|

市場調查報告書

商品編碼

2064440

氣墊包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Air Cushion Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

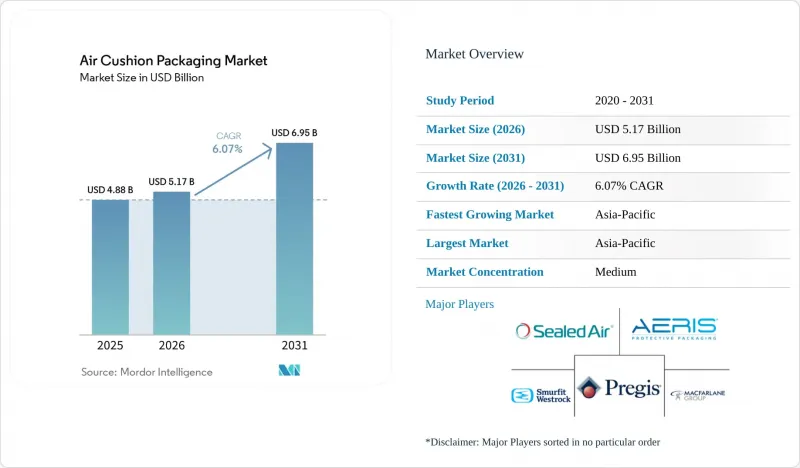

根據 Mordor Intelligence 預測,氣墊包裝市場規模將從 2025 年的 48.8 億美元成長到 2026 年的 51.7 億美元,到 2031 年將達到 69.5 億美元,2026 年至 2031 年的複合年成長率為 6.07%。

本報告按產品類型(空氣枕、氣泡墊、氣管)、材料類型(聚乙烯、聚丙烯、聚對苯二甲酸乙二醇酯等)、終端用戶行業(電子商務、消費電子、食品飲料、醫藥醫療設備、個人護理及化妝品、汽車等)和地區進行細分。市場預測以美元計價。

全球氣墊包裝市場趨勢及洞察

小包裹的不斷成長以及對防損的需求日益增加。

線上訂單量的成長仍然是氣墊包裝市場最強勁的需求來源。這是因為每次出貨量的增加都會產生新的運輸保護需求。隨著平均訂單價值的下降和出貨商品數量的減少,這種壓力反而加劇,因為與緊密包裝的多件商品訂單相比,鬆散包裝的瓦楞紙箱更容易在運輸過程中發生移動和損壞。因此,在產品損壞會立即導致退貨、更換成本和客戶服務費用的類別中,氣墊包裝市場的重要性更加凸顯。亞馬遜先前大量使用塑膠空氣枕,這表明在該公司轉向其他材料之前,中央充氣式填充材在大批量履約中發揮了重要作用。保護性包裝的成本遠低於逆向物流和產品流失的成本,因此對於能夠以更少的材料提供精準緩衝的供應商而言,它仍然具有經濟吸引力。在氣墊包裝市場,這不僅將需求與小包裹的成長聯繫起來,還將需求與避免大規模運輸網路中可預防的損壞的成本聯繫起來。

倉庫自動化和按需充氣技術的引入

倉庫自動化正在改變氣墊包裝市場在履約中心的運作方式,而不僅僅體現在材料使用上。一項針對2025年倉庫自動化的調查顯示,37%的受訪物流業者計畫將自動化作為一項核心營運改善措施,凸顯了市場對線上保護性包裝系統的持續關注。在實踐中,按需填充在自動化生產線上更受歡迎,因為它能減少儲存空間,降低使用前漏氣的風險,並使生產更貼合紙箱要求。 2025年9月,Storopack在其模組中新增了人工智慧視覺掃描功能,可在填充空氣或紙質緩衝材料之前計算空隙體積。這反映了市場朝著更高精度和減少廢棄物的方向發展。此外,氣墊包裝市場也受益於機器的普及通常會帶來耗材的持續採購。這提高了供應商的留存率,並降低了系統實施後轉換系統的成本。隨著履約公司擴大實現包裝站的自動化,能夠將硬體可靠性、軟體控制和薄膜性能整合到單一解決方案中的供應商,很可能在氣墊包裝市場中獲得優勢。

亞馬遜將在北美逐步淘汰塑膠氣墊

亞馬遜計劃在2024年中期前,將其北美地區95%的塑膠氣墊替換為100%再生紙填充材,並在2024年底前全面淘汰。預計這將使每年約20億件貨物的包裝中減少約150億個塑膠氣墊的使用。這表明,一家大型買家可以迅速調整其龐大履約網路中的材料需求,從而對氣墊包裝市場構成重大限制。這一轉變不僅影響了亞馬遜自身的採購,也迫使同一物流生態系統中的經銷商和服務合作夥伴調整其包裝選擇,使其與亞馬遜的政策保持一致。因此,儘管對保護性包裝材料的整體需求仍然存在,但氣墊包裝市場在北美地區發泡緩衝材料的龐大需求中所佔佔有率有所下降。亞馬遜已於2022年在歐洲和2020年在印度逐步淘汰了塑膠氣墊,這進一步表明,大型電商營運商可能會繼續減少對傳統塑膠氣墊的依賴。對於氣墊包裝市場而言,這凸顯了加快從依賴傳統 PE 氣墊過渡到可回收、紙質混合和其他符合監管規定的形式的必要性。

細分市場分析

到2025年,氣墊將佔據氣墊包裝市場55.34%的佔有率,顯著超越其他產品類型。其優勢在於:便於平放儲存、相容自動化線上灌裝以及具有優異的保護性能,且每立方英尺成本低廉,尤其適用於大批量運輸。氣墊包裝產業青睞這種包裝形式的另一個原因是,放氣後的薄膜卷比預充氣的包裝佔用占地面積更小,簡化了包裝站的操作人員補貨流程。主要供應商的專有機械系統進一步鞏固了其市場地位,因為客戶通常會成套購買硬體、薄膜和服務。這種強大的市場基礎確保了空氣枕在氣墊包裝市場中保持穩固的地位,即使材料偏好改變。

預計到2031年,氣泡墊將以6.75%的複合年成長率成長,成為氣墊包裝市場中成長最快的產品類型。其吸引力在於雙重用途:既可用作間隙填充材,又可用作表麵包裝材料,滿足運輸過程中對防刮擦和減震的需求。雖然氣管和充氣氣囊的銷售量仍然相對小規模,但它們在工業和醫療設備的運輸領域正日益受到重視,因為在這些領域,軸向載重分佈比簡單的間隙填充更為重要。 Storopack公司於2025年2月推出的「AIRfiber」也表明,氣墊包裝市場正在向紙基混合型產品轉型,模糊了傳統塑膠保護層和可回收紙質解決方案之間的界線。這種融合使品牌所有者能夠在保持緩衝性能的同時,使氣墊包裝適應更嚴格的可回收性要求。

區域分析

預計到2025年,亞太地區將以39.14%的市佔率引領氣墊包裝市場,並維持最高的成長率,到2031年複合年成長率將達到7.66%。該地區受益於大規模的製造地、活躍的出口活動以及廣泛的履約網路,這些因素持續推動多個產品類型對防護包裝的需求。中國憑藉其在線上零售物流和電子產品生產方面的規模,仍然是市場的主要貢獻者,既滿足了對標準間隙填充材的需求,也滿足了對更專業的充氣包裝的需求。印度正憑藉其製藥製造業、有組織的零售物流以及不斷擴大的國內包裝產能,成為重要的成長引擎。日本和韓國對電子和半導體相關運輸領域精密防護解決方案的穩定需求,使得氣墊包裝市場不僅與大批量履約需求緊密相連,也與高價值的工業應用息息相關。

北美仍然是氣墊包裝的第二大區域市場。雖然美國是該地區的中心,但亞馬遜計劃在2024年底前逐步淘汰北美地區的塑膠氣墊,這短期內對傳統塑膠緩衝材料的需求造成了不利影響,促使人們更加關注可回收且尺寸合適的替代品。同時,該地區仍然擁有大規模的物流網路,預計到2024年,美國、加拿大和墨西哥之間的貨運量將達到驚人的1.6兆美元,這為整個一體化分銷網路中輕質防護包裝材料的使用提供了支撐。墨西哥作為近岸外包中心也日益受到關注,為氣墊包裝市場創造了新的履約和包裝需求。

歐洲是受氣墊包裝市場法規影響最大的地區,因為PPWR 2025/40法規將改變包裝設計的優先順序和材料經濟性。德國仍然是歐洲的主要需求中心,而英國、法國和比荷盧經濟聯盟國家也是重要的市場,因為主要供應商已經在這些市場建立了密集的服務和分銷網路。歐盟委員會的指導意見明確指出,緩衝材料也將受到空間限制,這將促使客戶從2026年8月起轉向更精確的包裝系統和高度可回收的包裝形式。南美洲和中東及非洲雖然絕對規模仍然較小,但隨著供應商多元化經營到成熟的主要地區之外,這些地區也蘊藏著適度的成長機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 小包裹的不斷成長以及對防損的需求日益增加。

- 倉儲自動化和按需物流的普及

- 優先考慮減少貨物的重量和體積

- 含再生材料薄膜和可回收薄膜的創新

- 包裝站空間縮減和 SKU 合理化

- 針對尺寸合適的包裝操作,最佳化精確的空間填充。

- 市場限制因素

- 關注塑膠廢棄物及軟性薄膜回收利用面臨的挑戰

- 樹脂價格波動和設備更換成本

- 亞馬遜將在北美逐步淘汰塑膠空氣枕

- 歐盟空置空間與生產者責任延伸制度

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 空氣枕

- 氣泡墊

- 空氣管

- 材料類型

- 聚乙烯

- 聚丙烯

- 聚對苯二甲酸乙二酯

- 聚乳酸和澱粉的混合物

- 產業最終用途

- 食品/飲料

- 家用電子產品

- 電子商務

- 藥品和醫療設備

- 個人護理化妝品

- 室內設計和家具

- 車

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sealed Air Corporation

- Pregis LLC

- Storopack Hans Reichenecker GmbH

- Smurfit Westrock plc

- Intertape Polymer Group Inc.

- Veritiv Operating Company

- Macfarlane Group UK Ltd

- Airfil Protective Packaging Ltd.

- Inflatable Packaging, Inc.

- RAJAPACK SAS

- Kite Packaging Limited

- Dynaflex Private Limited

- Packman Packaging Private Limited

- Guangzhou PackBest Air Packaging Co., Ltd.

- Aeris Protective Packaging Inc.

- Shorr Packaging Corporation

- Advanced Protective Packaging Ltd.

- Polyair Inter Pack Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the air cushion packaging market size is expected to grow from USD 4.88 billion in 2025 to USD 5.17 billion in 2026 and is forecast to reach USD 6.95 billion by 2031 at 6.07% CAGR over 2026-2031.

This report is Segmented by Product Type (Air Pillows, Bubble Cushioning, and Air Tubes), Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, and More), End-Use Industry (E-Commerce, Consumer Electronics, Food and Beverages, Pharmaceutical and Medical Devices, Personal Care and Cosmetics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Air Cushion Packaging Market Trends and Insights

E-Commerce Parcel Growth and Damage Prevention Needs

Rising online order volumes remain the strongest demand base for the air cushion packaging market, as each additional shipment creates another need for transit protection. The pressure increases as basket sizes shrink and shipments contain fewer items, because loosely packed cartons are more prone to movement and breakage than dense multi-item orders. That makes the air cushion packaging market more relevant in categories where product damage quickly turns into returns, replacement costs, and customer service expenses. Amazon's earlier use of plastic air pillows at very large scale showed how central inflatable void-fill had become in high-throughput fulfillment before the company moved to another material path. The economic logic remains favorable for suppliers that can provide precise cushioning with low material use, because protective packaging still costs far less than reverse logistics and product loss. In the air cushion packaging market, this keeps demand tied not only to parcel growth itself but also to the cost of avoiding preventable damage in high-volume shipping networks.

Warehouse Automation and On-Demand Inflation Adoption

Warehouse automation is changing how the air cushion packaging market is deployed across fulfillment centers, not just how much material is used. A 2025 warehouse automation study indicated that 37% of surveyed logistics operators planned to implement automation as a core operational improvement, which supports continued interest in inline protective packaging systems. In practice, automated lines favor on-demand inflation because they reduce storage requirements, lower the risk of deflation before use, and allow output to more closely match carton requirements. Storopack expanded its module in September 2025 with AI-powered vision scanning that calculates void volumes before dispensing air or paper padding, which reflects the direction of the air cushion packaging market toward higher accuracy and lower waste. The air cushion packaging market also benefits from the fact that machine installations often lead to recurring consumable purchases, which strengthens supplier retention and raises switching costs after a system is in place. As more fulfillment operators automate pack stations, the air cushion packaging market is likely to reward suppliers that combine hardware reliability, software control, and film performance in a single offering.

Amazon's North America Plastic Air Pillow Phaseout

Amazon completed the replacement of 95% of plastic air pillows with 100% recycled paper filler in North America by mid-2024 and reached full elimination by the end of 2024, removing an estimated 15 billion plastic air pillows a year from around 2 billion shipments. This is a meaningful restraint on the air cushion packaging market because it shows that one large buyer can quickly reset material demand across a major fulfillment network. The transition also mattered beyond Amazon's own procurement because sellers and service partners inside the same logistics ecosystem faced pressure to align their own packaging choices with the platform's direction. The air cushion packaging market therefore lost part of a large-volume North American void-fill pool even though broader demand for protective packaging remained intact. Amazon had already phased out plastic air pillows in Europe in 2022 and in India in 2020, which reinforced the signal that large e-tailers may continue to reduce exposure to conventional plastic air formats. For the air cushion packaging market, this increases the urgency of shifting toward recyclable, paper-hybrid, and other compliance-friendly formats rather than relying on legacy PE air pillows.

Other drivers and restraints analyzed in the detailed report include:

- Recycled-Content and Recyclable Film Innovation

- Freight Weight and Cube Reduction Priorities

- EU Empty-Space and EPR Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air pillows held 55.34% of the air cushion packaging market share in 2025, which kept them well ahead of the other product types. Their lead came from flat-pack storage efficiency, compatibility with automated inline inflation, and a low cost-per-cubic-foot protection profile that remains attractive in high-volume fulfillment. The air cushion packaging industry also favors this format because deflated film rolls use far less floor space than pre-inflated stock, which helps operators simplify pack-station replenishment. Proprietary machine ecosystems from leading suppliers strengthen that position because customers often buy the hardware, film, and service model together. This installed base advantage keeps air pillows firmly embedded in the air cushion packaging market, even as material preferences evolve.

Bubble cushioning is projected to expand at 6.75% CAGR through 2031, making it the fastest-growing product category in the air cushion packaging market. Its appeal lies in its dual-use performance: it can serve as both void fill and surface wrap for shipments that require scratch protection and impact absorption. Air tubes and inflatable air bags remain smaller in revenue terms, but they are gaining ground in industrial equipment and pharmaceutical device transport where axial load distribution matters more than simple gap filling. Storopack's AIRfiber launch in February 2025 also showed that the air cushion packaging market is moving toward paper-based hybrid formats that blur the old line between inflatable plastic protection and recyclable paper solutions. That convergence gives brand owners a way to preserve cushioning performance while adapting the air cushion packaging market to stricter recyclability expectations.

Geography Analysis

Asia-Pacific led the air cushion packaging market with 39.14% revenue share in 2025 and is also expected to post the fastest regional CAGR at 7.66% through 2031. The region benefits from a large manufacturing base, robust export activity, and a broad e-commerce fulfillment network, which continues to drive demand for protective packaging across multiple product categories. China remains the central contributor because of its scale in online retail logistics and electronics production, which supports both standard void-fill demand and more specialized inflatable formats. India is becoming an important growth engine as pharmaceutical manufacturing, organized retail logistics, and domestic packaging capability continue to expand. Japan and South Korea add stable demand for precision protective solutions in electronics and semiconductor-related shipments, which keeps the air cushion packaging market tied to higher-value industrial uses as well as volume fulfillment demand.

North America remained the second-largest regional market for air cushion packaging. The United States anchors the region, but Amazon's full North American phaseout of plastic air pillows by the end of 2024 created a near-term headwind for conventional plastic void-fill demand and redirected attention toward recyclable and right-sized alternatives. At the same time, the region still offers a large logistics base, and US, Canada, and Mexico freight flows remained substantial at USD 1.6 trillion in 2024, which supports the use of lightweight protective formats across integrated distribution networks. Mexico is also gaining attention as a nearshoring hub, which adds new fulfillment and packaging demand nodes for the air cushion packaging market.

Europe is the geography most directly shaped by regulation in the air cushion packaging market because PPWR 2025/40 changes both packaging design priorities and material economics. Germany remains a leading European demand center, while the United Kingdom, France, and the Benelux countries continue to matter because major suppliers already have dense service and distribution coverage across those markets. The Commission's guidance makes it clear that void-fill materials count toward empty-space limits, which will push customers toward more precise packaging systems and higher-recyclability formats from August 2026 onward. South America and the Middle East and Africa remain smaller in absolute scale, but they still offer moderate growth opportunities as suppliers look for diversification beyond mature core regions.

- Sealed Air Corporation

- Pregis LLC

- Storopack Hans Reichenecker GmbH

- Smurfit Westrock plc

- Intertape Polymer Group Inc.

- Veritiv Operating Company

- Macfarlane Group UK Ltd

- Airfil Protective Packaging Ltd.

- Inflatable Packaging, Inc.

- RAJAPACK SAS

- Kite Packaging Limited

- Dynaflex Private Limited

- Packman Packaging Private Limited

- Guangzhou PackBest Air Packaging Co., Ltd.

- Aeris Protective Packaging Inc.

- Shorr Packaging Corporation

- Advanced Protective Packaging Ltd.

- Polyair Inter Pack Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Parcel Growth and Damage Prevention Needs

- 4.2.2 Warehouse Automation and On-Demand Inflation Adoption

- 4.2.3 Freight Weight and Cube Reduction Priorities

- 4.2.4 Recycled-Content and Recyclable Film Innovation

- 4.2.5 Pack-Station Space Compression and SKU Rationalization

- 4.2.6 Precision Void-Fill Optimization for Right-Sized Packaging Operations

- 4.3 Market Restraints

- 4.3.1 Plastic Waste Scrutiny and Flexible-Film Recycling Gaps

- 4.3.2 Resin Price Volatility and Equipment Switching Costs

- 4.3.3 Amazon's North America Plastic Air Pillow Phaseout

- 4.3.4 EU Empty-Space and EPR Rules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Air Pillows

- 5.1.2 Bubble Cushioning

- 5.1.3 Air Tubes

- 5.2 By Material Type

- 5.2.1 Polyethylene

- 5.2.2 Polypropylene

- 5.2.3 Polyethylene terephthalate

- 5.2.4 Polylactic Acid and Starch Blends

- 5.3 By End-Use Industry

- 5.3.1 Food and Beverages

- 5.3.2 Consumer Electronics

- 5.3.3 E-commerce

- 5.3.4 Pharmaceutical and Medical Devices

- 5.3.5 Personal Care and Cosmetics

- 5.3.6 Home Decor and Furnishings

- 5.3.7 Automotive

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sealed Air Corporation

- 6.4.2 Pregis LLC

- 6.4.3 Storopack Hans Reichenecker GmbH

- 6.4.4 Smurfit Westrock plc

- 6.4.5 Intertape Polymer Group Inc.

- 6.4.6 Veritiv Operating Company

- 6.4.7 Macfarlane Group UK Ltd

- 6.4.8 Airfil Protective Packaging Ltd.

- 6.4.9 Inflatable Packaging, Inc.

- 6.4.10 RAJAPACK SAS

- 6.4.11 Kite Packaging Limited

- 6.4.12 Dynaflex Private Limited

- 6.4.13 Packman Packaging Private Limited

- 6.4.14 Guangzhou PackBest Air Packaging Co., Ltd.

- 6.4.15 Aeris Protective Packaging Inc.

- 6.4.16 Shorr Packaging Corporation

- 6.4.17 Advanced Protective Packaging Ltd.

- 6.4.18 Polyair Inter Pack Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

氣墊包裝市場:全球市場預測,2026-2032年充氣包裝市場:2026-2032年全球市場預測(依材料、填充氣體類型、基材結構、應用、終端用戶產業及通路分類)

氣墊包裝市場:全球市場預測,2026-2032年充氣包裝市場:2026-2032年全球市場預測(依材料、填充氣體類型、基材結構、應用、終端用戶產業及通路分類) 植物纖維緩衝包裝市場預測至2034年—按纖維類型、形狀、應用、最終用戶和地區分類的全球分析環保運輸包裝市場預測至2034年-按產品類型、材料、功能、應用、最終用戶和地區分類的全球分析緩衝包裝市場預測—按產品類型、材料、最終用戶和地區分類的全球分析—2034年緩衝包裝解決方案市場預測至2034年-按產品類型、材料、最終用戶和地區分類的全球分析

植物纖維緩衝包裝市場預測至2034年—按纖維類型、形狀、應用、最終用戶和地區分類的全球分析環保運輸包裝市場預測至2034年-按產品類型、材料、功能、應用、最終用戶和地區分類的全球分析緩衝包裝市場預測—按產品類型、材料、最終用戶和地區分類的全球分析—2034年緩衝包裝解決方案市場預測至2034年-按產品類型、材料、最終用戶和地區分類的全球分析 全球緩衝材料市場:市場規模、佔有率、成長和行業分析:按材料類型、應用和地區預測(至2034年)

全球緩衝材料市場:市場規模、佔有率、成長和行業分析:按材料類型、應用和地區預測(至2034年) 氣墊包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,預測2026-2034年全球氣墊包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034)

氣墊包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,預測2026-2034年全球氣墊包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球氣墊包裝市場報告

2026年全球氣墊包裝市場報告