|

市場調查報告書

商品編碼

2064441

全面薪酬平台:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Total Rewards Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

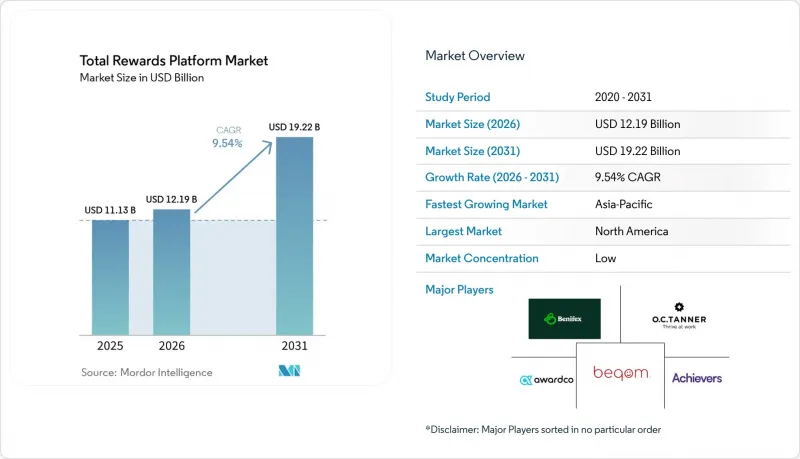

據 Mordor Intelligence 稱,2025 年全球獎勵平台市場總值達 111.3 億美元,預計從 2026 年到 2031 年將以 9.54% 的複合年成長率成長,到 2031 年達到 192.2 億美元。

本報告按部署類型(雲端部署和本地部署)、平台模組(績效與薪酬、薪酬管理、福利管理等)、組織規模(大型企業和中小企業)、最終用戶行業(銀行、金融服務、保險等)以及地區進行細分。市場預測以美元計價。

全球全面薪酬平台市場趨勢與洞察

對工資透明度和工資平等合規性的要求日益成長。

關於薪酬透明度的法律法規正從單純的聲譽問題轉變為營運要求,推動了對整體薪酬平台市場的直接投資。截至2026年4月,已有四個歐盟成員國將相關法規部分納入其國內法,另有九個成員國發布了立法草案,但員工人數超過150人的雇主仍需收集2026年的性別薪資差距數據,並於2027年6月前提交報告。至少有七個成員國,包括法國、丹麥和立陶宛,透過降低閾值或擴大雇主義務範圍,超越了指令的最低要求。這些差異促使跨國公司轉向實施能夠應用特定國家邏輯的薪酬差距校正模組,而不是依賴從人力資源資訊系統(HRIS)資料提取或手動報告等臨時解決方案。在美國,加州要求從2026年1月1日起將股票薪酬納入薪酬差距分析,這為薪酬數據管理增加了一個新的層面,而基本的薪資核算系統無法充分處理這一層面。這使得歐洲和北美地區對合規性主導的採購需求更加迫切,從而增強了全面薪酬平台市場的短期需求。

主導人工智慧技術實現薪資、福利和整體薪資的個人化和決策支援。

人工智慧在全面薪酬平台市場的影響最為顯著,體現在自動化薪酬差距監控、個人化福利指導和基於情境的薪酬規劃等方面。美世諮詢指出,人工智慧可以處理52%的薪酬相關交易,包括日常諮詢和標準福利管理任務。大型企業也採用以代理為基礎的系統,透過同時交叉比對市場基準、內部公平性數據和績效趨勢檢驗加薪方案,預計到2026年,採用率將達到48%。使用人工智慧驅動的績效評估工具的組織正在將年度考核週期從8-12週縮短至僅2週。然而,這些系統也帶來了管治風險,因為檢驗流程不足可能導致偏差的歷史薪酬資料繼續影響未來的建議。這催生了對「可解釋人工智慧」工具的新需求,這類工具能夠用簡單易懂的語言解釋薪酬決策背後的邏輯,並支援全面薪酬平台市場的人工監督。

整合原有的人力資源、薪資、保險和協作系統的複雜性。

在全面薪酬平台市場中,整合摩擦仍然是企業採用該平台的最大營運障礙。根據 Bindbee 數據顯示,68% 的企業仍在運行非整合的人力資源平台,與整合環境相比,這導致管理時間增加 23%,錯誤率高出 31%。 Lift HCM 的一項研究表明,一個擁有 150 名員工的企業每月在重複的管理任務上花費 51 小時,造成每年 21,420 美元的額外開銷。更大的挑戰在於持續的維護。擁有超過 20 個自訂整合的企業每年花費超過 50 萬美元,其中 60% 到 70% 的整合相關 IT 支出用於維護。由於安全審查和自訂欄位對應會延緩進度,Workday 的整合仍需要 1-3 週,SAP SuccessFactors 需要 2-4 週,而專有人力資源資訊系統 (HRIS) 的整合則需要 4-8 週。對於沒有專門整合團隊的中型企業而言,這種負擔尤其沉重,從而減緩了全面薪酬平台市場平台整合的進程。

細分市場分析

截至2025年,本地部署解決方案將佔整體薪酬平台市場佔有率的62.81%,這反映出企業更加重視長期契約,而非目前占主導地位的自管理系統。這項部署基礎是透過漫長的採購週期建立起來的,許多大型企業之所以繼續使用本地環境,是因為薪資核算、薪資和員工主資料高度客製化,難以遷移。預計到2031年,雲端部署將以12.36%的複合年成長率成長,成為整體薪資平台市場中成長最快的部署模式。這個時間節點至關重要,因為SAP將於2025年12月停止相容性支持,並計劃於2030年停止支持,這使得那些推遲遷移的雇主面臨著更緊迫的更新時間。此外,雲端基礎設施的可靠性也得到了提升,因為供應商可以在140多個國家/地區應用合規性更新,因此無需雇主手動管理當地法規的變更。

越來越多的雇主選擇混合部署模式,將核心員工記錄保留在本地,同時在雲端模組中運行獎勵計劃、勞動標準法 (LSA) 管理和薪資差距分析等功能。這種趨勢在受監管行業尤其明顯,這些行業既需要現代化的功能,又需要對敏感資料的儲存進行更嚴格的控制。這也意味著,全面薪酬平台產業並非簡單地從本地部署過渡到完全雲端,因為選擇性地採用雲端技術可以同時滿足合規性和營運需求。在歐洲和亞太部分地區,隨著 GDPR 和資料主權法規持續推動雲端技術的普及,混合模式可能仍將保持重要地位。

到2025年,獎勵與獎勵模組將佔據36.41%的市場佔有率,成為整體薪資平台市場中最大的模組。這是因為該模組通常是雇主選擇數位化的首選功能。雇主通常會優先實施認可計劃,因為這些計劃無需與獎勵系統深度整合即可啟動,並能立即展現員工的參與度和敬業度。此外,即使薪資預算面臨壓力,例如美國基於績效的平均加薪預算在2026年穩定在3.2%至3.6%,獎勵計畫仍是一種極具吸引力的低成本員工留任策略。預計到2031年,人力分析和降低薪資不平等模組的複合年成長率將達到11.21%,成為該模組組中成長最快的模組。這一成長速度主要受歐盟工資透明度法規的報告要求以及美國各州廣泛實施的工資相關立法的推動。

薪酬福利管理仍然是至關重要的中階。這是因為雇主希望使用統一的資料模型來管理績效評估計畫、員工登記流程和溝通工具,而不是將它們分散在不同的系統中。隨著採購負責人越來越要求薪資、福利和獎勵能夠協調運作,採購模式也正朝著捆綁式模式轉變。其餘模組(例如總薪酬報表、銷售績效管理、工作安排等)也在不斷發展,因為第一線經理在製定招聘和留任決策時需要最新的薪酬指南。所有這些模組的工作流程都涵蓋薪酬和醫療保險福利數據,因此安全性和審計管理現在從產品選擇階段就開始考慮,而不是作為實施後的IT審查。

區域分析

到2025年,北美將佔據全球薪酬平台市場佔有率的35.49%,成為最大的區域市場。美國仍是核心市場,到2026年,超過30%的美國國內勞動力將受到現行工資透明度法律的約束。隨著越來越多的州強制要求披露工資範圍和工資差距,這項法律範圍正在擴大。加拿大和墨西哥也在推動市場需求,儘管小規模。加拿大的聯邦工資平等框架持續鼓勵受監管的雇主採用薪酬分析工具。目前,北美地區正經歷著從單一合規工具向整合薪酬、福利、獎勵和分析功能的綜合套件的明顯轉變,這種綜合套件將整合到一個統一的工作流程中。

在歐洲,德國、英國和法國是主要參與者,這三個國家仍然是該地區最大的企業人力資本管理(HCM)市場。歐盟的《工資透明指令》透過強制報告工資差距、對超過5%的差距進行聯合工資評估以及更嚴格的工資保密規定,創造了短期採購需求。在德國,由於供應商需要遵守《一般資料保護規則》(DSGVO)、與DATEV薪資核算系統整合,並擁有能夠容納員工代表委員會(職工委員會)的流程,才能贏得當地企業客戶的青睞,因此在地化程度更高。在英國,需求仍然存在,因為即使在歐盟框架之外,擁有超過250名員工的雇主也必須強制報告性別薪資差距。

預計到2031年,亞太地區將以11.67%的複合年成長率成長,成為整體薪資平台市場成長最快的地區。印度的HR軟體市場預計將在2026年超過10億美元,而中國大型企業的數位轉型專案正在推動雲端薪資和獎勵工具的持續應用。日本的HR技術市場預計將在2026年達到18.2億美元,SmartHR於2025年6月發布的薪資核算功能表明,日本正在從人工流程轉向整合的人力資本管理(HCM)系統。南美、中東和非洲仍處於應用初期,其中巴西推動了福利管理的需求,沙烏地阿拉伯和阿拉伯聯合大公國促進了獎勵計畫的發展,而南非和奈及利亞則為跨國企業的部署提供了立足點。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 工資透明度提高,以及對工資平等合規性的需求日益成長

- 人力資源與薪資工作流程的雲端遷移

- 混合型和分散式勞動力:對數位化評估和自助式獎勵的需求日益成長

- 利用人工智慧技術實現薪資、福利和薪資方面的個人化和決策支援。

- 從分散的、獨立的工具過渡到整合的整體獎勵視覺化層。

- 透過生活風格消費帳戶和靈活的福利錢包擴大平台覆蓋範圍。

- 市場限制因素

- 將原有的人力資源、薪資、通訊業者和協作系統整合起來的複雜性。

- 資料隱私、人工智慧管治和跨境合規的重擔。

- 多邊稅收制度和賠償結算在地化帶來的複雜性。

- 本地人力資本管理套件的商品搭售以及專業供應商獲得市場佔有率的風險。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按實現類型

- 基於雲端的

- 本地部署

- 按平台模組

- 評估與補償

- 薪資管理

- 員工福利管理

- 人力資源分析與薪資差距調整

- 其他

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- 銀行及金融服務、保險

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Globoforce Limited(Workhuman)

- OC Tanner Company

- Achievers Solutions Inc.

- Awardco, Inc.

- Smartly, Inc.

- Bucketlist Rewards Inc.

- Kudos, Inc.

- Motivosity Inc.

- beqom SA

- Benifex Limited

- Perkbox Limited

- Benepass, Inc.

- Twic, Inc. DBA Forma

- Nayya Health, Inc.

- Bargain Technologies Private Limited

- Guusto Gifts Inc.

- WHAPPS LLC

- Benefitfocus.com, Inc.

- Businessolver

- Semos Cloud

第7章 市場機會與未來展望

According to Mordor Intelligence, the total rewards platform market size was valued at USD 11.13 billion in 2025 and is projected to reach USD 19.22 billion by 2031, at a CAGR of 9.54% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and On-Premises), Platform Module (Recognition and Rewards, Compensation Management, Benefits Administration, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Total Rewards Platform Market Trends and Insights

Rising Pay Transparency and Pay Equity Compliance Demand

Pay transparency legislation has moved from a reputational topic to an operating requirement, pushing direct investment across the total rewards platform market. As of April 2026, 4 EU member states had partial transpositions in force, and 9 more had published draft legislation, yet employers with 150 or more staff had to capture 2026 gender pay data for reporting due in June 2027. At least 7 member states, including France, Denmark, and Lithuania, were also moving beyond the Directive's minimum terms by lowering thresholds or widening employer obligations. That variation is pushing multinational employers toward pay equity modules that can apply country-specific logic, rather than relying on HRIS exports and manual reporting workarounds. In the United States, California's January 1, 2026, requirement to include equity awards in pay equity analysis has added another layer of compensation data management that basic payroll systems do not handle well. This is making compliance-led procurement more urgent in Europe and North America and is strengthening near-term demand in the total rewards platform market.

Artificial Intelligence-Driven Personalization and Decision Support Across Rewards, Benefits, and Compensation

AI is having its clearest effect in automated pay equity monitoring, personalized benefits guidance, and scenario-based compensation planning in the total rewards platform market. Mercer stated that AI can absorb 52% of transactional rewards workloads, including routine inquiries and standard benefits administration tasks. Large employers are also using agentic systems that test merit increase proposals against market benchmarks, internal equity data, and performance trends simultaneously, with adoption reaching 48% in 2026. Organizations using AI-assisted merit tools are shortening annual review cycles from 8-12 weeks to 2 weeks. The same systems create governance risk because biased historical pay data can continue to flow into future recommendations if testing controls are weak.That is creating fresh demand for explainable AI tools that can justify reward decisions in plain language and support human oversight across the total rewards platform market.

Legacy HR, Payroll, Carrier, and Collaboration-System Integration Complexity

Integration friction remains the clearest operating barrier to adoption in the total rewards platform market. Bindbee stated that 68% of organizations run disconnected HR platforms, leading to 23% more administrative time and 31% higher error rates than in unified environments. Lift HCM showed that a 150-employee organization can spend 51 hours each month on duplicate administrative work, which adds USD 21,420 in yearly overhead. The larger challenge is ongoing maintenance, because organizations with 20 or more custom integrations can spend more than USD 500,000 each year and direct 60%-70% of integration IT spend to upkeep. Integration timelines still run 1-3 weeks for Workday, 2-4 weeks for SAP SuccessFactors, and 4-8 weeks for proprietary HRIS estates, due to security reviews and custom field mapping that slow progress. This burden falls hardest on mid-market employers without dedicated integration teams, slowing platform consolidation in the total rewards platform market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration of HR and Rewards Workflows

- Hybrid and Distributed Workforces Increasing Need for Digital Recognition and Self-Service Rewards Access

- Data Privacy, Artificial Intelligence Governance, and Cross-Border Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises held 62.81% of the total rewards platform market share in 2025, reflecting the weight of long-running enterprise contracts over the current preference for self-managed systems. That installed base was built over long procurement cycles, and many large employers kept on-premises environments because payroll, rewards, and employee master data were deeply customized and difficult to move. Cloud-based deployment is projected to grow at a 12.36% CAGR through 2031, making it the fastest-growing deployment model in the total rewards platform market. The timing is important because SAP's December 2025 compatibility support expiry and its 2030 end-of-support path are creating specific renewal windows for employers that had delayed migration. Cloud infrastructure is also gaining credibility because vendors can push compliance updates across more than 140 countries without requiring each employer to manually manage local rule changes.

A growing number of employers are choosing a hybrid deployment, where core employee records remain on-premises while recognition, LSA administration, and pay equity analytics run in cloud modules. This pattern is especially visible in regulated sectors that want modern functionality but still need tighter control over sensitive data stores. It also means the total rewards platform industry is not moving in a straight line from on-premises to full cloud, because selective cloud adoption addresses compliance and operational needs simultaneously. In Europe and parts of Asia-Pacific, GDPR and data sovereignty rules will keep hybrid models relevant even as cloud adoption continues to rise.

Recognition and rewards held a 36.41% share in 2025, making it the largest module in the total rewards platform market, as it is often the first capability employers choose to digitize. Employers usually launch recognition first because it can go live without deep payroll integration and quickly show visible participation and engagement activity. Compressed salary budgets, with average US merit increase budgets stabilizing at 3.2%-3.6% for 2026, also kept recognition attractive as a lower-cost retention lever. People analytics and pay equity are projected to grow at a 11.21% CAGR through 2031, marking the fastest expansion within this module group. That pace is being driven by reporting requirements under EU pay transparency rules and by broader state-level pay legislation in the United States.

Compensation management and benefits administration remain important middle layers because employers want merit planning, enrollment, and communication tools to use the same data model rather than being split across separate systems. Procurement patterns are also shifting toward bundles, since buyers increasingly want compensation, benefits, and recognition to interact rather than sit in disconnected applications. The remaining module group, including total rewards statements, sales performance management, and workforce scheduling links, is growing, where frontline managers need current pay guidance during hiring and retention decisions. Across these modules, security and audit controls are becoming part of the product decision rather than a later IT review because the workflows span compensation and health benefits data.

Geography Analysis

North America held 35.49% of the total rewards platform market share in 2025, which made it the largest regional block. The United States remained the anchor market, with more than 30% of the national workforce covered by active pay transparency laws in 2026. That legal coverage is widening as more states finalize pay range disclosure and pay equity reporting mandates. Canada and Mexico added demand on a smaller scale, with Canada's federal pay equity framework continuing to support the adoption of compensation analytics among regulated employers. A clear regional shift is now underway from single-use compliance tools toward broader suites that integrate compensation, benefits, recognition, and analytics within a single workflow.

Europe is centered on Germany, the United Kingdom, and France, which remain the largest enterprise HCM markets in the region. The EU Pay Transparency Directive is creating a near-term procurement trigger by introducing mandatory pay gap reporting, joint pay assessments for gaps above 5%, and tighter rules on pay secrecy. Germany adds another layer of localization, as vendors need DSGVO compliance, DATEV payroll integration, and works council-ready processes to win local enterprise accounts. The United Kingdom still supports its own demand because employers with 250 or more workers remain subject to gender pay gap reporting outside the EU framework.

Asia-Pacific is projected to grow at a 11.67% CAGR through 2031, making it the fastest-growing geography in the total rewards platform market. India's HR software market is set to exceed USD 1 billion in 2026, while China continues to absorb cloud compensation and recognition tools through large-enterprise digitalization programs. Japan's HR technology market is expected to reach USD 1.82 billion in 2026, and SmartHR's June 2025 payroll calculation launch showed how the country is moving from manual processes to connected HCM systems. South America, the Middle East, and Africa remain earlier-stage adoption areas, with Brazil leading benefits administration demand, Saudi Arabia and the UAE supporting recognition growth, and South Africa and Nigeria serving as footholds for multinational rollout.

- Globoforce Limited (Workhuman)

- O.C. Tanner Company

- Achievers Solutions Inc.

- Awardco, Inc.

- Smartly, Inc.

- Bucketlist Rewards Inc.

- Kudos, Inc.

- Motivosity Inc.

- beqom SA

- Benifex Limited

- Perkbox Limited

- Benepass, Inc.

- Twic, Inc. DBA Forma

- Nayya Health, Inc.

- Bargain Technologies Private Limited

- Guusto Gifts Inc.

- WHAPPS LLC

- Benefitfocus.com, Inc.

- Businessolver

- Semos Cloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pay Transparency and Pay Equity Compliance Demand

- 4.2.2 Cloud Migration of HR and Rewards Workflows

- 4.2.3 Hybrid and Distributed Workforces Increasing Need for Digital Recognition and Self-service Rewards Access

- 4.2.4 Artificial Intelligence-driven Personalization and Decision Support Across Rewards, Benefits, and Compensation

- 4.2.5 Shift From Fragmented Point Tools to Unified Total Rewards Visibility Layers

- 4.2.6 Lifestyle Spending Accounts and Flexible Benefits Wallets Expanding Platform Scope

- 4.3 Market Restraints

- 4.3.1 Legacy HR, Payroll, Carrier, and Collaboration-system Integration Complexity

- 4.3.2 Data Privacy, Artificial Intelligence Governance, and Cross-border Compliance Burden

- 4.3.3 Multicountry Tax Treatment and Reward-fulfillment Localization Complexity

- 4.3.4 Native Human Capital Management Suite Bundling and Pure-play Displacement Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.2 By Platform Module

- 5.2.1 Recognition and Rewards

- 5.2.2 Compensation Management

- 5.2.3 Benefits Administration

- 5.2.4 People Analytics and Pay Equity

- 5.2.5 Other Platform Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Information Technology and Telecommunications

- 5.4.2 Banking, Financial Services, and Insurance

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Globoforce Limited (Workhuman)

- 6.4.2 O.C. Tanner Company

- 6.4.3 Achievers Solutions Inc.

- 6.4.4 Awardco, Inc.

- 6.4.5 Smartly, Inc.

- 6.4.6 Bucketlist Rewards Inc.

- 6.4.7 Kudos, Inc.

- 6.4.8 Motivosity Inc.

- 6.4.9 beqom SA

- 6.4.10 Benifex Limited

- 6.4.11 Perkbox Limited

- 6.4.12 Benepass, Inc.

- 6.4.13 Twic, Inc. DBA Forma

- 6.4.14 Nayya Health, Inc.

- 6.4.15 Bargain Technologies Private Limited

- 6.4.16 Guusto Gifts Inc.

- 6.4.17 WHAPPS LLC

- 6.4.18 Benefitfocus.com, Inc.

- 6.4.19 Businessolver

- 6.4.20 Semos Cloud

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

建築能源模擬軟體市場規模、佔有率和成長分析:按組件、部署模式、模擬類型、應用、建築類型、最終用戶和地區分類-2026-2033年產業預測

建築能源模擬軟體市場規模、佔有率和成長分析:按組件、部署模式、模擬類型、應用、建築類型、最終用戶和地區分類-2026-2033年產業預測 2026年上半年智慧建築新創公司-貫穿整個AEC/O生命週期的併購/投資/數位孿生/人工智慧新創企業

2026年上半年智慧建築新創公司-貫穿整個AEC/O生命週期的併購/投資/數位孿生/人工智慧新創企業 智慧建築市場:按組件、連接方式、部署方式、建築類型和最終用戶分類-2026-2032年全球市場預測

智慧建築市場:按組件、連接方式、部署方式、建築類型和最終用戶分類-2026-2032年全球市場預測 智慧建築市場規模、佔有率和趨勢分析報告:按組件、解決方案、服務、最終用途、地區和細分市場預測(2026-2033 年)

智慧建築市場規模、佔有率和趨勢分析報告:按組件、解決方案、服務、最終用途、地區和細分市場預測(2026-2033 年) 2026-2030年全球智慧建築市場

2026-2030年全球智慧建築市場 智慧幕牆市場-全球產業規模、佔有率、趨勢、機會、預測:依材料類型、技術、應用、地區和競爭格局分類,2021-2031年智慧建築市場-全球產業規模、佔有率、趨勢、機會與預測:按服務、解決方案類型、建築類型、地區和競爭格局分類,2021-2031年

智慧幕牆市場-全球產業規模、佔有率、趨勢、機會、預測:依材料類型、技術、應用、地區和競爭格局分類,2021-2031年智慧建築市場-全球產業規模、佔有率、趨勢、機會與預測:按服務、解決方案類型、建築類型、地區和競爭格局分類,2021-2031年 建築能耗模擬軟體市場:按組件、應用、最終用戶產業、部署模式、組織規模和地區分類

建築能耗模擬軟體市場:按組件、應用、最終用戶產業、部署模式、組織規模和地區分類 2026年全球智慧建築(非住宅建築)市場報告2026年全球辦公大樓市場報告

2026年全球智慧建築(非住宅建築)市場報告2026年全球辦公大樓市場報告