|

市場調查報告書

商品編碼

2064345

LED背光模組市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED Backlight Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

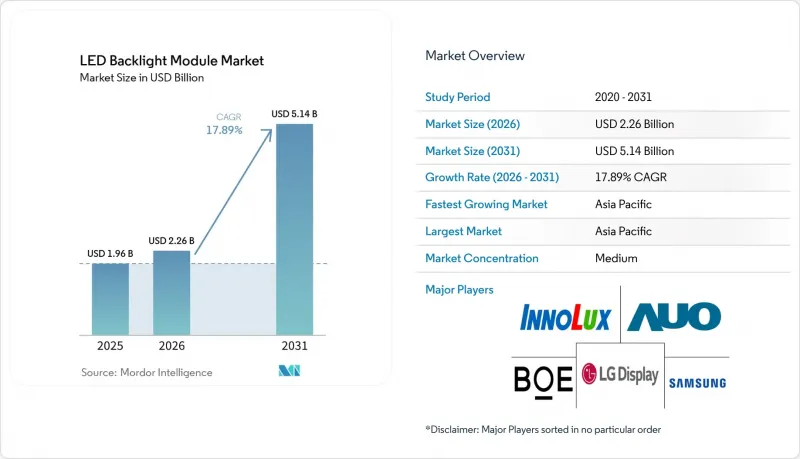

根據 Mordor Intelligence 預測,LED 背光模組市場預計將從 2025 年的 19.6 億美元成長到 2026 年的 22.6 億美元,到 2031 年達到 51.4 億美元,2026 年至 2031 年的複合年成長率為 17.89%。

本報告按背光技術(側發光LED模組、直下式發光LED模組)、面板尺寸(小面板、中面板等)、應用領域(電視、顯示器/筆記型電腦、智慧型手機/平板電腦、車載顯示器等)和地區(北美、歐洲、亞太、南美等)進行細分。市場預測以美元計價。

全球LED背光模組市場趨勢及洞察

高階電視擴大採用Mini-LED背光

三星的Neo QLED和LG的QNED系列電視均採用Mini-LED模組,擁有超過1000個調光區域,峰值亮度超過1500尼特,並具備100% DCI-P3色域覆蓋。零售價格正在下降,北美地區65吋機型的售價已低於1000美元,這使得其應用範圍超越了最初的發燒友群體。每個Mini-LED背光模組都包含5000到25000個晶片,這推動了對具備區域特定脈衝寬度調變(PWM)功能的高階驅動IC的需求。由此導致的元件成本上升為直下式LED背光模組供應商帶來了長期的收入成長,加速了LED背光模組市場向高階配置的轉型。

對高亮度汽車顯示器的需求不斷成長

隨著電動車駕駛座的重新設計,2000-3000尼特的背光亮度對於確保白天可視性至關重要。哈曼的「Ready Display」平台整合了冗餘LED燈串和超過1000個調光區域,以滿足ISO 15008可視性要求和ISO 26262功能安全法規的要求。目前,汽車零件供應商為此功能支付10-15%的模組溢價,確保了該設計在未來幾年內得到廣泛應用,並推高了整個LED背光模組市場的平均售價。

來自OLED和Micro-LED顯示器的競爭加劇

在售價超過 800 美元的旗艦智慧型手機和平板電腦中,OLED 面板已成為主流,取代了傳統的背光技術。 Micro-LED先導計畫預計在不產生有機材料劣化的情況下實現 OLED 等級的對比度,如果量產過程中良率能夠穩定,則有望實現大螢幕的量產。這些自發光技術正在蠶食高階市場的佔有率,並降低 LED 背光模組市場的上限。

細分市場分析

直下式Mini-LED模組預計將以18.23%的複合年成長率成長,反映出其在電視和遊戲顯示器領域的應用日益廣泛。側入式LED背光模組市場預計成長速度較慢,但其輕巧的設計和低於20美元的組件成本使其成為筆記型電腦和低價電視的必備之選。儘管製造商不斷改進雙邊結構和反射腔以維持市場佔有率,但Mini-LED憑藉其卓越的對比度和數千個調光區域,預計將成為長期成長的主要驅動力。

生產成本趨勢也印證了這種兩極化。由於驅動晶片價格下降和LED良率提高,Mini-LED電視的實際售價預計將從2022年的3000美元降至2025年的近1200美元。另一方面,側入式LED電視生產線的運轉率高,資本投資成本低,因此即使平均售價下降,製造商也能保持利潤,預計整個LED背光模組市場將實現均衡成長。

區域分析

預計到2025年,亞太地區將佔全球銷售額的67.82%,維持18.35%的複合年成長率,主要得益於京東方、天馬和TCL華星光電等廠商的產能擴張,以及中國、越南和印度等國的支持措施。本地化專案透過免除國內子組件的進口關稅降低了接收成本,從而促進了企業對組件整合生產線的內部投資。廣東和江蘇兩省的生產基地目前正在整合LED外延、磷光體合成和量子點薄膜生產,進一步強化了區域供應鏈。

在北美和歐洲,汽車顯示器市場普遍呈現顯著成長。日益嚴格的能耗法規正在加速商業指示牌和飯店顯示器向高效能背光技術的轉型。諸如JAPAN DISPLAY)在美國投資130億美元興建工廠等提案的生產回流項目,預計將在維持LED背光模組市場成長動能的同時,實現亞太地區以外的供應來源多元化。

南美洲、中東和非洲仍處於發展階段,當地整合商主要組裝用於零售指示牌和價格敏感型電視的模組。儘管這些地區的產量不足以挑戰亞太地區的主導地位,但關稅壁壘和本地在地採購規則可能會促使本地組裝在預測期內逐步擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階電視擴大採用Mini-LED背光

- 對高亮度汽車顯示器的需求不斷成長

- 側入式背光技術在輕薄筆記型電腦的成本優勢

- 中國和印度供應鏈本地化獎勵

- 節能法規鼓勵改用LED背光。

- 將量子點增強薄膜整合到液晶面板中

- 市場限制因素

- 來自OLED和Micro-LED顯示器的競爭加劇

- 知識產權使用費糾紛推高了零件成本。

- 高性能磷光體供應波動

- 稀土元素礦開採的環境監測

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 背光技術

- 側發光LED模組

- 直下式發光LED模組(全陣列/迷你LED)

- 按面板尺寸

- 小型面板(10英寸或更小)

- 中等尺寸面板(10-32吋)

- 大尺寸面板(32吋或更大)

- 透過使用

- 電視背光模組

- 顯示器/筆記型電腦背光模組

- 智慧型手機/平板電腦背光模組

- 汽車顯示背光模組

- 其他用途 - 顯示應用程式

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- Sharp Corporation

- Shenzhen Refond Optoelectronics Co., Ltd.

- Tianma Microelectronics Co., Ltd.

- Japan Display Inc.

- Rohinni LLC

- Radiant Opto-Electronics Corporation

- Lextar Electronics Corporation

- Winstar Display Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the lED backlight module market size is expected to increase from USD 1.96 billion in 2025 to USD 2.26 billion in 2026 and reach USD 5.14 billion by 2031, growing at a CAGR of 17.89% over 2026-2031.

This report is Segmented by Backlighting Technology (Edge-Lit LED Modules and Direct-Lit LED Modules), Panel Size (Small-Size Panels, Medium-Size Panels, and More), Application (Television, Monitor/Laptop, Smartphone/Tablet, Automotive Display, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Backlight Module Market Trends and Insights

Growing Penetration of Mini-LED Backlighting in Premium TVs

Samsung's Neo QLED and LG's QNED lineups now ship with 1,000-plus dimming-zone Mini-LED modules that deliver peak brightness beyond 1,500 nits and 100% DCI-P3 gamut. Retail price compression 65-inch sets selling below USD 1,000 in North America broadens adoption beyond early enthusiasts. Each Mini-LED backlight employs 5,000-25,000 chips, driving demand for advanced driver ICs with per-zone pulse-width modulation. The resulting bill-of-materials uplift underpins a multiyear revenue tailwind for direct-lit suppliers and accelerates the LED backlight module market's migration toward premium configurations.

Rising Demand for High-Brightness Automotive Displays

Electric-vehicle cockpit redesigns mandate 2,000-3,000 nit backlights for daytime readability. HARMAN's Ready Display platform integrates redundant LED strings and over 1,000 dimming zones to satisfy both ISO 15008 legibility and ISO 26262 functional-safety rules. Automotive tiers now pay 10-15% module premiums for this capability, locking in multiyear design wins and lifting average selling prices across the LED backlight module market.

Intensifying Competition from OLED and Micro-LED Displays

OLED panels dominate flagship smartphones and tablets priced above USD 800, displacing conventional backlights. Micro-LED pilots promise OLED-like contrast without organic degradation and could enter large-screen production once mass transfer yields stabilize. These self-emissive technologies siphon premium share, trimming the attainable ceiling for the LED backlight module market.

Other drivers and restraints analyzed in the detailed report include:

- Supply-Chain Localization Incentives in China and India

- Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- IP Royalty Disputes Elevating BOM Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-lit Mini-LED modules are projected to post an 18.23% CAGR, reflecting rising adoption in televisions and gaming monitors. The LED backlight module market for edge-lit designs will expand more slowly, yet its lightweight profile and sub-USD 20 bill of materials keep it vital for notebooks and budget TVs. Manufacturers continue to refine dual-edge configurations and reflective cavities to defend share, but the contrast advantage of thousands of dimming zones positions Mini-LED as the long-term growth engine.

Production cost curves reinforce this split. Falling driver-IC prices and improved LED binning yields reduced Mini-LED television street prices from USD 3,000 in 2022 to nearly USD 1,200 in 2025. Conversely, edge-lit lines enjoy higher utilization and low capital intensity, enabling manufacturers to profit even as average selling prices decline, ensuring balanced growth across the LED backlight module market.

Geography Analysis

Asia Pacific contributed 67.82% of revenue in 2025 and is projected to sustain an 18.35% CAGR, underpinned by BOE, Tianma, and TCL CSOT expansions, as well as supportive incentives in China, Vietnam, and India. Localization programs reduce landed costs by exempting domestic sub-assemblies from import duties, driving internal investment into module integration lines. Capacity corridors in Guangdong and Jiangsu now combine LED epitaxy, phosphor synthesis, and quantum-dot film production, fortifying the regional supply chain.

North America and Europe collectively register outsized growth in automotive displays. Stricter power-consumption limits accelerate the transition to high-efficiency backlights across commercial signage and hospitality displays. Proposed reshoring projects, such as Japan Display's USD 13 billion fab in the United States, could diversify supply away from the Asia Pacific while maintaining momentum for the LED backlight module market.

South America, the Middle East, and Africa remain nascent, with local integrators assembling modules for retail signage and price-sensitive televisions. Volumes in these regions are insufficient to challenge Asia Pacific dominance, yet tariff barriers and regional content rules could spur incremental localized assembly over the forecast horizon.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- Sharp Corporation

- Shenzhen Refond Optoelectronics Co., Ltd.

- Tianma Microelectronics Co., Ltd.

- Japan Display Inc.

- Rohinni LLC

- Radiant Opto-Electronics Corporation

- Lextar Electronics Corporation

- Winstar Display Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Penetration of Mini-LED Backlighting in Premium TVs

- 4.2.2 Rising Demand for High-Brightness Automotive Displays

- 4.2.3 Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- 4.2.4 Supply-Chain Localisation Incentives in China and India

- 4.2.5 Energy-Efficiency Regulations Favouring LED Backlight Retrofits

- 4.2.6 Integration of Quantum-Dot Enhancement Films in LCD Panels

- 4.3 Market Restraints

- 4.3.1 Intensifying Competition from OLED and Micro-LED Displays

- 4.3.2 IP Royalty Disputes Elevating BOM Costs

- 4.3.3 Supply Volatility of High-Performance Phosphors

- 4.3.4 Environmental Scrutiny on Rare-Earth Extraction

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Backlighting Technology

- 5.1.1 Edge-lit LED Modules

- 5.1.2 Direct-lit LED Modules (Full Array / Mini-LED)

- 5.2 By Panel Size

- 5.2.1 Small-size Panels (Less Than or Equal To 10 inches)

- 5.2.2 Medium-size Panels (Less Than 10 to Greater Than or Equal to 32 inches)

- 5.2.3 Large-size Panels (Less Than 32 inches)

- 5.3 By Application

- 5.3.1 Television (TV) Backlight Modules

- 5.3.2 Monitor / Laptop Backlight Modules

- 5.3.3 Smartphone / Tablet Backlight Modules

- 5.3.4 Automotive Display Backlight Modules

- 5.3.5 Other Application - Display Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 BOE Technology Group Co., Ltd.

- 6.4.4 AU Optronics Corp.

- 6.4.5 Innolux Corporation

- 6.4.6 Sharp Corporation

- 6.4.7 Shenzhen Refond Optoelectronics Co., Ltd.

- 6.4.8 Tianma Microelectronics Co., Ltd.

- 6.4.9 Japan Display Inc.

- 6.4.10 Rohinni LLC

- 6.4.11 Radiant Opto-Electronics Corporation

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 Winstar Display Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

光學薄膜市場:全球市場預測(2026-2032)

光學薄膜市場:全球市場預測(2026-2032) 光學薄膜市場報告:趨勢、預測及競爭分析(至2035年)

光學薄膜市場報告:趨勢、預測及競爭分析(至2035年) 反射偏光片市場規模、佔有率和成長分析:按類型、應用、最終用途、通路和地區分類-2026-2033年產業預測電視背光模組市場報告:趨勢、預測及競爭分析(至2035年)

反射偏光片市場規模、佔有率和成長分析:按類型、應用、最終用途、通路和地區分類-2026-2033年產業預測電視背光模組市場報告:趨勢、預測及競爭分析(至2035年) 光學薄膜市場:按類型、應用和地區分類光擴散膜市場:按材料類型、類別、應用和地區分類

光學薄膜市場:按類型、應用和地區分類光擴散膜市場:按材料類型、類別、應用和地區分類 顯示光學薄膜市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、裝置、製程、最終用戶及功能分類

顯示光學薄膜市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、裝置、製程、最終用戶及功能分類 全球光學薄膜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球光學薄膜市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球光學薄膜市場報告2A 和 3A 光學薄膜市場按材料、類型、厚度和應用分類-2026 年至 2032 年全球預測

2026年全球光學薄膜市場報告2A 和 3A 光學薄膜市場按材料、類型、厚度和應用分類-2026 年至 2032 年全球預測