|

市場調查報告書

商品編碼

2064514

邊緣人工智慧軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Edge AI Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

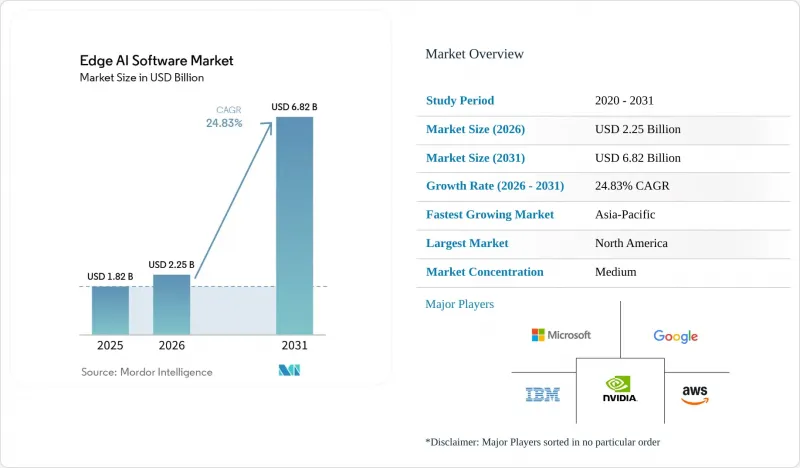

根據 Mordor Intelligence 預測,邊緣人工智慧軟體市場規模預計將在 2025 年達到 18.2 億美元,2026 年達到 22.5 億美元,到 2031 年達到 68.2 億美元,2026 年至 2031 年的複合年成長率為 24.83%。

本報告按交付類型(解決方案和服務)、資料模態(視覺資料、聽覺資料、文字和語言資料、環境和位置資料、多模態資料)、部署類型(雲端、本地部署等)、最終用戶產業(製造業、醫療保健、零售和消費品、能源和公共產業等)以及地區進行細分。市場預測以價值(美元)表示。

全球邊緣人工智慧軟體市場趨勢與洞察

物聯網終端資料激增

隨著工業和企業終端產生的機器數據量呈爆炸性成長,基於雲端的中繼架構難以高效處理這些數據,邊緣人工智慧軟體市場正蓬勃發展。 2026 年 5 月發表在《Discover Computing》上的一項關於 ELARA 框架的研究表明,在大規模聯網網路中,ELARA 框架的端到端延遲僅為 39-52 毫秒,頻寬降低高達 48%,任務完成率高達 93-98%。這直接支援對時間敏感的工作負載進行本地處理。這項結果意義重大,因為工業系統可以以 1 Hz 或更高的頻率在數千個節點上傳輸感測器資料流,而且隨著部署規模的擴大,將原始遙測資料發送到集中式基礎設施的成本會迅速增加。此外,根據思科發布的《2026 年無線通訊現況報告》,物聯網成長已成為企業無線投資的最大驅動力,超越了用戶移動性和高頻寬應用的普及。這表明,網路支出不僅受連接性增強的影響,也受終端智慧的影響。在此背景下,邊緣人工智慧軟體市場受益匪淺,因為企業需要一種軟體,它能夠在決定哪些資料應該傳輸到上游之前,先在本地過濾、關聯資料並採取行動。此外,僅靠原始容量不足以滿足此需求。

邊緣低延遲決策的需求

邊緣人工智慧軟體市場的發展也受到製造業、自主系統、公共產業和公共安全等領域即時決策需求的驅動。當延遲容忍度低於 50 毫秒或站點遙測資料量達到每天 1 Terabyte時,本地推理就成為一項實際需求,而不僅僅是設計選項。 2026 年 3 月,NVIDIA 和 T-Mobile 宣布將使用 NVIDIA Metropolis 平台,在分散式 5G 邊緣網路上整合實體人工智慧應用。這包括智慧公共產業運作、自動化公用事業巡檢以及反應速度至關重要的工業安全工作負載。同樣在 2026 年 3 月,惠普企業 (HPE) 發布了“HPE AI Grid”,可在分散式推理網站上提供可預測的低延遲效能。此外,Comcast 已開始在其網路上使用小型語言模型進行即時邊緣推理的現場測試。因此,邊緣人工智慧軟體市場正在轉向即使在運算資源受限的環境下也能穩定推理效能的平台。這是因為使用時的確定性行為比基準硬體上的平均吞吐量更重要。

整合異質邊緣環境的複雜性

邊緣人工智慧軟體市場仍然面臨著巨大的營運挑戰,因為大多數企業部署都涉及不同的處理器類型、作業系統和連接環境。 2026 年發表在 Sensors 上的一項關於 MIGS 架構的研究表明,整合異質設備需要能夠同時處理 Modbus、OPC UA 和 MQTT 協議的獨立於協議的中間件。這表明,在實際的工業環境中,互通性仍面臨許多挑戰。 2026 年 ZEDEDA 的一項調查也指出了類似的問題,41% 的企業認為分散式工作負載管理是一項主要挑戰,47% 的企業表示,採用混合雲端-邊緣架構需要在不同的硬體環境中實現一致的管治。這導致邊緣人工智慧軟體市場出現兩極化:擁有標準化設備的大型企業可以快速擴展,而擁有傳統操作技術的收購公司則往往面臨更長的引進週期和更高的整合成本。在開發出更通用的硬體抽象層之前,互通性仍將是限制部署速度和軟體標準化的結構性瓶頸。

細分市場分析

到了2025年,該解決方案在邊緣人工智慧軟體市場佔據62.72%的佔有率,並繼續保持主導地位,因為企業更傾向於整合平台而非模組化合約模式。這一趨勢反映了一種務實的採購趨勢:製造商、通訊業者和其他大型用戶都在尋求經過驗證的軟體包,這些軟體包將檢驗運行時、壓縮工具和配置編配整合到單一產品中。買家通常更青睞這種方法,因為它降低了邊緣互通性的不確定性,並減輕了整合不同供應商工具的負擔。在邊緣人工智慧軟體市場,這一趨勢使平台提供者獲得了早期收入優勢,因為他們可以銷售完整的營運層,而不僅僅是有限的功能。這一趨勢也表明,邊緣人工智慧軟體市場已經超越了試點階段,因為採購團隊通常只有在內部團隊確認了明確的長期營運路徑後,才會對捆綁解決方案進行標準化。

預計到2031年,服務市場將以25.64%的複合年成長率成長,超過整體邊緣人工智慧軟體市場的成長速度。這一差異表明,在初始軟體堆疊部署之後,部署管理方式正在轉變。許多公司缺乏必要的內部工程團隊來管理跨分散式資產的模型漂移,這導致外包邊緣MLOps、模型最佳化、生命週期管理以及跨所有資產的可觀測性等服務成為日益成長的趨勢。西門子在2026年4月宣布擴展其“西門子工業邊緣工業人工智慧套件”,進一步明確了這一轉變。該套件涵蓋跨多個工廠的模型訓練、部署、重新訓練和人工智慧模型管理。谷歌在2026年擴展了對iOS Swift、JavaScript和Android API的LiteRT-LM支持,這表明行動環境也出現了類似的趨勢,運行時環境的行為越來越像嵌入式管理層,而不是獨立的軟體產品。

因此,儘管邊緣人工智慧軟體市場的產品和服務經濟效益正逐漸趨於融合,但這兩類數據目前仍分開報告。對許多公司而言,整合解決方案仍然是初始採購選項,但隨著部署從試點階段過渡到全面運營,服務層的重要性日益凸顯。這一點在2023年和2024年部署了邊緣硬體且仍缺乏內部人工智慧人才的中型工業用戶中尤為明顯。因此,邊緣人工智慧軟體產業正從簡單的基於許可的軟體產品模式,向將軟體包與持續營運支援相結合的生命週期平台發展。

到2025年,視覺數據將佔營收的29.98%,成為邊緣AI軟體市場中最大的數據模態。這一主導地位建立在電腦視覺技術多年來在工廠檢測、安防監控和汽車感知系統等領域的應用之上。全球攝影機基礎設施仍然是主要的需求來源,因為許多終端仍在採集影像,但這些影片並未進行即時分析。 NVIDIA指出,到2026年,全球將安裝超過15億個攝影機,但其中只有不到1%的攝影機能夠進行有效的即時分析。這表明,本地視覺推理框架仍有很大的發展空間。對於邊緣AI軟體市場而言,這意味著視覺工作負載仍然是當前收入的基礎,因為它們與企業已有的支出項目(例如品管、安全監控和自動化檢測)直接相關。

隨著終端用戶希望在本地處理的資訊類型不斷擴展,其他資料模態也在不斷成長。文字和語言資料支援人機介面和本地對話功能,而環境和位置資料則與監控、路由和基礎設施等應用場景息息相關。隨著越來越多的公司尋求能夠同時解讀多個輸入而無需為每個資料流建立單獨模型的單一技術棧,多模態人工智慧正變得具有重要的戰略意義。 NVIDIA 於 2026 年 5 月發布的 Nemotron 3 Nano Omni 模型將視覺、語言和語音感知功能整合到一個緊湊的模型中,專為基於代理的邊緣工作負載而設計,這體現了向更整合的推理架構的轉變。邊緣人工智慧軟體市場正從中受益,因為當客戶需要更豐富的本地上下文資訊但又無法在資源受限的設備上支援多個完整的軟體堆疊時,多模態模態模型可以簡化操作複雜性。

預計到2031年,語音數據將以26.88%的複合年成長率成長,成為邊緣人工智慧軟體市場成長最快的模態。最強勁的需求來自旋轉機械中的語音異常檢測、倉庫機器人中的語音命令介面,以及醫療和銀行業中需要本地回應的互動式系統。語音工作負載還具有成本優勢,因為其模型通常比同類視覺系統更小,因此可以在配置較低的硬體上運行。這降低了已在大規模終端設備中部署MCU級設備的工業OEM廠商的進入門檻。未來,語音和多模態用例預計將在邊緣人工智慧軟體產業中變得越來越重要,因為它們無需像視覺推理那樣消耗大規模運算資源,即可帶來可操作的效能提升。

區域分析

2025年,北美繼續保持其最大區域貢獻者的地位,佔據邊緣人工智慧軟體市場佔有率的34.78%。該地區受益於超大規模資料中心業者平台和工業技術供應商的高度集中,使企業買家能夠比其他大多數地區更早獲得全端部署方案。北美邊緣人工智慧軟體市場也受益於成熟的企業軟體採購週期,大型企業在試點檢驗後越來越願意投資多站點部署。 HPE於2026年3月發布的「AI Grid」以及Comcast的分散式邊緣推理現場試驗表明,部署活動正從工廠擴展到通訊基礎設施和消費者服務交付網路。 IBM於2026年5月發布的「Sovereign Core」反映了數位主權和營運管理正在影響政府和受監管企業的需求這一採購格局。

預計到2031年,亞太地區將以26.71%的複合年成長率成長,成為邊緣人工智慧軟體市場成長最快的區域市場。這一成長勢頭主要得益於中國龐大的製造業規模、日本的機器人和汽車項目、印度的工程基礎以及韓國的半導體生態系統。 2026年3月,《日經新聞》引述富士嵌合體研究所的研究報告稱,人工智慧代理和基於邊緣的物理人工智慧推理將從2026年起推動日本市場擴張。邊緣環境在隱私保護和人工智慧代理商業化方面的重要性日益凸顯。這一成長趨勢意義重大,因為亞太地區邊緣人工智慧軟體市場與大規模工業部署以及本地設計生態系統密切相關,後者使得人工智慧功能能夠更緊密地整合到設備層。這也意味著,區域供應商和全球供應商在一個成本效益、在地化和硬體相容性與軟體功能同等重要的環境中競爭。

由於歐洲擁有強大的工業基礎和鼓勵買方主導型人工智慧部署模式的法規環境,因此在邊緣人工智慧軟體市場繼續保持顯著的佔有率。德國電信的「歐洲邊緣連續體」(European Edge Continuum)計畫於2025年進入即時實驗室和預生產階段,並於2026年實現商業部署,透過聯邦式互通邊緣基礎設施層支援歐洲的數位化主權議程。思科也重點介紹了奧迪與西門子合作,於2025年3月在博林格霍夫工廠部署的「邊緣雲端4生產」(Edge Cloud 4 Production)項目,該項目將虛擬化軟體定義自動化和人工智慧驅動的製程控制引入歐洲汽車製造業。這些案例表明,歐洲邊緣人工智慧軟體市場與工業現代化、資料管理和主權基礎設施建設等優先事項密切相關。南美洲、中東和非洲以及土耳其仍然是重要的市場,儘管目前規模較小,但對農業、普惠金融、智慧城市、物流和能源管理的投資正在這些地區創造對人工智慧應用的特定需求。在這些地區,行動優先連接和國家數位基礎設施計劃往往是推動技術普及的主要因素,而不是廣泛的企業標準化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 物聯網終端資料激增

- 邊緣低延遲決策的需求

- 對保護隱私的設備端推理的需求

- 相容於5G的分散式應用架構

- 艦隊規模邊緣模型運行與編配

- 安全關鍵型部署的身份驗證支援堆疊

- 市場限制因素

- 整合異質邊緣環境的複雜性

- 模型最佳化在受限設備上的局限性

- 受監管物品引入過程中的認證缺口

- 針對異質軟體堆疊的不成熟基準測試

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 解決方案

- 服務

- 按數據模態

- 視覺化數據

- 聽覺數據

- 文字和語言數據

- 環境和位置數據

- 多模態數據

- 部署模式

- 雲

- 現場

- 混合

- 按最終用戶行業分類

- 製造業

- 資訊科技/通訊

- 醫療保健和生命科學

- 汽車和運輸業

- 零售和消費品

- 能源公用事業

- 智慧城市與公共基礎設施

- 銀行業、金融服務業及保險業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- International Business Machines Corporation

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies, Inc.

- Nutanix, Inc.

- Siemens AG

- Synaptics Incorporated

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Edge Impulse, Inc.

- ClearBlade, Inc.

- ZEDEDA, Inc.

- Viso AI AG

- Latent AI, Inc.

- Gorilla Technology Group Inc.

- PTC Inc.

- Renesas Electronics Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the edge AI software market size is projected to be USD 1.82 billion in 2025, USD 2.25 billion in 2026, and reach USD 6.82 billion by 2031, growing at a CAGR of 24.83% from 2026 to 2031.

This report is Segmented by Offering (Solutions, and Services), Data Modality (Visual Data, Auditory Data, Text and Language Data, Environmental and Location Data, and Multimodal Data), Deployment Mode (Cloud, On-Premise, and More), End-User Industry (Manufacturing, Healthcare, Retail and Consumer Goods, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Edge AI Software Market Trends and Insights

Proliferation Of Internet Of Things Endpoint Data

The edge AI software market is gaining momentum because the amount of machine-generated data at industrial and enterprise endpoints has become too large for cloud-relay architectures to handle efficiently. Research on the ELARA framework, published in Discover Computing in May 2026, showed end-to-end latency of 39-52 milliseconds, bandwidth savings of up to 48%, and task completion rates of 93-98% across large-scale IoT networks, which directly supports local processing for time-sensitive workloads. That result matters because industrial systems can emit sensor streams at 1 Hz or higher across thousands of nodes, and the cost of transmitting raw telemetry into centralized infrastructure rises quickly as deployments scale. Cisco's State of Wireless Report 2026 also found that IoT growth ranked as the top driver of enterprise wireless investment, ahead of user mobility and high-bandwidth application adoption, which shows that network spending is now being shaped by endpoint intelligence rather than simple connectivity expansion. In this setting, the edge AI software market benefits because enterprises need software that can filter, contextualize, and act on data locally before deciding what should move upstream, and raw network capacity alone does not solve that requirement.

Demand For Low-Latency Decisioning At The Edge

The edge AI software market is also being pushed forward by use cases that require decisions in real time across manufacturing, autonomous systems, utilities, and public safety environments. Once latency budgets fall below 50 milliseconds, or site telemetry rises to 1 terabyte per day, local inference becomes a practical requirement rather than a design preference. NVIDIA and T-Mobile announced in March 2026 that they were integrating physical AI applications over distributed 5G edge networks with the NVIDIA Metropolis platform, including smart city operations, automated utility inspection, and industrial safety workloads where response speed is operationally critical. Hewlett Packard Enterprise also launched HPE AI Grid in March 2026 to deliver predictable low-latency performance across distributed inference sites, and Comcast began field trials for real-time edge inferencing on its network using small language models. The edge AI software market is therefore shifting toward platforms that can hold inference performance steady under constrained compute conditions, because average throughput on benchmark hardware matters less than deterministic behavior at the point of use.

Heterogeneous Edge Environment Integration Complexity

The edge AI software market still faces a major operational barrier because most enterprise deployments span different processor types, operating systems, and connectivity conditions. Research published in Sensors in 2026 on the MIGS architecture found that heterogeneous device integration requires protocol-agnostic middleware that can work across Modbus, OPC UA, and MQTT at the same time, which shows how difficult interoperability remains in real industrial settings. ZEDEDA's 2026 survey results also pointed to the same problem, with 41% of enterprises identifying distributed workload management as a primary challenge and 47% reporting the use of hybrid cloud-edge architectures that demand consistent governance across different hardware environments. This creates a split in the edge AI software market because large enterprises with standardized fleets can scale faster, while buyers with legacy operational technology face longer deployment cycles and higher integration costs. Until the sector develops a more universal hardware abstraction layer, interoperability will remain a structural drag on rollout speed and software standardization.

Other drivers and restraints analyzed in the detailed report include:

- Need For Privacy-Preserving On-Device Inference

- 5G-Enabled Distributed Application Architectures

- Model Optimization Limits On Constrained Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 62.72% of the edge AI software market share in 2025, which kept them in the leading position as enterprises favored integrated platforms over modular contracting models. That pattern reflects a practical buying preference because manufacturers, telecom operators, and other large users want validated packages that combine inference runtimes, compression tools, and deployment orchestration in one product. Buyers have generally preferred this route because it reduces interoperability uncertainty at the edge and lowers the burden of stitching together tools from different vendors. In the edge AI software market, that preference has given platform providers an early revenue advantage because they can sell a complete operating layer rather than only a narrow point capability. The same trend also shows that the edge AI software market has moved beyond trial deployments, since procurement teams usually standardize on bundled solutions only after internal teams see a clear path toward long-term operations.

Services are projected to expand at a 25.64% CAGR through 2031, and that pace is faster than the overall edge AI software market. That spread signals a change in how deployments are being managed after the initial software stack is installed. Enterprises are increasingly outsourcing edge MLOps, model optimization, lifecycle management, and fleet-wide observability because many do not have the internal engineering teams needed to manage model drift across distributed assets. Siemens made that transition more concrete in April 2026 when it announced broader availability for its Industrial AI Suite on Siemens Industrial Edge, covering model training, deployment, retraining, and AI model management across multiple factory sites. Google's expansion of LiteRT-LM support across iOS Swift, JavaScript, and Android APIs in 2026 showed a similar direction in mobile environments, where the runtime increasingly behaves like an embedded managed layer rather than a stand-alone software purchase.

The edge AI software market is therefore seeing a gradual blending of product and service economics, even if the two categories are still reported separately. Integrated solutions remain the first purchase for many enterprises, but service layers become more important once deployments move from pilots into full operations. That is especially visible among mid-market industrial users that installed edge hardware in 2023 and 2024 but still lack internal AI staffing depth. As a result, the edge AI software industry is developing toward lifecycle platforms that combine packaged software with ongoing operational support, rather than simple license-based software delivery.

Visual data accounted for 29.98% of revenue in 2025, making it the largest modality in the edge AI software market. That lead was built on years of computer vision deployment across factory inspection, security surveillance, and automotive perception systems. The installed global camera base continues to create a large demand reservoir because many endpoints still collect video that is not analyzed in real time. NVIDIA noted in 2026 that more than 1.5 billion cameras were installed globally and that less than 1% was being meaningfully analyzed in real time, which points to a large remaining opportunity for local visual inference frameworks. For the edge AI software market, this means visual workloads still anchor current revenue because they connect directly to established enterprise spending categories such as quality control, safety monitoring, and automated inspection.

Other data modalities are also expanding because end users are broadening the kinds of information they want to process locally. Text and language data support human-machine interfaces and local conversational functions, while environmental and location data are tied to monitoring, routing, and infrastructure use cases. Multimodal AI has become strategically important because enterprises increasingly want a single stack that can interpret several inputs at once without relying on separate models for each data stream. NVIDIA's Nemotron 3 Nano Omni model, released in May 2026, combined vision, language, and audio perception in one compact model designed for agentic edge workloads, which reflected this shift toward more unified inference architectures. The edge AI software market is gaining from this because multimodal models can simplify operational complexity when customers need richer local context but cannot support multiple full software stacks on constrained devices.

Auditory data is projected to grow at a 26.88% CAGR through 2031, which makes it the fastest-growing modality in the edge AI software market. The strongest demand is coming from audio anomaly detection in rotating machinery, voice-command interfaces in warehouse robotics, and conversational systems that need local responsiveness in healthcare and banking settings. Audio workloads also carry a cost advantage because the models are often smaller than comparable visual systems and can therefore run on more modest hardware footprints. That lowers deployment barriers for industrial original equipment manufacturers that already have installed MCU-class devices across large endpoint fleets. Over time, the edge AI software industry is likely to see auditory and multimodal use cases become more important because they offer practical performance gains without requiring the larger compute budgets that visual inference often demands.

Geography Analysis

North America held 34.78% of the edge AI software market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense concentration of hyperscaler platforms and industrial technology vendors, and that gives enterprise buyers earlier access to full-stack deployment options than most other regions. The edge AI software market also gains in North America from mature enterprise software procurement cycles, where large organizations are more willing to fund multi-site deployments after pilot validation. HPE's AI Grid launch in March 2026 and Comcast's field trials for distributed edge inferencing show that deployment activity is spreading beyond factories and into communications infrastructure and consumer service delivery networks. IBM's May 2026 launch of Sovereign Core also reflects a procurement environment where digital sovereignty and operational control are influencing both government and regulated enterprise demand.

Asia-Pacific is projected to expand at a 26.71% CAGR through 2031, which makes it the fastest-growing regional segment in the edge AI software market. That momentum is being supported by China's manufacturing scale, Japan's robotics and automotive programs, India's engineering base, and South Korea's semiconductor ecosystem. Nikkei reported in March 2026, citing Fuji Chimera Sogo Kenkyusho research, that AI agents and edge-based physical AI inference were expected to push market expansion in Japan from 2026 onward, with the edge environment gaining importance for both privacy protection and AI agent commercialization. This growth profile matters because the edge AI software market in Asia-Pacific is tied both to large industrial deployment volumes and to local design ecosystems that can embed AI functions closer to the device layer. It also means regional vendors and global suppliers are competing in a setting where cost efficiency, localization, and hardware alignment matter as much as software features.

Europe continues to hold a meaningful share of the edge AI software market because the region combines a strong industrial base with a regulatory environment that pushes buyers toward more controlled AI deployment models. Deutsche Telekom's European Edge Continuum moved into live lab and pre-production status in 2025 and continued toward commercial rollout in 2026, which supports Europe's digital sovereignty agenda through a federated and interoperable edge infrastructure layer. Cisco also highlighted Audi's Edge Cloud 4 Production deployment with Siemens at the Bollinger Hofe factory in March 2025, bringing virtualized software-defined automation and AI-driven process control into European automotive manufacturing. These examples show why the edge AI software market in Europe remains tied to industrial modernization, data control, and sovereign infrastructure priorities. South America, the Middle East and Africa, and Turkey are smaller in current scale, but they still matter because investment in agriculture, financial inclusion, smart cities, logistics, and energy control is creating selective demand for local AI execution. In those regions, adoption is often shaped by mobile-first connectivity and national digital infrastructure programs rather than by broad enterprise standardization.

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- International Business Machines Corporation

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies, Inc.

- Nutanix, Inc.

- Siemens AG

- Synaptics Incorporated

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Edge Impulse, Inc.

- ClearBlade, Inc.

- ZEDEDA, Inc.

- Viso AI AG

- Latent AI, Inc.

- Gorilla Technology Group Inc.

- PTC Inc.

- Renesas Electronics Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Internet of Things Endpoint Data

- 4.2.2 Demand for Low-Latency Decisioning at the Edge

- 4.2.3 Need for Privacy-Preserving On-Device Inference

- 4.2.4 5G-Enabled Distributed Application Architectures

- 4.2.5 Fleet-Scale Edge Model Operations and Orchestration

- 4.2.6 Certification-Ready Stacks for Safety-Critical Deployments

- 4.3 Market Restraints

- 4.3.1 Heterogeneous Edge Environment Integration Complexity

- 4.3.2 Model Optimization Limits on Constrained Devices

- 4.3.3 Certification Gaps for Regulated Deployments

- 4.3.4 Immature Benchmarking for Heterogeneous Software Stacks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Data Modality

- 5.2.1 Visual Data

- 5.2.2 Auditory Data

- 5.2.3 Text and Language Data

- 5.2.4 Environmental and Location Data

- 5.2.5 Multimodal Data

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premises

- 5.3.3 Hybrid

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Information Technology and Telecommunications

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Automotive and Transportation

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Energy and Utilities

- 5.4.7 Smart Cities and Public Infrastructure

- 5.4.8 Banking, Financial Services, and Insurance

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 NVIDIA Corporation

- 6.4.6 Intel Corporation

- 6.4.7 Qualcomm Technologies, Inc.

- 6.4.8 Nutanix, Inc.

- 6.4.9 Siemens AG

- 6.4.10 Synaptics Incorporated

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 Oracle Corporation

- 6.4.13 Edge Impulse, Inc.

- 6.4.14 ClearBlade, Inc.

- 6.4.15 ZEDEDA, Inc.

- 6.4.16 Viso AI AG

- 6.4.17 Latent AI, Inc.

- 6.4.18 Gorilla Technology Group Inc.

- 6.4.19 PTC Inc.

- 6.4.20 Renesas Electronics Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

邊緣人工智慧軟體市場-2026-2032年全球市場預測

邊緣人工智慧軟體市場-2026-2032年全球市場預測 邊緣人工智慧軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測

邊緣人工智慧軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測 2026-2030年全球邊緣人工智慧軟體市場

2026-2030年全球邊緣人工智慧軟體市場 邊緣人工智慧的現況:從「嵌入式世界 2026」中獲得的啟示

邊緣人工智慧的現況:從「嵌入式世界 2026」中獲得的啟示 邊緣人工智慧市場預測(視訊監控領域)至2034年:按組件、部署類型、企業規模、應用、最終用戶和地區分類的全球分析

邊緣人工智慧市場預測(視訊監控領域)至2034年:按組件、部署類型、企業規模、應用、最終用戶和地區分類的全球分析 2026年全球邊緣人工智慧軟體市場報告

2026年全球邊緣人工智慧軟體市場報告 全球邊緣人工智慧軟體市場評估:按產品、技術、資料模式和地區劃分,機會與預測(2018-2032 年)

全球邊緣人工智慧軟體市場評估:按產品、技術、資料模式和地區劃分,機會與預測(2018-2032 年) 邊緣人工智慧軟體市場規模、佔有率和成長分析(按組件、應用、設備類型、垂直產業和地區分類)-2026-2033年產業預測邊緣 AI 軟體市場更新:現有硬體供應商如何提升用戶參與度?

邊緣人工智慧軟體市場規模、佔有率和成長分析(按組件、應用、設備類型、垂直產業和地區分類)-2026-2033年產業預測邊緣 AI 軟體市場更新:現有硬體供應商如何提升用戶參與度? 全球邊緣人工智慧軟體市場:市場規模、佔有率、趨勢分析(按資料類型、提供的內容、產業和地區)、細分市場預測(2025-2030 年)

全球邊緣人工智慧軟體市場:市場規模、佔有率、趨勢分析(按資料類型、提供的內容、產業和地區)、細分市場預測(2025-2030 年)