|

市場調查報告書

商品編碼

2064461

GPU電源(PSU):市佔率分析、產業趨勢與統計數據以及成長預測(2026-2031)GPU Power Supply Unit (PSU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

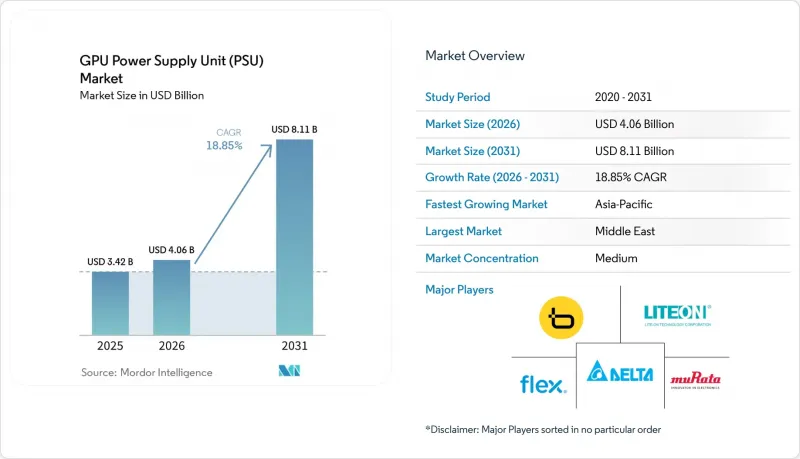

根據 Mordor Intelligence 預測,GPU 電源供應器 (PSU) 市場將從 2025 年的 34.2 億美元成長到 2026 年的 40.6 億美元,到 2031 年達到 81.1 億美元,2026 年至 2031 年的複合年成長率為 18.85%。

本報告按額定功率(低於 1kW、1-2kW、2-3kW、3-5kW、高於 5kW)、外形規格(CRPS、OCP PSU、超大規模資料中心業者專用及客製化設計)、最終用途(GPU 加速器伺服器、AI 推理伺服器、高效能運算系統)和地區(北美、南美、歐洲、亞太地區及其他地區)進行細分。市場預測以美元計價。

全球GPU電源(PSU)市場趨勢與洞察

人工智慧主導資料中心的激增

超大規模資料中心業者在2026年投入1,030億美元的資本支出,以支持已簽約的4.5吉瓦容量以及規劃中的9吉瓦容量,從而將併網週期從36個月縮短至18個月。 NVIDIA GB200 NVL72機架目前每個機櫃的功耗為120-140千瓦,迫使電源供應商從1-2千瓦的設計轉向直接連接到流體歧管的模組化5-10千瓦單元。維修現有設施不如新建設經濟,因為將一個傳統的10兆瓦資料中心升級到AI就緒密度需要花費每個設施300萬至400萬美元,而新建設需要1600萬美元,並且避免了熱設計方面的權衡。為了搶佔先機,供應商們正將庫存部署在維吉尼亞、德克薩斯州和新加坡的超大規模資料中心業者資料中心建設叢集附近。Delta電子透露,到 2025 年第四季度,人工智慧相關的電源將佔其伺服器電源銷售額的 50%。

基於GPU的高效能運算的快速普及

為了避免雲端資料傳輸成本,企業紛紛部署本地推理伺服器,企業級高效能運算叢集開始效法超大規模資料中心業者資料中心的架構。戴爾將於 2025 年 7 月推出的 PowerEdge XE7745 伺服器配備了內建的 3200 瓦 80 PLUS 鈦金認證電源,該電源針對雙 GPU 主機板進行了最佳化。測試期間,計算擴展導致每次查詢的功耗從 0.34 瓦時增加到 4.32 瓦時,迫使企業在不增加 GPU 數量的情況下將電源容量翻倍。 Flex 公司積極應對這一趨勢,並計劃於 2025 年在達拉斯、哥倫比亞和波蘭新增 113.4 萬平方英尺的產能,從而縮短客製化前置作業時間。雲端和企業規範的整合已將設計週期縮短至 12 個月,加速了供應商開發既符合開放運算專案 (OCP) 規範又符合專屬機架規範的互通平台。

氮化鎵組件供應鏈的變化

中國控制著全球98%的鎵產量,而2024年的出口限制已使現貨價格翻倍至2100美元/公斤,推高了高功率電源的物料清單成本。 Innoscience已將其8英寸晶圓的月產量擴大至15000片,良率達到97%,並與谷歌簽訂了契約,但中國以外的供應商面臨著突然禁運的風險。歐美供應商正在歐洲和北美聯合投資建設氮化鎵外延生產線,但商業規模生產仍需2-3年時間,因此價格波動預計將持續到2027年。

細分市場分析

預計到2025年,2-3千瓦級產品將佔GPU電源市場收入的42%,這表明它們與現有的208/240V配電系統和風冷方式相容。然而,隨著超大規模資料中心業者採用48V背板和液冷歧管來應對更高的熱負載,預計到2031年,功率超過5千瓦的電源將以20.04%的複合年成長率成長。 Navitas Semiconductor的12千瓦設計效率高達97.8%,為目前仍侷限於3.3千瓦晶片設計的廠商設定了目標上限。

由於3-5千瓦的電源與戴爾PowerEdge XE7745等雙GPU伺服器相容,因此升級推理叢集的公司傾向於選擇此類電源。雖然5千瓦以上GPU電源的市場主要集中在北美,但亞太地區的資料中心為了延後資本投資,正在將電源維修至2-3千瓦。 80 PLUS鈦金認證的成本(每個SKU 3500美元至8000美元不等)延緩了最高輸出範圍產品的上市,並給小規模供應商帶來了不成比例的負擔。

區域分析

預計到2025年,亞太地區仍將維持63%的銷售佔有率,主要得益於台灣垂直整合的供應鏈。在該地區,Delta電子、光寶科技和FSP集團合計佔全球產量的40%以上。Delta2025年第四季銷售額達1,616.1億新台幣(約51.1億美元),其中人工智慧電源佔其伺服器電源銷售額的50%。 InnoScience公司晶圓級氮化鎵生產確保了其原料的優先供應,使台灣組裝能夠提供比西方同行更短的前置作業時間。然而,隨著超大規模資料中心業者資料中心將設計流程內部化,OEM廠商的角色逐漸被限制在按圖生產,加劇了利潤率的壓力。

北美市場預計將以19.96%的複合年成長率成長,這主要得益於超超大規模資料中心業者的大規模投資和開發。這些公司目前正在建造35吉瓦的設施,並已與Brookfield簽訂了一份2026年至2030年期間10.5吉瓦的清潔能源供應合約。此外,杜克能源公司已撥款1,030億美元用於升級其電網,以滿足人工智慧(AI)應用日益成長的能源需求。 Flex公司於2025年擴大了其在美國的業務,新增了53.4萬平方英尺的生產空間,以響應市場對本地生產的日益成長的需求,從而降低地緣政治風險並確保供應鏈的韌性。

在歐洲和南美洲,資料中心的發展速度慢於北美,這主要是由於超大規模資料中心的數量較少以及環境許可法規更為嚴格。然而,歐洲的生態設計指令正在推動更節能環保的80 PLUS鈦金認證電源(PSU)的普及。相較之下,由於電網容量有限以及對進口組件的高度依賴等限制因素,中東和非洲仍處於發展初期。儘管面臨這些挑戰,沙烏地阿拉伯和阿拉伯聯合大公國等國的政府主導的人工智慧舉措正在加速建造第一批資料中心,這標誌著這些地區的資料中心發展已初見成效。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧主導資料中心的激增

- 基於GPU的高效能運算的快速普及

- 液冷機架架構的需求日益成長

- 利用數位雙胞胎技術整合電源單元監控

- 80 PLUS 鈦金及更高等級標準的強制性高效標準。

- 借助超大規模資料中心業者。

- 市場限制因素

- 氮化鎵(GaN)元件供應鏈的變化

- 功率輸出超過 5kW 時,溫度控管面臨挑戰。

- 維修舊式伺服器機架可行性的局限性

- 冗餘拓撲結構的高認證成本

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的額定輸出

- 1千瓦或以下

- 1~2kW

- 2~3kW

- 3~5kW

- 5千瓦或以上

- 按外形規格

- 通用冗餘電源(CRPS)

- Open Compute Project(OCP)PSU

- 專有設計和超大規模資料中心業者客製化設計

- 按最終用途

- GPU加速伺服器

- 人工智慧推理伺服器

- 高效能運算系統

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 其他

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Delta Electronics Inc.

- Lite-On Technology Corporation

- Flex Ltd.

- Zippy Technology Corp.

- Murata Manufacturing Co. Ltd.

- AcBel Polytech Inc.

- FSP Group

- Advanced Energy Industries Inc.

- CUI Inc.

- Sea Sonic Electronics Co. Ltd.

- Shenzhen Great Wall Technology Co. Ltd.

- Super Flower Computer Inc.

- Chicony Power Technology Co. Ltd.

- Bel Power Solutions and Protection

- TDK-Lambda Corporation

- Mean Well Enterprises Co. Ltd.

- Coolisys Technologies Corp.

- AsusTek Computer Inc.

- Enermax Technology Corporation

- Corsair Gaming Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the gPU power supply unit market size is expected to increase from USD 3.42 billion in 2025 to USD 4.06 billion in 2026 and reach USD 8.11 billion by 2031, growing at a CAGR of 18.85% over 2026-2031.

This report is Segmented by Output Power Rating (Up To 1 KW, 1-2 KW, 2-3 KW, 3-5 KW, and Above 5 KW), Form Factor (CRPS, OCP PSUs, and Proprietary and Hyperscaler Custom Designs), End Application (GPU Accelerator Servers, AI Inference Servers, and HPC Systems), and Geography (North America, South America, Europe, Asia-Pacific, and Rest of the World). Market Forecasts are Provided in Value (USD).

Global GPU Power Supply Unit (PSU) Market Trends and Insights

Surge in AI-Driven Data Centers

Hyperscalers committed USD 103 billion in 2026 capital expenditures to support 4.5 gigawatts of contracted capacity and a further 9 gigawatts in pipeline projects, accelerating grid interconnection timelines from 36 months to 18 months. NVIDIA GB200 NVL72 racks now draw 120-140 kilowatts per cabinet, compelling PSU vendors to move from 1-2 kilowatt designs to modular 5-10 kilowatt units that couple directly with liquid manifolds. Retrofit economics favor greenfield builds because upgrading a legacy 10-megawatt site to AI densities costs operators USD 3-4 million per facility, compared with USD 16 million for a new build that avoids thermal trade-offs. Vendors are staging inventory near hyperscaler construction clusters in Virginia, Texas, and Singapore to secure a first-mover advantage, and Delta Electronics disclosed that AI-related PSUs accounted for 50% of its server-PSU revenue in Q4 2025.

Rapid Adoption of GPU-Based High-Performance Computing

Enterprise HPC clusters are mirroring hyperscaler architectures as firms deploy on-premises inference servers to avoid cloud egress costs. Dell's PowerEdge XE7745, launched in July 2025, integrates a 3,200-watt 80 PLUS Titanium PSU tailored for dual-GPU boards. Test-time compute scaling lifted per-query energy from 0.34 Wh to 4.32 Wh, forcing enterprises to double PSU capacity without increasing GPU count. Flex Ltd backed the trend by adding 1.134 million ft2 of capacity across Dallas, Colombia, and Poland in 2025, shortening lead times for custom orders. The convergence of cloud and enterprise specifications is compressing design cycles to 12 months, encouraging vendors to develop interoperable platforms that satisfy both Open Compute Project and proprietary racks.

Supply Chain Volatility in Gallium Nitride Components

China controls 98% of global gallium output, and 2024 export curbs doubled spot prices to USD 2,100 kg-1, inflating BOM costs for high-power PSUs. Innoscience scaled wafer fabrication to 15,000 eight-inch units per month at 97% yields, locking in deals with Google but exposing non-Chinese vendors to sudden embargo risk. Western suppliers are co-funding gallium-nitride epi-lines in Europe and North America, but commercial scale remains two to three years away, maintaining price volatility through 2027.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Liquid-Cooled Rack Architectures

- Integration of Digital Twin-Enabled PSU Monitoring

- Thermal Management Challenges Above 5 kW Output

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 2-3 kilowatt category accounted for 42% of GPU power supply unit market revenue in 2025, underscoring its fit with existing 208/240 V power distribution and air cooling. Units above 5 kilowatts, however, are forecast to grow at a 20.04% CAGR through 2031 as hyperscalers standardize on 48 V backplanes and liquid manifolds to handle higher thermal loads. Navitas Semiconductor's 12-kilowatt blueprint validated 97.8% efficiency, establishing an aspirational ceiling for vendors still limited to 3.3-kilowatt silicon designs.

Enterprises upgrading inference clusters gravitate toward 3-5 kilowatt PSUs because they align with dual-GPU servers like Dell's PowerEdge XE7745. The GPU power supply unit market for the above-5-kilowatt tier is concentrated in North America, whereas Asia-Pacific data centers are retrofitting 2-3 kilowatt units to postpone capex. Certification costs under 80 PLUS Titanium, running USD 3,500-8,000 per SKU, delay launches in the highest-power bands, and disproportionately burden smaller vendors.

Geography Analysis

Asia-Pacific retained 63% revenue share in 2025, anchored by Taiwan's vertically integrated supply chain, where Delta Electronics, Lite-On Technology, and FSP Group collectively exceed 40% global output. Delta's Q4 2025 sales reached NTD 161.61 billion (USD 5.11 billion) with AI PSUs contributing 50% of server-power turnover. Innoscience's gallium nitride wafer-scale production secures priority access to raw materials, enabling Taiwanese assemblers to quote shorter lead times than their Western peers. Yet margin pressure is mounting as hyperscalers move design work in-house, relegating OEMs to build-to-print roles.

North America is projected to grow at a compound annual growth rate (CAGR) of 19.96% due to significant investments and developments by hyperscalers. These companies currently have 35 gigawatts of capacity under construction and have entered into a 10.5-gigawatt clean-energy agreement with Brookfield, which will span from 2026 to 2030. Additionally, Duke Energy has allocated USD 103 billion to grid upgrades to accommodate increasing energy demand driven by artificial intelligence (AI) applications. Flex Ltd expanded its U.S. operations in 2025 by adding 534,000 square feet of manufacturing space, addressing the growing preference for localized production to mitigate geopolitical risks and ensure supply chain resilience.

Europe and South America are experiencing slower growth than North America, primarily due to fewer hyperscale campuses and stricter environmental permitting regulations. However, Europe's Ecodesign Directive is driving the adoption of 80 PLUS Titanium power supply units (PSUs), which are more energy-efficient and environmentally friendly. In contrast, the Middle East and Africa regions remain in the early stages of development, constrained by limited grid capacity and a heavy reliance on imported components. Despite these challenges, sovereign AI initiatives in countries like Saudi Arabia and the United Arab Emirates are fostering the establishment of first-wave data centers, signaling the beginning of growth in these regions.

- Delta Electronics Inc.

- Lite-On Technology Corporation

- Flex Ltd.

- Zippy Technology Corp.

- Murata Manufacturing Co. Ltd.

- AcBel Polytech Inc.

- FSP Group

- Advanced Energy Industries Inc.

- CUI Inc.

- Sea Sonic Electronics Co. Ltd.

- Shenzhen Great Wall Technology Co. Ltd.

- Super Flower Computer Inc.

- Chicony Power Technology Co. Ltd.

- Bel Power Solutions and Protection

- TDK-Lambda Corporation

- Mean Well Enterprises Co. Ltd.

- Coolisys Technologies Corp.

- AsusTek Computer Inc.

- Enermax Technology Corporation

- Corsair Gaming Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI-Driven Data Centers

- 4.2.2 Rapid Adoption of GPU-Based High-Performance Computing

- 4.2.3 Growing Demand for Liquid-Cooled Rack Architectures

- 4.2.4 Integration of Digital Twin-Enabled PSU Monitoring

- 4.2.5 Increased Efficiency Mandates Under 80 PLUS Titanium and Beyond

- 4.2.6 Expansion of Hyperscaler In-House PSU Design Capabilities

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility in Gallium Nitride (GaN) Components

- 4.3.2 Thermal Management Challenges Above 5 kW Output

- 4.3.3 Limited Retrofit Viability in Legacy Server Racks

- 4.3.4 High Certification Costs for Redundant Topologies

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Output Power Rating

- 5.1.1 Up to 1 kW

- 5.1.2 1-2 kW

- 5.1.3 2-3 kW

- 5.1.4 3-5 kW

- 5.1.5 Above 5 kW

- 5.2 By Form Factor

- 5.2.1 Common Redundant Power Supply (CRPS)

- 5.2.2 Open Compute Project (OCP) PSUs

- 5.2.3 Proprietary and Hyperscaler Custom Designs

- 5.3 By End Application

- 5.3.1 GPU Accelerator Servers

- 5.3.2 AI Inference Servers

- 5.3.3 HPC Systems

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Delta Electronics Inc.

- 6.4.2 Lite-On Technology Corporation

- 6.4.3 Flex Ltd.

- 6.4.4 Zippy Technology Corp.

- 6.4.5 Murata Manufacturing Co. Ltd.

- 6.4.6 AcBel Polytech Inc.

- 6.4.7 FSP Group

- 6.4.8 Advanced Energy Industries Inc.

- 6.4.9 CUI Inc.

- 6.4.10 Sea Sonic Electronics Co. Ltd.

- 6.4.11 Shenzhen Great Wall Technology Co. Ltd.

- 6.4.12 Super Flower Computer Inc.

- 6.4.13 Chicony Power Technology Co. Ltd.

- 6.4.14 Bel Power Solutions and Protection

- 6.4.15 TDK-Lambda Corporation

- 6.4.16 Mean Well Enterprises Co. Ltd.

- 6.4.17 Coolisys Technologies Corp.

- 6.4.18 AsusTek Computer Inc.

- 6.4.19 Enermax Technology Corporation

- 6.4.20 Corsair Gaming Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球電化學絕緣市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電化學絕緣市場規模、佔有率、趨勢和成長分析報告(2026-2034年) DIN導軌電源市場:按輸出類型、效率等級、認證和應用分類 - 全球市場預測(2026-2032年)

DIN導軌電源市場:按輸出類型、效率等級、認證和應用分類 - 全球市場預測(2026-2032年) 2026年全球船舶和碼頭連接系統市場報告全球可程式電源市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026年全球船舶和碼頭連接系統市場報告全球可程式電源市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026-2030年全球交流電源系統市場氫電解整流器電源市場:按類型、技術類型、系統容量、配置、連接解決方案、電源系統、應用和最終用戶產業分類-2026年至2032年全球預測氫電解直流電源市場:2026年至2032年全球預測(按電解槽類型、額定功率、壓力、安裝方式、動作溫度、電壓範圍、應用和最終用戶產業分類)

2026-2030年全球交流電源系統市場氫電解整流器電源市場:按類型、技術類型、系統容量、配置、連接解決方案、電源系統、應用和最終用戶產業分類-2026年至2032年全球預測氫電解直流電源市場:2026年至2032年全球預測(按電解槽類型、額定功率、壓力、安裝方式、動作溫度、電壓範圍、應用和最終用戶產業分類) 電源供應器(PSU):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)單相DIN導軌電源市場依功率等級、輸出電壓、冷卻方式、連接器類型及最終用戶產業分類,全球預測,2026-2032年運算能力調度平台市場:全球預測(2026-2032 年),依技術應用、收入模式、部署模式、組織規模、垂直產業和應用領域分類

電源供應器(PSU):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)單相DIN導軌電源市場依功率等級、輸出電壓、冷卻方式、連接器類型及最終用戶產業分類,全球預測,2026-2032年運算能力調度平台市場:全球預測(2026-2032 年),依技術應用、收入模式、部署模式、組織規模、垂直產業和應用領域分類