|

市場調查報告書

商品編碼

2063752

教育產業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)HCM Software In Education - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

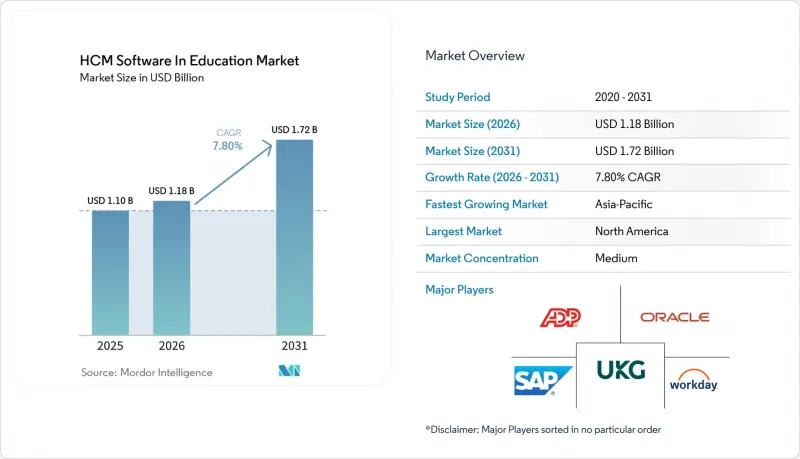

根據 Mordor Intelligence 預測,教育產業 hCM 軟體的市場規模預計將在 2025 年達到 11 億美元,2026 年達到 11.8 億美元,到 2031 年達到 17.2 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.8%。

本報告按部署模式(雲端和本地部署)、解決方案(核心人力資源、人才管理、人力資源管理、薪資核算、學習與發展)、教育機構類型(中小學、社區學院、大學、職業技術學院)、最終用戶(教師等)和地區進行細分。市場預測以美元計價。

全球HCM軟體市場趨勢及教育領域洞察

在大學推廣雲端優先策略

為了降低資料中心成本並支援遠端教職員訪問,各大學正在加速將薪資核算、福利和招聘業務遷移到雲端。自2024年以來,隨著混合式學習和多校區模式的興起,固定基礎設施的限制日益凸顯,這一轉變勢頭愈發強勁。供應商現在提供資料轉換工具、沙箱和託管服務,以降低複雜遷移帶來的風險。此外,雲端版本每季發布新功能,使教育機構無需進行耗時的升級專案即可實現分析和行動自助服務。 Workday 在2026會計年度財報中指出,隨著大規模公立大學以整合式雲端套件取代其傳統ERP系統,教育產業的訂單實現了兩位數成長。因此,教育領域的人力資本管理(HCM)軟體市場正經歷從本地部署到雲端訂閱的穩定工作負載遷移。儘管由於客製化ERP系統的高昂投資成本,仍存在一些阻力,但受維護合約到期和靈活擴展等因素的推動,企業仍然傾向於採用雲端服務。

加強對教師經驗管理的關注

教育機構正將教師滿意度視為一項策略重點,並將情緒分析、工作量追蹤和職業發展儀錶板整合到人力資源工作流程中。經驗管理工具能清楚展現教學負擔、科學研究成果及日常營運職責等數據,使院長能及早發現失衡之處。這項重視與STEM(科學、技術、工程和數學)領域教授競爭激烈的勞動力市場相契合,因為職業倦怠和人才流失會威脅到專案的持續發展。提案導師制組合、提醒管理人員注意工作量過大徵兆以及與學習發展資源庫整合的解決方案正日益普及。儘管管治的複雜性依然存在,例如教職員委員會要求公開績效指標如何影響晉升和終身教職,但各機構現在都將全面的員工敬業度分析視為人才保留的關鍵。

公共機構的預算限制

由於預算停滯、入學人數下降以及通膨壓力,公立大學無法獲得資金來升級其老化的人力資源系統,只能被迫延長現有系統的使用壽命。校董會通常會凍結招聘並推遲與IT相關的資本投資,以便將資金分配給教育優先事項。因此,供應商被迫提案分階段部署、延期付款或託管服務模式,將成本從資本投資預算轉移到營運預算。在財務狀況不確定的環境下,即使是極具吸引力的總體擁有成本 (TCO) 分析也難以克服管治的障礙。因此,緊張的融資延緩了升級週期,並限制了人力資本管理 (HCM) 軟體在教育市場的整體擴張。

細分市場分析

到2025年,本地部署系統將佔總收入的66.78%,這反映出大學希望繼續掌控敏感的薪資和福利記錄,而雲端訂閱的複合年成長率(CAGR)為10.72%。隨著中型大學從固定伺服器成本轉向可變訂閱費用,預計到2031年,教育市場採用雲端技術的人力資本管理(HCM)軟體市場規模將超過本地部署系統。

目前,混合架構彌合了傳統學生管理系統和雲端人力資源模組之間的差距,使教育機構能夠在滿足資料居住要求的同時,採用僅在雲端提供的AI功能。供應商提供自主託管選項和現成的連接器,用於跨環境同步記錄,從而減輕了曾經阻礙遷移的整合負擔。

儘管預計到2025年核心人力資源管理將維持45.61%的市場佔有率,但隨著大學競相吸引和留住專業教師,人才管理套件正以9.42%的複合年成長率快速成長。學習與發展目錄、人工智慧驅動的招聘以及微證書追蹤功能,使教育機構能夠利用以往僅限於企業人力資源部門使用的工具,從而擴大了人力資本管理軟體在教育領域戰略人才模組的市場佔有率。

儘管由於稅收和福利法規的不斷變化,薪資核算引擎仍然至關重要,但創新正著力於整合互動式代理,以解決薪資查詢並檢測和提醒異常情況。 ADP 於 2026 年 1 月發布的「AI 代理」可自動處理日常薪資查詢並檢測薪資核算中的異常情況,這反映了該公司在同質化領域尋求差異化的努力。這表明,差異化正在從事務處理轉向以使用者體驗為中心的功能。

區域分析

北美仍然是最大的區域貢獻者,預計到2025年將佔總收入的36.18%,這得益於該地區對雲端運算的早期採用以及《聯邦教育記錄隱私保護法》(FERPA)的嚴格管治。儘管面臨州財政預算壓力,私立大學和主要公立大學仍在繼續投資整合套件,從而保持了穩定的需求。加拿大也呈現類似的趨勢,各州都在支持數位化校園計畫。同時,墨西哥的教育機構已開始逐步淘汰人工考勤管理,但由於IT基礎設施有限,進展緩慢。

亞太地區是成長最快的地區,複合年成長率達8.98%。在中國和印度,政府正大力津貼數位化校園項目,以實現薪資核算和人才分析的標準化,並扶持與國家醫療和認證體系對接的本地供應商。在澳大利亞,雲端運算普及率很高,學習和發展工具的應用也較為成熟。但在日本,情況依然較為謹慎,私立大學在考慮進行雲端運算試點部署的同時,仍將敏感資料儲存在本地叢集上。

在歐洲,由於GDPR合規要求和南歐國家預算削減導致採購週期延長,成長緩慢。英國和德國正在對其人力資源和財務系統進行現代化改造,以加強審計應對力,而法國、義大利和西班牙集中式的公務員薪資系統卻阻礙了貿易發展。在中東,隨著沙烏地阿拉伯和阿拉伯聯合大公國將人力資本管理(HCM)要求納入國家教育改革計劃,強制要求在整合平台上追蹤教師培訓情況,市場正在加速成長。南美和非洲仍在發展中,但一些本地新創公司透過在地化的薪資核算和語言介面,正在為資源有限的小規模院校打開教育領域的人力資本管理軟體市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大學中「雲端優先」策略的擴展

- 教師經驗管理日益受到關注

- 人工智慧驅動的技能映射整合

- 學術機構薪資核算合規負擔日益加重

- 校園內混合辦公室模式的推廣

- 以數據分析主導的學生就業計畫的需求

- 市場限制因素

- 公共機構的預算限制

- 學生僱員的資料隱私問題引發了人們的擔憂。

- 分散的遺留SIS和ERP系統

- 小規模學院資訊科技人員短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 透過解決方案

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資核算

- 學習與發展

- 引擎類型

- K-12教育機構

- 社區大學

- 大學

- 職業技術教育機構

- 最終用戶

- 教職員

- 管理人員

- 學生員工

- 承包商和分包商

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- Oracle Corporation

- SAP SE

- UKG Inc.

- Cornerstone OnDemand Inc.

- Instructure Holdings Inc.

- Ellucian Company LP

- PeopleAdmin Inc.

- Frontline Technologies Group LLC

- PowerSchool Holdings Inc.

- ADP Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- BambooHR LLC

- Paycor HCM Inc.

- Namely Inc.

- Gusto, Inc.

- Ramco Systems Limited

- Civica UK Limited

- Blackboard Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the hCM software in education market size is expected to be USD 1.10 billion in 2025, USD 1.18 billion in 2026, and reach USD 1.72 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, and On-Premises), Solution (Core HR, Talent Management, Workforce Management, Payroll, and Learning and Development), Institution Type (K-12 Schools, Community Colleges, Universities, and Vocational and Technical Institutes), End-User (Faculty and Staff, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Education Market Trends and Insights

Growing Cloud-First Strategies Among Universities

Universities are accelerating migrations of payroll, benefits, and recruiting to cloud suites to eliminate data-center costs and support remote faculty access. The shift gained momentum after 2024 when hybrid teaching and multi-campus models exposed the limitations of fixed infrastructure. Providers now package data-conversion tools, sandboxes, and managed services that de-risk complex cutovers. Cloud editions also deliver quarterly feature releases, letting institutions adopt analytics and mobile self-service without long upgrade projects. Workday reported in its fiscal 2026 earnings that education-sector bookings grew by double digits, driven by large public universities replacing legacy ERP stacks with integrated cloud suites. As a result, the HCM software in education market records a steady transfer of workloads from on-premises to cloud subscriptions. Resistance persists where sunk costs in customized ERP stacks remain high, yet expiring maintenance contracts and the lure of elastic scaling continue to tip business cases in favor of cloud adoption.

Increasing Emphasis on Faculty Experience Management

Academic employers are elevating faculty satisfaction to strategic priority, embedding sentiment analysis, workload tracking, and professional-development dashboards into HR workflows. Experience-management tools surface data on teaching loads, research output, and service commitments, enabling deans to spot inequities early. The emphasis aligns with a competitive labor market for STEM professors, where burnout and poaching threaten program continuity. Solutions that recommend mentorship pairings, alert administrators to looming overloads, and integrate with learning-development libraries are gaining favor. Governance complexities remain, because faculty senates demand transparency on how metrics influence promotion and tenure, yet institutions now view holistic engagement analytics as essential for retention.

Budgetary Constraints in Public Institutions

Flat appropriations, enrollment dips, and inflationary pressures leave public universities extending the lives of aging HR systems rather than funding replacements. Boards often freeze hiring and defer IT capital outlays, reserving cash for instructional priorities. Consequently, vendors must propose phased deployments, deferred payment terms, or managed-service models that shift costs from capital to operating budgets. Even attractive total-cost-of-ownership analyses struggle to clear governance hurdles when fiscal forecasts remain uncertain. The funding squeeze therefore slows upgrade cycles and tempers overall expansion of the HCM software in education market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI-Powered Skills Mapping

- Rising Compliance Burden for Academic Payroll

- Data-Privacy Concerns Around Student Employees

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises systems held 66.78% of 2025 revenue, reflecting universities' desire to retain control of sensitive payroll and benefits records, yet cloud subscriptions are rising at a 10.72% CAGR. The HCM software in education market size for cloud deployments is expected to outpace on-premises growth through 2031 as mid-tier colleges convert fixed server costs into variable subscription fees.

Hybrid architectures now bridge legacy student systems and cloud HR modules, letting institutions meet data-residency mandates while adopting AI features delivered only in cloud releases. Vendors offer sovereign hosting options and pre-built connectors that synchronize records between environments, reducing the integration burden that once deterred migrations.

Core HR maintained 45.61% share in 2025, but talent-management suites are expanding at a 9.42% CAGR as universities compete to attract and retain specialized faculty. Learning-development catalogs, AI-driven recruiting, and micro-credential tracking give institutions tools once confined to corporate HR, broadening the HCM software in education market share for strategic talent modules.

Payroll engines remain indispensable because of ever-changing tax and benefit regulations, yet innovation concentrates on embedding conversational agents that resolve pay inquiries and surface anomaly alerts. ADP's launch of AI Agents in January 2026, which automate routine payroll inquiries and flag anomalies in pay runs, represents an effort to inject differentiation into a commoditized category. This indicates that differentiation is migrating from transactional processing to experience-centric capabilities.

Geography Analysis

North America remained the largest regional contributor with 36.18% revenue in 2025 thanks to early cloud adoption and strict FERPA governance. Private universities and flagship publics continue to fund integrated suites even amid state budget pressure, sustaining steady demand. Canada follows similar patterns as provinces sponsor digital-campus initiatives, while Mexico's institutions begin phasing out manual timekeeping, albeit at slower pace because of limited IT infrastructure.

Asia-Pacific is the fastest-growing territory, posting an 8.98% CAGR. China and India channel government grants into digital-campus programs that standardize payroll and talent analytics, lifting local vendors that integrate with national insurance and accreditation systems. Australia shows high cloud penetration and mature learning-development adoption, whereas Japan remains cautious, keeping sensitive data in on-premises clusters but exploring cloud pilots at private universities.

Europe grows modestly as GDPR compliance and budget austerity in southern states elongate procurement cycles. The United Kingdom and Germany modernize HR and finance stacks to enhance audit readiness, yet centralized civil-service pay frameworks in France, Italy, and Spain slow deal flow. The Middle East accelerates as Saudi Arabia and the United Arab Emirates embed HCM requirements in national education-transformation plans, mandating faculty-development tracking inside integrated platforms. South America and Africa are nascent, but regional startups that localize payroll and language interfaces open the HCM software in education market to smaller colleges with constrained resources.

- Workday Inc.

- Oracle Corporation

- SAP SE

- UKG Inc.

- Cornerstone OnDemand Inc.

- Instructure Holdings Inc.

- Ellucian Company L.P.

- PeopleAdmin Inc.

- Frontline Technologies Group LLC

- PowerSchool Holdings Inc.

- ADP Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- BambooHR LLC

- Paycor HCM Inc.

- Namely Inc.

- Gusto, Inc.

- Ramco Systems Limited

- Civica UK Limited

- Blackboard Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cloud-First Strategies Among Universities

- 4.2.2 Increasing Emphasis on Faculty Experience Management

- 4.2.3 Integration of AI-Powered Skills Mapping

- 4.2.4 Rising Compliance Burden for Academic Payroll

- 4.2.5 Expansion of Hybrid Work Models in Campuses

- 4.2.6 Demand for Analytics-Driven Student Employment Programs

- 4.3 Market Restraints

- 4.3.1 Budgetary Constraints in Public Institutions

- 4.3.2 Data-Privacy Concerns Around Student Employees

- 4.3.3 Fragmented Legacy SIS and ERP Stacks

- 4.3.4 Limited IT Talent in Small Colleges

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.2 By Solution

- 5.2.1 Core HR

- 5.2.2 Talent Management

- 5.2.3 Workforce Management

- 5.2.4 Payroll

- 5.2.5 Learning and Development

- 5.3 By Institution Type

- 5.3.1 K-12 Schools

- 5.3.2 Community Colleges

- 5.3.3 Universities

- 5.3.4 Vocational and Technical Institutes

- 5.4 By End-User

- 5.4.1 Faculty and Staff

- 5.4.2 Administrative HR

- 5.4.3 Student Employees

- 5.4.4 Contractors and Adjuncts

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 UKG Inc.

- 6.4.5 Cornerstone OnDemand Inc.

- 6.4.6 Instructure Holdings Inc.

- 6.4.7 Ellucian Company L.P.

- 6.4.8 PeopleAdmin Inc.

- 6.4.9 Frontline Technologies Group LLC

- 6.4.10 PowerSchool Holdings Inc.

- 6.4.11 ADP Inc.

- 6.4.12 Ceridian HCM Holding Inc.

- 6.4.13 Paycom Software Inc.

- 6.4.14 BambooHR LLC

- 6.4.15 Paycor HCM Inc.

- 6.4.16 Namely Inc.

- 6.4.17 Gusto, Inc.

- 6.4.18 Ramco Systems Limited

- 6.4.19 Civica UK Limited

- 6.4.20 Blackboard Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

教育證書檢驗市場預測至2034年—按組件、部署模式、檢驗類型、技術、應用、最終用戶和地區分類的全球分析

教育證書檢驗市場預測至2034年—按組件、部署模式、檢驗類型、技術、應用、最終用戶和地區分類的全球分析 2026年全球閱讀理解應用市場報告教育軟體市場預測至2034年—按軟體類型、部署模式、教育程度、應用、最終用戶和地區分類的全球分析

2026年全球閱讀理解應用市場報告教育軟體市場預測至2034年—按軟體類型、部署模式、教育程度、應用、最終用戶和地區分類的全球分析 2026-2030年全球教育應用市場2026年全球數學軟體市場報告

2026-2030年全球教育應用市場2026年全球數學軟體市場報告 防盜軟體市場:按類型、交付方式、組織規模、最終用戶和部署方式分類-2026-2032年全球市場預測教育類應用市場:2026-2032年全球市場預測(依應用類型、主題、獲利模式、設備類型、平台、應用類型及交付方式分類)2026年全球自適應學習軟體市場報告課件市場:依內容類型、平台類型和學科領域分類-2026-2032年全球預測2026年全球K-12教育學習管理系統市場報告

防盜軟體市場:按類型、交付方式、組織規模、最終用戶和部署方式分類-2026-2032年全球市場預測教育類應用市場:2026-2032年全球市場預測(依應用類型、主題、獲利模式、設備類型、平台、應用類型及交付方式分類)2026年全球自適應學習軟體市場報告課件市場:依內容類型、平台類型和學科領域分類-2026-2032年全球預測2026年全球K-12教育學習管理系統市場報告