|

市場調查報告書

商品編碼

2063818

Wi-Fi 7 路由器:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)Wi-Fi 7 Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

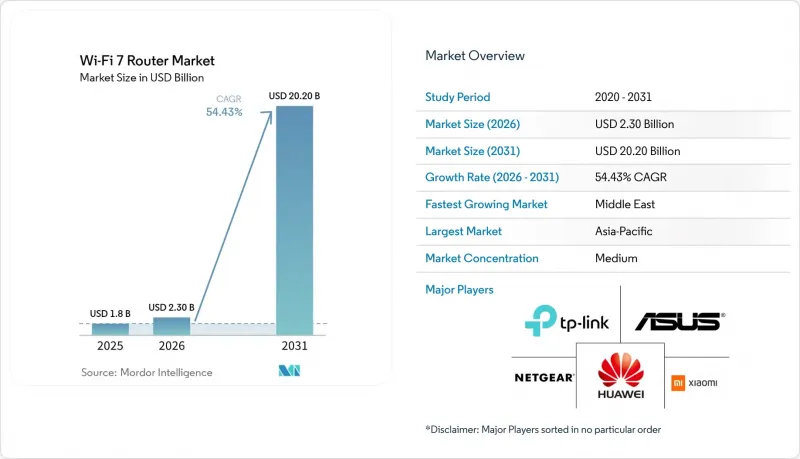

據 Mordor Intelligence 稱,2025 年 Wi-Fi 7 路由器市值為 18 億美元,預計到 2031 年將達到 202 億美元,而 2026 年為 23 億美元,2026 年至 2031 年預測期內的複合年成長率為 54.43%。

本報告按Wi-Fi標準(雙頻、三頻、四頻)、設計(傳統獨立式、網狀系統、遊戲最佳化型、企業級網路基地台)、最終用戶應用(住宅、中小企業、大型企業、公共設施、工業IoT)、銷售管道(線上、線下、服務供應商捆綁銷售等)和地區進行細分。市場預測以美元計價。

全球Wi-Fi 7路由器市場趨勢與洞察

網路服務供應商提供的多千兆網路方案激增

通訊業者正將Wi-Fi 7路由器與其5Gbps和10Gbps光纖套餐捆綁銷售,使設備從選購配件轉變為嵌入式服務層。 2026年2月,Google光纖在其Home 3G和Edge 8G套餐中整合了Wi-Fi 7硬體,提高了用戶留存率並降低了解約率。區域營運商也正在效仿這種模式,將路由器需求與其寬頻服務的差異化直接掛鉤。更短的投資回收期正促使OEM廠商轉向軟體主導的獲利模式,同時Wi-Fi 6設備的二手市場也不斷擴大。

在智慧辦公室部署高密度Wi-Fi的企業級應用

企業園區正在將Wi-Fi 6網路基地台升級到Wi-Fi 7,以適應每1000平方英尺超過100台設備的高密度部署。思科Catalyst 9170系列利用多連結操作將對延遲敏感的流量分配到6 GHz頻段,同時將正常負載轉移到5 GHz頻段,從而減少網路擁塞。 Ruckus Networks T670sn基於IEEE 802.1AS時序控制,將這項技術擴展到工業環境,並具備確定性機器控制功能。其320MHz寬頻頻道提高了每個裝置的無線吞吐量,從而減少了網路基地台總數和部署成本。然而,日益複雜的頻寬調諧正加速企業採用雲端管理網路架構。

Wi-Fi 7晶片組平均售價上漲

採用 5nm 和 6nm 製程製造的先進 Wi-Fi 7 晶片組相比 Wi-Fi 6E 晶片組成本高出 40% 至 60%,但供應商尚未能將這部分成本完全轉嫁給最終用戶。預計到 2025 年,入門級三頻路由器的價格將從 450 美元降至 250 美元左右,毛利率將壓縮至 15% 以下。在 1Gbps 寬頻主導的市場中,性能提升不足以支撐升級,從而削弱了價格的合理性。為了彌補這一不足,晶片組供應商推出了不包含 6GHz 頻段的雙頻型號,但這削弱了效能差異化,並有可能分散消費者對 Wi-Fi 7 價值的認知。

細分市場分析

預計到2031年,四頻Wi-Fi 7設備的複合年成長率將達到60.12%,超過三頻機種(後者在2025年的銷售量佔比為46.22%)。廠商在5GHz和2.4GHz頻段的基礎上,增加了兩個獨立的6GHz無線模組,從而能夠針對延遲敏感型工作負載、盡力而為型工作負載和物聯網工作負載進行精確的流量分割。這種架構使企業能夠在保持確定性吞吐量的同時降低網路基地台密度,從而降低整體擁有成本(TCO)。在6GHz頻段尚未普及的市場,雙頻設備仍有市場需求,但由於缺乏差異化,其定價能力有限,對Wi-Fi 7路由器市場整體價值的貢獻也相對較小。

客戶的準備情況正在推動升級週期。到 2026 年年中,超過 40% 的 Android 旗艦設備將配備 FastConnect 7800,這將即時催生對高頻寬路由器的需求。由於配置簡便且射頻管理複雜度較低,三頻系統仍將在住宅部署中佔據主導地位。然而,企業升級週期通常與基礎設施現代化計劃一致,目前正轉向四頻部署以適應高設備密度環境。預計這種轉變將推高平均售價,並將市場佔有率轉移到專注於企業級網路解決方案的供應商。

隨著電競場館和直播內容創作者對持續多Gigabit吞吐量和個位數毫秒延遲的需求日益成長,針對遊戲最佳化的 Wi-Fi 7 路由器預計將以 62.53% 的複合年成長率成長。多鏈路操作支援同時使用 5 GHz 和 6 GHz 頻段,從而降低競技場景中的抖動和封包遺失。儘管由於全屋覆蓋的需求,網狀網路系統將在 2025 年佔據 51.72% 的出貨量,但遊戲路由器正在建立一個高階細分市場,用戶願意為高級 QoS 控制、流量優先級和硬體差異化功能付費。與日益同質化的大眾市場路由器相比,這個細分市場展現出更強的價格韌性。

亞馬遜的 eero 7 系列產品定價比前代產品低約 30%,加劇了網狀網路系統的價格競爭,促使更多對成本敏感的家庭用戶選擇使用。獨立路由器在空間有限的情況下仍然有效,但其市佔率持續下降。隨著企業優先考慮集中管理和網路編配,企業級網路基地台正成為一個高價值的成長領域。同時,工業級 Wi-Fi 7 硬體正作為一個細分市場興起,憑藉其堅固的設計、耐高溫性能和 PoE+ 功能,滿足了製造和物流環境對可靠穩定無線連接的需求。

區域分析

到2025年,亞太地區將佔Wi-Fi 7路由器銷量的34%。這主要得益於韓國、印度和日本對6GHz頻段的早期採用。在韓國,室內EIRP限制為1瓦,使得320MHz頻段頻道可以不受距離限制地充分利用。同時,在印度,500MHz頻段將於2026年1月免許可使用,這將加速各大科技叢集企業園區的升級。在日本,5925-7125MHz頻段將作為免執照頻段淘汰,但動態頻率調整增加了部署的複雜性。相較之下,在中國,6GHz頻段分配給了IMT業務,限制了國內路由器的配置,使其只能採用雙頻配置,廠商也正在轉向出口主導成長策略。

預計到2031年,中東地區將以57.81%的複合年成長率實現最快成長,這主要得益於沙烏地阿拉伯和阿拉伯聯合大公國對智慧城市的大規模投資。在阿卜杜拉國王金融區,覆蓋全城的Wi-Fi 7網路已於2025年4月部署完畢,支援高密度連接和基於擴增實境技術的公共服務。預計到2026年底,海灣合作理事會(GCC)將統一6 GHz頻段政策,將降低認證門檻,提高設備互通性,並加速周邊區域市場的出貨。

北美和歐洲的普及趨勢有所不同。雖然像Brightspeed這樣的美國供應商將Wi-Fi 7路由器與千兆寬頻套餐捆綁銷售,但整體市場的過渡速度緩慢,超過25%的家庭仍然依賴Wi-Fi 4和Wi-Fi 5。在歐洲,即使在一些光纖覆蓋廣泛的國家,Wi-Fi 7的普及率也低於2%,這主要是由於消費者對Wi-Fi 6的滿意度以及ETSI EN 303 687標準的監管滯後。在南美和非洲,投資重點仍然放在光纖部署和固定無線網路擴充上,而不是升級到先進的用戶端設備。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網路服務供應商提供的多千兆網路方案激增

- 在智慧辦公室部署高密度Wi-Fi的企業級應用

- 在主要經濟區擴大 6 GHz 頻段頻率部署

- AR和VR串流媒體的應用場景不斷擴展

- 通訊業者提供的Wi-Fi 7相容CPE捆綁合約

- 改進 4K QAM 演算法以實現穩定的吞吐量

- 市場限制因素

- Wi-Fi 7晶片組平均售價上漲

- 先進技術(6奈米以下)的供應鏈限制因素

- 6GHz頻段共存認證方面的監理延誤。

- 與低成本 Wi-Fi 6E 部署基礎架構的競爭

- 宏觀經濟因素對市場的影響

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按 Wi-Fi 標準

- 雙頻 Wi-Fi 7 路由器

- 三頻 Wi-Fi 7 路由器

- 四頻 Wi-Fi 7 路由器

- 有意為之

- 傳統獨立路由器

- 網狀Wi-Fi系統

- 遊戲路由器

- 企業存取點

- 透過最終用戶應用程式

- 住宅

- 小型企業

- 大型企業和校園

- 公共設施及接待

- 工業IoT

- 透過分銷管道

- 線上零售

- 線下零售

- 服務供應商/CPE商品搭售

- 直接向企業銷售

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TP-Link Technologies Co., Ltd.

- ASUSTeK Computer Inc.

- Netgear, Inc.

- D-Link Corporation

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Linksys Holdings, Inc.

- Belkin International, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Zyxel Communications Corp.

- Synology Inc.

- QNAP Systems, Inc.

- Mercusys Technologies Co., Ltd.

- Edimax Technology Co., Ltd.

- Ruijie Networks Co., Ltd.

- Ruckus Wireless, Inc.

- Tenda Technology Co., Ltd.

- Keenetic Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the wi-Fi 7 router market size was valued at USD 1.8 billion in 2025 and is estimated to grow from USD 2.3 billion in 2026 to reach USD 20.2 billion by 2031, at a CAGR of 54.43% during the forecast period 2026-2031.

This report is Segmented by Wi-Fi Standard (Dual-Band, Tri-Band, Quad-Band), Design (Traditional Single-Unit, Mesh Systems, Gaming-Optimized, Enterprise Access Points), End-User Application (Residential, SME, Large Enterprises, Public Venues, Industrial IoT), Distribution Channel (Online, Offline, Service Provider Bundling, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wi-Fi 7 Router Market Trends and Insights

Surge in Multi-Gig Internet Plans Offered by ISPs

Telecom operators are bundling Wi-Fi 7 routers with 5 Gbps and 10 Gbps fiber tiers, shifting the device from a discretionary purchase to an embedded service layer. Google Fiber integrated Wi-Fi 7 hardware into its Home 3 Gig and Edge 8 Gig plans in February 2026, reinforcing contract lock-ins and reducing churn. Regional carriers are replicating this model, linking router demand directly to broadband differentiation. Compressed amortization cycles are pushing OEMs toward software-led monetization, while resale markets for Wi-Fi 6 devices are expanding in parallel.

Enterprise Adoption of High-Density Wi-Fi in Smart Offices

Corporate campuses are upgrading from Wi-Fi 6 to Wi-Fi 7 access points to support densities above 100 devices per 1,000 square feet. Cisco Catalyst 9170-series uses multi-link operation to segregate latency-sensitive traffic on 6 GHz while shifting routine loads to 5 GHz, reducing contention. Ruckus Networks T670sn extends this into industrial settings with IEEE 802.1AS-based timing for deterministic machine control. Wider 320-MHz channels increase per-radio throughput, lowering the total access point count and deployment cost. However, the complexity of spectrum coordination is accelerating enterprise adoption of cloud-managed network architectures.

Elevated Average Selling Prices of Wi-Fi 7 Chipsets

Advanced Wi-Fi 7 chipsets fabricated on 5 nm and 6 nm nodes carry a 40%-60% cost premium over Wi-Fi 6E silicon, yet vendors have been unable to fully transfer this to end users. Entry-level tri-band router prices fell from USD 450 to ~USD 250 within 2025, compressing gross margins below 15%. In markets where 1 Gbps broadband dominates, incremental performance gains are not sufficiently visible to justify upgrades, weakening price realization. To offset this, chipset suppliers are introducing dual-band variants that exclude the 6 GHz band, but this compromises performance differentiation and risks fragmenting consumer understanding of Wi-Fi 7's value.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Rollout of 6 GHz Spectrum Across Major Economies

- Proliferation of AR and VR Streaming Use-Cases

- Supply Chain Constraints for Advanced (≤ 6 nm) Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Quad-band Wi-Fi 7 equipment is projected to expand at a 60.12% CAGR through 2031, surpassing tri-band models that accounted for 46.22% of 2025 revenue. Vendors deploy two separate 6 GHz radios alongside 5 GHz and 2.4 GHz, enabling precise traffic segmentation across latency-critical, best-effort, and IoT workloads. This architecture allows enterprises to reduce access point density while maintaining deterministic throughput, improving the total cost of ownership. In markets without 6 GHz availability, dual-band devices remain relevant but lack differentiation, limiting pricing power and constraining their contribution to the overall Wi-Fi 7 router market value.

Client-side readiness is reinforcing the upgrade cycle. By mid-2026, over 40% of flagship Android devices integrated FastConnect 7800, creating immediate demand for higher-bandwidth routers. Tri-band systems will continue to dominate residential deployments due to simpler configuration and lower RF management complexity. However, enterprise refresh cycles, typically aligned with infrastructure renovation timelines, are shifting toward quad-band deployments to support dense device environments. This transition is expected to lift average selling prices and shift market share toward vendors focused on enterprise-grade networking solutions.

Gaming-optimized Wi-Fi 7 routers are projected to grow at a 62.53% CAGR, driven by esports venues and livestream creators requiring sustained multi-gigabit throughput and single-digit millisecond latency. Multi-Link Operation enables simultaneous use of 5 GHz and 6 GHz bands, reducing jitter and packet loss in competitive scenarios. While mesh systems accounted for 51.72% of 2025 shipments due to demand for whole-home coverage, gaming routers have established a premium niche where users pay for advanced quality of service controls, traffic prioritization, and hardware differentiation. This segment demonstrates stronger pricing resilience relative to commoditizing mass-market router categories.

Price compression in mesh systems is intensifying as Amazon's eero 7 lineup undercuts legacy offerings by ~30%, expanding adoption among cost-sensitive households. Single-unit routers remain viable for smaller spaces but continue to lose share. Enterprise access points represent a higher-value growth vector as organizations prioritize centralized management and network orchestration. Concurrently, industrial-grade Wi-Fi 7 hardware is emerging as a niche segment, with ruggedized designs, temperature tolerance, and PoE+ support addressing the needs of manufacturing and logistics environments that require reliable, deterministic wireless connectivity.

Geography Analysis

Asia-Pacific accounted for 34% of Wi-Fi 7 router revenue in 2025, driven by early 6 GHz enablement across South Korea, India, and Japan. South Korea's 1 W indoor EIRP limit enables full exploitation of 320 MHz channels without proximity constraints, while India's January 2026 de-licensing of 500 MHz is accelerating enterprise campus upgrades across major technology clusters. Japan allows 5925-7125 MHz for unlicensed use, though dynamic frequency coordination increases deployment complexity. In contrast, China assigns 6 GHz to IMT services, restricting domestic routers to dual-band configurations and pushing vendors toward export-driven growth strategies.

The Middle East is projected to register the fastest growth at a 57.81% CAGR through 2031, underpinned by large-scale smart-city investments in Saudi Arabia and the United Arab Emirates. King Abdullah Financial District deployed a city-wide Wi-Fi 7 network in April 2025, supporting high-density connectivity and AR-enabled public services. Anticipated harmonization of 6 GHz spectrum policies across the Gulf Cooperation Council by late 2026 is expected to reduce certification barriers, streamline device interoperability, and accelerate shipment volumes across adjacent regional markets.

Adoption trends diverge across North America and Europe. U.S. providers such as Brightspeed are bundling Wi-Fi 7 routers with multi-gig broadband plans, but over 25% of households still rely on Wi-Fi 4 and Wi-Fi 5, slowing mass-market conversion. European adoption remains below 2% in several fiber-dense countries due to consumer satisfaction with Wi-Fi 6 and regulatory delays under ETSI EN 303 687. In South America and Africa, investment priorities continue to favor fiber rollout and fixed-wireless expansion over upgrades to advanced customer-premises equipment.

- TP-Link Technologies Co., Ltd.

- ASUSTeK Computer Inc.

- Netgear, Inc.

- D-Link Corporation

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Linksys Holdings, Inc.

- Belkin International, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Zyxel Communications Corp.

- Synology Inc.

- QNAP Systems, Inc.

- Mercusys Technologies Co., Ltd.

- Edimax Technology Co., Ltd.

- Ruijie Networks Co., Ltd.

- Ruckus Wireless, Inc.

- Tenda Technology Co., Ltd.

- Keenetic Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Multi-Gig Internet Plans Offered by ISPs

- 4.2.2 Enterprise Adoption of High-Density Wi-Fi in Smart Offices

- 4.2.3 Expanding Rollout of 6 GHz Spectrum Across Major Economies

- 4.2.4 Proliferation of AR and VR Streaming Use-Cases

- 4.2.5 Integrated Wi-Fi 7 CPE Bundling Deals by Telecom Operators

- 4.2.6 4 K QAM Algorithm Enhancements Enabling Stable Throughput

- 4.3 Market Restraints

- 4.3.1 Elevated Average Selling Prices of Wi-Fi 7 Chipsets

- 4.3.2 Supply Chain Constraints for Advanced (<=6 nm) Nodes

- 4.3.3 Regulatory Delays on 6 GHz Co-existence Certification

- 4.3.4 Competition From Lower-Cost Wi-Fi 6E Install Base

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wi-Fi Standard

- 5.1.1 Dual-Band Wi-Fi 7 Routers

- 5.1.2 Tri-Band Wi-Fi 7 Routers

- 5.1.3 Quad-Band Wi-Fi 7 Routers

- 5.2 By Design

- 5.2.1 Traditional Single-Unit Routers

- 5.2.2 Mesh Wi-Fi Systems

- 5.2.3 Gaming-Optimized Routers

- 5.2.4 Enterprise Access Points

- 5.3 By End-User Application

- 5.3.1 Residential

- 5.3.2 Small and Medium Enterprises

- 5.3.3 Large Enterprises and Campuses

- 5.3.4 Public Venues and Hospitality

- 5.3.5 Industrial IoT

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.4.3 Service Provider/CPE Bundling

- 5.4.4 Enterprise Direct Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 ASUSTeK Computer Inc.

- 6.4.3 Netgear, Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Xiaomi Corporation

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 ZTE Corporation

- 6.4.8 Linksys Holdings, Inc.

- 6.4.9 Belkin International, Inc.

- 6.4.10 Ubiquiti Inc.

- 6.4.11 MikroTikls SIA

- 6.4.12 Zyxel Communications Corp.

- 6.4.13 Synology Inc.

- 6.4.14 QNAP Systems, Inc.

- 6.4.15 Mercusys Technologies Co., Ltd.

- 6.4.16 Edimax Technology Co., Ltd.

- 6.4.17 Ruijie Networks Co., Ltd.

- 6.4.18 Ruckus Wireless, Inc.

- 6.4.19 Tenda Technology Co., Ltd.

- 6.4.20 Keenetic Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment