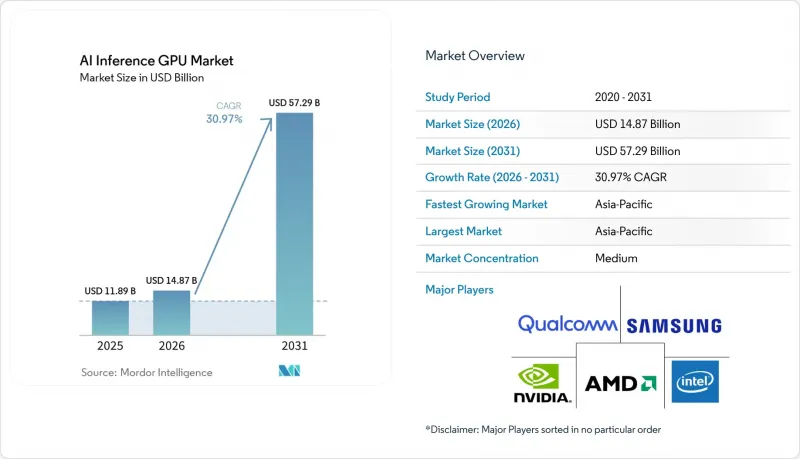

用於人工智慧推理的 GPU 市場規模預計將從 2025 年的 118.9 億美元和 2026 年的 148.7 億美元成長到 2031 年的 572.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 30.97%。

本報告按部署類型(雲端/資料中心、邊緣及其他)、外形規格(PCIe GPU、SXM/OAM GPU及其他)、應用領域(生成式人工智慧、電腦視覺、建議系統、自主系統及其他)和地區(北美、歐洲、亞太、南美及其他)進行細分。市場預測以美元計價。

全球人工智慧推理GPU市場趨勢與洞察

超大規模資料中心對產生式人工智慧服務的需求激增

超大規模雲端提供的推理叢集規模遠超訓練系統,這反映了單一大型語言模型可以處理數百萬個同時上線用戶的現實。微軟 Azure 在 2025 年底新增了 12 萬塊 NVIDIA H200 NVL GPU,以支援 GitHub Copilot 和 Azure OpenAI 端點。這些端點在 2025 年 12 月處理了超過 500 億次 API 呼叫。 Oracle 雲端基礎設施報告稱,由於採用了水冷機架設計,GPU 推理工作負載的運轉率達到了 99.95%,該設計可將結溫保持在 75 度C以下。 AWS 於 2026 年 3 月推出了客製化晶片“Inferentia 3”,其吞吐量是 Inferentia 2 的三倍,但對於利用 FP8 和 INT4 量化的混合精度工作負載,NVIDIA Blackwell NVL 仍然具有優勢。 Meta公司透露,其2025年400億美元的資本預算中將有180億美元用於推理基礎建設,凸顯了其自有而非租賃的戰略重點。隨著對話式人工智慧的延遲目標日益嚴格(從2024年的500毫秒降至2026年的200毫秒以下),對配備高頻寬記憶體和低延遲互連的GPU的需求持續成長。

電子商務平台上建議引擎的快速普及

即時個人化如今的延遲低於 10 毫秒,迫使零售商採用 GPU 進行推理,以便處理稀疏嵌入和動態特徵,避免批量處理的延遲。隨著賣家從基於 CPU 的協同過濾遷移到 GPU 加速的深度學習模型,亞馬遜 Personalize 在 2025 年提升了推理吞吐量。阿里雲的含光 800 晶片將淘寶和天貓的建議延遲從 35 毫秒降低到 12 毫秒,並在 2025 年雙十一購物節查詢期將每次查詢的能耗降低了 60%。 Shopify 於 2025 年 9 月整合了 NVIDIA TensorRT-LLM,使其產品發現模型能夠在 5 分鐘內適應庫存波動,並提高了試點參與者的轉換率。據位元組跳動稱,TikTok Shop 在 NVIDIA A100 和 H100 GPU 上每小時可處理 4 億次產品展示,而積極的模型剪枝將推理成本控制在商品交易總額 (GMV) 的 0.02% 以下。

高階推理GPU的初始投資成本很高

NVIDIA H200 NVL 的標價超過 4 萬美元,這對於沒有風險投資或雲端服務信貸的中型企業來說是一個巨大的障礙。戴爾科技的數據顯示,由於對高頻寬記憶體和水冷系統的需求,AI 最佳化伺服器的平均售價比去年同期上漲了 35%。 Supermicro 報告稱,GPU 伺服器的前置作業時間為 16 週,並且需要預付 50% 的定金,這意味著交貨時間要到 2026 年下半年。 Equinix 的數據顯示,AI 推理機架平均功耗為 25 千瓦,這增加了託管成本。 NVIDIA 的 DGX 雲端訂閱服務(每 GPU 小時 5.5 美元)是一種替代方案,但只有當利用率保持在 60% 以上時,本地部署才具有成本效益。

細分市場分析

2025年,隨著超大規模資料中心業者中心集中資源處理每日數十億次API調用,雲端和資料中心部署佔據了AI推理GPU市場佔有率的60.17%。 2025年下半年,微軟Azure新增12萬個H200 NVL單元,每月可支援500億次GitHub Copilot調用,凸顯了吞吐量指標對採購決策的重要性。 Meta公司斥資180億美元用於推理基礎建設,進一步顯示了從訓練到服務的轉變趨勢。

邊緣部署正以 31.53% 的複合年成長率快速發展,在延遲限制導致無法進行雲端往返處理的場景中,邊緣部署正迅速崛起。特斯拉的「全自動駕駛」電腦利用客製化加速器每秒處理 2300 幀攝影機影像,展現了邊緣應用所需的確定性效能。在工業自動化領域,設備內推理是滿足控制迴路時序要求的首選方案,但嚴格的功耗限制了 GPU 選擇,使其僅限於 Jetson AGX Orin 等 60 瓦以下的模組。因此,用於 AI 推理的 GPU 市場呈現兩極化:一方面是擁有充足電力的超大規模資料中心,另一方面是電力受限的邊緣站點。

區域分析

亞太地區預計在2025年將佔全球收入的69.52%,並在2031年之前以31.92%的複合年成長率成長,這主要得益於各國政府主導的人工智慧項目、與超大規模企業的合作以及資料中心的積極擴張。由於出口管制導致NVIDIA H100的供應受到限制,華為在2025年交付了超過5萬塊Ascend 910C加速器。 Reliance Jio和NVIDIA於2025年9月成立了一家合資企業,旨在為推進印度企業級人工智慧服務奠定基礎,目標是在2027年中期部署10萬塊H100 GPU。新加坡和泰國於2026年批准建造新的水冷園區,新增800兆瓦的容量,並將於2027年向GPU租戶開放。

北美地區對用於人工智慧推理的GPU的需求主要由超大規模雲端服務供應商和受監管企業推動,這些企業傾向於在本地部署推理系統以滿足資料主權要求。 AWS於2025年7月發布了“Inferentia 3”,報告稱其穩定擴散管道在遷移到TensorRT最佳化後延遲降低了40%。摩根大通經營著私有雲端,這表明該公司傾向於使用自有基礎設施來處理合規性至關重要的工作負載。一家加拿大能源公司於2026年初開始試行部署Groq語言處理單元,用於即時測井分析,顯示市場對低延遲晶片的興趣日益濃厚。

歐洲人工智慧法規增加了文件和透明度要求,延長了引進週期。西門子已證明合規是可行的。其基於 Gaudi 3 的 Simatic 人工智慧平台在滿足強制性風險評估揭露要求的同時,將半導體工廠的停機時間減少了 18%。法國和德國已撥款 20 億歐元(21.8 億美元)用於計劃於 2028 年運作的國家主導的推理雲項目,這表明隨著法規的日益清晰,市場需求將出現爆炸式成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心對產生式人工智慧服務的需求激增

- 電子商務平台上建議引擎的快速普及

- 電腦視覺在工業自動化領域的廣泛應用。

- 擴大對話式人工智慧在客戶支援營運的應用

- 針對變壓器剪枝推理最佳化的GPU的出現。

- 開放原始碼推理編譯器的可用性有助於降低整體擁有成本

- 市場限制因素

- 高階推理GPU的初始投資成本很高

- 邊緣部署中的功率和散熱限制

- 先進封裝基板的供應鏈波動

- 來自 RISC-V 和客製化 ASIC AI 加速器的競爭日益激烈。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端/資料中心

- 邊緣

- 嵌入式/裝置端

- 按外形規格

- PCIe GPU

- SXM/OAM GPUs

- 嵌入式模組

- 透過使用

- 人工智慧世代

- 電腦視覺

- 建議統

- 自主系統

- 自然語言處理/對話式人工智慧

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Baidu, Inc.

- Microsoft Corporation

- Graphcore Ltd.

- Tenstorrent Inc.

- Mythic AI, Inc.

- Flex Logix Technologies, Inc.

- Imagination Technologies Ltd.

- Arm Holdings plc

- Cerebras Systems, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI inference GPU market size is projected to expand from USD 11.89 billion in 2025 and USD 14.87 billion in 2026 to USD 57.29 billion by 2031, registering a CAGR of 30.97% between 2026 and 2031.

This report is Segmented by Deployment Type (Cloud/Data Center, Edge, and More), Form Factor (PCIe GPUs, SXM/OAM GPUs, and More), Application (Generative AI, Computer Vision, Recommendation Systems, Autonomous Systems, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI Inference GPU Market Trends and Insights

Surging Demand for Generative AI Services in Hyperscale Data Centers

Hyperscale clouds are provisioning inference clusters that now exceed the scale of their training systems, reflecting the reality that a single large language model serves millions of concurrent users. Microsoft Azure added 120,000 NVIDIA H200 NVL GPUs in late 2025 to support GitHub Copilot and Azure OpenAI endpoints, which processed more than 50 billion API calls in December 2025. Oracle Cloud Infrastructure reported 99.95% uptime for GPU inference workloads after adopting liquid-cooled rack designs that keep junction temperatures below 75 °C. AWS introduced Inferentia 3 custom silicon in March 2026, delivering triple the throughput of Inferentia 2, yet NVIDIA Blackwell NVL remains ahead in mixed-precision workloads that exploit FP8 and INT4 quantization. Meta revealed that inference infrastructure consumed USD 18 billion of its USD 40 billion 2025 capital budget, underscoring the strategic priority of owning rather than leasing capacity. As latency targets for conversational AI tighten from 500 milliseconds in 2024 to less than 200 milliseconds in 2026, demand for GPUs with high-bandwidth memory and low-latency interconnects continues to accelerate.

Rapid Proliferation of Recommendation Engines in E-commerce Platforms

Real-time personalization now operates at sub-10-millisecond latency, forcing retailers to adopt inference GPUs that manage sparse embeddings and dynamic features without batch delays. Amazon Personalize increased inference throughput in 2025 as merchants migrated from CPU-based collaborative filtering to GPU-accelerated deep learning models. Alibaba Cloud's Hanguang 800 chip cut recommendation latency from 35 milliseconds to 12 milliseconds on Taobao and Tmall, reducing per-query energy consumption by 60% during the 2025 Singles' Day peak. Shopify integrated NVIDIA TensorRT-LLM in September 2025, enabling product-discovery models to adapt to inventory changes within 5 minutes and boosting conversion rates for pilot merchants. ByteDance stated that TikTok Shop processes 400 million product impressions per hour on NVIDIA A100 and H100 GPUs, with inference costs representing less than 0.02% of gross merchandise value due to aggressive model pruning.

High Up-Front Capital Cost of High-End Inference GPUs

List prices for NVIDIA H200 NVL units exceed USD 40,000, creating a significant barrier for mid-tier enterprises that lack venture debt or cloud credits. Dell Technologies stated that AI-optimized server average selling prices rose 35% year over year due to high-bandwidth memory and liquid-cooling requirements. Supermicro reported 16-week lead times for GPU servers and required 50% deposits, extending deliveries into late 2026. Equinix data shows AI inference racks consume 25 kilowatts on average, driving a premium in colocation charges. NVIDIA's DGX Cloud subscription at USD 5.50 per GPU-hour offers an alternative, but ownership remains cost-effective only when utilization stays above 60%.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Computer Vision across Industrial Automation Lines

- Growing Adoption of Conversational AI in Customer Support Operations

- Power and Cooling Constraints in Edge Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud and data-center installations held 60.17% of the AI inference GPU market share in 2025 as hyperscalers pooled resources to serve billions of daily API calls. Microsoft Azure's addition of 120,000 H200 NVL units in late 2025 enabled 50 billion GitHub Copilot calls in a single month, underscoring the throughput criteria that dominate procurement decisions. Meta's USD 18 billion allocation to inference infrastructure further illustrates the pivot from training to serving.

Edge deployments, advancing at 31.53% CAGR, gain traction where latency budgets deny round-trip cloud processing. Tesla's Full-Self-Driving computer processes 2,300 camera frames per second on custom accelerators, demonstrating the deterministic performance edge applications demand. Industrial automation similarly favors on-device inference to meet control-loop timing requirements, but strict power envelopes constrain GPU selection to sub-60-watt modules, such as the Jetson AGX Orin. The AI inference GPU market thus bifurcates between power-rich hyperscale facilities and constrained edge sites.

Geography Analysis

Asia-Pacific accounted for 69.52% of revenue in 2025 and is forecast to grow at a 31.92% CAGR through 2031, supported by sovereign AI programs, hyperscale partnerships, and aggressive data center expansion. Huawei shipped more than 50,000 Ascend 910C accelerators in 2025 after export restrictions limited NVIDIA H100 availability. Reliance Jio and NVIDIA formed a joint venture in September 2025 to install 100,000 H100 GPUs by mid-2027, anchoring India's push for enterprise AI services. Singapore and Thailand approved new liquid-cooled campuses in 2026, adding 800 megawatts of capacity that will open to GPU tenants in 2027.

The demand for AI inference GPUs in North America is driven by hyperscale cloud providers and regulated enterprises that prefer on-premises inference to meet data-sovereignty mandates. AWS released Inferentia 3 in July 2025 and reported 40% lower latency for Stable Diffusion pipelines after migrating to TensorRT optimization. JPMorgan Chase operates a private cloud with more than 10,000 NVIDIA H100 GPUs, underscoring the bank's preference for owned infrastructure for compliance-sensitive workloads. Canadian energy firms started pilot deployments of Groq language-processing units in early 2026 for real-time well-log interpretation, signaling rising interest in deterministic-latency silicon.

Europe's AI Act adds documentation and transparency obligations, lengthening deployment cycles. Siemens showed compliance is achievable; its Gaudi 3-based Simatic AI platform reduced semiconductor-fab downtime by 18% while meeting mandated risk-assessment disclosures. France and Germany earmarked EUR 2 billion (USD 2.18 billion) for sovereign inference cloud programs that will come online in 2028, indicating pent-up demand once regulatory clarity improves.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Baidu, Inc.

- Microsoft Corporation

- Graphcore Ltd.

- Tenstorrent Inc.

- Mythic AI, Inc.

- Flex Logix Technologies, Inc.

- Imagination Technologies Ltd.

- Arm Holdings plc

- Cerebras Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Generative AI Services in Hyperscale Data Centers

- 4.2.2 Rapid Proliferation of Recommendation Engines in E-commerce Platforms

- 4.2.3 Expansion of Computer Vision across Industrial Automation Lines

- 4.2.4 Growing Adoption of Conversational AI in Customer Support Operations

- 4.2.5 Emergence of Transformer-Pruning Optimized Inference GPUs

- 4.2.6 Availability of Open-Source Inference Compilers Lowering TCO

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capital Cost of High-End Inference GPUs

- 4.3.2 Power and Cooling Constraints in Edge Deployments

- 4.3.3 Supply-Chain Volatility for Advanced Packaging Substrates

- 4.3.4 Rising Competition from RISC-V and Custom ASIC AI Accelerators

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud / Data Center

- 5.1.2 Edge

- 5.1.3 Embedded / On-Device

- 5.2 By Form Factor

- 5.2.1 PCIe GPUs

- 5.2.2 SXM / OAM GPUs

- 5.2.3 Embedded Modules

- 5.3 By Application

- 5.3.1 Generative AI

- 5.3.2 Computer Vision

- 5.3.3 Recommendation Systems

- 5.3.4 Autonomous Systems

- 5.3.5 NLP / Conversational AI

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Baidu, Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Graphcore Ltd.

- 6.4.10 Tenstorrent Inc.

- 6.4.11 Mythic AI, Inc.

- 6.4.12 Flex Logix Technologies, Inc.

- 6.4.13 Imagination Technologies Ltd.

- 6.4.14 Arm Holdings plc

- 6.4.15 Cerebras Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人工智慧推理市場規模、佔有率和成長分析:按產品/服務、部署模式、處理類型、企業規模、最終用戶產業、應用和地區分類-2026-2033年產業預測

人工智慧推理市場規模、佔有率和成長分析:按產品/服務、部署模式、處理類型、企業規模、最終用戶產業、應用和地區分類-2026-2033年產業預測 AI推理市場:按運算方法、記憶體、網路、部署方法、應用程式、最終用戶、國家和地區分類-全球產業分析、市場規模及佔有率、未來預測(2026-2033年)

AI推理市場:按運算方法、記憶體、網路、部署方法、應用程式、最終用戶、國家和地區分類-全球產業分析、市場規模及佔有率、未來預測(2026-2033年) 2026-2030年全球人工智慧推理服務市場

2026-2030年全球人工智慧推理服務市場 人工智慧推理市場分析及預測(至2035年):按類型、產品、技術、組件、應用、部署、最終用戶、功能和解決方案分類

人工智慧推理市場分析及預測(至2035年):按類型、產品、技術、組件、應用、部署、最終用戶、功能和解決方案分類 2026年全球多模態推理路由器市場報告

2026年全球多模態推理路由器市場報告 2026-2030年全球人工智慧推理硬體市場2026年全球人工智慧(AI)量化工具市場報告

2026-2030年全球人工智慧推理硬體市場2026年全球人工智慧(AI)量化工具市場報告 人工智慧推理解決方案市場:按解決方案、部署類型、組織規模、應用和最終用戶分類 - 2026-2032 年全球預測

人工智慧推理解決方案市場:按解決方案、部署類型、組織規模、應用和最終用戶分類 - 2026-2032 年全球預測 人工智慧推理晶片市場規模、佔有率和成長分析:按晶片類型、部署模式、應用、終端用戶產業、處理類型和地區分類-2026-2033年產業預測

人工智慧推理晶片市場規模、佔有率和成長分析:按晶片類型、部署模式、應用、終端用戶產業、處理類型和地區分類-2026-2033年產業預測 全球人工智慧推理市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

全球人工智慧推理市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)