|

市場調查報告書

商品編碼

2063898

鑽頭顏色:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Drill Collar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

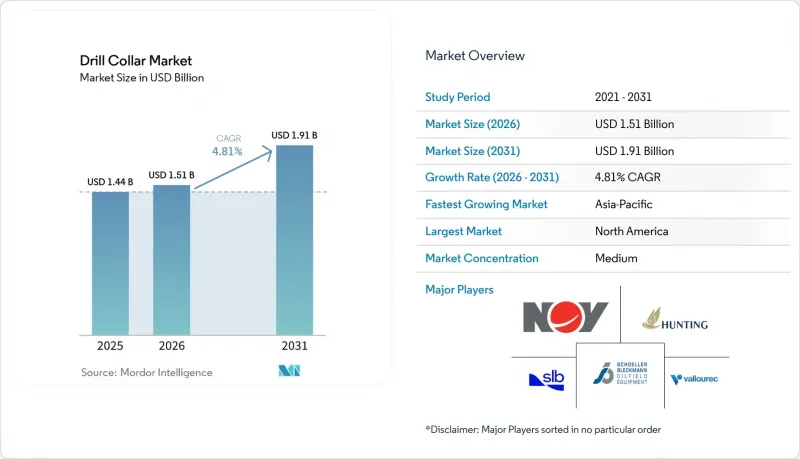

根據 Mordor Intelligence 預測,鑽鋌市場規模預計在 2025 年達到 14.4 億美元,2026 年達到 15.1 億美元,到 2031 年達到 19.1 億美元,2026 年至 2031 年的複合年成長率為 4.81%。

本報告按類型(標準鋼鑽鋌、非磁性鑽鋌)、材質等級(4145H改性鋼、4330V鋼、非磁性14Cr-MoV不銹鋼)、部署方式(陸上、海上)、應用領域(陸上鑽機、高溫高壓井、定向井和水平鑽井)以及南美(北美、歐洲和亞地區進行細分。市場預測以美元計價。

全球鑽鋌市場趨勢與洞察

從2025年起,全球鑽井鑽機數量將逐步恢復。

經過數年的下滑,國際鑽井活動在2026年初觸底反彈,共有1058座鑽井平台運作,其中包括229座海上鑽機。 ADNOC Drilling在2026年1月訂購了兩座總價值11.5億美元的高階自升式鑽機,進一步推動了這一成長趨勢。印度監管機構設定了1000億美元的上游鑽井目標,其中包括40口深水探勘井,每口井都需要專用的鑽鋌。雖然運作的第八代鑽井船採用混合動力系統,可將燃料消耗降低高達30%,但它們所瞄準的深井需要更重的鑽鋌,以確保在2000公尺深度下鑽壓。因此,市場需求正從大批量、低規格的替換轉向小批量、高規格的升級。

擴大深海和超深海鑽探項目

巴西石油公司(Petrobras)於2025年初批准了SEAP I和SEAP II項目,撥款超過120億美元用於32口位於2000米以上儲存。這些油井將承受超過15000磅/平方英吋(psi)的壓力,因此需要使用4330V或14Cr-MoV材質的套管。 Beacon Offshore Energy公司的Shenandoah油田凸顯了向極端環境的過渡,該油田在低於20000磅/平方英寸(psi)的壓力條件下,日產量超過10萬桶。 Equinor公司已為2026年的計畫撥款1,400億挪威克朗(約131億美元),其中包括Johan Sverdorp第二期計畫。由於北極地區的低溫環境,該計畫需要使用符合NORSOK認證標準的套管。在超深水作業中,獲利能力取決於避免管道堵塞,因為堵塞可能導致每天100萬美元的損失。因此,營運商正在投資研發高屈服強度的鍛造套管,並結合即時疲勞建模技術。這些技術難題正推動鑽鋌市場轉型為高品質金屬材料和數位支援服務。

原油價格波動抑制了油氣探勘開發領域的資本投資。

美國能源資訊署 (EIA) 指出,2024 年上游資本支出下降了 14%,上市生產商的現金流下降了 9%,這給可自由支配的鑽井預算帶來了壓力。雪佛龍公司已宣布 2026 年資本支出計畫為 180 億至 190 億美元,但這一上調取決於布蘭特原油價格穩定在每桶 70 美元以上。由於營運商可以迅速推遲完井作業或關閉鑽機而不會造成短期產量損失,因此鑽鋌的需求會間歇性波動。此類需求萎縮通常首先影響標準鋼材的訂單,導致工廠運轉率下降並擠壓利潤率。在損益平衡價格徘徊在全球基準價格附近的地區,由於採購團隊延後採購高合金鋼,鑽鋌市場的單位成長放緩。

細分市場分析

到2025年,標準鋼材將佔銷售量的65.1%,這反映了其低成本和對垂直井的適用性。然而,非磁性鑽鋌的年複合成長率(CAGR)為5.5%。這是因為高頻感測器無法容忍任何磁導率超過1.01的材料。受海底和長距離水平井數量增加的推動,非磁性鑽鋌的市場規模預計將在2026年至2031年間持續成長。哈里伯頓公司的EarthStar 3DX產品現已在其所有高溫高壓(HPHT)井下鑽具組合(BHA)中指定使用這種金屬材料,凸顯了其卓越的品質。

製造商正利用這一定價空間。由於合金需求增加,Scherrer Bleckmann公司2024年的息稅前利潤率(EBIT利潤率)達到了15.0%。在美國垂直深度超過1500公尺的頁岩地層中,由於業者積極重複利用庫存,標準鋼材仍佔據主導地位。然而,隨著帶磁力鑽桿在陸上作業中的應用,感測器密度不斷增加,因此,非磁性產品在鑽鋌市場的佔有率也在上升。

由於符合API標準且成本均衡,4145H改性鋼預計在2025年佔出貨量的44.9%。非磁性14Cr-MoV不銹鋼是成長最快的鋼種,複合年成長率達5.8%,主要得益於鹽層下下層油井中二氧化碳和硫化氫的高暴露環境。此鋼種鑽鋌市場的擴張在美國墨西哥灣20,000 psi專案中最為顯著。

4330V 是一種強度適中的選擇,適用於北極和超深海應用。 Equinor 公司在約翰·斯維爾多普二期工程中就使用了這種鋼材,該工程海底溫度常年保持在 4°C 左右。像 Tenaris Dopeless 這樣的高品質連接器可以降低咬合風險,延長重複使用週期,並幫助營運商避免合金價格波動的影響。

區域分析

受墨西哥灣深海活性化和美國頁岩氣開發的推動,北美地區在2025年佔據了38.5%的市場佔有率。但到2026年4月,該地區的鑽機數量已減少至548座。雪佛龍公司仍將2026年鑽機中的約70億美元分配給墨西哥灣項目,以支撐對非磁性及耐高溫高壓(HPHT)產品的需求。在加拿大,由於僅有54座運作中鑽井平台,該公司面臨運輸能力的限制。這限制了顏料的消耗,但也為專注於寒冷氣候金屬加工技術的供應商提供了一個利基市場。

預計到2031年,亞太地區的年複合成長率將達到6.2%,成長速度位居各地區之首。印度油氣總局正在上游業務領域投資1,000億美元,其中包括40口深水探勘井,每口井都需要專用的鑽鋌。印度石油天然氣公司(ONGC)價值3.855億美元的克里希納-戈達瓦里油田鑽探合約已提前訂購了耐高溫高壓(HPHT)合金。中海油文昌16-2號井正依賴國內鋼廠縮短前置作業時間,以提振區域需求。

挪威正引領歐洲經濟成長。 Equinor公司斥資1,400億挪威克朗制定的「2026計畫」旨在維持Johan Sverdrup油田目前的產量水平,並將Braydabrik油田的日產量提升至14萬桶,這兩個油田均已通過北極鑽井標準認證。挪威不斷上漲的二氧化碳價格推動了混合動力鑽機的應用,但諷刺的是,鑽探更深的油井需要更堅固、更重的井口組件。在中東和非洲,ADNOC Drilling公司價值36億美元的訂單證實了市場對高品質井下鑽具組合(BHA)的長期需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從2025年起,全球鑽井鑽機數量將逐步恢復。

- 擴大深海和超深海鑽探項目

- 定向鑽井和水平鑽井技術的快速發展

- OEM主導的顏色重量最佳化降低了鑽機排放氣體。

- 對用於高頻隨鑽測量/隨鑽測量的非磁性彩色塗料的需求正在激增。

- 透過使用數位雙胞胎預測疲勞壽命,可以延長使用壽命。

- 市場限制因素

- 原油價格波動抑制了油氣探勘開發行業的資本支出。

- 替代地下配重方案的可用性

- 低磁導率非磁性合金供應短缺

- 對挖掘廢棄物的更嚴格規定縮短了顏色週期。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 標準鋼鑽鋌

- 非磁性鑽鋌

- 按材料等級

- 4145H 改性鋼

- 4330V鋼

- 非磁性14Cr-MoV不銹鋼

- 不同的發展

- 陸上

- 離岸

- 透過使用

- 陸域鑽機

- 高壓高溫井

- 定向鑽井和水平鑽井

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 挪威

- 英國

- 俄羅斯

- 荷蘭

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 奈及利亞

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Hunting plc

- SLB NV

- NOV Inc.

- SBO AG

- China Vigor Drilling Oil Tools and Equipment Co., Ltd.

- International Drilling Services Ltd.(IDS)

- Zhong Yuan Special Steel Co., Ltd.

- American Oilfield Tools, Inc.

- Workstrings International Ltd.

- Texas Steel Conversion, Inc.

- Challenger International, Inc.

- Vallourec SA

- Weatherford International plc

- Tenaris SA

- Jiangsu Shuguang Huayang Drilling Tool Co., Ltd.

- Superior Drillpipe Manufacturing, Inc.

- Tejas Tubular Products, Inc.

- Drill Collars & Drill Pipe, Inc.

- Ramco Tubular Services, Inc.

- Drill Collar USA, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the drill collar market size is projected to be USD 1.44 billion in 2025, USD 1.51 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 4.81% from 2026 to 2031.

This report is Segmented by Type (Standard Steel Drill Collar, Non-Magnetic Drill Collar), Material Grade (4145H Mod Steel, 4330V Steel, Non-Magnetic 14Cr-MoV Stainless), Deployment (Onshore, Offshore), Application (Land Rigs, HPHT Wells, Directional and Horizontal Drilling), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Drill Collar Market Trends and Insights

Recovery in Global Rig Counts Post 2025

International rig activity found a floor in early 2026 with 1,058 units working, including 229 offshore rigs, after several years of attrition. ADNOC Drilling reinforced the upward trend by ordering two premium jack-ups valued at USD 1.15 billion in January 2026. India's regulator outlined a USD 100 billion upstream target that includes 40 deepwater wildcats, each demanding dedicated drill-collar strings. Reactivated eighth-generation drillships employ hybrid power that cuts fuel use by as much as 30%, yet the deeper wells they target require heavier collars to deliver weight-on-bit at 2,000 m water depth. As a result, demand is migrating from high-volume, low-spec replacements to lower-volume, high-spec upgrades.

Growth of Deep- & Ultra-Deepwater Drilling Projects

Petrobras approved SEAP I and SEAP II in early 2025, earmarking more than USD 12 billion for 32 wells in reservoirs beyond 2,000 m depth, with pressures above 15,000 psi that mandate 4330V or 14Cr-MoV collars. Beacon Offshore Energy's Shenandoah field surpassed 100,000 bpd under 20,000 psi conditions, underscoring the shift toward extreme environments. Equinor allocated NOK 140 billion (USD 13.1 billion) for 2026 projects such as Johan Sverdrup Phase 2, where Arctic temperatures demand NORSOK-certified collars. Ultra-deepwater economics depend on avoiding stuck-pipe events that cost USD 1 million per day, so operators invest in collars forged for high yield strength and paired with real-time fatigue models. These technical thresholds are pushing the drill collar market toward premium metallurgy and digital support services.

Crude-Oil Price Volatility Dampens E&P CAPEX

The U.S. Energy Information Administration noted a 14% decline in upstream capital spending during 2024 and a 9% slide in cash flow among public producers, squeezing discretionary drilling budgets. Chevron disclosed a USD 18-19 billion 2026 capital plan but tied any upside to Brent benchmarks stabilizing above USD 70 per barrel. Operators can quickly defer completions or idle rigs without near-term production loss, causing sporadic demand swings for drill collars. Such pullbacks typically hit standard steel orders first, compressing plant utilization and eroding margins. In regions where breakeven prices hover near global benchmarks, procurement teams delay high-alloy purchases, slowing unit growth in the drill collar market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Directional & Horizontal Drilling

- OEM-Led Collar Weight Optimization to Cut Rig Emissions

- Availability of Substitute Down-Hole Weight Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard steel accounted for 65.1% of 2025 volume, reflecting its low cost and readiness for vertical wells. Non-magnetic collars, however, are expanding at 5.5% CAGR because high-frequency sensors cannot tolerate magnetic permeability above 1.01. The drill collar market size for non-magnetic variants is projected to expand from 2026 through 2031 as subsalt and long-reach laterals proliferate. Halliburton's EarthStar 3DX now specifies this metallurgy on every HPHT BHA, validating the premium.

Manufacturers exploit the pricing headroom: Schoeller-Bleckmann's 2024 EBIT margin reached 15.0% on stronger alloy demand. Standard steel continues to dominate U.S. shale where vertical sections exceed 1,500 m and operators recycle inventory aggressively. Yet as wired pipe migrates into land operations, sensor density rises and the non-magnetic share of the drill collar market rises alongside.

4145H modified steel secured 44.9% of 2025 shipments thanks to its API acceptance and balanced cost. Non-magnetic 14Cr-MoV stainless is the fastest-growing grade at 5.8% CAGR, supported by pre-salt wells with high CO2 and H2S exposure. Drill collar market size growth in this grade is most noticeable in the U.S. Gulf of Mexico's 20,000 psi projects.

4330V provides a higher-strength middle ground for Arctic and ultra-deepwater applications. Equinor employs it in Johan Sverdrup Phase 2 where seabed temperatures hover near 4 °C. Premium connections such as Tenaris Dopeless reduce galling risk, extending reuse cycles and shielding operators from volatile alloy prices.

Geography Analysis

North America commanded 38.5% share in 2025 on the back of Gulf of Mexico deepwater and U.S. shale intensity, though regional rig counts slipped to 548 units by April 2026. Chevron still directs roughly USD 7 billion of its 2026 budget to Gulf projects, maintaining a floor for non-magnetic and HPHT-rated demand. Canada's modest 54 working rigs grapple with takeaway constraints, tempering collar consumption but supporting niche suppliers skilled in cold-weather metallurgy.

Asia-Pacific is forecast to grow at 6.2% CAGR through 2031, the fastest pace among regions. India's Directorate General of Hydrocarbons is steering USD 100 billion toward upstream work that includes 40 deepwater wildcats, each requiring dedicated drill-collar strings. ONGC's USD 385.5 million contract for Krishna-Godavari drilling places early orders for HPHT-ready alloys. CNOOC's Wenchang 16-2 adds regional pull, relying on domestic mills for shorter lead times.

Europe growth is anchored by Norway. Equinor's NOK 140 billion 2026 plan keeps Johan Sverdrup on plateau and moves Breidablikk toward 140,000 bpd, both certified under Arctic drilling codes. Norway's sharp CO2 price encourages hybrid rigs that paradoxically need stiffer, heavier collars to manage deeper wells. In the Middle East and Africa, ADNOC Drilling's USD 3.6 billion award slate confirms prolonged appetite for premium BHAs.

- Hunting plc

- SLB N.V.

- NOV Inc.

- SBO AG

- China Vigor Drilling Oil Tools and Equipment Co., Ltd.

- International Drilling Services Ltd. (IDS)

- Zhong Yuan Special Steel Co., Ltd.

- American Oilfield Tools, Inc.

- Workstrings International Ltd.

- Texas Steel Conversion, Inc.

- Challenger International, Inc.

- Vallourec S.A.

- Weatherford International plc

- Tenaris S.A.

- Jiangsu Shuguang Huayang Drilling Tool Co., Ltd.

- Superior Drillpipe Manufacturing, Inc.

- Tejas Tubular Products, Inc.

- Drill Collars & Drill Pipe, Inc.

- Ramco Tubular Services, Inc.

- Drill Collar USA, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recovery in global rig counts post-2025

- 4.2.2 Growth of deep- & ultra-deep-water drilling projects

- 4.2.3 Rapid adoption of directional & horizontal drilling

- 4.2.4 OEM-led collar weight optimisation to cut rig emissions

- 4.2.5 Surging demand for non-magnetic collars for high-freq MWD/LWD

- 4.2.6 Digital-twin based fatigue-life prediction extends service life

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility dampens E&P CAPEX

- 4.3.2 Availability of substitute down-hole weight solutions

- 4.3.3 Supply crunch in low-permeability non-magnetic alloys

- 4.3.4 Stricter drilling-waste regulations shortening collar cycles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Standard Steel Drill Collar

- 5.1.2 Non-magnetic Drill Collar

- 5.2 By Material Grade

- 5.2.1 4145H Mod Steel

- 5.2.2 4330V Steel

- 5.2.3 Non-magnetic 14Cr-MoV Stainless

- 5.3 By Deployment

- 5.3.1 Onshore

- 5.3.2 Offshore

- 5.4 By Application

- 5.4.1 Land Rigs

- 5.4.2 High-Pressure High-Temperature (HPHT) Wells

- 5.4.3 Directional and Horizontal Drilling

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Norway

- 5.5.2.2 United Kingdom

- 5.5.2.3 Russia

- 5.5.2.4 Netherlands

- 5.5.2.5 Germany

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Iran

- 5.5.5.4 Nigeria

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Hunting plc

- 6.4.2 SLB N.V.

- 6.4.3 NOV Inc.

- 6.4.4 SBO AG

- 6.4.5 China Vigor Drilling Oil Tools and Equipment Co., Ltd.

- 6.4.6 International Drilling Services Ltd. (IDS)

- 6.4.7 Zhong Yuan Special Steel Co., Ltd.

- 6.4.8 American Oilfield Tools, Inc.

- 6.4.9 Workstrings International Ltd.

- 6.4.10 Texas Steel Conversion, Inc.

- 6.4.11 Challenger International, Inc.

- 6.4.12 Vallourec S.A.

- 6.4.13 Weatherford International plc

- 6.4.14 Tenaris S.A.

- 6.4.15 Jiangsu Shuguang Huayang Drilling Tool Co., Ltd.

- 6.4.16 Superior Drillpipe Manufacturing, Inc.

- 6.4.17 Tejas Tubular Products, Inc.

- 6.4.18 Drill Collars & Drill Pipe, Inc.

- 6.4.19 Ramco Tubular Services, Inc.

- 6.4.20 Drill Collar USA, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

鑽鋌市場報告:按類型、應用、設計和地區分類(2026-2034 年)

鑽鋌市場報告:按類型、應用、設計和地區分類(2026-2034 年) 鑽鋌市場:鋌類型、重量範圍、材質、銷售管道、應用、最終用途-2026-2032年全球市場預測

鑽鋌市場:鋌類型、重量範圍、材質、銷售管道、應用、最終用途-2026-2032年全球市場預測 中東和非洲鑽鋌:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

中東和非洲鑽鋌:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)