|

市場調查報告書

商品編碼

2063924

北美學習管理系統 (LMS):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)North America Learning Management Systems (LMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

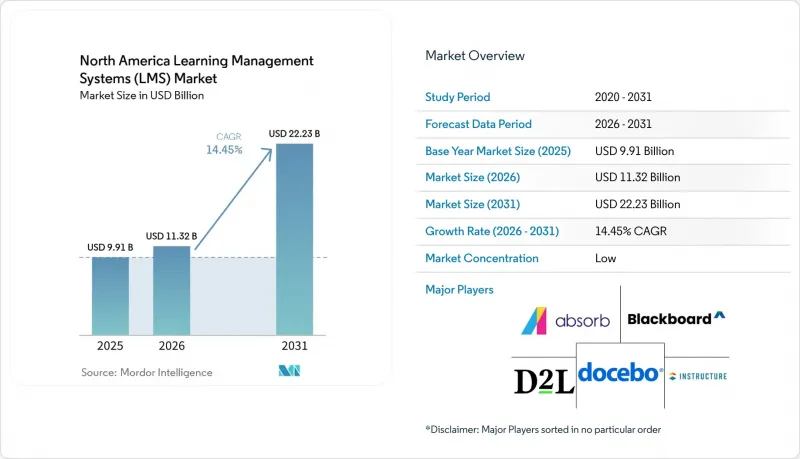

根據 Mordor Intelligence 預測,北美學習管理系統 (LMS) 市場規模將從 2025 年的 99.1 億美元和 2026 年的 113.2 億美元成長到 2031 年的 222.3 億美元,2026 年至 2031 年的複合年成長率為 14.45%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)、學習類型(學術學習等)、企業規模(大型企業和中小企業)、產業(資訊科技和電信等)以及地區進行細分。市場預測以美元計價。

北美學習管理系統(LMS)市場趨勢與洞察

企業技能發展和合規性的數位化

北美學習管理系統 (LMS) 市場正獲得雇主的持續支持,他們現在將技能提升不再僅僅視為偶爾的人才培育舉措,而是視為營運需求。 2026 年 1 月,Instructure 宣布 Canvas Career 正式上線,旨在支持以技能為導向的員工學習和成人學習者的與勞動力市場需求相符的教育計畫。這凸顯了該平台的需求與招募和內部調動需求之間的緊密聯繫。受監管的採購負責人也在保持支出穩定,因為他們需要記錄並建立搜尋的培訓完成情況、認證狀態和學習者記錄,以服務大規模的用戶群體。 TotaraGov 表示,其平台已被 50 多個美國政府機構使用,其中包括美國農業部的 AgLearn 環境,該環境在 30 個機構擁有 14 萬用戶,這表明可審計的數位化學習已深度融入公共部門的運作。 Docebo 也宣布與美國主要的金融服務監管機構簽訂契約,強調了學習系統在高度監管環境下的重要性。這些技能、壓力和持續的合規要求共同為北美學習管理系統市場創造了強大的需求基礎,即使一般的軟體預算受到嚴格審查。

引入人工智慧驅動的個人化和學習分析

北美學習管理系統 (LMS) 市場正從簡單的內容傳送轉向支援即時學習決策的平台。 2026 年 4 月,Docebo 發布了 AgentHub,它將學習交付、企業知識、技能智慧和基於代理的人工智慧整合到一個統一的環境中,這表明供應商正在將 LMS 重新定義為更主動的系統層。 Litmos 正在推進影片評估,利用人工智慧和機器學習來評估學習者的語氣、清晰度和關鍵字使用情況,無需人工評分,從而擴展了分散式團隊的可擴展技能檢驗。 Instructure 還在 2026 年 4 月的 Canvas 層級更新中引入了 AI Nutrition Facts,使買家能夠清晰地了解人工智慧功能的工作原理及其處理過程。這些版本發布意義重大,因為許多教育機構、公共部門和受監管企業的買家都要求自動化能夠提高學習者的學習成果,同時又不損害管治或課責。因此,能夠展示高度透明的人工智慧工作流程的供應商正在北美學習管理系統市場中佔據更有利的地位。

對資料隱私和網路安全的擔憂

在北美學習管理系統市場,由於學生和員工資料管治的高度敏感性,其普及速度仍然緩慢。根據CoSN發布的《2025年全國學生資料隱私報告》,88%的學區教育科技負責人將學生資料隱私列為兩大優先事項之一,凸顯了該議題在教育相關採購決策中的關鍵性。報告也發現,只有43%的機構定期對其隱私實踐進行審計,顯示許多機構在擴展數位化學習應用的同時,仍在努力解決管治的不足。此外,CoSN的調查顯示,55%的受訪者擔心如何管理大量未經審查的課堂技術,這提高了學習管理系統供應商在添加人工智慧和第三方功能方面的門檻。因此,負責人在批准部署之前,會就資料存取、儲存、監控和機構管理等問題提出更嚴格的要求。因此,需求並未驟降,但在北美學習管理系統市場,對於注重隱私的市場區隔而言,普及之路更為漫長。

細分市場分析

2025年,北美學習管理系統市場中,解決方案將佔據71.44%的市場佔有率(按組件分類),這意味著軟體訂閱和平台許可仍將是主要的支出領域。服務板塊預計將以16.27%的複合年成長率成長,並預計在2026年至2031年間成為北美學習管理系統市場中成長最快的板塊。當前規模與未來成長之間的差距表明,買家越來越關注平台運營,而非平臺本身。從舊有系統遷移、與企業應用程式整合、人工智慧配置、學習者支援和持續最佳化,如今已成為許多大型客戶採購決策的重要組成部分。 Instructure獨家擁有K16 Solutions,能夠直接實現遷移需求的貨幣化,這表明供應商現在將服務視為戰略收入來源,而非外圍輔助服務。

因此,北美學習管理系統市場越來越重視超越初始設定之外的後續服務。中型企業買家也需要支持,因為許多企業缺乏內部團隊來管理學習整合、人工智慧策略調整和內容重組。這使得目標業務機會擴展到託管學習支援、營運管理和持續改進服務。 Absorb 的 2025 年藍圖重點介紹了人工智慧驅動的個人化學習、策略學習手冊和同儕學習社區,顯示即使是面向客戶的創新,在運作後也會產生新的部署和使用支援需求。隨著北美學習管理系統產業越來越依賴分析、自動化和遷移工作,服務將繼續快速發展,而解決方案將維持更大的收入基礎。

2025年,北美學習管理系統市場中,雲端部署將佔據65.32%的市場佔有率,這印證了從傳統基礎設施向雲端遷移的長期趨勢穩步推進。混合部署預計將在2026年至2031年間以15.34%的複合年成長率成長,成為該領域成長最快的部署類型。這一趨勢表明,許多買家並非將雲端部署與本地部署視為絕對選項。相反,他們正在建立分階段架構,在保留敏感儲存庫和本機管理功能的同時,將面向使用者的學習功能遷移到更靈活的環境中。 TotaraGov在公共部門的成功案例(已在美國50多個政府機構部署)表明,現代學習環境能夠在滿足嚴格的管治要求的同時,避免所有買家都必須遵循相同的架構路徑。

對於高等教育機構和政府機構而言,過渡的時機與最終目標架構同等重要,因為這需要確保在過渡期間訪問的連續性、原有內容的保存以及可靠的審計追蹤。 Instructure 與 K16 的夥伴關係正體現了這一點,其重點在於為從傳統平台遷移的教育機構提供課程遷移、評估資料遷移和結構維護服務。隨著領先供應商將人工智慧功能整合到現有產品層級中,而非僅限於客製化環境,雲端服務也變得越來越具有戰略意義。 Instructure 於 2026 年 4 月將 IgniteAI Agent 功能整合到 Canvas Next 中。 Docevo 的 2026 年發布週期也強調了透過其雲端平台持續提供人工智慧功能。在北美學習管理系統市場,混合部署正在彌合當前營運限制與向雲端主導學習環境長期過渡之間的差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業技能發展和合規性的數位化

- 引入人工智慧驅動的個人化和學習分析

- 建立混合式和非同步學習模式

- 以分散式培訓為導向的雲端原生學習管理系統現代化

- 檢驗的數位資格與基於技能的招募相結合

- 簡化資格認證的學習者記錄互通性和課責

- 市場限制因素

- 資料隱私和網路安全問題

- 整合傳統人力資源資訊系統 (HRIS)、學生資訊系統 (SIS) 和內容系統的複雜性。

- 各州在人工智慧和學生數據監管方面存在差異

- 學區網路保險和安全管理成本增加

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 不同的發展

- 雲

- 現場

- 混合

- 透過學習類型

- 學術學習

- 企業培訓

- 政府/公共培訓

- 技能發展/認證

- 最終用戶

- 資訊科技(IT)/通訊

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 製造和工業運營

- 零售與電子商務

- 教育

- 政府/公共部門

- 能源公用事業

- 媒體與娛樂

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Blackboard LLC

- Instructure, Inc.

- D2L Corporation

- Docebo Inc.

- Absorb Software Inc.

- Litmos US, LP

- Moodle Pty Ltd.

- Totara Learning Solutions

- LearnUpon

- 360LEARNING SA

- Epignosis LLC

- SkyPrep Inc.

- Axonify Inc.

- Meridian Knowledge Solutions

- Thinkific Labs Inc.

- Thought Industries

- Learning Pool

- Schoox

- Skilljar

- LearnWorlds(CY)Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america learning management systems (LMS) market size is projected to expand from USD 9.91 billion in 2025 and USD 11.32 billion in 2026 to USD 22.23 billion by 2031, registering a CAGR of 14.45% between 2026 and 2031.

This report is Segmented by Component (Solution, and Services), Deployment (Cloud, On-Premises, and Hybrid), Learning Type (Academic Learning, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Learning Management Systems (LMS) Market Trends and Insights

Enterprise Upskilling and Compliance Digitization

The North America learning management systems market is receiving steady support from employers that now treat reskilling as an operating requirement rather than an occasional talent initiative. Instructure announced the broad availability of Canvas Career in January 2026 to support skills-first workforce learning for adult learners and workforce-aligned education programs, underscoring how closely platform demand is now tied to employability and internal mobility needs. Regulated buyers are also keeping spending consistent because training completion, certification status, and learner records must be documented and retrievable across large user populations. TotaraGov states that its platform serves more than 50 U.S. government agencies, including USDA's AgLearn environment, which has 140,000 users across 30 agencies, demonstrating how deeply auditable digital learning is embedded in public-sector operations. Docebo also disclosed customer wins with a major U.S. financial services regulator, reinforcing the importance of learning systems in highly supervised environments. This blend of skills, pressure, and recurring compliance needs gives the North America learning management systems market a durable demand floor even when general software budgets face scrutiny.

AI-Powered Personalization and Learning Analytics Adoption

The North America learning management systems market is moving from basic content delivery toward platforms that guide learning decisions in real time. Docebo launched AgentHub in April 2026 to combine learning delivery, enterprise knowledge, skills intelligence, and agentic AI in a single environment, demonstrating how vendors are repositioning the LMS as a more active system layer. Litmos is promoting AI and machine learning video assessments that evaluate learner tone, clarity, and keyword use without manual grading, which expands scalable skills validation for distributed teams. Instructure also introduced AI Nutrition Facts within its April 2026 Canvas tier update, giving buyers clearer visibility into how AI-enabled features work and what they process. Those releases matter because many education, public-sector, and regulated enterprise buyers want automation that improves learner outcomes without weakening governance or explainability. As a result, vendors that can show transparent AI workflows are gaining a stronger position in the North America learning management systems market.

Data Privacy and Cybersecurity Concerns

The North America learning management systems market still faces slower procurement where student or employee data governance is highly sensitive. CoSN's 2025 National Student Data Privacy Report found that 88% of district ed-tech leaders ranked student data privacy as a top-two priority, underscoring how central this issue has become in education purchasing decisions. The same report showed that only 43% conducted regular audits of their privacy practices, indicating that many institutions are still working through governance gaps as they expand digital learning use. CoSN also found that 55% of respondents were concerned about managing the influx of unvetted classroom technologies, which raises the bar for LMS vendors adding AI and third-party capabilities. Buyers are therefore asking harder questions on data access, retention, oversight, and institutional control before approving deployments. The result is not a collapse in demand, but a longer path to conversion across privacy-sensitive segments of the North America learning management systems market.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid and Asynchronous Learning Normalization

- Cloud-Native LMS Modernization for Distributed Training

- Legacy HRIS, SIS, and Content-System Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 71.44% of the North America learning management systems market share by component in 2025, indicating that software subscriptions and platform licenses remained the core spending areas. Services are projected to grow at a 16.27% CAGR, marking the fastest expansion in the North America learning management systems market size by component from 2026 to 2031. That gap between current scale and future growth shows that buyers increasingly value the work around the platform rather than the platform itself. Migration from legacy systems, integration with enterprise applications, AI configuration, learner support, and ongoing optimization are now part of the buying decision in many larger accounts. Instructure's exclusive access to K16 Solutions directly monetizes migration demand and shows that vendors now treat services as a strategic revenue line rather than a peripheral attachment.

The North America learning management systems market is therefore placing more value on services that extend well beyond initial setup. Mid-market buyers also need support, as many lack in-house teams to manage learning integrations, AI policy tuning, and content restructuring. This is widening the addressable opportunity into managed learning support, operational administration, and continuous improvement work. Absorb's 2025 roadmap emphasized AI-driven personalized learning, strategic learning playbooks, and peer learning communities, which indicates that even customer-facing innovations can create new implementation and enablement needs after go-live. As the North America learning management systems industry becomes more dependent on analytics, automation, and migration work, services are likely to remain the faster-moving component, even as solutions maintain the larger revenue base.

Cloud deployment captured 65.32% of the North America learning management systems market by deployment mode in 2025, confirming that the long migration away from older infrastructure is well advanced. Hybrid deployment is projected to expand at a 15.34% CAGR from 2026 to 2031, which makes it the fastest-growing mode in this segmentation. That pattern shows that many buyers are not choosing between cloud and on-premises in absolute terms. They are instead building staged architectures that preserve sensitive repositories or local controls while moving user-facing learning functions into more flexible environments. TotaraGov's public-sector presence across more than 50 U.S. agencies demonstrates that modern learning deployments can meet strict governance requirements without forcing every buyer onto the same architectural path.

In higher education and government, migration timing often matters as much as the final target architecture, because institutions need continuity of access, preservation of legacy content, and dependable audit trails during transition periods. Instructure's K16 partnership reflects this reality by focusing directly on course migration, assessment transfer, and preservation of structure for institutions leaving older platforms. Cloud delivery is also becoming more strategic, as major vendors are placing new AI capabilities within existing product tiers rather than reserving them for custom environments. Instructure embedded IgniteAI Agent capabilities in Canvas Next during April 2026, and Docebo's 2026 release cycle highlighted continued delivery of AI-enabled features through its cloud platform. For the North America learning management systems market, hybrid deployment is serving as the bridge between current operational constraints and a longer-term move toward cloud-led learning environments.

List of Companies Covered in this Report:

- Blackboard LLC

- Instructure, Inc.

- D2L Corporation

- Docebo Inc.

- Absorb Software Inc.

- Litmos US, L.P.

- Moodle Pty Ltd.

- Totara Learning Solutions

- LearnUpon

- 360LEARNING SA

- Epignosis LLC

- SkyPrep Inc.

- Axonify Inc.

- Meridian Knowledge Solutions

- Thinkific Labs Inc.

- Thought Industries

- Learning Pool

- Schoox

- Skilljar

- LearnWorlds (CY) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise Upskilling and Compliance Digitization

- 4.2.2 AI-Powered Personalization and Learning Analytics Adoption

- 4.2.3 Hybrid and Asynchronous Learning Normalization

- 4.2.4 Cloud-Native LMS Modernization for Distributed Training

- 4.2.5 Verifiable Digital Credentials and Skills-Based Hiring Integration

- 4.2.6 Learner Record Interoperability and Short-Form Credential Accountability

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Concerns

- 4.3.2 Legacy HRIS, SIS, and Content-System Integration Complexity

- 4.3.3 Fragmented State AI and Student-Data Regulation

- 4.3.4 Rising Cyber-Insurance and Security-Control Costs for School Districts

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Learning Type

- 5.3.1 Academic Learning

- 5.3.2 Corporate Training

- 5.3.3 Government / Public Training

- 5.3.4 Skill Development / Certification

- 5.4 By End User Vertical

- 5.4.1 Information Technology (IT) and Telecommunications

- 5.4.2 Banking, Financial Services, and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing and Industrial Operations

- 5.4.5 Retail and E-commerce

- 5.4.6 Education

- 5.4.7 Government and Public Sector

- 5.4.8 Energy and Utilities

- 5.4.9 Media and Entertainment

- 5.5 By End User Enterprise Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium-sized Enterprises

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Blackboard LLC

- 6.4.2 Instructure, Inc.

- 6.4.3 D2L Corporation

- 6.4.4 Docebo Inc.

- 6.4.5 Absorb Software Inc.

- 6.4.6 Litmos US, L.P.

- 6.4.7 Moodle Pty Ltd.

- 6.4.8 Totara Learning Solutions

- 6.4.9 LearnUpon

- 6.4.10 360LEARNING SA

- 6.4.11 Epignosis LLC

- 6.4.12 SkyPrep Inc.

- 6.4.13 Axonify Inc.

- 6.4.14 Meridian Knowledge Solutions

- 6.4.15 Thinkific Labs Inc.

- 6.4.16 Thought Industries

- 6.4.17 Learning Pool

- 6.4.18 Schoox

- 6.4.19 Skilljar

- 6.4.20 LearnWorlds (CY) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

個人化學習市場預測(2034 年)-按組成部分、學習形式、技術、交付方式、應用、最終用戶和地區分類的全球分析

個人化學習市場預測(2034 年)-按組成部分、學習形式、技術、交付方式、應用、最終用戶和地區分類的全球分析 數位學術學習管理系統市場-全球市場預測(2026-2032年)學習管理系統 (LMS) 市場:按組件、用例、許可類型、內容傳送格式、定價模式、組織規模、部署模式和最終用戶分類——2026-2032 年全球市場預測

數位學術學習管理系統市場-全球市場預測(2026-2032年)學習管理系統 (LMS) 市場:按組件、用例、許可類型、內容傳送格式、定價模式、組織規模、部署模式和最終用戶分類——2026-2032 年全球市場預測 隨選學習管理系統市場:依部署模式、交付方式、使用者類型、最終使用者和地區分類

隨選學習管理系統市場:依部署模式、交付方式、使用者類型、最終使用者和地區分類 2026年全球個人化播客平台市場報告學習管理系統(LMS)市場:依部署模式、應用程式、交付方式、使用者類型、產業和地區分類2026年全球科學研究與開發市場報告2026年全球行動學習管理系統(LMS)軟體市場報告2026年全球個人化學習市場報告個人化學習體驗平台市場預測至2032年:按學習方法、部署類型、應用、最終用戶和地區分類的全球分析

2026年全球個人化播客平台市場報告學習管理系統(LMS)市場:依部署模式、應用程式、交付方式、使用者類型、產業和地區分類2026年全球科學研究與開發市場報告2026年全球行動學習管理系統(LMS)軟體市場報告2026年全球個人化學習市場報告個人化學習體驗平台市場預測至2032年:按學習方法、部署類型、應用、最終用戶和地區分類的全球分析