|

市場調查報告書

商品編碼

2063738

南美洲汽車碳纖維複合材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)South America Automotive Carbon Fiber Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

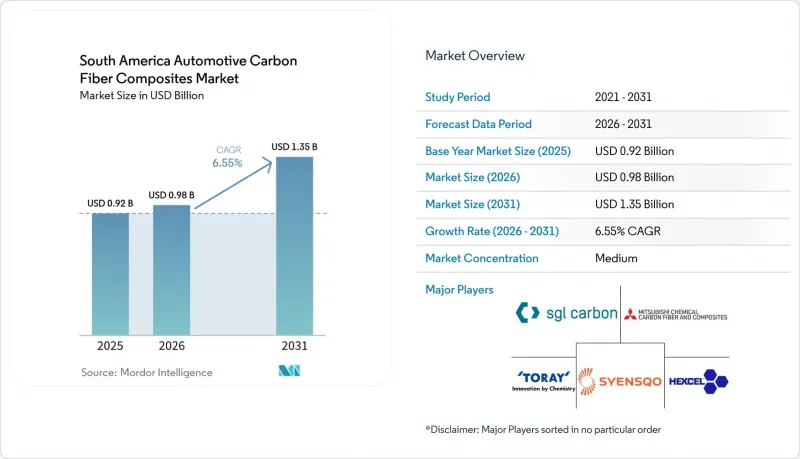

根據 Mordor Intelligence 預測,南美汽車碳纖維複合材料市場規模將從 2025 年的 9.2 億美元和 2026 年的 9.8 億美元成長到 2031 年的 13.5 億美元,2026 年至 2031 年的複合年成長率為 6.55%。

本報告按產品類型(樹脂轉注成形、手工積層、真空灌注模塑、射出成型)、應用領域(結構件、動力傳動系統總成件等)、車輛類型(乘用車、商用車)和地區(巴西、阿根廷等)進行細分。市場預測以美元計價。

南美洲汽車碳纖維複合材料市場趨勢與洞察

從內燃機轉向電動車,降低車輛重量

電池式電動車(BEV)平台比內燃機汽車重300-400公斤,除非減輕底盤重量,否則續航里程會下降。車輛總重每降低10%,電動車的續航里程就能增加6-8%。碳纖維車身面板比鋼材輕50-60%,結構件比鋁材輕30-35%。一體成型壓模成型製程可在5分鐘內完成車頂面板的硬化,展現了目前生產效率的提升。一旦年產量超過15,000輛,採用連續纖維部件將成為可能。預計到2035年,拉丁美洲的乘用車需求將超過900萬輛,因此,如今以輕量化為設計理念的OEM平台將在未來實現規模經濟效益。巴西已經出現了早期商業性成功案例。 Suzano公司用於紙漿運輸的電動卡車表明,在不超出軸重限制的情況下,可以透過減輕重量來增加負載容量。

嚴格的區域二氧化碳排放法規

巴西的「車輛空氣污染控制計畫 (PROCONVE)」L-8 將車隊平均二氧化碳排放限制在 2028 年前每公里 101 克,超標每克罰款 150 雷亞爾。除非汽車製造商能夠透過減輕車重來抵消內燃機和電池排放的罰款,否則將面臨與車重無關的罰款。因此,複合複合材料引擎蓋、車頂和尾門的使用成為優先事項。阿根廷也於 2024 年推出了類似的框架,但由於貨幣限制導致預浸料進口複雜,其實施仍不均衡。南方共同市場與歐盟達成的協議將生命週期碳核算應用於出口車型,並鼓勵原始設備製造商 (OEM) 過渡到使用再生纖維和生物基樹脂,並發布環境產品聲明 (EPD)。

碳纖維成本和前驅體價格飆升

碳纖維的交易價格為每公斤15至30美元,是鋼鐵和鋁價格的數倍。這是因為聚丙烯腈(PAN)前驅體佔最終生產成本的一半以上。 2025年,巴西石油公司(Petrobras)優先生產丙烯酸纖維而非出口前驅體,導致PAN現貨價格在六個月內上漲了21%。由於生產一噸纖維需要消耗高達3萬千瓦時的電力,巴西的工業用電價格使生產成本增加了約2,700美元,阻礙了碳化製程在國內的推廣。來自中國的大直徑碳纖維在離岸價(FOB)上更便宜,但35%的反傾銷稅限制了區域內的套利空間。

細分市場分析

預計到2031年,射出成型的複合年成長率將達到6.95%,這意味著伺服驅動注塑機和套模塗佈製程的年產量將達到5萬件。 Syensqo公司的Fibreject製程能夠生產短纖維熱塑性外殼,將生產週期縮短至兩分鐘以內,這對於南美洲汽車碳纖維複合材料市場中大批量轎車而言至關重要。相比之下,預計到2025年,樹脂轉注成形(RTM)將佔南美汽車碳纖維複合材料市場40.87%的佔有率。手工積層在小批量生產的客車和卡車零件中仍然普遍存在,因為這些零件的模具攤銷成本很低,但由於巴西工資通膨的加劇,其成本優勢正在逐漸減弱。

真空灌注成型過程介於兩者之間,能夠在4-8小時內成型中等批量電池外殼,模具成本僅為高壓釜成型的一半。如果能夠克服本地纖維成本壁壘,東麗的下一代壓模成型製程預計在2030年前取代RTM製程用於生產車頂板。射出成型的需求與乘用車的電氣化密切相關,因為降低零件成本可以抵消電池的高成本。專注於自動纖維鋪放(AFP)的製造商仍需要國內的纖維束鋪放生產線來確保原料的穩定供應,這凸顯了整合上游工程的戰略意義。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從內燃機轉向電動車,降低車輛重量

- 嚴格的區域二氧化碳排放目標

- 政府對永續材料的獎勵

- 南方共同市場區域內的國內採購規則

- 模組化電池組設計需要碳纖維增強複合材料(CFRP)機殼

- 市場限制因素

- 碳纖維高成本,前驅體價格飆升

- 先進複合材料加工領域熟練工人短缺

- 丙烯腈前驅區域供不應求

- 巴西對PAN纖維的進口關稅政策不透明

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 樹脂轉注成形

- 手工積層

- 真空灌注處理

- 射出成型

- 按應用程式類型

- 結構組裝

- 動力傳動系統部件

- 內部的

- 外部的

- 車輛類型

- 搭乘用車

- 商用車輛

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ACTION COMPOSITES

- Aksa Carbon

- Carbon Revolution

- Formosa Plastics Corporation

- Hexcel Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Mubea CarboTech

- Owens Corning

- Plasan North America

- SGL Carbon

- Syensqo

- TEIJIN Ltd.

- TORAY INDUSTRIES, INC.

- Voith Composites

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america automotive carbon fiber composites market size is projected to expand from USD 0.92 billion in 2025 and USD 0.98 billion in 2026 to USD 1.35 billion by 2031, registering a CAGR of 6.55% between 2026 to 2031.

This report is Segmented by Production Type (Resin Transfer Molding, Hand Layup, Vacuum Infusion Processing, and Injection Molding), Application Type (Structural Assemblies, Powertrain Components, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), and Geography (Brazil, Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America Automotive Carbon Fiber Composites Market Trends and Insights

ICE-to-EV Lightweighting Push

Battery-electric platforms carry a 300-400 kg mass penalty versus internal-combustion counterparts, which erodes range unless chassis weight drops. Every 10% curb-weight cut extends EV range by 6-8%, and carbon fiber delivers 50-60% savings against steel in body panels and 30-35% against aluminum in structural nodes. Integrated press-molding that cures roof panels in under five minutes demonstrates the productivity gains now possible, making continuous-fiber parts viable once annual volumes pass 15,000 units. Latin American passenger-car demand is set to rise past 9 million units by 2035, so OEM platforms engineered for lightweighting today will bank scale benefits later. Early commercial success is visible in Brazil, where electric trucks that haul pulp for Suzano show how mass savings can raise payload without breaching axle limits.

Stringent Regional CO2 Fleet Targets

Brazil's Programa de Controle da Poluicao do Ar por Veiculos Automotores (PROCONVE) L-8 caps fleet-average emissions at 101 g CO2/km by 2028, backed by penalties of BRL 150 per excess gram per vehicle. Automakers will incur material-neutral fines unless mass reductions offset combustion or battery penalties, so composite hoods, roof panels, and tailgates are climbing priority lists. Argentina rolled out a similar framework in 2024, though its enforcement remains uneven because currency controls complicate prepreg imports. The Mercosur-EU pact overlays lifecycle-carbon accounting on export models, nudging OEMs toward recycled fiber streams and bio-based resins that carry published environmental product declarations.

High Carbon-Fiber Cost and Precursor Price Spikes

Carbon fiber trades at USD 15-30 per kg, many multiples above steel and aluminum, because PAN precursor forms more than half of the final production cost. Petrobras prioritized acrylic fiber over export precursor in 2025, which lifted spot PAN pricing 21% inside six months. Since a ton of fiber consumes up to 30,000 kWh, Brazil's industrial power tariff adds nearly USD 2,700 to production cost, deterring local carbonization. Chinese large-tow grades are lower on a free-on-board basis, yet a 35% antidumping duty blocks easy arbitrage inside the bloc.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Sustainable Materials

- Domestic-Content Rules Within Mercosur Bloc

- Skills Shortage in Advanced-Composite Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injection molding's 6.95% CAGR through 2031 shows how servo-driven presses and in-mold coatings are scaling toward 50,000 parts per year. Syensqo's Fibreject process supports short-fiber thermoplastic housings that drop cycle times below two minutes, a critical gate for high-volume sedans in the South America automotive carbon fiber composites market. In contrast, resin transfer molding held 40.87% South America automotive carbon fiber composites market share in 2025. Hand Layup persists in low-volume bus and truck parts where tool amortization stays minor, but rising Brazilian wage inflation narrows its cost edge.

Vacuum Infusion splits the difference, with mid-volume battery enclosures molded in 4-8 hours and tooling costs half that of autoclaves. Toray's next-gen press-molding could displace RTM for roof panels by 2030 if local fiber cost hurdles fall. Demand for Injection Molding aligns with passenger-car electrification because lower part cost offsets the battery premium. Producers betting on automated fiber placement still need a domestic tow-spreading line to lock in feedstock security, reinforcing the strategic case for upstream integration.

List of Companies Covered in this Report:

- 3M

- ACTION COMPOSITES

- Aksa Carbon

- Carbon Revolution

- Formosa Plastics Corporation

- Hexcel Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Mubea CarboTech

- Owens Corning

- Plasan North America

- SGL Carbon

- Syensqo

- TEIJIN Ltd.

- TORAY INDUSTRIES, INC.

- Voith Composites

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ICE-to-EV lightweighting push

- 4.2.2 Stringent regional CO2-fleet targets

- 4.2.3 Government incentives for sustainable materials

- 4.2.4 Domestic-content rules within Mercosur bloc

- 4.2.5 Modular battery-pack designs demanding CFRP enclosures

- 4.3 Market Restraints

- 4.3.1 High carbon-fiber cost and precursor price spikes

- 4.3.2 Skills shortage in advanced-composite processing

- 4.3.3 Limited acrylonitrile precursor availability regionally

- 4.3.4 Uncertain Brazilian import tariff policy on PAN fibers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Resin Transfer Molding

- 5.1.2 Hand Layup

- 5.1.3 Vacuum Infusion Processing

- 5.1.4 Injection Molding

- 5.2 By Application Type

- 5.2.1 Structural Assemblies

- 5.2.2 Power-train Components

- 5.2.3 Interiors

- 5.2.4 Exteriors

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACTION COMPOSITES

- 6.4.3 Aksa Carbon

- 6.4.4 Carbon Revolution

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 Hexcel Corporation

- 6.4.7 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.8 Mubea CarboTech

- 6.4.9 Owens Corning

- 6.4.10 Plasan North America

- 6.4.11 SGL Carbon

- 6.4.12 Syensqo

- 6.4.13 TEIJIN Ltd.

- 6.4.14 TORAY INDUSTRIES, INC.

- 6.4.15 Voith Composites

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

汽車碳纖維市場:預測(至2034年)-按纖維類型、樹脂類型、複合材料類型、製造流程、車輛類型、應用、最終用戶和地區分類的全球分析

汽車碳纖維市場:預測(至2034年)-按纖維類型、樹脂類型、複合材料類型、製造流程、車輛類型、應用、最終用戶和地區分類的全球分析 全球汽車碳纖維複合材料市場:機會與策略展望(至2035年)

全球汽車碳纖維複合材料市場:機會與策略展望(至2035年) 汽車碳纖維市場:依車輛種類、原料、纖維等級及應用分類-2026-2032年全球市場預測2026年全球智慧尾門市場報告汽車用碳纖維熱塑性塑膠市場:依纖維類型、車輛類型、製程類型、樹脂類型和應用分類-2026-2032年全球市場預測自行車碳纖維車架市場:依自行車類型、車架類型和銷售管道分類-2026-2032年全球市場預測

汽車碳纖維市場:依車輛種類、原料、纖維等級及應用分類-2026-2032年全球市場預測2026年全球智慧尾門市場報告汽車用碳纖維熱塑性塑膠市場:依纖維類型、車輛類型、製程類型、樹脂類型和應用分類-2026-2032年全球市場預測自行車碳纖維車架市場:依自行車類型、車架類型和銷售管道分類-2026-2032年全球市場預測 碳纖維傳動軸市場規模、佔有率和成長分析:按類型、材質、應用、製造流程、終端用戶產業和地區分類-2026-2033年產業預測

碳纖維傳動軸市場規模、佔有率和成長分析:按類型、材質、應用、製造流程、終端用戶產業和地區分類-2026-2033年產業預測 碳纖維引擎蓋市場規模、佔有率和成長分析:按產品類型、材質類型、車輛類型、製造流程、分銷管道和地區分類-2026-2033年產業預測

碳纖維引擎蓋市場規模、佔有率和成長分析:按產品類型、材質類型、車輛類型、製造流程、分銷管道和地區分類-2026-2033年產業預測 碳纖維擾流板市場規模、佔有率和成長分析:按產品類型、車輛類型、最終用戶、銷售管道、價格範圍和地區分類-2026-2033年產業預測

碳纖維擾流板市場規模、佔有率和成長分析:按產品類型、車輛類型、最終用戶、銷售管道、價格範圍和地區分類-2026-2033年產業預測 2026-2034年全球汽車用碳纖維熱塑性塑膠市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球汽車用碳纖維熱塑性塑膠市場規模、佔有率、趨勢及成長分析報告