|

市場調查報告書

商品編碼

2064019

COB LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)COB LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

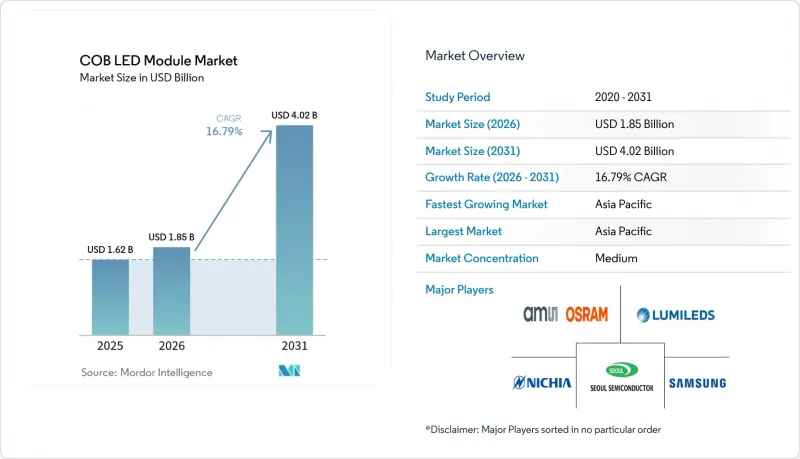

根據 Mordor Intelligence 預測,COB LED 模組市場規模預計在 2025 年達到 16.2 億美元,在 2026 年達到 18.5 億美元,在 2031 年達到 40.2 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 16.79%。

本報告按輸出功率範圍(低功率COB模組、中功率COB模組等)、應用領域(通用照明、汽車照明、工業照明、建築及戶外照明等)和地區(北美、南美、歐洲、亞太等)進行細分。市場預測以美元(USD)計價。

全球COB LED模組市場趨勢及洞察

加強全球能源效率法規

歐盟2019/2020生態設計法規及美國類似法規的嚴格規定,迫使供應商提高組件效率、延長光通量維持時間並減少閃爍。被歸類為光源的COB產品必須獲得EPREL認證才能進入歐洲市場。這項要求增加了合規成本,同時也限制了小規模、未經認證的製造商進入市場。自2026年12月起,永續產品生態設計法規將增加循環經濟的要求,並鼓勵採用符合Zhaga Book 12標準且可連接插座和易於維護的設計。第三方測試、符合IEC 62031標準以及確保光生物安全性的負擔,正在加速擁有可出具合格聲明的認可測試實驗室的製造商之間的整合。

中功率模組的每流明價格大幅下降。

2022年至2025年間,中功率COB LED模組的價格大幅下降。這一價格下跌主要得益於中國供應商利用其國內MOCVD產能。然而,這種通縮趨勢導致封裝企業的毛利率大幅減半。 2026年初,為因應貴金屬價格飆升,價值鏈上的50多家企業紛紛漲價以彌補損失的利潤。價格回升改變了競爭格局,競爭焦點從單純的價格競爭轉向差異化。目前,關鍵的差異化因素包括色彩穩定性、高顯色性(高CRI)磷光體以及板載驅動功能,這些都足以支撐平均售價的上漲。歐洲、美國和日本的供應商憑藉其獨特的磷光體配方,能夠提供超越單純光通量的附加價值,從而更好地從這個不斷變化的市場環境中獲益。

由於中國低成本的生產能力,價格下降

中國晶片和封裝製造商的產能擴張速度超過了國內需求的成長速度。這種供需失衡導致持續的供應過剩,壓低了中功率產品的平均售價。主流的板載晶片(COB)價格大幅下跌,迫使台灣和東南亞一些獲利能力的製造商關閉生產線或轉向小眾應用領域。中國上市LED企業的平均毛利率下降,引發了第一波協同提價通知。儘管各方正在努力恢復產品價值,但中東和非洲的通用照明市場仍然對價格非常敏感。因此,許多外國品牌被迫轉向差異化程度較高的高階細分市場。

細分市場分析

預計2026年至2031年間,功率超過50W的高功率模組將以17.73%的複合年成長率成長,超過COB LED模組市場的整體成長速度。單源封裝即可提供超過5000流明的光通量,簡化了體育場館泛光燈、工業高棚燈和戶外區域照明的光學和佈線。 Bridgelux的第二代F90系列正是此趨勢的典範,其40W的發送器可提供8000流明的光通量,同時在60 度C的溫度波動範圍內,色差Δu'v'小於0.004。同時,中功率產品的 COB LED 模組市場依然龐大,預計到 2025 年將佔商業下照燈和建築重點照明市場 41.47% 的佔有率。 10W 以下的低功率模組主要集中在顯示器背光、內凹照明和裝飾燈條領域,但晶片級封裝在更小的尺寸內提供相同的光通量,給低功率模組帶來了越來越大的壓力。

採購決策會沿著輸出功率軸呈現分化。高功率發光二極體的買家優先考慮使用壽命和熱裕度,他們願意使用昂貴的陶瓷基板和銅片來避免過早的光通量衰減。電力公司和體育場館業主認為,高昂的安裝成本是合理的,因為在5萬小時的運作週期內,照明燈具的數量減少,維護成本也極低。同時,在中功率級別,每流明成本的競爭異常激烈,中國供應商的定價比國際品牌低10%至25%。來自歐洲、美國和日本的老牌製造商透過提供穩定的色坐標和符合DLC溢價補貼條件的優質磷光體混合物來維持市場佔有率,尤其是在顯色指數(CRI)達到90的酒店等場所。

區域分析

預計到2025年,亞太地區將佔全球COB LED模組銷售額的66.73%,並將在2031年之前繼續保持市場中心地位,複合年成長率(CAGR)為17.95%。中國憑藉著廣東和江蘇兩省的端到端LED叢集以及政府對晶片製造廠和封裝生產線資本投資的補貼獎勵,在市場中佔據主導地位。電視、筆記型電腦和顯示器等產品對Mini-LED背光的廣泛應用,維持了國內強勁的需求,而積極的出口策略則推動了東南亞地區通用型產品的供應。日本和韓國則專注於汽車、顯示器和醫療設備等規模較小但盈利的細分市場,利用陶瓷、AlGaN外延技術和嚴格的可靠性測試,以獲得高價產品。

到2025年,北美和歐洲市場合計將佔全球銷售額的約四分之一。電力公司補貼、DLC高級等級補貼以及歐盟生態設計法規推動的維修項目,正在加速螢光和HID泛光燈被光效超過150 lm/W、顯色指數(CRI)達到90的COB照明燈具所取代。與2026年FIFA世界盃和2028年洛杉磯奧運會相關的體育場館維修項目備受矚目,需要能夠實現無閃爍8K廣播級畫質的高功率模組。歐洲循環經濟政策傾向於採用可插拔、可維修且帶有數位產品護照的COB模組,而符合Zhaga Book 12機械結構標準的供應商將獲得優先待遇。

南美洲、中東和非洲是COB LED模組的新興市場,但市場規模雖小,成長迅速。在巴西和墨西哥,工業LED高棚燈正被應用於食品加工廠和物流園區。同時,波灣合作理事會(GCC)成員國正在投資建造智慧城市走廊,這需要防護等級為IP69K、能夠抵禦沙塵和鹽霧的COB泛光燈。在非洲,採用低功耗COB光源以延長電池壽命的離網太陽能燈正逐漸獲得市場認可,但價格因素限制了高階型號的普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 嚴格的全球能源效率法規

- 中功率模組的每流明價格大幅下降。

- 智慧互聯照明生態系的普及

- 電動車OEM廠商向整合式頭燈架構的過渡

- 高階顯示器中Mini-LED背光技術的蓬勃發展

- 都市區體育場館維修工程中高功率COB的必要性。

- 市場限制因素

- 中國低成本生產能力所帶來的價格壓力

- 功率低於 50 瓦的模組散熱成本較高,溫度控管成本也較高。

- 與晶片級/覆晶封裝的競爭

- 磷光體和基板材料的供應鏈波動

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 輸出範圍

- 低功耗COB模組(小於10瓦)

- 中功率COB 模組(10-50 瓦)

- 高功率COB模組(50瓦或以上)

- 透過使用

- 一般照明

- 汽車照明

- 工業照明

- 建築/戶外照明

- 其他用途(園藝、紫外線防護、特殊應用)

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 南美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Toyoda Gosei Co., Ltd.

- Luminus Devices, Inc.

- ProPhotonix Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the cOB lED module market size is projected to be USD 1.62 billion in 2025, USD 1.85 billion in 2026, and reach USD 4.02 billion by 2031, growing at a CAGR of 16.79% from 2026 to 2031.

This report is Segmented by Power Range (Low Power COB Modules, Mid Power COB Modules, and More), Application (General Lighting, Automotive Lighting, Industrial Lighting, Architectural and Outdoor Lighting, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global COB LED Module Market Trends and Insights

Stringent Energy-Efficiency Regulations Worldwide

Regulatory tightening in the EU under Ecodesign Regulation 2019/2020 and parallel rules in the United States pushes suppliers to raise module efficacy, extend lumen maintenance, and curb flicker. COB products classified as light sources must secure EPREL registration before entering European channels, a requirement that adds compliance costs but also limits the entry of smaller, unaccredited fabricators. From December 2026, the Ecodesign for Sustainable Products Regulation adds circularity mandates that reward socketable, serviceable designs aligned with Zhaga Book 12 holders. The burden of third-party testing, IEC 62031 conformity, and photobiological safety accelerates consolidation among manufacturers with accredited labs capable of issuing declarations of conformity.

Rapid Decline in USD/Lumen for Mid-Power Modules

Between 2022 and 2025, prices for mid-power COB LED modules dropped significantly. This price drop was largely driven by Chinese suppliers, who capitalized on their domestic MOCVD capacity. However, this deflationary trend led to a significant halving of packaging houses' gross margins. By early 2026, in response to surging precious-metal prices, over 50 companies spanning the value chain implemented price increases to recoup lost margins. This price rebound has shifted the competitive landscape, moving the focus from mere pricing to differentiation. Key differentiators now include color stability, high-CRI phosphors, and integrated driver-on-board features, all of which justify elevated average selling prices. Suppliers from the West and Japan, armed with proprietary phosphor mixes, stand to gain the most from this evolving landscape, as their offerings emphasize value beyond just raw lumens.

Price Erosion from Chinese Low-Cost Capacity

Chinese chipmakers and packagers are ramping up capacity, outpacing domestic demand growth. This imbalance has led to a consistent supply surplus, pushing mid-power average selling prices (ASPs) downward. Mainstream Chip-on-Board (COB) prices declined significantly, prompting some marginal producers in Taiwan and Southeast Asia to either shut down production lines or pivot to niche applications. The average gross margin for publicly listed Chinese LED companies dipped, prompting the first wave of coordinated price increase notifications. While efforts to restore value are underway, the market for commodity luminaires in the Middle East and Africa remains price-sensitive. As a result, many foreign brands find themselves relegated to premium sub-segments, where differentiation is more pronounced.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Integrated Headlamp Architectures in EVs

- Mass Adoption of Smart, Connected Lighting Ecosystems

- High Thermal-Management Cost for Less Than 50 W Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-power modules above 50 W are on track to expand at 17.73% CAGR during 2026-2031, outstripping the broader COB LED module market. Single-source packages delivering more than 5,000 lm streamline optics and wiring in stadium floodlights, industrial high bays, and outdoor area fixtures. Bridgelux's Generation 2 F90 family illustrates the trend, offering 8,000 lm from a 40 W emitter while preserving Δu'v' color shift below 0.004 across a 60 °C temperature swing. Meanwhile, the COB LED module market for mid-power products remains large, accounting for 41.47% of the market in 2025 across commercial downlights and architectural accents. Low-power modules under 10 W cluster into display backlighting, cove lighting, and decorative strips, but face rising pressure from chip-scale packages that achieve equivalent flux in slimmer footprints.

The purchasing calculus diverges along this power axis. Buyers of high-power emitters prize lifetime and thermal headroom, tolerating premium ceramic substrates and copper coins to avoid premature lumen depreciation. Utilities and stadium owners view the higher acquisition cost as justified by reduced fixture counts and minimal maintenance over 50,000 h duty cycles. Conversely, the mid-power tier competes on dollars per lumen, with Chinese suppliers undercutting global brands by 10-25%. Here, Western and Japanese incumbents defend territory by offering better phosphor blends that lock in color point and qualify for DLC Premium rebates, especially in CRI 90 hospitality spaces.

Geography Analysis

Asia-Pacific accounted for 66.73% of global revenue in 2025 and will remain the epicenter of the COB LED module market through 2031, with a forecast 17.95% CAGR. China dominates with end-to-end LED clusters in Guangdong and Jiangsu, plus state incentives that defray capex for chip fabs and packaging lines. Mini-LED backlight adoption in televisions, notebooks, and monitors keeps domestic demand robust, while export aggressiveness fuels commodity supply across Southeast Asia. Japan and South Korea pursue smaller but lucrative niches in automotive, display, and medical equipment, leveraging ceramics, AlGaN epitaxy, and rigorous reliability tests to fetch premiums.

North America and Europe together accounted for roughly one-quarter of revenue in 2025. Retrofit programs driven by utility rebates, DLC Premium tiers, and EU Ecodesign rules accelerate replacement of fluorescent troffers and HID floodlights with COB fixtures exceeding 150 lm/W and CRI 90. Stadium renovations connected to the 2026 FIFA World Cup and the 2028 Los Angeles Olympics create headline projects that call for high-power modules capable of delivering flicker-free 8K broadcast levels. Circular-economy policies in Europe prefer socketable, repairable COB modules with digital product passports, rewarding suppliers that align mechanical footprints with Zhaga Book 12.

South America, the Middle East, and Africa are smaller but growing markets for COB LED modules. Brazil and Mexico deploy industrial LED high bays in food processing and logistics parks, while the Gulf Cooperation Council members invest in smart-city corridors that demand IP69K-rated COB floodlights to withstand sand and saline fog. Africa shows early traction for off-grid solar lanterns that integrate low-power COB engines for extended battery life, though price sensitivity limits the adoption of higher-tier products.

- ams OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Toyoda Gosei Co., Ltd.

- Luminus Devices, Inc.

- ProPhotonix Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Energy-Efficiency Regulations Worldwide

- 4.2.2 Rapid Decline in USD/Lumen for Mid-Power Modules

- 4.2.3 Mass Adoption of Smart, Connected Lighting Ecosystems

- 4.2.4 OEM Shift Toward Integrated Headlamp Architectures in EVs

- 4.2.5 Mini-LED Backlighting Boom in Premium Displays

- 4.2.6 Urban Stadium and Arena Renovations Demanding High-Power COB

- 4.3 Market Restraints

- 4.3.1 Price Erosion from Chinese Low-Cost Capacity

- 4.3.2 High Thermal-Management Cost for Less Than 50 W Modules

- 4.3.3 Competition from Chip-Scale and Flip-Chip Packages

- 4.3.4 Supply-Chain Volatility in Phosphor and Substrate Materials

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 Low Power COB Modules (Greater Than or Equal To 10 W)

- 5.1.2 Mid Power COB Modules (Less Than 10 W - Greater Than or Equal To 50 W)

- 5.1.3 High Power COB Modules (Less Than 50 W)

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.2 Automotive Lighting

- 5.2.3 Industrial Lighting

- 5.2.4 Architectural and Outdoor Lighting

- 5.2.5 Other Applications (Horticulture, UV, Specialty)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Nichia Corporation

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Citizen Electronics Co., Ltd.

- 6.4.7 Bridgelux, Inc.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Epistar Corporation

- 6.4.11 Lextar Electronics Corp.

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Luminus Devices, Inc.

- 6.4.14 ProPhotonix Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2034年板載晶片LED市場預測-按類型、材料、應用和地區分類的全球分析

2034年板載晶片LED市場預測-按類型、材料、應用和地區分類的全球分析 晶片封裝 (COB) LED 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2026–2034)

晶片封裝 (COB) LED 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2026–2034) 2025-2029年全球板載晶片(COB)LED市場

2025-2029年全球板載晶片(COB)LED市場 板載晶片LED市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年

板載晶片LED市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年 COB攝影燈市場按應用、光類型、色溫、終端用戶產業、通路、額定功率、光束角、驅動器類型和外殼材質分類-2026-2032年全球預測

COB攝影燈市場按應用、光類型、色溫、終端用戶產業、通路、額定功率、光束角、驅動器類型和外殼材質分類-2026-2032年全球預測 全球板載晶片LED市場

全球板載晶片LED市場 板載晶片 LED 市場(按產品、材料、應用、國家和地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

板載晶片 LED 市場(按產品、材料、應用、國家和地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測