|

市場調查報告書

商品編碼

2063809

銀行、金融服務和保險 (BFSI) 行業的人力資本管理 (HCM) 軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)HCM Software In The BFSI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

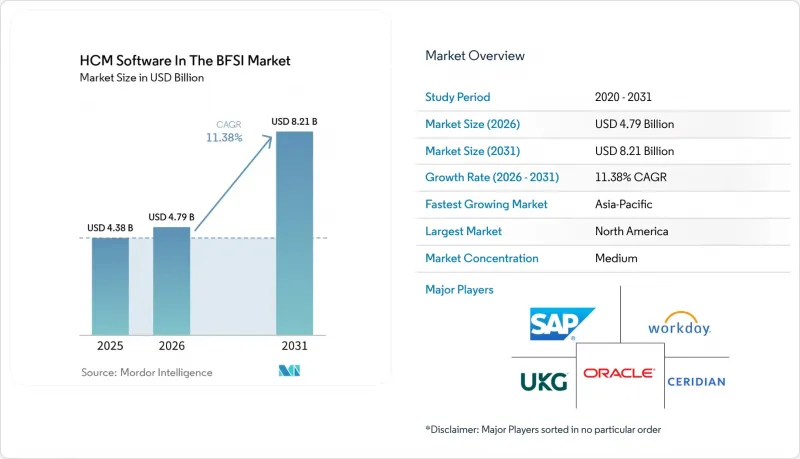

根據 Mordor Intelligence 預測,BFSI 產業的 HCM 軟體市場規模將從 2025 年的 43.8 億美元成長到 2026 年的 47.9 億美元,到 2031 年將達到 82.1 億美元,2026 年至 2031 年的複合年成長率為 11.38%。

本報告按部署模式(雲端和本地部署)、組織規模(大型企業、中小企業)、軟體類型(核心人力資源、薪資、人才管理、勞動力管理等)、服務(實施和整合服務、諮詢和培訓服務等)以及地區進行細分。市場預測以美元計價。

全球HCM軟體市場趨勢及BFSI產業洞察

全球金融服務監理日益複雜。

金融監理機構正將員工資料管治直接納入其審慎法律規範,使人力資本管理(HCM)套件轉型為合規領域的前沿系統。歐盟的《數位營運彈性法案》要求銀行整理所有第三方人力資源服務供應商並制定退出策略,這項任務非常適合擁有不可篡改審計日誌的雲端平台。巴塞爾協議III第三支柱的更新要求即時核對工資、福利和供應商支出,加速了分析模組的普及應用。在美國,紐約州第500部分網路安全修正案將加密要求擴展至人力資源資料庫,提高了為受美國監管公司提供服務的供應商的合規門檻。這種不均衡的現狀有利於那些維護特定司法管轄區規則庫的供應商,而小規模的區域性企業則難以取得法律工程資源。

主要銀行加速採用雲端運算技術

總體擁有成本 (TCO) 研究日益表明,基於訂閱的雲端人力資本管理 (HCM) 比資料中心續訂週期更具吸引力。紐約梅隆銀行 (BNY Mellon) 在 35 個國家實施 Workday 多年,整合了全球薪資核算,將月末結算時間縮短了 40%,充分展現了大規模SaaS 遷移的經濟效益。在菲律賓,中國儲蓄銀行 (China Bank Savings) 部署了 Darwinbox,將分店員工入職時間縮短了 40%,並展示了一種適用於新興市場的行動優先模式。這些案例凸顯了基於雲端的 HCM 如何實現即時勞動力分析,從而指導資本配置決策,涵蓋從分店精簡到數位化通路人員配置等各個方面。

嚴格的資料居住要求和主權要求

強制資料本地化正在將目標市場分割成孤立的區域市場。中國的《個人資料保護法》強制要求銀行將員工資料儲存在當地的伺服器上,迫使跨國公司並行維護多個人力資源系統。俄羅斯的《152-FZ法案》也施加了類似的限制,迫使西方供應商依賴本地託管合作夥伴。印度預計2026年頒布的《數位個人資料保護法》草案將進一步限制資料外流。這些法規推高了供應商的成本,並使全球平台的整合變得更加複雜。

細分市場分析

預計到 2025 年,BFSI 產業 HCM 軟體市場的雲端領域將佔 61.23%,到 2031 年將以 11.82% 的複合年成長率成長。全球領先的銀行正在採用雲端套件來滿足 DORA 審計要求並獲得即時人才洞察,而混合部署透過確保合規性、可擴展性和彈性,正在推動全球金融機構的長期現代化。

隨著銀行逐步淘汰大型主機時代的HR系統,雲端採用正在加速。紐約梅隆銀行和中國儲蓄銀行在遷移後,週期時間縮短了40%。混合模式填補了資料主權規則仍然嚴格的空白,允許敏感的薪資表保留在本地,同時將分析層部署在雲端。這種柔軟性將維持這一發展勢頭,直到透過採用通用API解決整合瓶頸為止。

預計到2025年,大型企業將佔總收入的58.23%,這反映了它們在銀行、金融服務和保險(BFSI)人力資本管理(HCM)市場的主導地位。它們的規模使它們能夠協商捆綁式契約,整合涵蓋薪資核算、合規和勞動力規劃等複雜模組。然而,隨著市場趨於飽和,成長正在放緩,未來的擴張可能更依賴更嚴格的監管和更先進的分析技術,而不是新的採用。

受全數位化貸款機構和從一開始就採用SaaS平台的區域性銀行的推動,市場上的中小企業正以11.89%的複合年成長率成長。 Levo信用社於2026年部署了Paylocity,將其薪資預支系統整合在一起。同時,Ujjivan小額金融銀行正利用本地語言介面來吸引本地人才。更短的採購週期和更少的客製化負擔使中小企業能夠在幾週內完成系統升級,從而鞏固了其作為永續成長驅動力的地位。

區域分析

2025年,北美在銀行、金融服務和保險(BFSI)行業的人力資本管理(HCM)軟體市場佔據領先地位,這主要得益於嚴格的網路安全法規和SaaS的早期應用。紐約梅隆銀行採用Workday系統,Revo信用社採用Paylocity系統,都顯示頂級和中型金融機構正在優先考慮統一薪資核算和預支薪資服務。加拿大各省勞動法的差異以及墨西哥強制推行的電子薪資核算也進一步推動了市場需求。

亞太地區將成為2031年之前成長最快的地區,這主要得益於新型銀行的快速湧現以及東協各國監管法規的協調統一。中國銀行儲蓄銀行、泰米爾納德邦商業銀行和烏吉萬小額金融銀行正在積極採用「行動優先」策略,以縮短客戶註冊時間並實現區域稅務合規的自動化。儘管中國的數據本地化法規導致市場碎片化,但也為國內雲端服務供應商帶來了機會。同時,印度頒布的資料保護法將進一步推動對區域特定實例的需求。

在歐洲,積極的雲端遷移與嚴格的資料主權監管之間保持著平衡。 DORA(資料保護規範)推動了平台升級,而GDPR和國家居住要求則減緩了跨境標準化進程。 Zalaris的託管服務合約凸顯了市場對合規營運外包的高需求。在南美洲,由於銀行考慮貨幣波動,市場成長更為穩定;而在中東和非洲,隨著NexHRM和Ramco等行動原生供應商與當地支付基礎設施的整合,市場正在逐步開放。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球金融服務監理日益複雜。

- 主要銀行加速採用雲端運算技術

- 整合人工智慧驅動的合規性分析

- 以員工體驗為中心的HR模式轉型

- 對即時薪資核算和預支薪資服務的需求

- 純數位金融機構的擴張

- 市場限制因素

- 嚴格的資料居住和主權要求

- 整合傳統核心銀行體系面臨的挑戰

- 主要金融機構的高轉換成本

- 人力資源資料中的網路安全和詐欺風險

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 雲

- 現場

- 按組織規模

- 大公司

- 小型企業

- 軟體類型

- 核心人力資源

- 薪資管理

- 人才管理

- 勞動力管理

- 分析與報告

- 按服務

- 實施和整合服務

- 諮詢和培訓服務

- 託管服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing Inc.

- Cornerstone OnDemand Inc.

- Paycom Software Inc.

- Paylocity Holding Corporation

- Intuit Inc.

- BambooHR LLC

- Gusto Inc.

- Namely Inc.

- Ramco Systems Limited

- Zoho Corporation Private Limited

- Sage Group plc

- Cegid Group

- Darwinbox Digital Solutions Private Limited

- Personio GmbH

- SumTotal Systems LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the hCM software in the BFSI market size is expected to increase from USD 4.38 billion in 2025 to USD 4.79 billion in 2026 and reach USD 8.21 billion by 2031, growing at a CAGR of 11.38% over 2026-2031.

This report is Segmented by Deployment Mode (Cloud and On-Premise), Organization Size (Large Enterprises, Small and Medium Enterprises), Software Type (Core HR, Payroll Management, Talent Management, Workforce Management, and More), Services (Implementation and Integration Services, Consulting and Training Services, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In The BFSI Market Trends and Insights

Rising Regulatory Complexity in Global Financial Services

Financial regulators now weave workforce-data governance directly into prudential frameworks, turning HCM suites into front-line compliance systems. The EU Digital Operational Resilience Act obliges banks to map every third-party HR service provider and maintain exit strategies, a task suited to cloud platforms with immutable audit logs. Basel III Pillar 3 updates demand real-time reconciliation of payroll, benefits, and contractor spend, driving uptake of analytics modules. In the United States, New York's Part 500 cybersecurity amendments extend encryption requirements to HR databases, lifting the compliance bar for vendors serving U.S.-regulated entities. This patchwork rewards providers that maintain jurisdiction-specific rule libraries, leaving smaller regional players scrambling for legal-engineering resources.

Accelerated Cloud Adoption by Tier-1 Banks

Total-cost-of-ownership studies increasingly favor subscription-based cloud HCM over data-center refresh cycles. BNY Mellon's multi-year Workday rollout unified global payroll across 35 countries and trimmed month-end close by 40%, validating large-scale SaaS migration economics. In the Philippines, Chinabank Savings deployed Darwinbox, cutting branch-staff onboarding time by 40% and showcasing a mobile-first paradigm suited to emerging markets. These examples underscore how cloud HCM enables real-time workforce analytics that guide capital-allocation decisions, from branch rationalization to digital-channel staffing.

Stringent Data Residency and Sovereignty Requirements

Data-localization mandates are fragmenting the addressable market into regional islands. China's Personal Information Protection Law requires banks to store employee data on mainland servers, prompting multinationals to maintain parallel HR instances. Russia's 152-FZ imposes similar constraints, pushing Western vendors toward local hosting partners. India's draft Digital Personal Data Protection Act, expected in 2026, would further restrict outbound data flows. These rules inflate vendor costs and complicate global platform harmonization.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI-Powered Compliance Analytics

- Shift to Employee Experience-Centric HR Models

- Legacy Core Banking System Integration Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud slice of the HCM software market in the BFSI sector accounted for 61.23% in 2025 and is forecast to grow at a 11.82% CAGR through 2031. Leading global banks selected cloud suites to meet DORA audit requirements and gain real-time workforce insights, while hybrid adoption ensures compliance, scalability, and resilience, driving long-term modernization across financial institutions worldwide.

Cloud adoption accelerates as banks retire mainframe-era HR engines; BNY Mellon and Chinabank Savings demonstrated 40% cycle-time reductions post-migration. Hybrid models bridge gaps where strict data-sovereignty rules persist, allowing analytics layers to reside in the cloud while sensitive payroll tables stay on-premise. This flexibility sustains momentum until universal API adoption removes integration bottlenecks.

Large enterprises commanded 58.23% of revenue in 2025, reflecting their dominance in the BFSI HCM market. Their scale allows them to negotiate bundled contracts and integrate complex modules across payroll, compliance, and workforce planning. However, growth is slowing as saturation sets in, with future expansion tied more to regulatory upgrades and advanced analytics than to fresh deployments.

SMEs in the market are advancing at an 11.89% CAGR, driven by digital-only lenders and community banks that deploy SaaS platforms from the outset. Levo Credit Union adopted Paylocity in 2026 to integrate earned-wage access, while Ujjivan Small Finance Bank leverages vernacular interfaces to reach rural talent pools. Faster procurement cycles and reduced customization burdens enable SMEs to roll out upgrades in weeks, positioning them as durable growth engines.

Geography Analysis

North America led the HCM software market in BFSI during 2025, driven by stringent cybersecurity rules and early SaaS adoption. BNY Mellon's Workday rollout and Levo Credit Union's Paylocity deployment illustrate how both top-tier and mid-tier institutions prioritize unified payroll and earned-wage access. Canada's provincial labor-law variations and Mexico's electronic payroll mandates add incremental demand.

Asia-Pacific is the fastest-growing region through 2031, fueled by rapid neobank proliferation and regulatory harmonization across ASEAN. Chinabank Savings, Tamilnad Mercantile Bank, and Ujjivan Small Finance Bank showcase mobile-first deployments that cut onboarding times and automate localized tax compliance. China's data-localization rules fragment the landscape but create opportunities for domestic cloud providers, while India's upcoming data-protection act will further boost demand for region-specific instances.

Europe balances aggressive cloud migration with strict oversight of data sovereignty. DORA drives platform upgrades, while GDPR and national residency rules slow cross-border standardization. Zalaris' managed-services deal highlights appetite for outsourcing compliance. South America's growth is steadier as banks weigh currency volatility, and the Middle East and Africa are opening via mobile-native vendors such as NexHRM and Ramco that integrate with local payment rails.

- Workday Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing Inc.

- Cornerstone OnDemand Inc.

- Paycom Software Inc.

- Paylocity Holding Corporation

- Intuit Inc.

- BambooHR LLC

- Gusto Inc.

- Namely Inc.

- Ramco Systems Limited

- Zoho Corporation Private Limited

- Sage Group plc

- Cegid Group

- Darwinbox Digital Solutions Private Limited

- Personio GmbH

- SumTotal Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Regulatory Complexity in Global Financial Services

- 4.2.2 Accelerated Cloud Adoption by Tier-1 Banks

- 4.2.3 Integration of AI-Powered Compliance Analytics

- 4.2.4 Shift to Employee Experience-Centric HR Models

- 4.2.5 Demand for Real-Time Payroll and Earned Wage Access

- 4.2.6 Expansion of Digital-Only Financial Institutions

- 4.3 Market Restraints

- 4.3.1 Stringent Data Residency and Sovereignty Requirements

- 4.3.2 Legacy Core Banking System Integration Challenges

- 4.3.3 High Switching Costs for Large Financial Institutions

- 4.3.4 Cybersecurity and Fraud Risks in HR Data

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensdity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Software Type

- 5.3.1 Core HR

- 5.3.2 Payroll Management

- 5.3.3 Talent Management

- 5.3.4 Workforce Management

- 5.3.5 Analytics & Reporting

- 5.4 By Services

- 5.4.1 Implementation and Integration Services

- 5.4.2 Consulting and Training Services

- 5.4.3 Managed Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 UKG Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 Automatic Data Processing Inc.

- 6.4.7 Cornerstone OnDemand Inc.

- 6.4.8 Paycom Software Inc.

- 6.4.9 Paylocity Holding Corporation

- 6.4.10 Intuit Inc.

- 6.4.11 BambooHR LLC

- 6.4.12 Gusto Inc.

- 6.4.13 Namely Inc.

- 6.4.14 Ramco Systems Limited

- 6.4.15 Zoho Corporation Private Limited

- 6.4.16 Sage Group plc

- 6.4.17 Cegid Group

- 6.4.18 Darwinbox Digital Solutions Private Limited

- 6.4.19 Personio GmbH

- 6.4.20 SumTotal Systems LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment