|

市場調查報告書

商品編碼

2063969

360度回饋軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)360-Degree Feedback Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

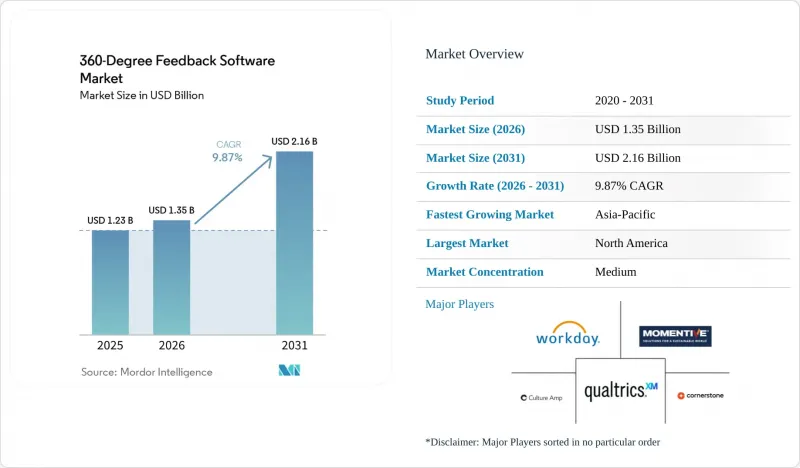

根據 Mordor Intelligence 預測,360 度回饋軟體市場將從 2025 年的 12.3 億美元成長到 2026 年的 13.5 億美元,然後在 2031 年達到 21.6 億美元,2026 年至 2031 年的複合年成長率為 9.87%。

本報告按元件(軟體和服務)、部署類型(雲端、本地部署、混合部署)、企業規模(中小企業和大型企業)、產業(IT與電信、銀行、金融服務和保險、醫療保健和生命科學等)、定價模式(訂閱等)以及地區進行細分。市場預測以美元計價。

全球360度回饋軟體市場趨勢及洞察

人工智慧驅動的個人化回饋工作流程

生成式人工智慧 (AI) 透過根據個人能力差距客製化問題集,並將原始的多層次數據快速轉化為輔導建議,從而將洞察的前置作業時間從數週縮短至數小時。微軟 Viva Glint、SAP SuccessFactors 和 Oracle HCM Cloud 都已發布了主動式 AI 功能,這些功能可以視覺化情緒趨勢並指出績效不一致之處,促使 48% 的歐洲人力資源團隊計劃在 2025 年前試用專用 AI 績效工具。無法整合即時個人化和偏見篩檢功能的供應商將面臨價格競爭的風險,因為買家越來越將這些功能視為「必備條件」。

將360度回饋整合到持續績效管理套件中

隨著季度績效考核取代年度績效評估,企業被迫將回饋、目標追蹤和同儕評價整合到統一的工作流程中。 Workday 於 2025 年斥資 11 億美元收購 Sana,被視為其將人工智慧驅動的人才智慧整合到整個人力資本管理 (HCM) 套件中的一項舉措,凸顯了高度整合的分析技術如今對繼任計劃和技能發展產生的重大影響。因此,在 360 度回饋軟體市場,套件整合成為一項關鍵的採購標準,迫使獨立供應商決定是自主開發還是尋求合作夥伴。

對資料隱私和心理測量偏差的擔憂

諸如GDPR和加州ADMT等嚴格的法律法規要求演算法決策更加透明,這增加了供應商的合規成本,也提高了訴訟風險。 2025年發表在《應用心理學雜誌》上的一篇報導指出,大型企業中30%的評估結果受到評估人員的偏見影響,導致買家要求提供加密、審計日誌和統計偏差檢查。在這些安全措施方面落後的供應商將面臨採購延誤和聲譽受損的風險。

細分市場分析

到2025年,軟體收入將佔360度回饋軟體市場總收入的78.92%,反映出授權和訂閱費用的主導地位。然而,預計到2031年,服務領域的複合年成長率將達到10.96%,高於整體市場成長率。根據SurveyConnect的研究,員工人數超過5,000人的公司中,40%的人力資源部門無法在一個月內創建可操作的儀表板,這推動了對諮詢服務的需求。因此,供應商現在正將季度校準研討會納入其高級套餐,並將軟體和服務整合到單一訂閱中。

360度回饋軟體市場正受惠於服務夥伴透過評估員培訓、心理測量檢驗和文化轉型藍圖來實現獲利。這一趨勢在需要第三方認證的高度監管行業中尤為顯著,例如GDPR和醫療保健認證。 Paychex於2025年1月宣布以41億美元收購Paycor,凸顯了在約74.5萬家合併基本客群中,透過交叉銷售實施方案和諮詢服務所帶來的巨大收入協同效應,以及預計每年超過8000萬美元的成本協同效應。

到2025年,雲端採用將佔據360度回饋軟體市場佔有率的69.14%,這主要得益於其可擴展性、自動化更新和較低的初始資本投入。然而,混合配置預計到2031年將以11.42%的複合年成長率成長,成為所有採用模式中成長率最高的。阿拉伯聯合大公國法規強制要求聯邦政府僱員記錄必須儲存在國內,這推動了人們對託管在國內資料中心的私有雲端節點的興趣。 SAP的2026版SuccessFactors展示了領先供應商如何平衡資料主權和敏捷性,利用雲端基礎架構實現即時人工智慧,同時支援客戶管理的獎勵文件儲存。

混合架構對金融服務、醫療保健和政府機構極具吸引力,因為這些機構必須在資料主權要求與雲端原生平台的敏捷性和人工智慧能力之間取得平衡。在傳統的製造業和國防相關企業中,由於空氣間隙網路和嚴格的網路安全協定的限制,雲端連接受到限制,因此本地部署仍然普遍存在。然而,隨著供應商逐步停止對本地部署的支持,轉而支持託管在客戶管理的資料中心中的私有雲端實例,這個細分市場正在萎縮。

區域分析

預計到2025年,北美地區的收入將佔全球總收入的39.28%,主要得益於財富500強企業跨平台部署以及重視透明人才流程的合規環境。聯邦承包商正轉向混合部署模式,導致合約週期延長,但隨著採購者增加諮詢和安全模組,平均合約價值也在不斷攀升。該地區也受益於人工智慧賦能的人力資源工具的早期應用,不僅強化了數據主導的決策,也加速了平台升級。此外,強大的供應商生態系統和高水準的人力資源技術投資能力進一步鞏固了北美地區的領先地位。

儘管歐洲的銷售成長放緩,但由於GDPR提高了供應商轉換成本,合約續約率依然強勁。 Lattice的數據顯示,51%的歐洲公司會進行季度評估,這顯示市場對持續回饋機制的需求十分旺盛。由於嚴格的法律監管,買家更傾向於選擇能夠提供清晰審計追蹤和自動刪除工作流程的平台,而這種複雜性也保護了現有供應商的市場滲透率。這種法規環境有利於與供應商建立長期合作關係,並增加了對合規的企業級解決方案的需求。此外,對多語言員工的需求也進一步提升了對可客製化和在地化平台的需求。

亞太地區的需求成長勢頭強勁,複合年成長率高達12.36%。印度供應商如Darwinbox正在對勞動法進行在地化,並提供本地語言介面;中國國有企業則在國家數位化專案的推動下,推動人才管理現代化。在日本和韓國,人們仍然普遍存在向上級反饋的文化抵觸情緒,因此供應商正致力於開發匿名保障和小組討論模式,以在不違背“面子”觀念的前提下維護用戶信任。中小企業的快速數字化轉型以及對低成本SaaS的廣泛應用,也正在擴大全部區域的目標市場。此外,政府主導的數位轉型(DX)舉措的增加,也加速了企業採用結構化回饋系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧驅動的個人化回饋工作流程

- 將360度回饋整合到持續績效管理系統中。

- 擴大混合辦公和遠距辦公模式

- 對數據驅動型領導力發展專案的需求日益成長

- 透過免費增值模式的市場推廣策略,擴大新興市場中小企業的採用率。

- 監理機構越來越重視客觀的員工評價

- 市場限制因素

- 對資料隱私和心理測量偏差的擔憂

- 傳統層級文化中變革管理的挑戰

- 微企業人力資源技術預算的限制

- 與傳統HCM/ERP系統的互通性差距

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 不同的發展

- 雲

- 現場

- 混合

- 按組織規模

- 小型企業

- 大公司

- 按行業分類

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 政府/公共部門

- 其他工業部門

- 定價模式

- 基於訂閱

- 永久許可證/一次許可證

- 按使用量計費/計量收費

- 免費增值

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Culture Amp Pty Ltd

- Qualtrics LLC

- Momentive Global Inc.

- Cornerstone OnDemand Inc.

- Workday Inc.

- Inspire Software Inc.

- Leapsome GmbH

- EchoSpan Inc.

- Spidergap Ltd

- Trakstar Inc.

- Reflektive Inc.

- SurveySparrow Inc.

- EngageRocket Pte. Ltd.

- Betterworks Systems Inc.

- PeopleGoal Ltd.

- 15Five Inc.

- AssessTEAM LLC

- ClearCompany Inc.

- Synergita Software Pvt. Ltd.

- Reviewsnap, LLC

- OrangeHRM Inc.

- PeopleFluent Holdings Corp.

- Lattice HR Inc.

- Saba Software Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the 360-degree feedback software market size is expected to grow from USD 1.23 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 9.87% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, and More), Pricing Model (Subscription-Based, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global 360-Degree Feedback Software Market Trends and Insights

AI-Driven Personalized Feedback Workflows

Generative AI now tailors question sets to individual competency gaps and rapidly converts raw multi-rater data into coaching prompts, slashing insight lead time from weeks to hours. Microsoft Viva Glint, SAP SuccessFactors, and Oracle HCM Cloud have all released agentic AI features that surface sentiment patterns and flag rating discrepancies, prompting 48% of European HR teams to pilot specialized AI performance tools in 2025. Vendors unable to embed real-time personalization or bias screening risk price erosion as buyers increasingly view those capabilities as table stakes.

Integration of 360-Degree Feedback into Continuous Performance Management Suites

Quarterly reviews are replacing annual appraisals, pushing organizations to converge feedback, goal tracking, and peer recognition into unified workflows. Workday's 2025 acquisition of Sana for USD 1.1 billion was framed as a move to weave AI-driven talent intelligence across its HCM suite, underscoring how tightly integrated analytics now shape succession planning and skill development. Stand-alone vendors, therefore, face a build-or-partner decision as cross-suite integration has become a primary buying criterion in the 360-degree feedback software market.

Concerns Over Data Privacy and Psychometric Bias

Strict statutes like GDPR and California ADMT now require transparency on algorithmic decision-making, elevating vendor compliance costs and amplifying litigation risk. A 2025 Journal of Applied Psychology article revealed that 30% of responses in large firms were skewed by rater bias, prompting buyers to demand encryption, audit logs, and statistical bias checks. Vendors lagging on these safeguards face procurement delays and potential reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hybrid and Remote Work Operating Models

- Rising Demand for Data-Driven Leadership Development Programs

- Change-Management Challenges in Traditional Hierarchical Cultures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 78.92% of market revenue of the 360-degree feedback software market in 2025, reflecting the dominance of license and subscription fees, yet services are projected to expand at 10.96% CAGR through 2031, outpacing the overall market rate. SurveyConnect observed that 40% of HR teams in firms above 5,000 employees failed to create actionable dashboards within a month, catalyzing demand for advisory projects. As a result, vendors now bundle quarterly calibration workshops into premium tiers, blending software and services in one subscription.

The 360-degree feedback software market benefits as service partners monetize rater-training, psychometric validation, and culture-change roadmaps, especially in regulated verticals where GDPR or healthcare accreditation demands third-party attestation. Paychex's January 2025 announcement of its USD 4.1 billion acquisition of Paycor highlighted expected run-rate cost synergies exceeding USD 80 million, with substantial revenue synergy opportunities tied to cross-selling implementation and advisory services across a combined customer base of approximately 745,000 clients.

Cloud deployment commanded 69.14% of the 360-degree feedback software market share in 2025, driven by scalability, automatic updates, and lower upfront capital expenditure, yet hybrid configurations are growing at 11.42% CAGR through 2031, the fastest rate among deployment models. UAE regulations that require federal employee records to stay on national soil have spurred interest in private cloud nodes hosted in domestic data centers. SAP's 2026 SuccessFactors release leverages cloud infrastructure for real-time AI while supporting customer-controlled storage for compensation files, illustrating how large vendors balance sovereignty and agility.

Hybrid architectures appeal to financial services, healthcare, and government entities that must balance data sovereignty mandates with the agility and AI capabilities of cloud-native platforms. On-premises deployments persist in legacy manufacturing firms and defense contractors where air-gapped networks and stringent cybersecurity protocols prohibit cloud connectivity, though this segment is contracting as vendors phase out on-premises support in favor of private cloud instances hosted in customer-controlled data centers.

Geography Analysis

North America generated 39.28% of 2025 revenue, sustained by Fortune 500 cross-suite expansions and a compliance environment that rewards transparent talent processes. Federal contractors moving to hybrid deployments have lengthened deal cycles but lifted average contract value as buyers layer advisory and security modules. The region also benefits from early adoption of AI-enabled HR tools, which enhances analytics-driven decision-making and accelerates platform upgrades. Additionally, strong vendor ecosystems and high HR tech spending capacity continue to reinforce North America's leadership position.

Europe posts slower topline growth yet enjoys sticky renewal rates because GDPR heightens vendor switching costs. Lattice data show 51% of European firms run quarterly reviews, cementing demand for continuous feedback loops. High legal scrutiny means buyers favor platforms that provide clear audit trails and automated deletion workflows, adding complexity that protects incumbent penetration. This regulatory environment encourages long-term vendor relationships and increases demand for compliant, enterprise-grade solutions. Moreover, multilingual workforce requirements further drive the need for customizable and localized platforms.

Asia-Pacific is the clear volume driver with a 12.36% CAGR. Indian vendors such as Darwinbox localize labor codes and offer vernacular interfaces while Chinese state-owned enterprises modernize talent oversight under national digitalization programs. Cultural hesitancy toward upward feedback persists in Japan and South Korea, so vendors invest in anonymity guarantees and group discourse formats that sustain user confidence without violating face-saving norms. Rapid SME digitization and cost-sensitive SaaS adoption are also expanding the addressable market across the region. In addition, increasing government-led digital transformation initiatives are accelerating enterprise adoption of structured feedback systems.

- Culture Amp Pty Ltd

- Qualtrics LLC

- Momentive Global Inc.

- Cornerstone OnDemand Inc.

- Workday Inc.

- Inspire Software Inc.

- Leapsome GmbH

- EchoSpan Inc.

- Spidergap Ltd

- Trakstar Inc.

- Reflektive Inc.

- SurveySparrow Inc.

- EngageRocket Pte. Ltd.

- Betterworks Systems Inc.

- PeopleGoal Ltd.

- 15Five Inc.

- AssessTEAM LLC

- ClearCompany Inc.

- Synergita Software Pvt. Ltd.

- Reviewsnap, LLC

- OrangeHRM Inc.

- PeopleFluent Holdings Corp.

- Lattice HR Inc.

- Saba Software Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Personalised Feedback Workflows

- 4.2.2 Integration of 360-Degree Feedback into Continuous Performance Management Suites

- 4.2.3 Expansion of Hybrid and Remote-Work Operating Models

- 4.2.4 Rising Demand for Data-Driven Leadership Development Programs

- 4.2.5 Growing Adoption Across Emerging-Market SMBs Via Freemium GTM Strategies

- 4.2.6 Increasing Regulatory Emphasis on Objective Employee Evaluations

- 4.3 Market Restraints

- 4.3.1 Concerns Over Data Privacy and Psychometric Bias

- 4.3.2 Change-Management Challenges in Traditional Hierarchical Cultures

- 4.3.3 Limited HR Tech Budgets in Micro-enterprises

- 4.3.4 Interoperability Gaps with Legacy HCM/ERP Stacks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium-sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 By Pricing Model

- 5.5.1 Subscription-Based

- 5.5.2 Perpetual / One-Time License

- 5.5.3 Usage-Based / Pay-Per-Use

- 5.5.4 Freemium

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Culture Amp Pty Ltd

- 6.4.2 Qualtrics LLC

- 6.4.3 Momentive Global Inc.

- 6.4.4 Cornerstone OnDemand Inc.

- 6.4.5 Workday Inc.

- 6.4.6 Inspire Software Inc.

- 6.4.7 Leapsome GmbH

- 6.4.8 EchoSpan Inc.

- 6.4.9 Spidergap Ltd

- 6.4.10 Trakstar Inc.

- 6.4.11 Reflektive Inc.

- 6.4.12 SurveySparrow Inc.

- 6.4.13 EngageRocket Pte. Ltd.

- 6.4.14 Betterworks Systems Inc.

- 6.4.15 PeopleGoal Ltd.

- 6.4.16 15Five Inc.

- 6.4.17 AssessTEAM LLC

- 6.4.18 ClearCompany Inc.

- 6.4.19 Synergita Software Pvt. Ltd.

- 6.4.20 Reviewsnap, LLC

- 6.4.21 OrangeHRM Inc.

- 6.4.22 PeopleFluent Holdings Corp.

- 6.4.23 Lattice HR Inc.

- 6.4.24 Saba Software Inc.

- 6.4.25 BambooHR LLC

- 6.4.26 Zoho Corporation Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

雲端商業分析市場:2026-2032年全球市場預測(按組件、分析類型、資料類型、部署模型、組織規模、應用程式和最終用戶分類)

雲端商業分析市場:2026-2032年全球市場預測(按組件、分析類型、資料類型、部署模型、組織規模、應用程式和最終用戶分類) 個人化學習分析市場預測至2034年-按組件、部署模式、分析類型、技術、應用、最終用戶和地區分類的全球分析

個人化學習分析市場預測至2034年-按組件、部署模式、分析類型、技術、應用、最終用戶和地區分類的全球分析 2026年全球讀取檢測與分析市場報告

2026年全球讀取檢測與分析市場報告 商業分析市場報告:按軟體、部署類型、最終用戶、行業和地區分類(2026-2034 年)基於SaaS的商業分析市場:依架構類型、部署模式、組織規模、分析類型和產業分類-2026年至2032年全球市場預測商業分析市場:按類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測2026年全球商業分析與企業軟體市場報告2026年全球360度回饋軟體市場報告

商業分析市場報告:按軟體、部署類型、最終用戶、行業和地區分類(2026-2034 年)基於SaaS的商業分析市場:依架構類型、部署模式、組織規模、分析類型和產業分類-2026年至2032年全球市場預測商業分析市場:按類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測2026年全球商業分析與企業軟體市場報告2026年全球360度回饋軟體市場報告 全球資料提取市場規模、佔有率、趨勢和成長分析報告(2026-2034年)按部署模式、定價模式、應用領域和客戶類型分類的簡報撰寫和分析軟體市場,全球預測(2026-2032 年)

全球資料提取市場規模、佔有率、趨勢和成長分析報告(2026-2034年)按部署模式、定價模式、應用領域和客戶類型分類的簡報撰寫和分析軟體市場,全球預測(2026-2032 年)