|

市場調查報告書

商品編碼

2064525

冷藏展示櫃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Refrigerated Display Cases - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

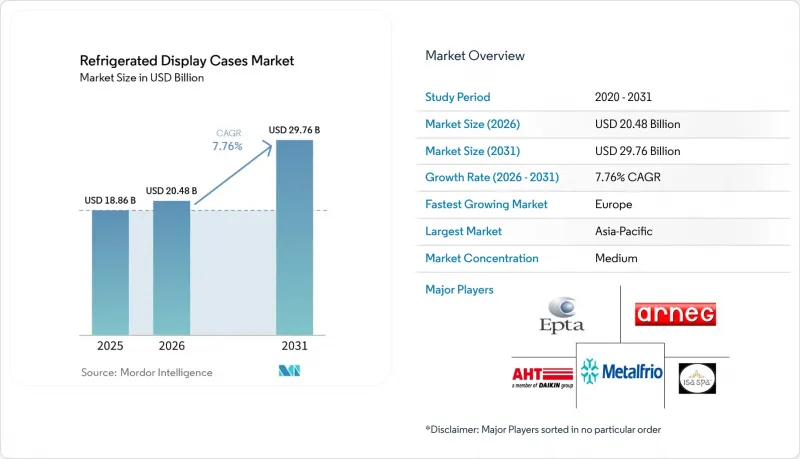

根據 Mordor Intelligence 預測,冷藏展示櫃市場規模將從 2025 年的 188.6 億美元和 2026 年的 204.8 億美元成長到 2031 年的 297.6 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.76%。

本報告依冷凍方式(插電式、半插電式、遙控式)、產品設計(垂直、水平式、混合式、半立式)、應用領域(零售店、餐廳/飯店等)、終端用戶(超級市場/大賣場、便利商店、專賣店、折扣店等)及地區進行細分。市場預測以美元計價。

全球冷藏展示櫃市場趨勢及洞察

零售連鎖店整修與便利商店擴張

零售商店的現代化改造專案正在推動冷藏展示櫃的需求超越常規的更換週期。便利商店正在擴大已調理食品、包裝飲料和冷藏食品的銷售空間,這導致每家整修的門市需要更多的展示櫃。預計便利商店食品服務銷售額將從2005年的11.9%成長到2025年的28.5%,佔門市總利潤的38.9%,凸顯了業者為何在門市設計中優先考慮冷藏食品的可見性。作為其2026年「未來之路計畫」的一部分,Love's Travel Stops正在投資7億美元,用於分店20家新店和整修35家現有門市,該計畫的核心是最佳化食品和飲料菜單。此趨勢對冷藏展示櫃市場有重大影響。這是因為與傳統的以加油為主的便利商店佈局相比,以食品主導的便利商店通常需要更多的冷藏展示空間。這使得新店分店和店鋪整修都保持了強勁的需求。

天然冷媒與節能維修週期

在冷藏展示櫃市場,一波升級改造浪潮正在興起,其驅動力並非來自可自由支配的支出,而是冷媒法規。歐盟第2024/573號法規於2024年3月生效,收緊了歐盟範圍內氟化溫室氣體的分階段減排計畫。在美國,新的聯邦法規正在加速新型商用冷凍設備向全球暖化潛勢較低的冷媒過渡,從而加快了舊HFC系統的更換週期。美國環保署(EPA)也在2024年提高了自主型展示櫃R290冷媒的充填量上限,擴大了丙烷型即插即用系統的應用範圍,使其大規模面積以往更大。 2025年至2029年間,美國食品零售商計劃安裝1,470個新的跨臨界二氧化碳冷藏櫃,並升級13,400個現有系統,這充分體現了轉型規模之大。在冷藏展示櫃市場,這些監管合規期限限制了需求,因為企業不能無限期地推遲設備決策。

高昂的初始維修和安裝成本

資本成本仍是冷藏展示櫃市場普及應用的一大直接障礙,尤其對小規模企業而言更是如此。在新建設中,超臨界二氧化碳系統比傳統的氫氟碳化合物(HFC)系統成本高出10%至20%,而在維修項目中,由於通常需要額外的基礎設施建設,這一差距會進一步擴大。如果企業在同一規劃週期內還要承擔門市改造、節能升級和冷媒合規等費用,那麼這筆負擔就更加難以承受。紐約州撥款35萬美元,幫助布朗克斯區的兩家Key Food超市過渡到R290冷藏櫃,這表明公共支持已經開始減輕小規模的大規模網路和更長期的資本規劃中。同時,在零售業分散、缺乏規模優勢的零售環境中,也減緩了過渡的步伐。

細分市場分析

截至2025年,插電式冷藏展示櫃將佔據58.37%的市場佔有率,並持續維持其在冷藏展示櫃市場中最大細分市場的地位。這一主導地位反映了自主型冷藏展示櫃的廣泛應用,它們被廣泛應用於便利商店、麵包店、專賣店和小規模雜貨店。由於安裝簡單且無需集中式冷凍設備,插電式系統仍然是許多維修專案的標準選擇。美國環保署(EPA)於2024年提高了R290嵌入式冷藏櫃的冷媒充填量限制,擴大了丙烷型插電式冷藏展示櫃適用的店鋪類型範圍,進一步增強了中小商店升級改造的必要性。

預計從2026年到2031年,遠端系統將以8.34%的複合年成長率成長,成為冷藏展示櫃市場中成長最快的系統配置。這一成長主要得益於新建超級市場和大規模整修項目的推進,這些項目傾向於採用集中式二氧化碳製冷系統,因為該系統能夠實現更廣泛的溫度控制和系統整合。 Food Lion在2025年底於夏洛特地區的整修項目中,部分門市引入了二氧化碳製冷系統,這表明大型連鎖超市正在將門市整修與冷媒更換相結合。半即插即用系統目前仍處於中間位置,尤其是在歐洲零售業。在歐洲,熱回收和水循環佈局能夠滿足中型門市的需求,這些門市需要比完全遠端安裝更高的柔軟性。因此,冷藏展示櫃產業正逐漸形成一個更清晰的區分:適用於維修的即插即用型系統和主導超市主導的遠端安裝系統。

到2025年,立式展示櫃將佔據55.12%的市場佔有率,繼續成為冷藏展示櫃市場的核心設計形式。這一地位源於其在乳製品、生鮮食品、飲料和周邊展示領域的廣泛應用,在這些領域,貨架可見性和展示各種SKU的能力至關重要。 Epta公司於2026年推出的「Zenith」系列產品,與先前的型號相比,節能高達36%,同時展示面積增加了13%,充分展現了立式展示櫃如何提升效率和銷售業績。隨著零售商尋求更有效率的現有占地面積利用率,這種組合有助於維持直立式展示櫃的市場主導地位。

混合式配置預計到2031年將以8.56%的複合年成長率成長,成為冷藏展示櫃市場中成長最快的設計細分市場。零售商對混合展示形式表現出越來越濃厚的興趣,這種形式將開放式和封閉式展示櫃結合在同一條生產線上,同時也能提高能源管理效率。臥式冷藏櫃仍廣泛應用於冷凍櫃和冰淇淋展示,AHT公司於2024年底推出的「KIGALI XL」產品,展現了該公司在該細分市場持續的產品研發,重點關注可視性和基於R290冷媒的性能。混合式配置成長的重要性源自於其滿足了零售商減少門市獨立冷藏櫃生產線、提高品類擺放柔軟性的需求。冷藏展示櫃產業的競爭格局正在從簡單的外形設計轉向如何使每個櫃體佈局都能兼顧能源效率和商品展示品質。

區域分析

到2025年,歐洲將佔據冷藏展示櫃市場39.41%的佔有率,成為最大的區域貢獻者。這一區域主導地位反映了超級市場的高密度分佈以及更早地向二氧化碳製冷過渡,而這得益於比許多其他市場更為嚴格的環境法規。歐盟第2024/573號條例進一步強化了逐步淘汰含氟溫室氣體的進程,敦促歐盟各地的業者加速系統現代化改造計畫。這項政策背景也得到了門市翻新活動的推動,例如Waitrose Colesdon的2025年冷凍設備升級和門市整修項目,該項目中的系統升級與一項更廣泛的現代化改造項目同步進行。

預計到2031年,亞太地區將以8.73%的複合年成長率成長,成為冷藏展示櫃市場成長最快的地區。都市化、便利商店的擴張以及對低溫運輸基礎設施的持續投資正在推動中國、印度、韓國和東南亞的需求成長。韓國便利商店產業已進入品質提升階段,超過70%的業者已將老舊設備更換為變頻式高效冷藏展示櫃。印度也正在崛起為強勁的需求中心,有組織的零售業擴張以及供應商的投資(例如Elanpro的「2025體驗中心」計畫)推動了印度國內商用冷凍和冷凍設備市場的成長。

北美仍是第二大區域市場,也是冷藏展示櫃市場採用天然冷媒的主要爭議點。在美國,一項針對自足式系統中高全球暖化潛勢(GWP)冷媒的新聯邦法規於2025年1月生效,其適用範圍於2026年1月擴大至遠端冷凝應用,從而導致更嚴格的合規階段。隨著克羅格(Kroger)、奧樂齊(Aldi)、全食超市(Whole Foods)和沃爾瑪(Walmart)等大型零售商已開始調整其新的門市冷凍策略,採用二氧化碳跨臨界系統,該地區的發展方向正變得越來越清晰。南美洲受益於有組織的零售業的擴張和進口即插即用型設備的供應,而中東地區仍然受到炎熱潮濕環境的限制,這種環境並不適合標準的二氧化碳跨臨界設計。非洲的低溫運輸發展仍處於早期階段,但 Frigoglass 在埃及的擴張(透過與 Fresh SAE 的合作,目標是年產 10 萬台)表明,該地區的冷藏展示櫃市場具有長期成長潛力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 零售連鎖店整修與便利商店擴張

- 天然冷媒與能源效率提升維修循環

- 生鮮食品、冷凍食品和即食食品的促銷都有所成長。

- 實施智慧監控和預測性維護

- 用於全通路食品揀選和微型倉配的冷藏暫存區

- 高級生鮮食品區整修

- 市場限制因素

- 高昂的初始維修和安裝成本

- 能源和生命週期服務成本負擔

- 二氧化碳、R290 和 A2L 系統工程師短缺

- 周邊環境和電網波動帶來的性能風險

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 不同的冷凍系統

- 外掛

- 半插件

- 偏僻的

- 透過產品設計

- 垂直的

- 水平的

- 混合

- 半垂直(傾斜)

- 透過使用

- 零售店

- 餐廳和飯店

- 其他用途

- 最終用戶

- 超級市場和大賣場

- 便利商店

- 專賣店

- 折扣店

- 設有加油站的商店

- 餐廳和咖啡館

- 麵包店

- 飯店

- 其他終端用戶商店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Epta SpA

- Arneg SpA

- ISA SpA

- AHT Cooling Systems GmbH

- Metalfrio Solutions SA

- Frigoglass Services Single Member SA

- True Manufacturing Co., Inc.

- Zero Zone, Inc.

- Turbo Air Inc.

- Beverage-Air Corporation

- Structural Concepts Corporation

- Hill PHOENIX, Inc.

- TEFCOLD A/S

- Ugur Cooling Inc. Co.

- Migali Industries Inc.

- Qingdao Hiron Commercial Cold Chain Co., Ltd.

- Gram Professional ApS

- Fagor Professional, S.Coop.

- Liebherr-Hausgerate GmbH

- Hoshizaki America, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the refrigerated display cases market size is projected to expand from USD 18.86 billion in 2025 and USD 20.48 billion in 2026 to USD 29.76 billion by 2031, registering a CAGR of 7.76% between 2026 and 2031.

This report is Segmented by Refrigeration Architecture (Plug-In, Semi Plug-In, and Remote), Product Design (Vertical, Horizontal, Hybrid, and Semi-Vertical), Application (Retail Stores, Restaurants and Hotels, and More), End User (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Discount Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Refrigerated Display Cases Market Trends and Insights

Retail Chain Refurbishment and Convenience Store Expansion

Retail modernization programs are extending demand for refrigerated display cases beyond a typical replacement cycle. Convenience stores are allocating more floor space to prepared meals, packaged beverages, and chilled foodservice, which raises the number of cases needed in each remodeled outlet. C-store foodservice accounted for 28.5% of total in-store sales in 2025, up from 11.9% in 2005, and contributed 38.9% of in-store gross profit, underscoring why operators are redesigning stores around chilled food visibility. Love's Travel Stops committed USD 700 million in 2026 to open 20 locations and remodel 35 existing sites under its Road Ahead Plan, with a stronger food-and-beverage offer at the center of the program. In the refrigerated display cases market, that pattern matters because a food-led convenience format typically needs more linear chilled frontage than a legacy fuel-centered layout. This is keeping demand active in both new openings and store refresh work.

Natural Refrigerant and Energy-Efficiency Retrofit Cycle

The refrigerated display case market is undergoing a replacement wave driven by refrigerant rules rather than discretionary spending. Regulation (EU) 2024/573 took effect in March 2024 and tightened the phasedown path for fluorinated greenhouse gases across the European Union. In the United States, newer federal rules have pushed the sector toward lower-global-warming-potential refrigerants in new commercial refrigeration equipment, thereby shortening the replacement window for older HFC-based systems. The EPA also raised the R290 charge limit for self-contained display cases in 2024, which widened the use case for propane-based plug-in systems in larger footprints than before. Between 2025 and 2029, U.S. food retailers planned to install 1,470 new transcritical CO2 stores and replace 13,400 existing systems, which shows how large the transition pipeline has become. In the refrigerated display cases market, these compliance deadlines are serving as a floor for demand, as operators cannot indefinitely defer equipment decisions.

High Upfront Retrofit and Installation Costs

Capital costs remain a direct brake on adoption in the refrigerated display case market, especially for smaller operators. Transcritical CO2 systems can cost 10-20% more than conventional HFC systems in new builds, and retrofit projects often require additional infrastructure work, widening the gap further. That burden becomes harder to absorb when operators are also funding store remodels, energy upgrades, and refrigerant compliance in the same planning cycle. New York State awarded USD 350,000 to support 2 Bronx Key Food stores in shifting to R290 cases, demonstrating that public support is already helping smaller retailers cover the economic costs. In the refrigerated display cases market, this favors large chains that can spread transition costs across bigger store networks and longer capital programs. It also slows conversion in fragmented retail environments where stores lack scale purchasing power.

Other drivers and restraints analyzed in the detailed report include:

- Fresh, Frozen, and Grab-and-Go Food Merchandising Growth

- Smart Monitoring and Predictive Maintenance Adoption

- Energy and Lifecycle Service Cost Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plug-in refrigerated display cases held 58.37% of the market share in 2025, maintaining their position as the largest architecture segment in the refrigerated display cases market. Their lead reflects the deep installed base of self-contained units across convenience stores, bakeries, specialty retailers, and smaller grocery formats. Plug-in systems remain the default choice in many retrofit projects because they are easier to install and do not require a centralized refrigeration plant. The 2024 increase in EPA charge limits for R290 self-contained cases widened the range of store formats that propane-based plug-in units can serve, which strengthened the case for replacement in smaller and medium-sized outlets.

Remote systems are projected to grow at a 8.34% CAGR from 2026 to 2031, making them the fastest-growing architecture in the refrigerated display cases market. Growth is being driven by new supermarket builds and large remodel programs that favor centralized CO2 racks for broader temperature control and system integration. Food Lion's late-2025 remodel program in the Charlotte region included CO2-based cooling systems in select stores, which shows how large chains are pairing store renewal with refrigerant transition. Semi plug-in systems continue to occupy the middle ground, especially in European retail, where heat recovery and waterloop layouts support medium-format stores that need more flexibility than a full remote setup. The refrigerated display cases industry is therefore splitting more clearly between retrofit-friendly plug-in units and chain-led remote builds.

Vertical cases accounted for 55.12% share in 2025 and remained the core design format across the refrigerated display cases market. Their position comes from strong use in dairy, fresh food, beverage, and perimeter merchandising, where shelf visibility and broad SKU display are critical. Epta's Zenith line, launched in 2026, delivered up to 36% energy savings compared to prior models while expanding the display area by up to 13%, demonstrating how vertical cabinets improve both efficiency and sales performance. That combination helps vertical formats defend their lead as retailers look for higher productivity from existing floor space.

Hybrid configurations are projected to expand at a 8.56% CAGR through 2031, making them the fastest-growing design segment in the refrigerated display cases market. Retailers are showing more interest in mixed-display formats that can combine open and closed presentation within a single run while improving energy control. Horizontal cases continue to serve freezer chest and ice cream applications, and AHT's KIGALI XL launch in late 2024 demonstrated continued product development focused on visibility and R290-based performance in that market segment. Hybrid growth is important because it reflects retailer demand for fewer separate case lines across the store and better flexibility in category placement. In the refrigerated display case industry, design competitions are now centered less on simple form factors and more on how each cabinet layout supports both energy savings and merchandising quality.

Geography Analysis

Europe held 39.41% of the refrigerated display cases market share in 2025, making it the largest regional contributor. The region's lead reflects a dense supermarket base and an earlier move into CO2 refrigeration, supported by tighter environmental rules than in most other markets. Regulation (EU) 2024/573 strengthened the phase-out path for fluorinated greenhouse gases and is forcing operators across the European Union to bring forward system replacement plans. That policy backdrop is being reinforced by store refresh activity, including projects such as Waitrose Coulsdon's 2025 refrigeration replacement and store update, which linked system renewal with broader modernization work.

Asia-Pacific is projected to grow at a 8.73% CAGR through 2031, making it the fastest-growing region in the refrigerated display cases market. Urbanization, the expansion of convenience retail, and continued investment in cold chain infrastructure are driving broader demand across China, India, South Korea, and Southeast Asia. South Korea's convenience store base has entered a quality-upgrade phase, with operators replacing older units with inverter-based, high-efficiency display cases at conversion rates above 70%. India is also emerging as a stronger demand center, with domestic commercial refrigeration growth supported by organized retail expansion and supplier investments such as Elanpro's 2025 experience center initiative.

North America remained the second-largest regional market and a key battleground for natural refrigerant adoption in the refrigerated display cases market. The United States entered a more binding compliance phase when new federal restrictions on higher-GWP refrigerants in self-contained installations took effect in January 2025 and were further extended to remote condensing applications in January 2026. Large retailers, including Kroger, ALDI, Whole Foods, and Walmart, have already aligned their new-store refrigeration strategy with CO2 transcritical adoption, which is tightening the direction of travel for the region. South America is supported more by organized retail expansion and imported plug-in units, while the Middle East remains constrained by high ambient conditions that are less favorable to standard CO2 transcritical designs. Africa is still at an earlier stage of cold chain development, but Frigoglass's Egypt expansion, with a target of 100,000 units of annual production through its partnership with Fresh S.A.E, points to a longer-term growth position for the refrigerated display cases market in the region

- Epta S.p.A.

- Arneg S.p.A.

- ISA S.p.A.

- AHT Cooling Systems GmbH

- Metalfrio Solutions S.A.

- Frigoglass Services Single Member S.A.

- True Manufacturing Co., Inc.

- Zero Zone, Inc.

- Turbo Air Inc.

- Beverage-Air Corporation

- Structural Concepts Corporation

- Hill PHOENIX, Inc.

- TEFCOLD A/S

- Ugur Cooling Inc. Co.

- Migali Industries Inc.

- Qingdao Hiron Commercial Cold Chain Co., Ltd.

- Gram Professional ApS

- Fagor Professional, S.Coop.

- Liebherr-Hausgerate GmbH

- Hoshizaki America, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail Chain Refurbishment and Convenience Store Expansion

- 4.2.2 Natural Refrigerant and Energy-Efficiency Retrofit Cycle

- 4.2.3 Fresh, Frozen, and Grab-and-Go Food Merchandising Growth

- 4.2.4 Smart Monitoring and Predictive Maintenance Adoption

- 4.2.5 Omnichannel Grocery Pickup and Micro-Fulfillment Chilled Staging

- 4.2.6 Premium Fresh Food Perimeter Remodeling

- 4.3 Market Restraints

- 4.3.1 High Upfront Retrofit and Installation Costs

- 4.3.2 Energy and Lifecycle Service Cost Burden

- 4.3.3 Technician Shortage for CO2, R290, and A2L Systems

- 4.3.4 High-Ambient and Grid-Volatility Performance Risk

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Refrigeration Architecture

- 5.1.1 Plug-In

- 5.1.2 Semi Plug-In

- 5.1.3 Remote

- 5.2 By Product Design

- 5.2.1 Vertical

- 5.2.2 Horizontal

- 5.2.3 Hybrid

- 5.2.4 Semi-Vertical

- 5.3 By Application

- 5.3.1 Retail Stores

- 5.3.2 Restaurants and Hotels

- 5.3.3 Other Applications

- 5.4 By End User

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Specialty Stores

- 5.4.4 Discount Stores

- 5.4.5 Fuel Station Stores

- 5.4.6 Restaurants and Cafes

- 5.4.7 Bakeries

- 5.4.8 Hotels

- 5.4.9 Other End User Outlets

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Epta S.p.A.

- 6.4.2 Arneg S.p.A.

- 6.4.3 ISA S.p.A.

- 6.4.4 AHT Cooling Systems GmbH

- 6.4.5 Metalfrio Solutions S.A.

- 6.4.6 Frigoglass Services Single Member S.A.

- 6.4.7 True Manufacturing Co., Inc.

- 6.4.8 Zero Zone, Inc.

- 6.4.9 Turbo Air Inc.

- 6.4.10 Beverage-Air Corporation

- 6.4.11 Structural Concepts Corporation

- 6.4.12 Hill PHOENIX, Inc.

- 6.4.13 TEFCOLD A/S

- 6.4.14 Ugur Cooling Inc. Co.

- 6.4.15 Migali Industries Inc.

- 6.4.16 Qingdao Hiron Commercial Cold Chain Co., Ltd.

- 6.4.17 Gram Professional ApS

- 6.4.18 Fagor Professional, S.Coop.

- 6.4.19 Liebherr-Hausgerate GmbH

- 6.4.20 Hoshizaki America, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

LED冷藏展示櫃照明市場預測至2034年:按類型、應用和地區分類的全球分析

LED冷藏展示櫃照明市場預測至2034年:按類型、應用和地區分類的全球分析 冷藏展示櫃市場報告:依產品類型、產品設計、最終用途及地區分類,2026-2034年

冷藏展示櫃市場報告:依產品類型、產品設計、最終用途及地區分類,2026-2034年 冷藏展示櫃市場:2026-2032年全球市場預測(依產品類型、服務類型、溫度、門類型、最終用戶和安裝配置分類)義式霜淇淋展示櫃市場:依產品類型、門類型、容量範圍、最終用戶和安裝方式分類,全球預測(2026-2032年)

冷藏展示櫃市場:2026-2032年全球市場預測(依產品類型、服務類型、溫度、門類型、最終用戶和安裝配置分類)義式霜淇淋展示櫃市場:依產品類型、門類型、容量範圍、最終用戶和安裝方式分類,全球預測(2026-2032年) 冷藏展示櫃市場規模、佔有率和趨勢分析報告:按展示類型、類型、設計、最終用途和細分市場預測(2025-2033 年)

冷藏展示櫃市場規模、佔有率和趨勢分析報告:按展示類型、類型、設計、最終用途和細分市場預測(2025-2033 年) 2026年全球保溫器展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球檯式保溫器與展示櫃市場報告

2026年全球保溫器展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球檯式保溫器與展示櫃市場報告 冷藏展示櫃市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、產品設計、地區和競爭格局分類,2021-2031年

冷藏展示櫃市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、產品設計、地區和競爭格局分類,2021-2031年