|

市場調查報告書

商品編碼

2063907

虛擬實境(VR)企業培訓:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Virtual Reality (VR) Corporate Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

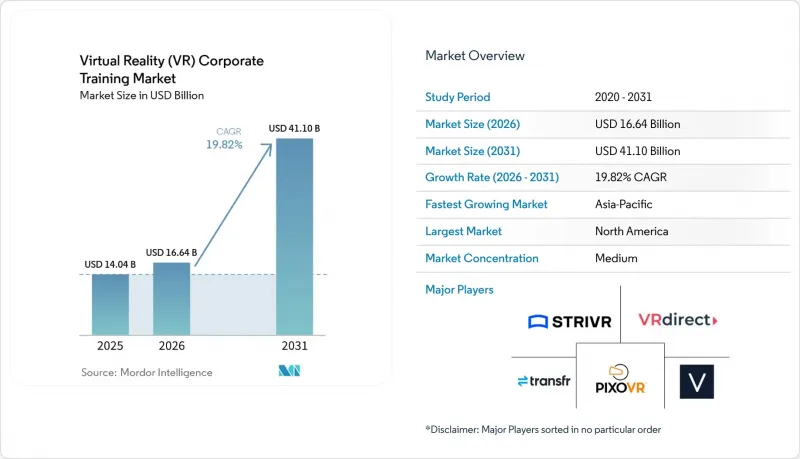

據 Mordor Intelligence 稱,2025 年利用虛擬實境 (VR) 進行企業培訓的市場價值為 140.4 億美元,預計到 2031 年將從 2026 年的 166.4 億美元成長至 411 億美元,預測期(2026-2031 年)的複合年成長率為 19.82%。

本報告按元件(硬體、軟體、服務)、部署類型(雲端、本地部署、混合部署)、企業規模(大型企業、中小企業)、培訓類型(安全合規、技術營運、其他)、產業(製造業、醫療保健、零售業、其他)和地區進行細分。市場預測以美元計價。

全球虛擬實境(VR)企業培訓市場趨勢與洞察

事實證明,它可以減少培訓時間和錯誤率。

在虛擬實境(VR)企業培訓市場,如果能夠將身臨其境型學習與縮短技能習得時間結合,其應用將會得到最快速的擴展。一項涵蓋37項同儕審查研究的2025年綜述發現,基於VR的安全培訓在即時知識獲取和危險識別方面優於傳統的課堂培訓。該綜述表明,傳統培訓小組在相同時間內遺忘陳述性知識的速度要快得多,這凸顯了VR的價值在於其效果能夠持續到培訓結束後。另一項2025年的研究發現,產業工人在接受VR訓練後,安全意識提高了30%,安全知識提高了25%,風險感知提高了30%。企業應用案例也表明,使用VR後,平均培訓時間從傳統課堂的120分鐘縮短至30分鐘。因此,培訓時間的縮短和知識維持率的提高,正在推動擁有大規模員工且需要定期更新認證的組織持續投資於VR。

高風險業務流程對安全模擬的需求日益成長

由於在職培訓會使員工面臨受傷、設備損壞和運作中斷的風險,虛擬實境 (VR) 企業培訓市場在風險較高的業務流程中具有明確的應用前景。 VR 讓員工在可控環境中重複接觸危險任務,而不會危及人員或資產安全。 2025 年的一項調查發現,86.67% 的倉庫環境專業人員認為 VR 安全訓練有效且逼真。同一項調查還發現,75% 的受訪者認為 VR 安全培訓具有成本效益。另一項 2025 年的調查顯示,接受 VR 培訓的產業員工的安全意識和風險意識均有顯著提高。隨著物流、製造和建設產業的雇主尋求更安全的培訓方法,身臨其境型模擬正逐漸成為 VR 企業培訓市場的核心。

客製化內容、系統整合和設備部署的初始成本較高。

在虛擬實境(VR)企業培訓市場,買家在評估客製化內容、系統整合和設備部署的第一年總成本時仍然猶豫不決。根據VRC的報告,傳統的專業互動模組每小時內容成本在5萬至20萬美元之間,並且需要持續維護以更新場景,從而適應不斷變化的流程。該報告還指出,如果將硬體、授權和IT整合等成本考慮在內,一個針對100-200名用戶的培訓計畫第一年的成本可能高達15萬至30萬美元。對於專業人員較少或培訓頻率較低的企業來說,這筆費用負擔尤其沉重,因為這會導致更長的投資回收期。雖然AutoVRse和其他無程式碼方法縮短了開發週期並降低了客製化開發成本,但高度專業化的工作流程仍需要對內部流程進行設計、檢驗和映射。因此,虛擬實境 (VR) 企業培訓市場的一些買家仍然選擇分階段、逐個地點部署,而不是立即在全公司範圍內推廣。

細分市場分析

到2025年,硬體將佔虛擬實境(VR)企業培訓市場佔有率的43.81%。這反映了多站點組織建構企業級VR設備的成本。由於獨立式頭戴裝置設定複雜度低,且買家擁有的負擔較輕,因此佔據了新部署的大部分佔有率。有線系統在外科、航空和國防等領域的培訓中仍然發揮著重要作用,因為這些領域對視覺保真度的要求仍然很高。控制器、追蹤器和觸覺工具在維護和設備模擬中變得越來越重要,因為它們透過增加互動增強了程式真實性。儘管買家計劃未來將價值創造轉移到軟體上,但虛擬實境(VR)企業培訓市場在其初始部署階段仍然以硬體為中心。

軟體市場預計將在2026年至2031年間以22.42%的複合年成長率成長,並有望成為虛擬實境(VR)企業培訓市場中成長最快的細分領域。這項轉變正從客製化引擎開發轉向無程式碼創作平台,使企業內部學習團隊能夠更快地建立模組。基於雲端的內容管理、行為分析以及與學習管理系統(LMS)的整合正逐漸成為標準軟體需求,而非可選附加元件。 *Virtual Reality* 的一項2026年研究表明,整合人工智慧大規模語言模型(AI-LLM)的VR培訓在知識獲取、一周後的記憶維持率以及學員自我效能方面均優於標準VR培訓。服務在VR企業培訓產業中仍然佔據重要地位,因為許多公司仍然需要外部支援來設計客製化場景、規劃部署和管理營運。

預計到2025年,基於雲端的交付方式將佔虛擬實境(VR)企業培訓市場58.62%的佔有率,凸顯了對可擴展內容管理的強勁需求。雲端交付使企業能夠將更新的模組分發到全球各地的頭戴式設備,而無需在每個地點重新映像設備。這一優勢在合規性項目中尤其重要,因為過時的內容可能會導致審計問題。在國防、金融和其他高度受控的環境中,本地部署仍然至關重要,因為這些環境需要更嚴格的資料居住要求和隔離的系統。因此,在VR企業培訓市場中,雲端部署在規模和更新速度至關重要的領域是首選,而在需要更高控制層級的用例中,則保留了本地部署選項。

在虛擬實境(VR)企業培訓市場,混合部署預計到2031年將以21.36%的複合年成長率成長。這種模式結合了雲端規模交付、本地身分管理以及敏感績效資料的本地處理。隨著雇主考慮如何使眼動追蹤、語音和行為數據符合GDPR和新的AI管治法規,這種平衡變得日益重要。對於希望集中管理內容並同時保持嚴格的內部安全工作流程的大型企業而言,混合架構尤其重要。因此,虛擬實境(VR)企業培訓市場的部署選擇越來越受到隱私管治和企業IT政策的驅動,而非設備類型或頻寬。

區域分析

2025年,北美繼續保持領先地位,佔據虛擬實境(VR)企業培訓市場36.51%的佔有率。美國的需求主要得益於製造業、零售業、醫療保健業和金融服務業等行業的早期企業應用。該地區還受益於密集的供應商網路,其中包括專注於安全、醫療模擬、軟性技能和企業部署的供應商。這種集中化使得買家能夠比較不同的供應商,快速開展試點實施,並將應用範圍從單一用例擴展到更廣泛的學習項目。因此,在虛擬實境(VR)企業培訓市場,北美仍然是大規模企業部署的最佳標竿。

以德國、英國和法國為首的歐洲,持續保持虛擬實境(VR)企業培訓第二大市場的地位。根據NMY報告顯示,漢莎航空培訓公司每年為超過2萬名機組人員實施VR安全模擬培訓,與傳統培訓方式相比,節省了1,400萬歐元(約1,526萬美元)的成本。 2025年4月, 生物識別,歐洲GDPR及相關人工智慧管治法規對生物辨識和推理資料的更嚴格審查可能會減緩VR技術的普及速度,但這可能有利於注重隱私的平台設計。

預計到2031年,亞太地區將以23.81%的複合年成長率成長,成為虛擬實境(VR)企業培訓市場成長最快的地區。全部區域龐大的產業勞動力、國內頭戴式設備生態系統的擴展以及公共職業培訓計畫的開展,正在推動VR技術的應用。印度、中國、日本、韓國、新加坡和澳洲尤其適合進行VR培訓,因為這些國家擁有大規模的勞動力和特定產業的技能缺口。中東地區在建築、能源、政府和國防項目方面的投資也在不斷增加,而南美洲則受益於製造業的數位化和勞動力現代化,發展勢頭強勁。雖然非洲的VR應用仍處於起步階段,但採礦、能源和政府機構的應用案例正在為南非、埃及和奈及利亞等國的VR企業培訓市場奠定堅實的基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 已經證明,訓練時間可以縮短,錯誤率可以降低。

- 在高風險工作流程中,對安全模擬的需求日益成長。

- 分散式勞動力隊伍的訓練標準化

- 透過獨立式耳機和雲端交付降低部署門檻。

- 人工智慧驅動的場景產生可以減少自訂內容的積壓。

- 可用於審計的技能遙測技術,以支援監管能力保證。

- 市場限制因素

- 客製化內容、整合和在所有車輛上部署都需要較高的初始成本。

- 重複使用引起的暈動病、耳機帶來的疲勞以及衛生方面的限制。

- 對與眼動追蹤、語音和行為數據相關的生物識別和人工智慧管治進行審查。

- 由於網路安全和身份檢驗要求,採購流程出現延誤。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 獨立式頭戴顯示器

- 有線頭戴式顯示器

- 控制器、追蹤器和周邊設備

- 觸覺回饋和配件

- 軟體

- 內容創作與場景設計

- 內容管理與分發平台

- 分析和評估軟體

- 用於學習管理系統 (LMS) 和人力資源資訊系統 (HRIS) 的整合軟體

- 服務

- 客製化內容開發

- 實施和系統整合

- 受管設備及程序操作

- 支援與維護

- 硬體

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按培訓類型

- 安全合規培訓

- 技術/操作培訓

- 軟性技能和領導力培訓

- 銷售和客戶服務培訓

- 新進員工培訓和入職指導

- 設備模擬與維修培訓

- 按最終用戶行業分類

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 能源公用事業

- 運輸/物流

- BFSI

- 建築與工程

- 政府、國防和公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Strivr Labs, Inc.

- VRdirect GmbH

- PixoVR, Corp.

- Transfr Inc.

- Virti Inc.

- Mursion, Inc.

- Osso VR, Inc.

- Oxford Medical Simulation Ltd.

- FVRVS Limited, trading as FundamentalXR

- Pixaera Inc.

- JCR Group Ltd, trading as Bodyswaps

- 3spin Learning GmbH & Co. KG

- TLN Training Limited, trading as Gemba

- WorldViz, Inc.

- SimX, Inc.

- Interplay Learning, Inc.

- Humulo Virtual Reality Inc.

- Skillveri Training Solutions Pvt Ltd.

- Moth+Flame, Inc.

- Innoactive GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the virtual reality (VR) corporate training market size was valued at USD 14.04 billion in 2025 and estimated to grow from USD 16.64 billion in 2026 to reach USD 41.10 billion by 2031, at a CAGR of 19.82% during the forecast period (2026-2031).

This report is Segmented by Component (Hardware, Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and SMEs), Training Type (Safety and Compliance, Technical and Operational, and More), Industry Vertical (Manufacturing, Healthcare, Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Virtual Reality (VR) Corporate Training Market Trends and Insights

Proven Reduction In Training Time And Error Rates

In the virtual reality (VR) corporate training market, adoption rises fastest when employers can tie immersive learning to a faster time-to-competency. A 2025 review covering 37 peer-reviewed studies found that VR-based safety training produced stronger immediate knowledge acquisition and hazard identification than traditional classroom formats. The same review showed that traditional training groups lost declarative knowledge much faster over comparable periods, underscoring VR's value beyond the session. A separate 2025 study found that industrial workers improved safety awareness by 30%, safety knowledge by 25%, and risk awareness by 30% after VR training. Reports also showed that average training duration fell from 120 minutes in classroom settings to 30 minutes with VR in enterprise use cases. This mix of shorter training time and stronger retention supports recurring investment when organizations need repeat certification across large workforces.

Rising Need For Safe Simulation In High-Risk Workflows

The virtual reality corporate training market has a clear use case in high-risk workflows, as live practice exposes workers to injury, equipment damage, and downtime. VR lets workers repeat hazardous tasks in a controlled environment without risking people or assets. A 2025 study found that 86.67% of warehouse-environment experts rated VR safety training as effective and realistic. The same study found that 75% of respondents considered VR safety training cost-effective. Another 2025 study also showed measurable gains in safety awareness and risk awareness among industrial workers trained with VR. As logistics, manufacturing, and construction employers seek safer rehearsal methods, immersive simulation is moving closer to the core of the virtual reality corporate training market.

High Upfront Cost Of Custom Content, Integration, And Fleet Rollout

The virtual reality (VR) corporate training market still faces hesitation when buyers evaluate the full first-year cost of custom content, systems integration, and device fleets. VRC reported that professional interactive modules historically required USD 50,000 to USD 200,000 per completed hour of content, with ongoing maintenance needed to keep scenarios aligned with changing procedures. The same source said programs for 100 to 200 users in year 1 can range from USD 150,000 to USD 300,000, once hardware, licensing, and IT integration are included. This burden is hardest for organizations with small specialist crews or infrequent training because the payback period is longer. AutoVRse and other no-code approaches are reducing development time and easing pressure on custom build costs, but highly specific workflows still require design, validation, and internal process mapping. For that reason, some buyers in the virtual reality (VR) corporate training market still phase rollouts site by site instead of expanding immediately across the full enterprise.

Other drivers and restraints analyzed in the detailed report include:

- Standardization Of Training Across Distributed Workforces

- Falling Deployment Friction From Standalone Headsets And Cloud Delivery

- Motion Sickness, Headset Fatigue, And Hygiene Constraints In Repeated Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 43.81% of the virtual reality (VR) corporate training market share in 2025, which reflected the cost of enterprise fleet buildouts across multi-site organizations. Standalone headsets led most new deployments because they reduced setup complexity and lowered the ownership burden for buyers. Tethered systems kept a premium role in surgical, aviation, and defense training where higher visual fidelity still mattered. Controllers, trackers, and haptic tools gained relevance in maintenance and equipment simulation because they added interaction, which improved procedural realism. The virtual reality (VR) corporate training market, remained hardware-heavy at the point of first rollout, even when buyers planned to shift value capture toward software over time.

Software is projected to expand at a 22.42% CAGR from 2026 to 2031, making it the fastest-growing component in the virtual reality (VR) corporate training market. The shift is moving from bespoke engine development toward no-code authoring platforms that let internal learning teams build modules faster. Cloud content management, behavioral analytics, and LMS integration are becoming baseline software requirements rather than optional add-ons. A 2026 study in Virtual Reality found that AI-LLM-integrated VR training outperformed standard VR on knowledge acquisition, 1-week retention, and trainee self-efficacy. Services remain important within the VR corporate training industry because many enterprises still need outside support for custom scenario design, rollout planning, and managed operations.

Cloud-based delivery captured 58.62% of the virtual reality (VR) corporate training market in 2025, underscoring a strong preference for scalable content management. Cloud delivery helps organizations push updated modules to global headset fleets without reimaging devices at each site. That advantage matters most in compliance programs where outdated content can create audit problems. On-premises deployments still matter in defense, finance, and other tightly controlled environments that require stronger data residency or isolated systems. The virtual reality corporate training market has therefore favored cloud, where scale and update speed matter, while preserving on-premises options for higher-control use cases.

Hybrid deployment is forecast to grow at a 21.36% CAGR through 2031 in the virtual reality (VR) corporate training market. This model combines cloud-scale distribution with local identity controls and local handling of sensitive performance data. That balance is gaining relevance as employers review how eye-gaze, voice, and behavioral data fit within GDPR and newer AI-governance rules. Hybrid architectures are especially relevant for large enterprises that want centralized content management without giving up tighter internal security workflows. Deployment choices in the virtual reality (VR) corporate training market are therefore being shaped more by privacy governance and enterprise IT policy than by device type or bandwidth.

Geography Analysis

North America held 36.51% of the virtual reality (VR) corporate training market share in 2025, maintaining its leading position. The United States drove most of that demand through earlier enterprise adoption across manufacturing, retail, healthcare, and financial services. The region also benefits from a dense vendor base, including providers focused on safety, healthcare simulation, soft skills, and enterprise deployment. This concentration helps buyers compare vendors, pilot faster, and expand from one use case into broader learning programs. In the virtual reality (VR) corporate training market, North America therefore remained the clearest reference point for scaled enterprise deployment.

Europe remained the second-largest region in the virtual reality (VR) corporate training market, led by Germany, the United Kingdom, and France. NMY reported that Lufthansa Aviation Training used VR safety simulations for more than 20,000 flight attendants annually and achieved EUR 14 million (USD 15.26 million) in savings relative to traditional formats. Uptale announced a strategic alliance with VRdirect in April 2025 to serve more than 350 enterprise customers across Europe, North America, and Asia, which strengthened regional platform reach. Europe also faces tighter scrutiny of biometric and inferred data under GDPR and related AI governance rules, which can slow procurement but also reward privacy-focused platform design.

Asia-Pacific is projected to expand at a 23.81% CAGR through 2031, making it the fastest-growing region in the virtual reality corporate training market. Industrial workforce scale, expanding domestic headset ecosystems, and public workforce upskilling programs are supporting adoption across the region. India, China, Japan, South Korea, Singapore, and Australia align well with VR training because they combine large labor pools with sector-specific skills gaps. The Middle East is also increasing investment in construction, energy, government, and defense programs, while South America is building momentum from manufacturing digitization and workforce modernization. Africa remains earlier in adoption, but mining, energy, and government use cases provide a strong base for the VR corporate training market in countries such as South Africa, Egypt, and Nigeria.

- Strivr Labs, Inc.

- VRdirect GmbH

- PixoVR, Corp.

- Transfr Inc.

- Virti Inc.

- Mursion, Inc.

- Osso VR, Inc.

- Oxford Medical Simulation Ltd.

- FVRVS Limited, trading as FundamentalXR

- Pixaera Inc.

- JCR Group Ltd, trading as Bodyswaps

- 3spin Learning GmbH & Co. KG

- TLN Training Limited, trading as Gemba

- WorldViz, Inc.

- SimX, Inc.

- Interplay Learning, Inc.

- Humulo Virtual Reality Inc.

- Skillveri Training Solutions Pvt Ltd.

- Moth+Flame, Inc.

- Innoactive GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proven Reduction in Training Time and Error Rates

- 4.2.2 Rising Need for Safe Simulation in High-Risk Workflows

- 4.2.3 Standardization of Training Across Distributed Workforces

- 4.2.4 Falling Deployment Friction from Standalone Headsets and Cloud Delivery

- 4.2.5 AI-Generated Scenario Authoring Compressing Custom Content Backlogs

- 4.2.6 Audit-Ready Skills Telemetry Supporting Regulated Competency Assurance

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Custom Content, Integration, and Fleet Rollout

- 4.3.2 Motion Sickness, Headset Fatigue, and Hygiene Constraints in Repeated Use

- 4.3.3 Biometric and AI-Governance Scrutiny Over Eye-Gaze, Voice, and Behavioral Data

- 4.3.4 Procurement Delays from Cybersecurity and Identity-Stack Validation Requirements

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Standalone Head-Mounted Displays

- 5.1.1.2 Tethered Head-Mounted Displays

- 5.1.1.3 Controllers, Trackers, and Peripherals

- 5.1.1.4 Haptics and Accessories

- 5.1.2 Software

- 5.1.2.1 Content Authoring and Scenario Design

- 5.1.2.2 Content Management and Delivery Platforms

- 5.1.2.3 Analytics and Assessment Software

- 5.1.2.4 LMS and HRIS Integration Software

- 5.1.3 Services

- 5.1.3.1 Custom Content Development

- 5.1.3.2 Implementation and Systems Integration

- 5.1.3.3 Managed Device and Program Operations

- 5.1.3.4 Support and Maintenance

- 5.1.1 Hardware

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Training Type

- 5.4.1 Safety and Compliance Training

- 5.4.2 Technical and Operational Training

- 5.4.3 Soft Skills and Leadership Training

- 5.4.4 Sales and Customer Interaction Training

- 5.4.5 Onboarding and Employee Orientation

- 5.4.6 Equipment Simulation and Maintenance Training

- 5.5 By End User Industry Vertical

- 5.5.1 Industrial Manufacturing

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and Ecommerce

- 5.5.4 Energy and Utilities

- 5.5.5 Transportation and Logistics

- 5.5.6 BFSI

- 5.5.7 Construction and Engineering

- 5.5.8 Government, Defense, and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Strivr Labs, Inc.

- 6.4.2 VRdirect GmbH

- 6.4.3 PixoVR, Corp.

- 6.4.4 Transfr Inc.

- 6.4.5 Virti Inc.

- 6.4.6 Mursion, Inc.

- 6.4.7 Osso VR, Inc.

- 6.4.8 Oxford Medical Simulation Ltd.

- 6.4.9 FVRVS Limited, trading as FundamentalXR

- 6.4.10 Pixaera Inc.

- 6.4.11 JCR Group Ltd, trading as Bodyswaps

- 6.4.12 3spin Learning GmbH & Co. KG

- 6.4.13 TLN Training Limited, trading as Gemba

- 6.4.14 WorldViz, Inc.

- 6.4.15 SimX, Inc.

- 6.4.16 Interplay Learning, Inc.

- 6.4.17 Humulo Virtual Reality Inc.

- 6.4.18 Skillveri Training Solutions Pvt Ltd.

- 6.4.19 Moth+Flame, Inc.

- 6.4.20 Innoactive GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

寵物行為矯正應用程式和訓練平台市場預測至2034年—全球平台類型、訓練重點領域、服務模式、經營模式、最終用戶和區域分析寵物訓練應用程式和虛擬訓練平台市場預測至2034年—按平台類型、訓練重點領域、服務模式、經營模式、最終用戶和地區分類的全球分析自閉症人士的社交技能虛擬實境訓練市場:2034 年預測-按訓練模組、技術平台、經營模式、交付方式、最終用戶和地區分類的全球分析體驗式學習平台市場預測至2034年:按組件、學習風格、技術、最終用戶、應用和地區分類的全球分析身臨其境型學習市場預測至2034年—按技術、組件、設備、應用、最終用戶和地區分類的全球分析

寵物行為矯正應用程式和訓練平台市場預測至2034年—全球平台類型、訓練重點領域、服務模式、經營模式、最終用戶和區域分析寵物訓練應用程式和虛擬訓練平台市場預測至2034年—按平台類型、訓練重點領域、服務模式、經營模式、最終用戶和地區分類的全球分析自閉症人士的社交技能虛擬實境訓練市場:2034 年預測-按訓練模組、技術平台、經營模式、交付方式、最終用戶和地區分類的全球分析體驗式學習平台市場預測至2034年:按組件、學習風格、技術、最終用戶、應用和地區分類的全球分析身臨其境型學習市場預測至2034年—按技術、組件、設備、應用、最終用戶和地區分類的全球分析 2026年全球虛擬培訓與模擬市場報告

2026年全球虛擬培訓與模擬市場報告 全球虛擬培訓和模擬市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虛擬實境(VR)技能培訓市場預測至2032年:按組件、培訓類型、最終用戶和地區分類的全球分析

全球虛擬培訓和模擬市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虛擬實境(VR)技能培訓市場預測至2032年:按組件、培訓類型、最終用戶和地區分類的全球分析 虛擬培訓與模擬市場規模、佔有率及成長分析(按類型、垂直產業、應用、部署類型、最終用戶與地區分類)-2026-2033年產業預測教育和模擬訓練領域的虛擬實境市場預測至2032年:按組件、部署模式、應用、最終用戶和地區分類的全球分析

虛擬培訓與模擬市場規模、佔有率及成長分析(按類型、垂直產業、應用、部署類型、最終用戶與地區分類)-2026-2033年產業預測教育和模擬訓練領域的虛擬實境市場預測至2032年:按組件、部署模式、應用、最終用戶和地區分類的全球分析