|

市場調查報告書

商品編碼

2064436

加密貨幣錢包:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Crypto Wallet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

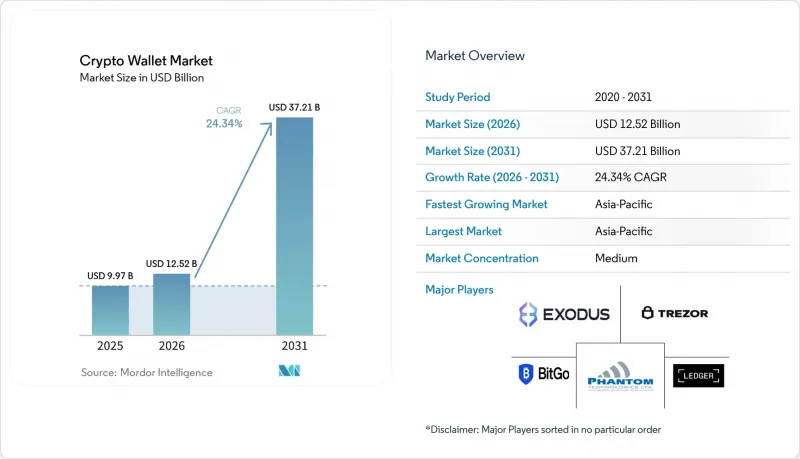

根據 Mordor Intelligence 預測,加密貨幣錢包市場規模將在 2025 年達到 99.7 億美元,2026 年達到 125.2 億美元,2031 年達到 372.1 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 24.34%。

本報告按錢包類型(熱錢包和冷錢包)、應用領域(交易、P2P支付、匯款、商家支付和電子商務、DeFi和Web3接入)、最終用戶(個人用戶、企業、加密貨幣原生機構、金融機構和金融科技公司、商家和支付服務提供者、其他)以及地區進行細分。市場預測以美元(USD)為單位。

全球加密貨幣錢包市場趨勢及洞察

擴大 DeFi 和 Web3 的參與度

DeFi 是推動加密貨幣錢包需求成長的主要結構性因素,因為錢包已成為進行代幣化資產兌換、質押、流動性提供和存取的主要介面。隨著透過錢包整合執行的交易與更廣泛的鏈上金融活動和各種應用相連接,其活動不再局限於實驗性的個人用途。到 2025 年,透過錢包提供者進行的嵌入式兌換交易將顯著增加,這將強化錢包的作用,使其不再只是被動的儲存工具,而是成為交易層。到 2025 年,代幣化的現實世界資產也將迅速成長,凸顯了對支援合規所有權、可審計轉帳和直接用戶管理的託管介面的需求。隨著越來越多的用戶直接從錢包環境存取 DeFi,加密貨幣錢包市場有望透過兌換、路由和高級安全功能獲得更強勁的獲利機會。這就是為什麼隨著錢包原生執行方式相對於交易所原生執行方式獲得更大佔有率,加密貨幣錢包市場持續受益的原因。

機構投資者和金融部門的招聘人數增加

機構投資者的購買是加密貨幣錢包市場的主要驅動力。這是因為財務部門使用加密貨幣錢包需要比個人投資者交易更嚴格的控制系統。到2026年,上市公司的參與度將進一步提高,僅Strategy Inc.一家公司截至2026年5月11日就持有818,869枚比特幣。這表明,財務部門規模的採用可以如何改變錢包需求和託管架構。根據Coinbase在2025年發布的一項調查,超過75%的受訪者計劃在2025年增加其數位資產配置,84%的受訪者已經在使用穩定幣或考慮採用。這表明對受監管的錢包基礎設施的需求正在成長。機構投資者的需求正在從簡單的冷熱錢包分離發展到多方運算、策略控制和受監管的結算連接,這提升了企業錢包平台的價值。美國會計和託管方面的監管變化也在擴大銀行和授權提供者的基本客群,為加密貨幣錢包市場帶來更大的長期發展機會。隨著這些買家進入市場,加密貨幣錢包市場正在從純粹的功能主導轉變為服務主導和合規主導。

私鑰和助記詞的複雜性

管理私鑰和助記詞仍然是加密貨幣錢包市場的一大障礙,因為資金恢復仍然依賴許多消費者不熟悉的用戶行為。風險不僅限於技術難度,還包括因簡單錯誤或不當備份操作而導致的永久性損失。 2025年,ThreatFabric發布了名為「Crocodilus」的安卓惡意軟體,該軟體利用虛假的緊急備份提示誘騙用戶在受感染的裝置上直接洩露錢包助記詞。為了應對這個問題,加密貨幣錢包市場正在向帳戶抽象、智慧錢包和恢復模型轉型,以減少用戶直接處理助記詞的需求。根據Ethereum.org預測,到2026年4月,將有超過2,600萬個ERC-4337智慧錢包部署,用戶操作次數將超過1.7億次。這項轉型需要時間,因為現有用戶需要重新培訓,而新用戶則需要從頭開始學習不同的安全模型。在這項轉型普及之前,加密貨幣錢包市場在易用性方面可能仍會受到經驗不足用戶的限制。

細分市場分析

預計到 2025 年,熱錢包將佔加密貨幣錢包總收入的 56.23%,繼續主導加密貨幣錢包市場,成為日常交易、DeFi 存取和頻繁兌換的最便捷選擇。這種主導地位反映了用戶在需要即時執行、dApp 連接和便利的資產組合轉移時,仍然傾向於使用連網錢包。行動端、網頁端和桌面端熱錢包仍然服務於不同的用戶群體,行動端更適合日常交易,而瀏覽器整合設定則更適合高級 DeFi 活動。便利性優勢依然顯著,這也是為什麼熱錢包在加密貨幣錢包產業擁有最廣泛商業性覆蓋率的原因。此外,錢包原生交易的成長也使熱錢包受益,用戶現在無需返回中心化交易所介面即可進行兌換、橋接和協議互動。

冷錢包是成長最快的類型,預計到2031年,冷錢包加密貨幣錢包市場將以25.74%的複合年成長率成長。這一成長反映了機構投資者財務部門的採購、對交易對手風險日益成長的敏感性,以及持有更大餘額且持有時間更長的用戶的需求不斷成長。 Strategy Inc.財務部門的分析強調了為什麼大額擁有者越來越依賴冷藏保管架構來進行資產隔離和授權控制。硬體供應商在2025年推出了更先進的產品,例如Ledger Nano Gen5和Trezor Safe 7,進一步推動了安全性和易用性的提升,使其成為主流。混合模式(軟體錢包處理日常交易,硬體簽名設備保護儲備)現在很常見,這重塑了加密貨幣錢包市場在設備和軟體層面的獲利模式。紙錢包仍然是少數,由於其檢驗能力有限、易用性差以及與當前合規要求的兼容性低,其市場佔有率正在不斷萎縮。

區域分析

預計到2025年,亞太地區將佔據加密貨幣錢包市場36.81%的佔有率,同時也是成長最快的地區,預計到2031年複合年成長率將達到25.24%。這顯示亞太地區的加密貨幣錢包市場成長並非源自於較小的基數,而是源自於用戶廣泛且深厚的需求。印度在2025年全年保持全球加密貨幣普及率的領先地位,其鏈上交易量高達3,380億美元,鞏固了其主導地位。日本和韓國由於監管的進步、交易頻率的提高以及穩定幣使用量的增加,推動了該地區錢包的普及,並創造了新的需求領域。巴基斯坦和越南也正朝著2025年正式承認加密貨幣錢包的方向發展,這將支持該地區在行動優先、匯款需求旺盛的市場中迎來下一波錢包普及浪潮。綜上所述,這些因素確保了亞太地區在加密貨幣錢包市場中繼續保持核心地位,無論對於個人用戶還是專業用戶都是如此。

在2025年和2026年,北美和歐洲仍然是機構投資者對加密貨幣錢包市場的主要需求中心。在北美,美國受益於穩定幣和市場結構方面更清晰穩定的發展方向,這在一定程度上緩解了人們對託管整合和監管准入的疑慮。 Strategy Inc.在2026年5月發布的一份報告指出,摩根士丹利、高盛和花旗集團等主要銀行宣布提供比特幣交易、託管和借貸服務,反映出相關設施的營運環境更加規範化。在歐洲,2026年《加密資產行銷條例》(MiCA)的全面實施及其相關報告規則加強了許可、記錄保存和資訊揭露要求,提高了服務提供者的營運門檻。這使得規模更大、資本更雄厚的公司獲得了競爭優勢,歐洲加密貨幣錢包市場正在逐步重組,形成數量更少、合規性更高的服務提供者格局。

在南美洲、中東和非洲,加密貨幣錢包市場呈現不同的需求結構。穩定幣在資金安全、商家支付和跨境匯款方面發揮越來越重要的作用。在南美洲,該地貨幣的普及;一項由某聯盟開展的研究表明,使用與美元掛鉤的穩定幣的哥倫比亞公司能夠顯著降低通貨膨脹造成的損失。同時,在阿根廷,USDC佔據了穩定幣交易量的很大佔有率。巴西也正在透過實施《虛擬資產法》來改善其商業環境,該法案將於2025年生效,屆時將允許錢包提供商擴大市場參與企業範圍。在中東和非洲,阿拉伯聯合大公國正將自身打造成為高階支付中心,而在撒哈拉以南非洲地區,受1萬美元以下小額匯款的推動,預計到2025年,鏈上交易量將年增超過50%。這些地區整體上正在擴大加密貨幣錢包市場,不僅透過交易需求,而且透過實際的支付案例。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大對 DeFi 和 Web3 的參與

- 機構投資人和財政部的採用率提高

- 利用穩定幣的匯款和支付服務

- 以行動優先的用戶註冊流程,並將支付管道從法定貨幣擴展到加密資產。

- 透過帳戶抽象化和無種子恢復來改善用戶體驗

- 對人工智慧代理和機器錢包的需求

- 市場限制因素

- 私鑰和助記詞的複雜性

- 網路釣魚、資料竊取和錢包盜用案件呈現上升趨勢。

- 分散式自我管理合規和旅行規則帶來的負擔

- 硬體錢包成本上漲和安全元件供應風險

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 錢包類型

- 熱錢包

- 冷錢包

- 透過使用

- 交易

- P2P支付

- 匯款

- 商戶支付與電子商務

- 存取 DeFi 和 Web3

- 最終用戶

- 個人用戶

- 公司

- 加密貨幣原生機構

- 金融機構及金融科技公司

- 商家和支付服務提供者

- Web3 工作室和開發人員

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ledger SAS

- Trezor Company sro

- Exodus Movement, Inc.

- Zengo Ltd.

- Phantom Technologies, Inc.

- ARGENT LABS LIMITED

- Zerion, Inc.

- SafePal LTD

- Tangem AG

- Shift Crypto AG

- Coinkite Inc.

- CoolBitX Ltd.

- ELLIPAL LIMITED

- Horkos, Inc.

- IoTrust Co., Ltd.

- ONEKEY LIMITED

- Yanssie HK Limited

- BitGo, Inc.

- Fireblocks Inc.

- Cobo Global Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the crypto wallet market size is projected to be USD 9.97 billion in 2025, USD 12.52 billion in 2026, and reach USD 37.21 billion by 2031, growing at a CAGR of 24.34% from 2026 to 2031.

This report is Segmented by Wallet Type (Hot Wallets, and Cold Wallets), Application (Trading, Peer-To-Peer Payments, Remittance, Merchant Payments and E-Commerce, and DeFi and Web3 Access), End-User (Individual Users, Enterprises, Crypto-Native Institutions, Financial Institutions and Fintechs, Merchants and Payment Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Crypto Wallet Market Trends and Insights

Expanding DeFi and Web3 Participation

DeFi has become a major structural driver of demand for the crypto wallet market, as wallets are now the primary interfaces for swaps, staking, liquidity provision, and access to tokenized assets. Activity is no longer concentrated in experimental retail use, as wallet-linked execution is increasingly tied to broader on-chain financial activity and a wider set of applications. Embedded swap activity via wallet providers rose meaningfully in 2025, reinforcing the wallet's role as a transaction layer rather than a passive storage tool. Tokenized real-world assets also expanded sharply by 2025, underscoring the need for custody interfaces that support compliant ownership, auditable movement, and direct user control. As more users interact with DeFi directly from wallet environments, the crypto wallet market is seeing stronger monetization opportunities through swaps, routing, and premium security features. This is why the crypto wallet market continues to benefit when wallet-native execution gains share relative to exchange-native execution.

Rising Institutional and Treasury Adoption

Institutional buying has become a major driver of the crypto wallet market because treasury use requires stronger controls than consumer trading. Public company participation widened further by 2026, and Strategy Inc. alone held 818,869 BTC as of May 11, 2026, which illustrates how treasury-scale adoption can reshape wallet demand and custody architecture. A Coinbase institutional survey released in 2025 found that more than 75% of respondents planned to increase their digital asset allocations in 2025, and 84% were already using or considering stablecoins, pointing to broader demand for regulated wallet infrastructure. The institutional requirement is moving beyond simple hot-and-cold separation toward multi-party computation, policy controls, and regulated settlement connectivity, which raises the value of enterprise wallet platforms. U.S. accounting and custody changes also widened the addressable base for banks and licensed providers, which supports a larger long-term opportunity for the crypto wallet market. As these buyers enter, the crypto wallet market is becoming more service-led and compliance-led, not only feature-led.

Private Key and Seed Phrase Complexity

Private key and seed phrase management remains a basic friction point for the crypto wallet market because fund recovery still depends on user behavior that feels unfamiliar to most consumers. The risk is not only technical difficulty but also the permanent loss scenario that can result from a simple mistake or poor backup practices. ThreatFabric disclosed the Crocodilus Android malware in 2025, and the attack used fake urgent backup prompts to trick users into revealing wallet phrases directly on compromised devices. In response, the crypto wallet market is moving toward account abstraction, smart wallets, and recovery models that reduce direct phrase handling, and Ethereum.org reported more than 26 million ERC-4337 smart wallet deployments with over 170 million UserOperations by April 2026. Even so, migration takes time because existing users must be re-educated while new users must learn a different security model from the start. Until that transition becomes more standard, the crypto wallet market will continue to face a usability ceiling among less experienced users.

Other drivers and restraints analyzed in the detailed report include:

- Stablecoin-Based Remittance and Payments Utility

- Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion

- Rising Phishing, Drainers, and Wallet Exploits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot wallets accounted for 56.23% of revenue in 2025, keeping them at the center of the crypto wallet market as the most practical option for daily trading, DeFi access, and frequent swaps. Their lead reflects the continued preference for internet-connected wallets when users need immediate execution, dApp connectivity, and simple portfolio movement. Mobile, web, and desktop hot wallets each still serve distinct user groups, with mobile favored for daily transfers and browser-linked setups preferred for deeper DeFi activity. The convenience advantage remains strong, which is why hot wallets have maintained the broadest commercial reach in the crypto wallet industry. Hot wallets also benefit from wallet-native transaction growth, as users can now swap, bridge, and interact with protocols without returning to centralized exchange interfaces.

Cold wallets are the fastest-growing type, with the crypto wallet market size for cold wallets projected to expand at a 25.74% CAGR through 2031. That growth reflects institutional treasury buying, higher sensitivity to counterparty risk, and stronger demand from users holding larger balances for longer periods. Strategy Inc.'s treasury position highlights why large holders increasingly depend on cold storage architecture for asset segregation and approval control. Hardware providers responded with more advanced products in 2025, including Ledger Nano Gen5 and Trezor Safe 7, both of which pushed security and usability improvements further into the mainstream. A hybrid model is now common, in which software wallets handle daily activity and hardware signers protect reserve balances, reshaping how the crypto wallet market is monetized across device and software layers. Paper wallets remain a minor and declining niche because they offer limited verification, poor usability, and little alignment with current compliance expectations.

Geography Analysis

Asia-Pacific held 36.81% of the crypto wallet market share in 2025 and is also the fastest-growing region, with a 25.24% CAGR through 2031. That combination shows that the crypto wallet market in Asia-Pacific is not growing from a small base, but from deep and broad user demand. India remained the global leader in crypto adoption through 2025, and the country also recorded USD 338 billion in on-chain transaction volume, which supported its leading position. Japan and South Korea added a different layer of demand, with regulatory progress, high trading intensity, and stronger stablecoin usage supporting regional wallet activity. Pakistan and Vietnam also moved toward more formal policy recognition in 2025, which supports the next wave of regional wallet adoption in remittance-heavy and mobile-first markets. This mix keeps Asia-Pacific at the center of the crypto wallet market across both retail and professional use.

North America and Europe remained the main poles of institutional demand in the crypto wallet market during 2025 and 2026. In North America, the United States benefited from clearer, more stable direction on stablecoins and market structure, which reduced some of the hesitation around custody integration and regulated access. Strategy Inc.'s May 2026 filing noted that major banks, including Morgan Stanley, Goldman Sachs, and Citigroup, had announced bitcoin trading, custody, and lending services, reflecting a more normalized institutional environment. In Europe, full MiCA enforcement in 2026 and related reporting rules raised the operating bar for providers by increasing authorization, record-keeping, and disclosure requirements. That favors larg, nd better-capitalized firms gradually reshaping the crypto wallet market in Europe toward fewer providers with stronger compliance capacity.

South America, the Middle East, and Africa added a different demand profile to the crypto wallet market, with stablecoins playing a more functional role in treasury preservation, merchant settlement, and cross-border transfers. South American adoption is supported by local-currency pressure, and a consortium study showed that Colombian companies using USD-pegged stablecoins materially reduced inflation losses on treasury funds, while USDC captured a large share of stablecoin volume in Argentina. Brazil also improved the operating environment in 2025 through secondary rules under its Virtual Assets Law, which enabled wallet providers to gain greater market participation. In the Middle East and Africa, the UAE is positioning itself as a premium institutional hub, while sub-Saharan Africa recorded more than 50% year-over-year growth in on-chain transaction volumes in 2025, led by retail transfers below USD 10,000. Together, these regions are expanding the crypto wallet market through practical payment use cases rather than solely on trading demand.

- Ledger SAS

- Trezor Company s.r.o.

- Exodus Movement, Inc.

- Zengo Ltd.

- Phantom Technologies, Inc.

- ARGENT LABS LIMITED

- Zerion, Inc.

- SafePal LTD

- Tangem AG

- Shift Crypto AG

- Coinkite Inc.

- CoolBitX Ltd.

- ELLIPAL LIMITED

- Horkos, Inc.

- IoTrust Co., Ltd.

- ONEKEY LIMITED

- Yanssie HK Limited

- BitGo, Inc.

- Fireblocks Inc.

- Cobo Global Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding DeFi and Web3 Participation

- 4.2.2 Rising Institutional and Treasury Adoption

- 4.2.3 Stablecoin-Based Remittance and Payments Utility

- 4.2.4 Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion

- 4.2.5 Account Abstraction and Seedless Recovery Reducing User Friction

- 4.2.6 AI-Agent and Machine-Wallet Demand

- 4.3 Market Restraints

- 4.3.1 Private Key and Seed Phrase Complexity

- 4.3.2 Rising Phishing, Drainers, and Wallet Exploits

- 4.3.3 Fragmented Self-Custody Compliance and Travel Rule Burden

- 4.3.4 Hardware Wallet Cost Inflation and Secure-Element Supply Risk

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wallet Type

- 5.1.1 Hot Wallets

- 5.1.2 Cold Wallets

- 5.2 By Application

- 5.2.1 Trading

- 5.2.2 Peer-To-Peer Payments

- 5.2.3 Remittance

- 5.2.4 Merchant Payments and E-Commerce

- 5.2.5 DeFi and Web3 Access

- 5.3 By End-User

- 5.3.1 Individual Users

- 5.3.2 Enterprises

- 5.3.3 Crypto-Native Institutions

- 5.3.4 Financial Institutions and Fintechs

- 5.3.5 Merchants and Payment Providers

- 5.3.6 Web3 Studios and Developers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ledger SAS

- 6.4.2 Trezor Company s.r.o.

- 6.4.3 Exodus Movement, Inc.

- 6.4.4 Zengo Ltd.

- 6.4.5 Phantom Technologies, Inc.

- 6.4.6 ARGENT LABS LIMITED

- 6.4.7 Zerion, Inc.

- 6.4.8 SafePal LTD

- 6.4.9 Tangem AG

- 6.4.10 Shift Crypto AG

- 6.4.11 Coinkite Inc.

- 6.4.12 CoolBitX Ltd.

- 6.4.13 ELLIPAL LIMITED

- 6.4.14 Horkos, Inc.

- 6.4.15 IoTrust Co., Ltd.

- 6.4.16 ONEKEY LIMITED

- 6.4.17 Yanssie HK Limited

- 6.4.18 BitGo, Inc.

- 6.4.19 Fireblocks Inc.

- 6.4.20 Cobo Global Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

加密貨幣錢包市場-2026-2032年全球市場預測

加密貨幣錢包市場-2026-2032年全球市場預測 加密貨幣錢包市場規模、佔有率和趨勢分析報告:按錢包類型、作業系統、應用程式、最終用戶、地區和細分市場預測(2026-2033 年)

加密貨幣錢包市場規模、佔有率和趨勢分析報告:按錢包類型、作業系統、應用程式、最終用戶、地區和細分市場預測(2026-2033 年) 全球加密貨幣錢包市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球加密貨幣錢包市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球加密貨幣錢包市場預測(至2034年):按類型、技術/功能、作業系統、應用程式、最終用戶和地區分類

全球加密貨幣錢包市場預測(至2034年):按類型、技術/功能、作業系統、應用程式、最終用戶和地區分類 加密貨幣錢包市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用途、應用、地區和競爭格局分類,2021-2031年)企業加密貨幣錢包市場按錢包類型、部署類型、組織規模、分銷管道、資產類型和行業垂直領域分類,全球預測,2026-2032年

加密貨幣錢包市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用途、應用、地區和競爭格局分類,2021-2031年)企業加密貨幣錢包市場按錢包類型、部署類型、組織規模、分銷管道、資產類型和行業垂直領域分類,全球預測,2026-2032年 加密貨幣錢包市場規模、佔有率和成長分析(按類型、作業系統、應用程式、最終用戶和地區分類)—2026-2033年產業預測

加密貨幣錢包市場規模、佔有率和成長分析(按類型、作業系統、應用程式、最終用戶和地區分類)—2026-2033年產業預測 2025年去中心化加密錢包全球市場報告2025年全球加密錢包市場報告

2025年去中心化加密錢包全球市場報告2025年全球加密錢包市場報告 2025-2029年全球加密錢包市場

2025-2029年全球加密錢包市場