|

市場調查報告書

商品編碼

2063990

葡萄採摘機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Grape Harvesting Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

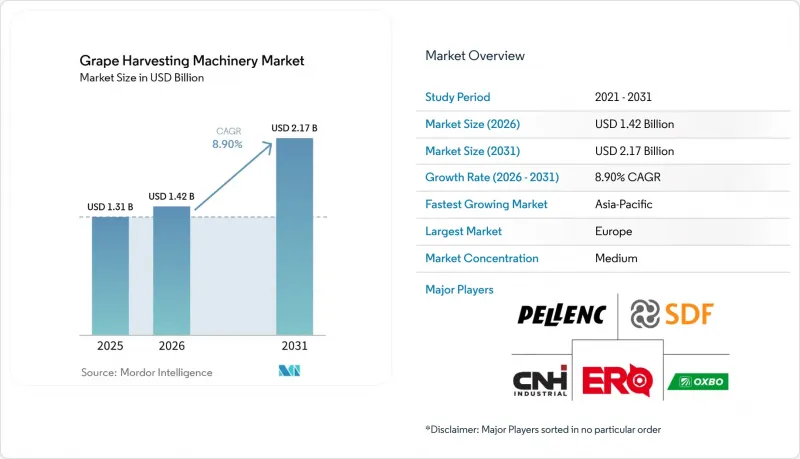

根據 Mordor Intelligence 預測,葡萄收割機市場規模將從 2025 年的 13.1 億美元成長到 2026 年的 14.2 億美元,到 2031 年達到 21.7 億美元,2026 年至 2031 年的複合年成長率預計為 8.9%。

本報告按收割機類型(自走式、牽引式等)、操作模式(手動、輔助、精準導航等)、動力來源(柴油、混合動力、電力)、葡萄園規模(小規模葡萄園(小於50公頃)等)和地區(北美、南美、歐洲等)進行分類。市場預測以美元計價。

全球葡萄採摘機市場趨勢及洞察

由於人手不足,機械化程度迅速提高。

葡萄園人手不足是全部區域面臨的持續挑戰,促使人們採用機械化葡萄採摘解決方案。美國農業部 (USDA) 報告稱,2025 年 H-2A 簽證核准數量將增加,薪資成長速度將超過其他農業部門。在澳大利亞,2025 年合約採摘價格將達到每小時 345 美元(525 澳元),遠高於人工採摘的成本,從而加速了自動化採摘機的採購。在德國,2025 年的人手不足將導致葡萄產量比過去十年的平均值下降 16%,促使傳統酒莊轉向機械化。加州納帕谷的一家高階酒莊在 2025 年實施了夜間機械化採摘,以應對人手不足並保持葡萄的酸度。由於人事費用超過了葡萄價格的成長速度,自動化解決方案對於確保盈利至關重要。

主要生產商之間的葡萄園整合

產業整合正將需求從數千家小規模酒莊轉移到少數資本密集買家手中。在美國,2025年6月,葡萄酒集團(Wine Group)從星座品牌(衛星群 Brands)手中收購了6,600英畝土地,擴大了對機械化採收設備的需求。同月,總部位於加州的阿特拉斯葡萄園管理公司(Atlas Vineyard Management)收購了總部位於奧勒岡州的Results Partners公司。此次收購使其在奧勒岡州的管理面積擴大到9000英畝,並促成了多單位採收合約的簽訂。大規模酒莊正致力於品牌標準化,這需要統一的數據介面,並推動自動駕駛技術的應用,以緩解季節性勞動力短缺問題。隨著併購的推進,訂單越來越集中在配備先進感測器的高產能平台。

高初始投資

大量初始投資阻礙了採收機械的普及,尤其對於小規模、分散的葡萄園主更是如此。入門級自走式採收機的價格約為 8 萬美元,而高級型號的價格則超過 40 萬美元,這使得小規模生產商難以負擔。在歐洲,超過一半的葡萄園面積不足一公頃,儘管有補貼計劃,但機械利用率和投資回報率仍然很低。在許多非機械化市場地區,例如美國的加州和澳大利亞,租賃和合約服務的不完美進一步減緩了機械化的普及。高成本和資金籌措繼續限制機械化採收機的使用,尤其是在小規模葡萄園和傳統葡萄酒產區。

細分市場分析

到2025年,自走式葡萄收割機將佔48.5%的市場佔有率,這反映了其在200公頃以上農場的生產力優勢。從2026年到2031年,曳引機式葡萄收割機預計將以11.8%的複合年成長率成為葡萄收割機市場規模成長最快的機型,因為生產商正在充分利用現有動力。牽引式收割機目前已被應用於各種類型的農場,實現了不同作物間的機器輪換,並擴展了其在葡萄以外的效用。高容量自走式收割機,例如Pellenc OPTIMUM XXL80,配備了遙測功能,可在每次作業後記錄並上傳產量資料。同時,高階酒莊仍偏好自走式收割機,看重其能夠減少曳引機造成的土壤壓實並提升清洗效率。

曳引機式設備的激增主要源自於對資本效率的追求。包括GREGOIRE在內的葡萄園設備製造商正在拓展其產品線,推出相容ISOBUS的曳引機式平台。這些平台不僅滿足精密農業和數位化監測的需求,還能降低擁有成本。製造商正致力於開發可適應各種配置和相容振動篩技術的模組化平台。

到2025年,配備GPS導航和攝影機分類機以輔助人工監控的輔助式和精準導航式葡萄收割機將佔據54.2%的市場佔有率。人工收割機仍存在於歐洲老舊的基礎設施中,但其市場佔有率仍不足葡萄收割機市場的三分之一。預計2026年至2031年間,自主和半自動作業的成長率將最高,複合年成長率將達13.2%。這主要得益於感測器整合系統的日益普及,這些系統減少了對人工的依賴。 2024年2月,在澳洲杜克斯頓葡萄園進行的一項測試表明,自主曳引機能夠有效率地將樹冠資料傳輸到收割機的控制系統,引導收割機沿著最佳路徑作業。同時,法律規範也在發生變化,在設有地理圍欄的私人土地上進行無人作業正變得越來越合法。

儘管前景光明,但轉型成本是推廣應用的主要障礙。自動駕駛系統比駕駛輔助系統成本更高。然而,考慮到加州的加班費,全天候自動駕駛在經濟上頗具吸引力。在歐盟,嚴格的資料隱私法規要求使用安全的雲端服務。這促使目的地設備製造商 (OEM) 建立區域資料中心。此外,考慮購買自動駕駛系統的公司在做出決定前,會將責任責任險費用作為關鍵因素。

區域分析

到2025年,歐洲將佔據葡萄採摘機械市場37.1%的主導地位。法國、義大利和西班牙先進的機械化水準為此提供了有力支撐。歐盟通用農業政策(CAP)為該地區提供了11.2億美元(10.61億歐元)的巨額資金,重點用於主要葡萄酒產區的車輛現代化和精密農業發展。氣候變遷的影響凸顯,預計2025年德國的葡萄收成將下降,這促使一些傳統上較為保守的葡萄園主開始採用機械化採摘。為了現代化,義大利已撥款1.52億美元(1.441億歐元)用於2026年的葡萄園改造,重點是採摘機械的現代化。在以老牌製造商為主導的歐洲市場,輕便、數位化程度高、燃油效率高的採摘機械的需求正在顯著成長,尤其是在高階葡萄園和梯田式阿爾卑斯山葡萄園。

在亞太地區,葡萄採摘機市場預計將在2026年至2031年間以9.4%的複合年成長率穩定成長。在中國,寧夏的葡萄酒廠正在推動現代化改造,並在地區補貼的支持下降低了機械引進成本,以應對國內葡萄酒產量下降的情況。在澳大利亞,人事費用的上漲將導致機械租賃費用在2025年達到每小時約345美元,加速了大規模葡萄園中自動採摘機的試點部署。同時,在印度,馬哈拉斯特拉邦拉邦政府已將機械化津貼範圍擴大到葡萄採摘機,這表明新興商業葡萄園對機械化的接受度正在不斷提高。

在北美,受主要葡萄酒產區葡萄園整合的推動,對高產能葡萄採摘機的需求激增。一些引人注目的收購,例如葡萄酒集團(The Wine Group)計劃於2025年收購佔地6600英畝的大型葡萄園,正在為引入高效採摘系統鋪平道路,從而減少對勞動力的依賴。同時,製造商正在加強區域供應鏈並提升售後服務。 Oxbo位於紐約的工廠就是一個典型的例子,該工廠正在改善東海岸葡萄園(這些葡萄園往往被忽視)的零件供應和服務速度。在南美洲,智利和阿根廷的葡萄酒生產商都在增加對機械化的投資,旨在降低生產成本、確保穩定的收成並增強出口競爭力,尤其是在人事費用不斷上漲的情況下。同時,在中東和非洲,儘管機械化仍處於起步階段,但我們看到選擇性機械化方面正在取得進展。在南非西開普省和土耳其色雷斯等仍嚴重依賴勞動力的地區,商業葡萄園正在投資現代化的收割設備,以提高營運效率並維持出口品質。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於人手不足,機械化程度迅速提高。

- 主要葡萄酒生產商對葡萄園的整合

- 政府對機械化的補助和稅額扣抵

- 引進需要數據驅動型機械的精準葡萄栽培技術。

- 新型租賃和訂閱式所有權模式

- 輕型自推進微型收割機的研發

- 市場限制因素

- 大量初始資本投資

- 操作人員技能和維護複雜性

- 人們對手工採摘的優質品種的品質表示擔憂

- 陡峭葡萄園的適用性局限性

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按收割機類型

- 自走式葡萄收割機

- 拖曳式/拖曳式葡萄收割機

- 曳引機式葡萄收割機

- 透過操作模式

- 手動轉向和操作

- 輔助駕駛/精準引導駕駛

- 自動駕駛/半自動駕駛

- 透過動力來源

- 柴油收割機

- 混合收割機

- 電動收割機

- 葡萄園面積

- 小規模葡萄園(少於50公頃)

- 中型葡萄園(51-200公頃)

- 大型葡萄園(超過200公頃)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 法國

- 義大利

- 西班牙

- 德國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 澳洲

- 日本

- 印度

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 摩洛哥

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pellenc SAS

- New Holland Agriculture-Braud(CNH Industrial NV)

- Oxbo International Corporation(Ploeger Oxbo Group BV)

- Gregoire SAS(SDF SpA)

- ERO GmbH

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Alma SRL

- CRF Costruzioni SRL

- Blueline Manufacturing Company

- American Grape Harvesters Inc.

- Bobard SAS

- Nairn Harvesters Limited

- Reese Group Ltd.

- Weremczuk FMR Sp. z oo

第7章 市場機會與未來展望

According to Mordor Intelligence, the grape harvesting machinery market size is anticipated to increase from USD 1.31 billion in 2025 to USD 1.42 billion in 2026 and reach USD 2.17 billion by 2031, growing at a CAGR of 8.9% during 2026-2031.

This report is Segmented by Harvester Type (Self-Propelled, Trailed or Towed, and More), by Mode of Operation (Manual, Assisted or Precision-Guided, and More), by Power Source (Diesel, Hybrid, and Electric), by Vineyard Size ( Small Vineyards (Below 50 Hectares), and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value in USD.

Global Grape Harvesting Machinery Market Trends and Insights

Labor-Shortage Driven Mechanization Surge

Labor shortages in vineyard operations are becoming a persistent challenge across major wine-producing regions, driving the adoption of mechanized grape harvesting solutions. The United States Department of Agriculture (USDA) reported rising H-2A certifications in 2025 and wage inflation that outpaced other farm sectors. Australia experienced contract-harvesting fees of USD 345 (AUD 525) per hour in 2025, dwarfing hand-picking costs and accelerating the purchase of automated pickers. Germany's 2025 harvest fell 16% below the ten-year average due to crew shortages, prompting traditional estates to turn to machinery. Premium properties in Napa Valley, California, United States, adopted night mechanical picking in 2025 to address labor shortages and maintain fruit acidity. With labor costs rising faster than grape prices, automated solutions have become critical to ensuring profitability.

Vineyard Consolidation Among Large Producers

Consolidation shifts demand from thousands of small owners to a few capital-intensive buyers. In the United States, the Wine Group acquired 6,600 acres from Constellation Brands in June 2025, expanding its mechanized fleet requirement . Atlas Vineyard Management, headquartered in California, United States, acquired Results Partners, based in Oregon, United States, during the same month. This acquisition expanded its managed acreage in Oregon to 9,000, facilitating multi-unit harvester contracts. Larger estates are focusing on standardizing brands, requiring uniform data interfaces, and advocating for autonomous features to mitigate seasonal labor demands. As mergers progress, order volumes are increasingly concentrated on high-capacity platforms equipped with advanced sensors.

High Upfront Capital Expenditure

High capital requirements hinder the adoption of grape harvesting machinery, especially for small, fragmented vineyard operators. Entry-level self-propelled harvesters cost around USD 80,000, while advanced models exceed USD 400,000, limiting affordability for small-scale growers. In Europe, where over half of vineyards span less than 1 hectare, low machinery utilization and return on investment persist despite subsidy programs. Underdeveloped rental and contractor-based services in many regions outside mechanized markets, such as California, the United States, and Australia, further slow adoption. High costs and limited financing continue to restrict the use of mechanized harvesters, particularly in smaller vineyards and traditional wine regions.

Other drivers and restraints analyzed in the detailed report include:

- Government Mechanization Subsidies and Tax Credits

- Precision-Viticulture Adoption Requiring Data-Ready Machinery

- Operator-Skill and Maintenance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled machines captured 48.5% of the grape harvesting machinery market share in 2025, reflecting productivity advantages for estates above 200 hectares. Tractor-mounted units posted the fastest 11.8% CAGR over 2026-2031 in the grape harvesting machinery market size as growers leverage existing horsepower. Harvesters designed for trailing are now serving a diverse range of farms, enabling equipment rotation across various crops and broadening their utility beyond grapes. High-capacity self-propelled models, such as the Pellenc OPTIMUM XXL80, come equipped with telemetry features that record and upload yield data with every pass. Meanwhile, premium wineries continue to favor self-propelled machines, valuing their ability to reduce tractor compaction and enhance cleaning modules.

Driving the surge in tractor-mounted units is a focus on capital efficiency. Manufacturers, including GREGOIRE and other vineyard equipment providers, are broadening their offerings with ISOBUS-compatible tractor-mounted platforms. These platforms not only align with precision agriculture and digital monitoring needs but also offer lower ownership costs. Manufacturers are focusing on modular platforms and interchangeable shaker technologies compatible with various configurations.

Assisted and precision-guided harvesters held the largest share, 54.2%, in 2025, driven by GPS steering and camera sorters that augment human oversight. Manual machines linger in aging European fleets, yet account for less than one-third of the grape harvesting machinery market. Autonomous/Semi-Autonomous operations are projected to register the fastest CAGR of 13.2% during 2026-2031, driven by increasing adoption of sensor-integrated systems that reduce dependence on manual labor. In February 2024, trials at Duxton Vineyards in Australia demonstrated that autonomous tractors can efficiently transmit canopy data to harvester controls, guiding pickers along optimal paths. Meanwhile, regulatory frameworks are adapting to authorize driverless operations on geofenced private lands.

Despite the promise, transition costs pose a significant barrier to adoption. Autonomous systems come with a higher price tag than their assisted counterparts. Yet, California's overtime premiums render round-the-clock driverless operations financially appealing. In the European Union, stringent data privacy regulations mandate the use of secure cloud services. This has prompted Original Equipment Manufacturers (OEMs) to set up regional data centers. Furthermore, potential buyers are weighing liability insurance premiums as a crucial factor before finalizing their purchases.

Geography Analysis

In 2025, Europe commanded a dominant 37.1% share of the grape harvesting machinery market, bolstered by advanced mechanization in France, Italy, and Spain. The region benefited from robust funding of USD 1.12 billion (EUR 1.061 billion) from the Annual Common Agricultural Policy, underscoring its commitment to fleet renewal and precision agriculture in key wine-producing areas. Highlighting the impact of climate volatility, Germany's 2025 crop shortfall nudged its traditionally conservative vineyard estates towards embracing mechanized harvesting. In a bid to modernize, Italy earmarked USD 152 million (EUR 144.1 million) for vineyard restructuring in 2026, with a focus on harvester upgrades. The European market, dominated by established manufacturers, is witnessing a pronounced shift in demand towards lightweight, digitally advanced, and fuel-efficient harvesting units, particularly for premium vineyards and Alpine terrace cultivation.

Asia-Pacific is set to witness a robust 9.4% CAGR in the grapes harvesting machinery market between 2026 and 2031. In China, Ningxia estates are modernizing their operations to counteract a dip in national wine output, bolstered by regional subsidies that ease machinery costs. In Australia, wage pressures have driven machinery hire rates to nearly USD 345 per hour in 2025, spurring large vineyard estates to accelerate trials of autonomous harvesting. Meanwhile, in India, the Maharashtra government is expanding mechanization grants to include grape pickers, signaling growing acceptance of mechanization in emerging commercial vineyards.

North America is witnessing a surge in demand for high-capacity grape harvesting machinery, fueled by increasing vineyard consolidation in major wine-producing states. Notable acquisitions, such as The Wine Group's 2025 buyout of a sprawling 6,600-acre vineyard, are paving the way for efficient harvesting fleets that promise reduced labor reliance. Concurrently, manufacturers are bolstering regional supply chains and enhancing aftermarket services. A case in point is Oxbo's New York facility, which is amplifying parts accessibility and service responsiveness for the often-overlooked East Coast vineyards. In South America, both Chilean and Argentine wine producers are ramping up investments in mechanization. Their goal: to curtail production costs, ensure consistent harvests, and bolster their competitive edge in exports, especially in light of rising labor costs. Meanwhile, the Middle East and Africa, still in the nascent stages of adoption, are witnessing selective mechanization growth. Regions like South Africa's Westerreliance on labormore amidn Cape and Turkey's Thrace are seeing commercial vineyards invest in modern harvesting tools, aiming to boost operational efficiency and maintain export quality.

- Pellenc S.A.S.

- New Holland Agriculture - Braud (CNH Industrial N.V.)

- Oxbo International Corporation (Ploeger Oxbo Group B.V.)

- Gregoire S.A.S. (SDF S.p.A.)

- ERO GmbH

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Alma S.R.L.

- CRF Costruzioni S.R.L.

- Blueline Manufacturing Company

- American Grape Harvesters Inc.

- Bobard S.A.S.

- Nairn Harvesters Limited

- Reese Group Ltd.

- Weremczuk FMR Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor-shortage driven mechanization surge

- 4.2.2 Vineyard consolidation among large wine producers

- 4.2.3 Government mechanization subsidies and tax credits

- 4.2.4 Precision-viticulture adoption requiring data-ready machinery

- 4.2.5 Emerging rental and subscription ownership models

- 4.2.6 Development of lightweight self-propelled micro-harvesters

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Operator-skill and maintenance complexity

- 4.3.3 Quality concerns for premium hand-picked varietals

- 4.3.4 Limited suitability on extreme-slope vineyards

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Harvester Type

- 5.1.1 Self-Propelled Grape Harvesters

- 5.1.2 Trailed / Towed Grape Harvesters

- 5.1.3 Tractor-Mounted Grape Harvesters

- 5.2 By Mode of Operation

- 5.2.1 Manual Steering & Operation

- 5.2.2 Assisted / Precision-Guided Operation

- 5.2.3 Autonomous / Semi-Autonomous Operation

- 5.3 By Power Source

- 5.3.1 Diesel-Powered Harvesters

- 5.3.2 Hybrid Harvesters

- 5.3.3 Electric Harvesters

- 5.4 By Vineyard Size

- 5.4.1 Small Vineyards (Below 50 Hectares)

- 5.4.2 Medium Vineyards (51-200 Hectares)

- 5.4.3 Large Vineyards (Above 200 Hectares)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 France

- 5.5.3.2 Italy

- 5.5.3.3 Spain

- 5.5.3.4 Germany

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Australia

- 5.5.4.3 Japan

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Morocco

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Pellenc S.A.S.

- 6.4.2 New Holland Agriculture - Braud (CNH Industrial N.V.)

- 6.4.3 Oxbo International Corporation (Ploeger Oxbo Group B.V.)

- 6.4.4 Gregoire S.A.S. (SDF S.p.A.)

- 6.4.5 ERO GmbH

- 6.4.6 Kubota Corporation

- 6.4.7 Yanmar Holdings Co., Ltd.

- 6.4.8 Alma S.R.L.

- 6.4.9 CRF Costruzioni S.R.L.

- 6.4.10 Blueline Manufacturing Company

- 6.4.11 American Grape Harvesters Inc.

- 6.4.12 Bobard S.A.S.

- 6.4.13 Nairn Harvesters Limited

- 6.4.14 Reese Group Ltd.

- 6.4.15 Weremczuk FMR Sp. z o.o.