|

市場調查報告書

商品編碼

2063819

網狀Wi-Fi系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Mesh Wi-fi Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

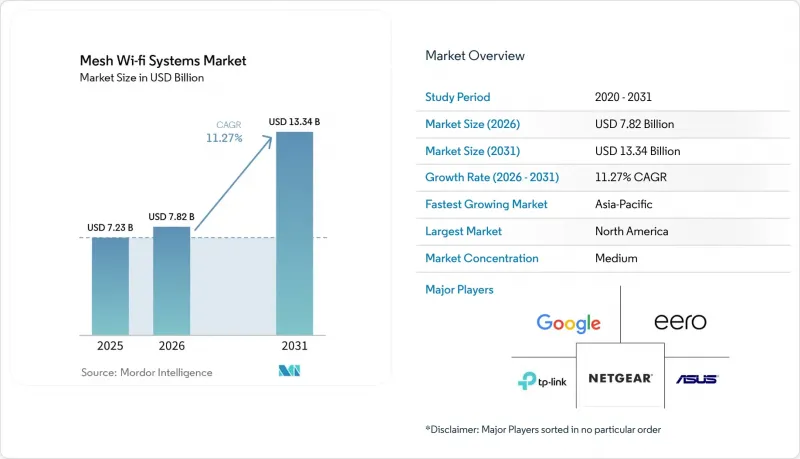

根據 Mordor Intelligence 預測,網狀 Wi-Fi 系統市場規模將從 2025 年的 72.3 億美元和 2026 年的 78.2 億美元成長到 2031 年的 133.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按組件(硬體、軟體、服務)、頻段數量(雙頻、三頻、四頻及更多)、Wi-Fi 標準(Wi-Fi 5、Wi-Fi 6、Wi-Fi 6E 和 Wi-Fi 7)、應用(例如,住宅)、配銷通路(線上零售/市場、線下/實體店)和地區(例如,北美)和地區細分(例如,北美)和地區地區(例如,)和地區市場(例如,北美)和地區市場進行細分。市場預測以美元計價。

全球網狀Wi-Fi系統市場趨勢與洞察

智慧家庭設備安裝數量爆炸性成長。

目前,每個家庭平均擁有 15 到 20 台連網設備,從音箱到家用電器,都在爭取頻寬。隨著超過 500 台設備通過 Matter 1.4.2 認證,住宅可以集中控制這些設備,使網狀網路系統成為家庭網路的必備基礎。與擴充器相比,基於 Thread 的網狀網路可將封包遺失降低 40%,從而提高用戶滿意度並顯著減少向網路服務供應商 (ISP) 尋求支援的情況。因此,零售商正在推廣將網狀網路套件與智慧燈泡和智慧門鎖組合在一起的「全屋套裝」。由此可見,隨著住宅中攝影機或語音助理數量的增加,網狀 Wi-Fi 系統市場也相應成長。

Gigabit及光纖到府網路的快速普及

韓國、日本和美國主要都市地區的通訊業者正在提供對稱Gigabit服務,這暴露了家庭Wi-Fi連線的脆弱性。為了維持承諾的速度,通訊業者將網狀網路節點整合到高級光纖套餐中,每月收費5至10美元的費用,將資本投資轉化為訂閱收入。歐洲有2.95億戶家庭處於光纖服務覆蓋範圍內,中國有2.068億Gigabit用戶也呈現類似的趨勢,最後一公里效能已成為競爭優勢。因此,隨著每條光纖連接接入用戶家中,網狀Wi-Fi系統市場的價值不斷提升。

半導體供應持續短缺

由於智慧型手機和資料中心客戶搶先於消費網路供應商取得晶圓配額,先進的 6nm 和 5nm 半導體產能依然緊張。 Wi-Fi 7 晶片組的成本比 Wi-Fi 6E 高出 40-50%,迫使供應商優先開發旗艦級網狀網路系統,並推遲更廣泛產品線的部署。超過 30 週的前置作業時間給營運資金帶來壓力,擾亂了庫存計劃,並限制了旺季的供應。在新增產能投入運作之前,供應瓶頸將繼續限制出貨量,延緩價格恢復正常,並減緩網狀 Wi-Fi 系統市場的短期成長。

細分市場分析

截至2025年,硬體在網狀Wi-Fi市場佔有率中佔63.4%。這是因為用戶仍然首先需要購買實體節點以確保可靠的網路覆蓋範圍。然而,業務收益正以13.81%的複合年成長率成長,顯示隨著網路服務供應商和供應商銷售安全訂閱、家長監控、分析功能等服務,市場正向持續收入模式轉變。隨著通訊業者將每月5至15美元的費用納入光纖套餐,預計從2026年到2031年,與服務相關的網狀Wi-Fi系統市場規模將逐年超過硬體市場。

這種轉變是由軟體創新所驅動的。雲端控制面板讓住宅能夠查看裝置層級的網路狀況,而人工智慧引擎則無需使用者介入即可自動調整頻道選擇。掌握了空中下載 (OTA) 更新和數據分析技術的供應商正在提升客戶終身價值,並縮短目前仍主導節點升級的 4-5 年更換週期。因此,制勝策略是將價格合理的硬體與高度成熟的雲端功能相結合,從而鼓勵用戶在初始部署後長期付費使用。

到2025年,雙頻套裝將佔據網狀Wi-Fi系統市場48.19%的佔有率。這是因為注重成本的消費者發現,2.4 GHz和5 GHz頻段的覆蓋範圍足以滿足電子郵件、串流媒體和智慧音箱的使用需求。隨著頻寬需求的激增,三頻型號透過增加第二個5 GHz頻段用於專用回程傳輸鏈路,從而在價格和性能之間取得平衡。四頻系統目前以15.62%的複合年成長率快速成長,充分利用了全球監管機構開放的6 GHz頻段。

在Wi-Fi 7中,廠商會分配一個6GHz無線模組用於回程傳輸,另一個用於客戶端,而傳統設備則繼續使用2.4GHz和5GHz頻段。更低的干擾和延遲將使8K串流媒體和雲端遊戲能夠共存。隨著晶片組價格的下降,四頻產品的價格差距正在縮小,這促使電力用戶、遠端辦公人員和遊戲玩家轉向更高階的套裝產品。因此,預計到2031年,網狀Wi-Fi系統市場中四頻產品的市場規模成長速度將超過其他任何配置。

區域分析

預計到2025年,北美將佔全球網狀Wi-Fi系統市場營收的38.96%。這主要得益於Gigabit光纖的普及、智慧家庭的滲透以及通訊業者面向數千萬用戶提供的網狀Wi-Fi套餐。美國在區域市場規模上佔據主導地位,這得益於其高達424.5億美元的BEAD計畫資金,用於支持全州網路建設。在加拿大,1,200萬條光纖連線以及每月10加幣(約7.90美元)的加值服務正推動著網狀Wi-Fi系統的穩定普及;而在墨西哥,800萬條光纖到戶(FTTH)線路則將網狀Wi-Fi的需求集中在三大城市。

歐洲緊追在後,擁有1.6億光纖用戶,普及率高達54%。這凸顯了當通訊速度超過1Gbps時,傳統路由器已無法滿足需求。德國電信和橘子等通訊業者正在將網狀網路整合到其Gigabit套餐中,而歐盟的《網路安全彈性法案》規定了五年的安全支持,進一步增強了消費者的信心。在俄羅斯,分散式節點正在混凝土多用戶住宅中部署,這凸顯了現有建築存量如何影響網狀Wi-Fi市場的架構選擇。

亞太地區正經歷最快的成長,複合年成長率高達14.28%,這主要得益於中國2.068億Gigabit用戶以及印度連接25萬個村莊的「BharatNet」計畫。日本85%的光纖普及率和韓國95%的光纖到戶(FTTH)覆蓋率正在加速Wi-Fi 7的普及,主要源自於遊戲玩家對穩定、低延遲連線的需求。東南亞的主要城市正在新建光纖骨幹網上建立網狀網路,每套設備的價格低於150美元,使新興中產階級家庭能夠更負擔得起服務。除這三大地區外,中東正朝著「沙烏地阿拉伯2030願景」推動寬頻現代化;南美洲在宏觀經濟壓力下保持著溫和成長;撒哈拉以南非洲仍處於起步階段,目前4G固定無線網路比光纖到戶更受歡迎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧家庭設備安裝數量爆炸性成長。

- Gigabit及光纖到府網路的快速普及

- Wi-Fi 6/6E 晶片組價格下降

- 通訊業者將推出網狀CPE,實現全屋覆蓋。

- 政府主導的數位包容計劃

- 人工智慧驅動的自癒網路演算法

- 市場限制因素

- 半導體供應緊張的局面依然存在。

- 家庭網路日益脆弱,容易受到網路安全攻擊。

- 消費者對Wi-Fi標準(6E與7)的困惑

- 網路設備進口關稅

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 按樂隊數量

- 雙頻網狀系統

- 三頻網狀系統

- 四頻及更高頻段的網狀系統

- 按 Wi-Fi 標準

- Wi-Fi 5(802.11ac)

- Wi-Fi 6(802.11ax)

- Wi-Fi 6E(802.11axe)

- Wi-Fi 7(802.11be)

- 透過使用

- 住宅

- 適用於商業和企業用途

- 工業與物流

- 政府/公共部門

- 透過分銷管道

- 線上零售和市場

- 線下/實體店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 大洋洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 北非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NETGEAR Inc.

- TP-Link Corporation Limited

- Eero LLC

- Google LLC

- Linksys Holding Inc.

- ASUStek Computer Inc.

- D-Link Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Communications Co., Ltd.

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Commscope Holding Company Inc.

- ARRIS International plc

- Netis Systems Co., Ltd.

- Vilo Living Inc.

- Actiontec Electronics Inc.

- Synology Inc.

- Cambium Networks Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the mesh wi-Fi system markets size is projected to expand from USD 7.23 billion in 2025 and USD 7.82 billion in 2026 to USD 13.34 billion by 2031, registering a CAGR of 11.27% between 2026 to 2031.

This report is Segmented by Component (Hardware, Software, and Services), Band Count (Dual-Band, Tri-Band, Quad-Band, and Higher), Wi-Fi Standard (Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, and More), Distribution Channel (Online Retail and Marketplaces, and Offline/Brick-and-Mortar), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Mesh Wi-fi Systems Market Trends and Insights

Explosive Growth in Smart-Home Device Installations

Households now host 15-20 connected devices, from speakers to appliances, all vying for bandwidth. Matter 1.4.2 certification across more than 500 devices lets homeowners unify control, so mesh systems become the logical backbone. Compared with extenders, Thread-based mesh cuts packet loss by 40%, improving user satisfaction and slashing ISP support calls. As a result, retailers promote "whole-home bundles" that pair mesh kits with smart bulbs and locks. The Mesh Wi-Fi systems market, therefore, expands in lockstep with every incremental camera or voice assistant added to a residence.

Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet

Operators in South Korea, Japan, and large U.S. metros deliver symmetrical gigabit services that expose weak Wi-Fi links inside the home. To preserve promised speeds, telcos package mesh nodes into premium fiber plans, charging USD 5-10 per month and converting capital expenditure into subscription revenue. Europe's 295 million homes passed by fiber, and China's 206.8 million gigabit users repeat the pattern, proving that last-mile performance is now a competitive differentiator. Consequently, the Mesh Wi-Fi systems market captures value every time a new fiber strand reaches a front door.

Persistent Semiconductor Supply Constraints

Advanced 6 nm and 5 nm semiconductor capacity remains constrained as smartphone and data-center customers outcompete consumer networking vendors for wafer allocation. Wi-Fi 7 chipsets carry a 40-50% cost premium over Wi-Fi 6E, forcing vendors to prioritize flagship mesh systems and delay broader portfolio rollouts. Lead times extending beyond 30 weeks strain working capital, disrupt inventory planning, and limit peak-season availability. Until additional fabrication capacity comes online, supply bottlenecks will continue to suppress unit shipments, delay price normalization, and moderate near-term growth in the Mesh Wi-Fi systems market.

Other drivers and restraints analyzed in the detailed report include:

- Price Erosion in Wi-Fi 6/6E Chipsets

- Telco Adoption of Mesh CPE for Whole-Home Coverage

- Rising Cyber-Security Vulnerabilities in Home Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 63.4% of the Mesh Wi-Fi market share in 2025, as customers still purchase physical nodes as the first step toward reliable coverage. Yet service revenue, growing at a 13.81% CAGR, signals a pivot to recurring revenue as ISPs and vendors sell security subscriptions, parental controls, and analytics. The Mesh Wi-Fi systems market size tied to services is projected to outpace hardware incrementally each year between 2026 and 2031 as telcos bake USD 5-15 monthly charges into fiber bundles.

Software innovation underpins this shift. Cloud dashboards give homeowners device-level visibility, while AI engines orchestrate channel selection without user input. Vendors that master over-the-air updates and data analytics increase lifetime customer value, mitigating the 4- to 5-year replacement cycle that still governs node refreshes. The winner's playbook, therefore, combines affordable hardware with sticky cloud features that users pay for long after the initial install.

Dual-band kits held 48.19% share of the Mesh Wi-Fi system market in 2025 because cost-sensitive buyers needed only 2.4 GHz and 5 GHz coverage for email, streaming, and smart speakers. As bandwidth demand balloons, tri-band models add a second 5 GHz radio for dedicated backhaul, balancing price and performance. Quad-band systems are now expanding at a 15.62% CAGR, leveraging 6 GHz channels unlocked by global regulators.

With Wi-Fi 7, vendors dedicate one 6 GHz radio to backhaul and a second to clients, while legacy devices remain on 2.4 GHz and 5 GHz. Interference drops, latency sinks, and 8K streaming coexist with cloud gaming. As chipset pricing falls, quad-band premiums narrow, nudging power users, remote workers, and gamers toward higher-tier bundles. The Mesh Wi-Fi systems market size for quad-band products is therefore set to grow faster than any other configuration through 2031.

Geography Analysis

North America generated 38.96% of the Mesh Wi-Fi systems market revenue in 2025, underpinned by gigabit fiber coverage, smart-home penetration, and telco mesh bundles that now serve tens of millions of subscribers. The United States dominates regional value, backed by USD 42.45 billion in BEAD program funding that supports networks in every state. Canada's 12 million fiber homes and CAD 10 (USD 7.90) monthly managed Wi-Fi premiums add steady uptake, while Mexico's 8 million FTTH lines cluster mesh demand in its three largest cities.

Europe follows, buoyed by 160 million fiber subscribers and a 54% take-up rate that spotlights the inadequacy of legacy routers once speeds exceed 1 Gbps. Operators such as Deutsche Telekom and Orange integrate mesh networking into gigabit plans, while the EU's Cyber Resilience Act requires 5-year security support, boosting consumer trust. Russia deploys distributed nodes in concrete apartment blocks, highlighting how building stock shapes architectural choices in the Mesh Wi-Fi market.

Asia-Pacific is the fastest climber at a 14.28% CAGR, propelled by China's 206.8 million gigabit users and India's BharatNet project linking 250,000 villages. Japan's 85% fiber penetration and South Korea's 95% FTTH reach foster early adoption of Wi-Fi 7, as gamers demand stable, low-latency links. Southeast Asian capitals layer mesh onto new fiber backbones priced below USD 150 per kit, pushing affordable coverage into rising middle-class homes. Outside the top three regions, the Middle East modernizes broadband for Saudi Vision 2030, South America scales slowly amid macroeconomic stress, and sub-Saharan Africa remains early-stage, favoring 4G fixed wireless over FTTH for now.

- NETGEAR Inc.

- TP-Link Corporation Limited

- Eero LLC

- Google LLC

- Linksys Holding Inc.

- ASUStek Computer Inc.

- D-Link Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Communications Co., Ltd.

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Commscope Holding Company Inc.

- ARRIS International plc

- Netis Systems Co., Ltd.

- Vilo Living Inc.

- Actiontec Electronics Inc.

- Synology Inc.

- Cambium Networks Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in Smart-Home Device Installations

- 4.2.2 Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet

- 4.2.3 Price Erosion in Wi-Fi 6/6E Chipsets

- 4.2.4 Telco Adoption of Mesh CPE for Whole-Home Coverage

- 4.2.5 Government-Funded Digital-Inclusion Programs

- 4.2.6 AI-Driven Self-Healing Network Algorithms

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Constraints

- 4.3.2 Rising Cyber-Security Vulnerabilities in Home Networks

- 4.3.3 Consumer Confusion Over Wi-Fi Standards (6E vs 7)

- 4.3.4 Import Tariffs on Networking Hardware

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Band Count

- 5.2.1 Dual-Band Mesh Systems

- 5.2.2 Tri-Band Mesh Systems

- 5.2.3 Quad-Band and Higher Mesh Systems

- 5.3 By Wi-Fi Standard

- 5.3.1 Wi-Fi 5 (802.11ac)

- 5.3.2 Wi-Fi 6 (802.11ax)

- 5.3.3 Wi-Fi 6E (802.11axe)

- 5.3.4 Wi-Fi 7 (802.11be)

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial and Enterprise

- 5.4.3 Industrial and Logistics

- 5.4.4 Government and Public Sector

- 5.5 By Distribution Channel

- 5.5.1 Online Retail and Marketplaces

- 5.5.2 Offline / Brick-and-Mortar

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Oceania

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 North Africa

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NETGEAR Inc.

- 6.4.2 TP-Link Corporation Limited

- 6.4.3 Eero LLC

- 6.4.4 Google LLC

- 6.4.5 Linksys Holding Inc.

- 6.4.6 ASUStek Computer Inc.

- 6.4.7 D-Link Corporation

- 6.4.8 Ubiquiti Inc.

- 6.4.9 Zyxel Communications Corporation

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Xiaomi Communications Co., Ltd.

- 6.4.12 Shenzhen Tenda Technology Co., Ltd.

- 6.4.13 Mercusys Technologies Co., Ltd.

- 6.4.14 Commscope Holding Company Inc.

- 6.4.15 ARRIS International plc

- 6.4.16 Netis Systems Co., Ltd.

- 6.4.17 Vilo Living Inc.

- 6.4.18 Actiontec Electronics Inc.

- 6.4.19 Synology Inc.

- 6.4.20 Cambium Networks Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

通訊業者的Wi-Fi設備市場預測(至2034年)-按組件、安裝位置、技術標準、應用、最終用戶和地區分類的全球分析

通訊業者的Wi-Fi設備市場預測(至2034年)-按組件、安裝位置、技術標準、應用、最終用戶和地區分類的全球分析 無線基礎設施市場(2026年第一季):4G、5G、6G無線接取網和核心網路分析

無線基礎設施市場(2026年第一季):4G、5G、6G無線接取網和核心網路分析 電信級Wi-Fi設備市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、最終用戶、地區和競爭格局分類,2021-2031年日本無線基礎設施(2026):無線接取網路市場分析與預測 | 4G、5G、6G 基地台、開放式無線接取網路、虛擬無線接取網

電信級Wi-Fi設備市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、最終用戶、地區和競爭格局分類,2021-2031年日本無線基礎設施(2026):無線接取網路市場分析與預測 | 4G、5G、6G 基地台、開放式無線接取網路、虛擬無線接取網 2026年全球遠端Wi-Fi模組市場報告2026年全球汽車Wi-Fi模組市場報告2026年全球Wi-Fi模組市場報告

2026年全球遠端Wi-Fi模組市場報告2026年全球汽車Wi-Fi模組市場報告2026年全球Wi-Fi模組市場報告 WiFi 6 網路卡市場依產品類型、介面、最終用戶和通路分類,全球預測,2026-2032 年

WiFi 6 網路卡市場依產品類型、介面、最終用戶和通路分類,全球預測,2026-2032 年 家庭寬頻Wi-Fi設備市場規模、佔有率和成長分析(按設備類型、技術、連接類型、消費者和地區分類)-產業預測(2026-2033年)

家庭寬頻Wi-Fi設備市場規模、佔有率和成長分析(按設備類型、技術、連接類型、消費者和地區分類)-產業預測(2026-2033年) 汽車Wi-Fi模組市場規模、佔有率和成長分析(按類型、技術、銷售管道、應用和地區分類)—產業預測(2026-2033年)

汽車Wi-Fi模組市場規模、佔有率和成長分析(按類型、技術、銷售管道、應用和地區分類)—產業預測(2026-2033年)