|

市場調查報告書

商品編碼

2064358

麥克普羅:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Mecoprop - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

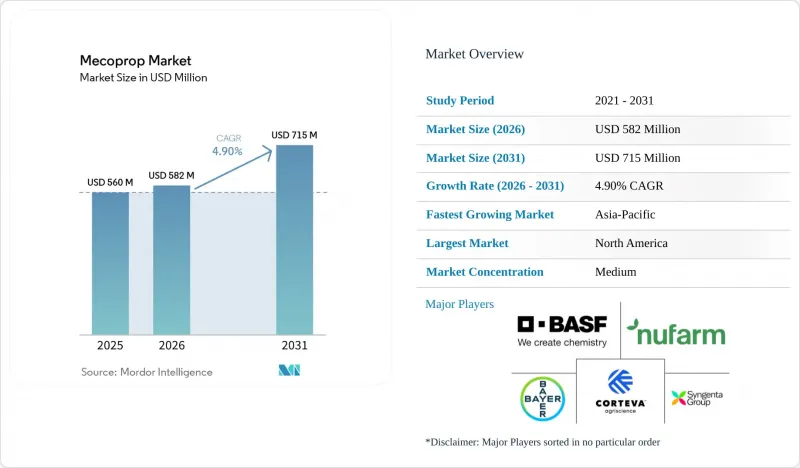

據 Mordor Intelligence 稱,2025 年麥草畏市場價值 5.6 億美元,預計到 2031 年將達到 7.15 億美元,而 2026 年為 5.82 億美元,預測期(2026-2031 年)複合年成長率為 4.9%。

本報告按產品類型(甲氧丙酸原藥和甲氧丙酸製劑)、劑型(乳化濃縮液(EC) 及其他)、作物/應用(草坪和觀賞植物及其他)、配銷通路(直接銷售給分銷商及其他)和地區(北美、南美、歐洲、亞太及其他)進行細分。市場預測以美元 (USD) 為單位。

全球麥草畏市場趨勢與洞察

隨著Glyphosate使用禁令範圍的擴大,草坪護理人員被迫改用選擇性苯氧基除草劑。

地方政府對Glyphosate使用的限制正在加速高爾夫球場、運動場和公園等場所轉向苯氧基類除草劑的轉變。草坪管理人員擴大採用由2,4-D、麥草畏和甲草胺磷組成的三組分混合劑,以在不依賴非選擇性除草劑的情況下控制闊葉雜草。加拿大衛生署於2025年續簽了幾種甲草胺磷組合藥物的批准,維持了其列出的商用和住宅用途。太平洋西北地區的推廣指南建議每英畝使用0.75磅酸當量進行廣譜噴灑,強調了甲草胺磷對細葉匍匐翦股穎的安全性。美國正在進行的關於Glyphosate供應可靠性的政策審查正在支持這一轉變,並確保到2031年對苯氧基類替代品的穩定需求。這一趨勢為成熟市場和新興市場的甲草胺磷市場提供了持續的利多因素。

低毒性的甲氧丙酸-P對映體獲得監管部門批准

單一對映體甲氧丙酸(mecoprop-P)的加速核准,使其在哺乳動物毒性和環境持久性方面優於外消旋混合物,從而開闢了新的消費和專業應用領域。加拿大衛生署於2025年批准了多項新的和更新的申請,顯示其對R-對映體的安全性充滿信心。剪切機大學的資料庫仍然顯示,外消旋甲氧丙酸鈉具有生殖毒性,凸顯了純化物質的優越性。具備對映體特異性合成能力的製造商正獲得監管機構的優先待遇,並在高價值草坪市場領域鞏固其市場佔有率。風險評估的降低將使其能夠在先前限制使用苯氧基農藥的地區(例如歐洲的一些城市)進行分銷。隨著核准範圍的擴大,從2026年到2031年,對甲氧丙酸製劑的需求將支撐銷售量的穩定成長和定價能力的提升。

嚴格規定食品作物中苯氧基酸類物質的最大殘留限量

歐洲和北美的食品安全監管機構正在實施更低的殘留限量標準,限制苯氧基類除草劑在穀物、油籽和飼料作物中的使用。推廣指南包括延長2,4-D及其相關混合物的收穫前間隔期,凸顯了監管合規的挑戰。出口型生產商正在避免在糧食作物輪作中使用甲草胺,因為如果殘留量超過目的地基準值,他們的貨物可能會被拒收。資料庫剪切機顯示某些鹽類具有生殖毒性,這加大了監管機構對更嚴格監測的壓力。隨著監測力度的加大,需求正從糧食作物轉向草坪、觀賞植物和工業植被管理,這可能會抑制甲草胺市場的成長。

細分市場分析

2025年,甲氧丙酸-P製劑佔據了甲氧丙酸市場56%的最大佔有率。這主要歸功於其易用性和即時應用性,深受承包商和家庭用戶的青睞。濃縮製劑面向合約配藥商和經驗豐富的經銷商,預計在2026年至2031年間將以7.7%的複合年成長率快速成長,這主要得益於中國和印度非專利藥產量的增加。如果滿足資料提交要求,美國等監管管道(例如有條件註冊)將允許進口新的原料藥 )。 API供應量的增加將促進價格敏感地區的在地化製劑生產。因此,製劑將繼續主導甲氧丙酸市場,而原料藥的分銷範圍將擴展到新興經濟體。

原料藥)的購買者受益於靈活的混合配方,他們可以根據當地農業需求選擇溶劑、助劑和包裝。亞洲製劑生產商通常選擇重新包裝成 1 公升瓶裝,以適應小規模農戶的購買力。南美的主要經銷商則傾向於進口桶裝產品,以便為區域品牌提供自動化填充生產線。隨著單獨使用和混合使用甲氧丙酸鉀的植物毒性數據不斷積累,預計對濃縮液的需求將會增加。高階品牌製劑與經濟實惠的非專利藥之間的相互作用,將在未來塑造甲氧丙酸鉀市場的市場動態。

2025年,乳化濃縮液仍以40%的佔有率佔據麥草畏市場最大佔有率,主要得益於專業噴霧器對罐混柔軟性和設備相容性的重視。可溶性濃縮劑緊隨其後,這得歸功於其高活性成分含量和輕便的包裝。即用型氣霧劑預計將以8.4%的複合年成長率(CAGR)實現最高成長率,從2026年到2031年,這主要得益於DIY銷售、低揮發性鹽分和內置漂移防護裝置等優勢。顆粒劑配方則應用於草坪細分市場,透過結合肥料和除草劑,實現全年有效。乳化劑技術的持續創新,例如嵌入式安全劑,對於面臨抗性雜草的廣袤糧田而言,仍然至關重要。

消費者對便利性的追求推動了氣霧劑產品的成長,家庭使用者需要易於使用、無需計量的除草方案。零售商店的陳列策略是將氣霧劑產品放置在噴灌器和草籽附近,以促進衝動消費。製造商正在改進配方,以減少氣味和污漬,從而提高郊區家庭的接受度。水溶性濃縮液因其有助於減少溶劑排放受到公園管理部門的青睞。細分市場的多元化確保了穩定的需求,在不斷變化的用戶偏好與美克丙市場整體規模之間取得了平衡。

區域分析

2025年,北美地區佔據了麥草畏市場最大的佔有率,達到31%,這主要得益於其在高爾夫球場、運動場和住宅草坪上的廣泛應用。 2026年至2031年,由於成熟需求被更嚴格的市政農藥法規和日益成長的有機種植趨勢所抵消,預計市場成長將保持溫和的複合年成長率。美國關於Glyphosate供應的政策討論正在推動市場向苯氧類製劑多元化發展,從而支撐了麥草畏的基準需求。加拿大維持著簡化的註冊流程,並在2025年更新了幾種麥草畏-P產品,以確保持續供應。儘管水麻和地膚的抗藥性出現凸顯了綜合治理的必要性,但苯氧類除草劑仍是重要的防治工具。

亞太地區是成長最快的區域市場,預計到2031年將以8.6%的複合年成長率成長,這主要得益於快速的都市化、可支配收入的增加以及電子商務分銷管道的擴張。儘管中國在工業生產和出口方面佔據主導地位,但印度和東南亞國家住宅草坪的普及率正在不斷提高。BASF公司和科迪華農業科技公司透過在印度推出「Clearfield Mustard」生產系統(計畫於2026年上市),展現了其對適用於草坪和特種作物的性狀組合的重視。在澳洲的高爾夫球場和運動草坪領域,對用於控制抗性闊葉雜草的選擇性除草劑的持續投資,推動了麥草畏的銷售量。地方政府對公園建設和綠化項目的撥款也增加了對專業草坪管理服務的需求。

預計到2025年,歐洲將佔據相當大的銷售佔有率,並在2026年至2031年間保持強勁的複合年成長率,這主要得益於更嚴格的法規和對有機草坪管理日益成長的需求。紐發姆有限公司(Nufarm Ltd.)位於懷克(Wyke)的工廠在2025年實現了銷售量成長,但由於苯氧基除草劑價格下跌,利潤率面臨壓力。愛爾蘭和英國的除草劑抗性調查顯示,雜草對ALS和ACCase的抗性日益增強,這促使人們對含有苯氧基活性成分的多效製劑重新燃起興趣。德國和法國在穀物和油籽種植方面的農業應用依然強勁,而英國則主要依賴草坪和公共設施市場。東歐大片穀物種植的需求旺盛,但地緣政治的不確定性正在影響消費模式。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 隨著Glyphosate使用禁令範圍的擴大,草坪護理人員正在轉向使用選擇性苯氧基除草劑。

- 低毒性甲氧丙酸對映異構體獲得監管部門批准

- 在日益都市化的經濟區域,專業的草坪和花園護理服務不斷發展。

- 將抗除草劑種子披衣技術應用於種子萌發前後的害蟲防治,可實現兩者的結合。

- DIY零售市場中即用型家用草坪除草劑越來越受歡迎。

- 線上農藥市場的快速成長正在推動開發中國家分銷網路的擴張。

- 市場限制因素

- 食用作物中苯氧酸的嚴格殘留基準值

- 闊葉雜草抗藥性的出現降低了田間防治效果。

- 主要原料2,4-二氯苯酚的價格波動影響了生產成本。

- 人們越來越傾向於採用有機草坪和景觀管理方法。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- Mecoprop-P 技術

- 含有甲氧丙酸磷的產品

- 配方

- 乳化濃縮液(EC)

- 可溶性濃縮液(SL)

- 顆粒製備

- 即用型氣霧劑

- 按作物/用途

- 草坪和觀賞植物

- 穀物和豆類

- 住宅草坪和花園

- 透過分銷管道

- 直接銷售給批發商

- 線上農藥平台

- 零售花園中心

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Corteva Agriscience

- Bayer AG

- Nufarm Limited

- Syngenta Crop Protection AG

- Albaugh, LLC

- FMC Corporation

- UPL Limited

- Jiangsu Jiangnan Agrochemical Co., Ltd.

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Shandong Rainbow Agro Co., Ltd.

- Nutrien Ltd.

- HELM AG

- Valent USA LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the mecoprop market size was valued at USD 560 million in 2025 and estimated to grow from USD 582 million in 2026 to reach USD 715 million by 2031, at a CAGR of 4.9% during the forecast period (2026-2031).

This report is Segmented by Product Type (Mecoprop-P Technical, and Mecoprop-P Formulated Products), by Formulation (Emulsifiable Concentrate (EC), and More), by Crop/Application (Turf and Ornamentals, and More), by Distribution Channel (Direct Sales To Distributors, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD)

Global Mecoprop Market Trends and Insights

Expanding Bans on Glyphosate Pushing Turf Managers Toward Selective Phenoxy Herbicides

Municipal limitations on glyphosate have accelerated substitution toward phenoxy herbicides in golf courses, sports fields, and municipal parks. Turf managers increasingly adopt three-way mixes of 2,4-D, dicamba, and Mecoprop-P to maintain broadleaf control without depending on non-selective burndown programs. Health Canada renewed multiple Mecoprop-P combinations in 2025, keeping professional and residential label uses open. Extension guides in the Pacific Northwest recommend broadcast rates of 0.75 pound acid equivalent per acre, highlighting Mecoprop-P's safety on fine bentgrass. Ongoing United States policy reviews of glyphosate supply reliability reinforce the shift, ensuring steady demand for phenoxy alternatives through 2031. The trend provides a durable tailwind for the mecoprop market across mature and emerging regions.

Regulatory Approvals of Mecoprop-P Enantiomer with Lower Toxicity Profile

Fast-track registrations for single-enantiomer Mecoprop-P reduce mammalian toxicity and environmental persistence relative to racemic mixtures, unlocking new consumer and professional applications. Health Canada cleared several new or renewed dossiers in 2025, signaling confidence in the R-enantiomer's safety profile. The University of Hertfordshire database still flags racemic Mecoprop-sodium as posing reproductive hazards, underscoring the advantage of purified material. Manufacturers with enantiomer-specific synthesis capacity are gaining regulatory preference, consolidating market share in high-value turf segments. Lower hazard ratings open distribution in jurisdictions that previously restricted phenoxy use, such as several European municipalities. As approvals spread, demand for Mecoprop-P formulations will support stable volume growth and improved pricing power during 2026-2031.

Stringent Maximum Residue Limits for Phenoxy Acids in Food Crops

Food-safety regulators in Europe and North America enforce lower residue tolerances that restrict phenoxy applications in cereals, oilseeds, and forage. Extension guides list long preharvest intervals for 2,4-D and related mixtures, highlighting compliance challenges. Export-oriented growers face shipment rejection if residues exceed destination limits, prompting avoidance of Mecoprop in edible rotations. The University of Hertfordshire database continues to flag reproductive hazards for certain salts, adding regulatory pressure for tighter oversight. As scrutiny mounts, demand migrates from food crops to turf, ornamentals, and industrial vegetation management, potentially trimming mecoprop market growth.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Professional Turf and Lawn Care Services in Urbanizing Economies

- Integration of Herbicide-Tolerant Seed Coatings Enabling Combined Pre and Post Emergence Control

- Emerging Resistance in Broadleaf Weeds is Reducing Field Efficacy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mecoprop-P formulated products generated the largest 56% share of mecoprop market size in 2025 as contractors and homeowners preferred the ready-to-spray ease of use. Technical concentrates serve toll formulators and experienced distributors and are projected to grow at the fastest 7.7% CAGR during 2026-2031, propelled by rising generic output in China and India. Regulatory pathways, such as United States conditional registrations, allow new technical imports once data call-ins are met. Growing concentrate availability boosts local formulation in price-sensitive regions. Consequently, formulated products will retain the bulk of the mecoprop market, while concentrates expand their reach into emerging economies.

Technical material buyers benefit from flexible blending that tailors solvent choice, adjuvants, and packaging to local agronomic needs. Asian formulators often down-pack into one-liter bottles that align with the purchasing power of smallholders. Larger distributors in South America prefer drum imports that feed automated filling lines for regional brands. As phytotoxicity data accumulate for Mecoprop-P alone and in mixes, demand for concentrates should strengthen. The interplay between premium branded formulations and cost-efficient generics will shape future mecoprop market dynamics.

Emulsifiable concentrates maintained the largest 40% mecoprop market share in 2025 because professional applicators value tank-mix flexibility and equipment compatibility. Soluble concentrates followed due to higher active loading and lighter packaging. Ready-to-use aerosols are forecast for the fastest 8.4% CAGR from 2026-2031, supported by DIY merchandising, low-volatility salts, and built-in drift guards. Granular formulations serve niche lawn segments where combined fertilizer and weed control provide season-long benefit. Continued innovation in emulsifiable technology, such as built-in safeners, maintains relevance in broadacre cereals facing resistant weeds.

Consumer convenience dictates aerosol growth as homeowners seek grab-and-go weed solutions without measuring. Retail planograms place aerosols near sprinkler gear and grass seed to capture impulse traffic. Manufacturers reformulate to reduce odor and staining, increasing acceptance among suburban households. Water-based, soluble concentrates appeal to parks departments seeking to reduce solvent emissions. Segment diversity ensures steady demand and balances the overall mecoprop market size against evolving user preferences.

Geography Analysis

North America held the largest 31% share of the mecoprop market in 2025, driven by extensive use on golf courses, sports fields, and residential lawns. Growth is forecast to be at a descent CAGR during 2026-2031, as mature demand is offset by stricter municipal pesticide bylaws and rising organic preferences. United States policy discussions on glyphosate supply encourage diversification into phenoxy mixes, underpinning baseline Mecoprop demand. Canada maintains a streamlined registration process, renewing multiple Mecoprop-P products in 2025 to ensure continued supply. Resistance emergence in waterhemp and kochia underscores the need for integrated management, but phenoxy herbicides remain a critical tool.

Asia-Pacific is the fastest-growing regional market, with a 8.6% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and expanding e-commerce distribution. China dominates technical production and exports, while India and Southeast Asian nations add residential lawn adoption. BASF SE and Corteva Agriscience introduced the Clearfield Mustard production system in India in 2026, showcasing the corporate focus on trait packages that can be transferred to turf and specialty crops. Australia's golf and sports turf sector continues to invest in selective herbicides to manage resistant broadleaf weeds, sustaining Mecoprop volume. Regional governments fund park construction and greening projects, thereby increasing demand for professional turf services.

Europe accounted for a significant share of 2025 sales and is projected to grow at descent CAGR during 2026-2031, given regulatory tightness and rising organic lawn care. Nufarm Ltd.'s Wyke facility delivered volume gains in 2025 but faced margin pressure from low phenoxy prices. Herbicide resistance surveys in Ireland and the United Kingdom highlight the spread of ALS and ACCase resistance, prompting renewed interest in multi-mode mixes that include phenoxy actives. Germany and France sustain agricultural use in cereals and oilseeds, while the United Kingdom depends on turf and amenity markets. Eastern Europe shows steady demand from broadacre grains, although geopolitical uncertainties influence spending patterns.

- BASF SE

- Corteva Agriscience

- Bayer AG

- Nufarm Limited

- Syngenta Crop Protection AG

- Albaugh, LLC

- FMC Corporation

- UPL Limited

- Jiangsu Jiangnan Agrochemical Co., Ltd.

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Shandong Rainbow Agro Co., Ltd.

- Nutrien Ltd.

- HELM AG

- Valent U.S.A. LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding bans on glyphosate pushing turf managers toward selective phenoxy herbicides

- 4.2.2 Regulatory approvals of Mecoprop-P enantiomer with lower toxicity profile

- 4.2.3 Growth of professional turf and lawn care services in urbanizing economies

- 4.2.4 Integration of herbicide-tolerant seed coatings enabling combined pre and post emergence control

- 4.2.5 Rising adoption of ready-to-use consumer lawn weed control products in DIY retail

- 4.2.6 Rapid growth of online agrochemical marketplaces boosting distribution reach in developing nations

- 4.3 Market Restraints

- 4.3.1 Stringent maximum residue limits for phenoxy acids in food crops

- 4.3.2 Emerging resistance in broadleaf weeds is reducing field efficacy

- 4.3.3 Price volatility of key feedstock 2,4-Dichlorophenol is impacting production cost

- 4.3.4 Increasing shift toward organic lawn and landscape management

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Mecoprop-P Technical

- 5.1.2 Mecoprop-P Formulated Products

- 5.2 By Formulation

- 5.2.1 Emulsifiable Concentrate (EC)

- 5.2.2 Soluble Concentrate (SL)

- 5.2.3 Granular Formulations

- 5.2.4 Ready-to-Use Aerosols

- 5.3 By Crop/Application

- 5.3.1 Turf and Ornamentals

- 5.3.2 Cereals and Pulses

- 5.3.3 Residential Lawns and Gardens

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales to Distributors

- 5.4.2 Online Agrochemical Platforms

- 5.4.3 Retail Garden Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Corteva Agriscience

- 6.4.3 Bayer AG

- 6.4.4 Nufarm Limited

- 6.4.5 Syngenta Crop Protection AG

- 6.4.6 Albaugh, LLC

- 6.4.7 FMC Corporation

- 6.4.8 UPL Limited

- 6.4.9 Jiangsu Jiangnan Agrochemical Co., Ltd.

- 6.4.10 Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- 6.4.11 Shandong Rainbow Agro Co., Ltd.

- 6.4.12 Nutrien Ltd.

- 6.4.13 HELM AG

- 6.4.14 Valent U.S.A. LLC

7 Market Opportunities and Future Outlook

除草墊市場-2026-2032年全球市場預測

除草墊市場-2026-2032年全球市場預測 2026年全球磺酸鹽顆粒市場報告2026年諾氟拉松除草劑全球市場報告

2026年全球磺酸鹽顆粒市場報告2026年諾氟拉松除草劑全球市場報告 電腦視覺除草市場預測至2034年:按組件、部署模式、作物類型、技術、應用、最終用戶和地區分類的全球分析

電腦視覺除草市場預測至2034年:按組件、部署模式、作物類型、技術、應用、最終用戶和地區分類的全球分析 全球除草劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球除草劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 不織布膜市場規模、佔有率和成長分析:按材料、應用、銷售管道和地區分類-2026-2033年產業預測

不織布膜市場規模、佔有率和成長分析:按材料、應用、銷售管道和地區分類-2026-2033年產業預測 除草劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作用機制、作物類型、地區和競爭格局分類,2021-2031年機器人除草市場預測至2034年—按產品類型、控制方法、動力來源、農場規模、應用、最終用戶和地區分類的全球分析

除草劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作用機制、作物類型、地區和競爭格局分類,2021-2031年機器人除草市場預測至2034年—按產品類型、控制方法、動力來源、農場規模、應用、最終用戶和地區分類的全球分析 吡唑磺隆市場:按作物類型、配方、應用方法、最終用途、分銷管道和地區分類除草劑市場:按控制方法、應用領域、雜草類型、最終用戶和地區分類。

吡唑磺隆市場:按作物類型、配方、應用方法、最終用途、分銷管道和地區分類除草劑市場:按控制方法、應用領域、雜草類型、最終用戶和地區分類。