|

市場調查報告書

商品編碼

2063664

AI程式碼產生和開發者支援工具:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年)AI Code Generation And Developer Assistant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

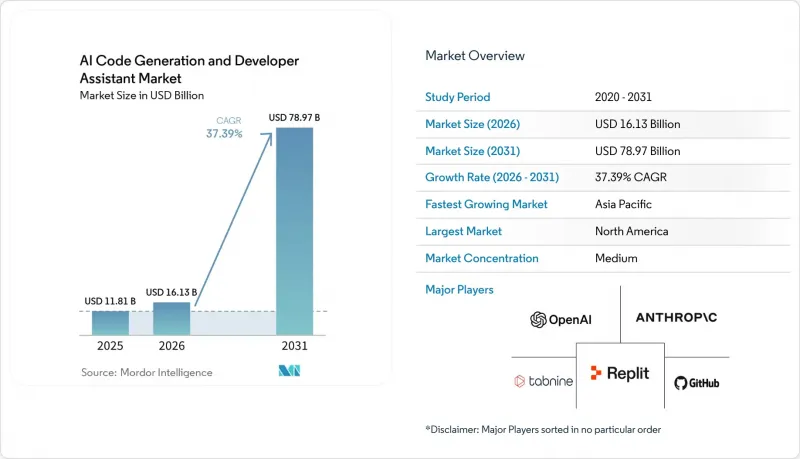

根據 Mordor Intelligence 預測,人工智慧程式碼產生市場規模將從 2025 年的 118 億美元成長到 2026 年的 161.3 億美元,然後在 2031 年達到 789.7 億美元,2026 年至 2031 年的複合年成長率為 37.39%。

本報告按部署模式(雲端、本地部署、混合部署)、功能(程式碼產生、自動補全等)、最終用戶產業(個人開發者、自由工作者等)、應用程式領域(軟體開發、DevOps 和 CI/CD、資料科學和分析等)以及地區進行細分。市場預測以美元計價。

全球人工智慧程式碼生成及開發者支援工具市場趨勢及洞察

企業採用人工智慧輔助開發工具的趨勢正在加速。

2025年和2026年,隨著越來越多的公司尋求縮短產品發布週期以應對勞動力短缺,企業採購規模大幅擴張。微軟宣布,截至2026年第二季度,其Microsoft 365 Copilot許可證數量已達1500萬,GitHub Copilot付費用戶470萬,顯示經營團隊對自動化編碼平台的支援力度已達到一定水準。 Replit報告稱,財富500強企業中有85%正在使用其工作空間,證明試驗計畫階段。將程式碼助理整合到日常工作流程中的公司,其程式碼完成速度平均提升了55%,但法律和合規性審查會延長採用週期。提供清晰的智慧財產權(IP)補償和使用情況分析功能的供應商越來越受歡迎,尤其是在監管嚴格的行業。因此,提供企業級管治功能的供應商的收入短期內集中度顯著提高。

大規模語言模型的快速發展使得上下文感知程式碼產生成為可能。

2026年初發布的GPT-5.4提高了推理準確率,擴大了上下文窗口,並允許助手在一次提示中覆蓋整個程式碼庫。 GitHub在數小時內就整合了此次升級,這立即提升了多文件編輯和自動化測試產生的解決方案成功率。 Anthropic的Claude 3.5 Sonnet已整合到Replit的Agent中,並在發布後的幾個月內使該平台的收入成長了十倍。領先的模型供應商正從純粹的推理服務轉向差異化的推理API,打造一個高階層級,而這對於對成本敏感的企業來說往往遙不可及。小規模的開放原始碼模式則落後於此,市場呈現兩極化的局面:一邊是精英付費服務,另一邊是成本績效的替代方案。

人工智慧生成程式碼的知識產權和授權方面存在不確定性

一起指控 Copilot 的訓練程序侵犯版權庫的集體訴訟尚未解決,這在知識產權管理嚴格的行業經營團隊中引發了猶豫。 Tabnine 透過僅採用寬鬆授權協議並提供廣泛的賠償條款來應對此問題。由於法律上的澄清不太可能在 2027 年之前出現,許多公司要求對所有人工智慧生成的內容進行人工審核,並提供將程式碼片段與提示資訊關聯起來的審計追蹤。擁有透明資料集來源和合約賠償條款的供應商正在吸引金融和醫療保健行業的客戶,而採用不透明模型的供應商則面臨更長的銷售週期。

細分市場分析

預計到2025年,雲端領域將佔據市場規模的63.71%,反映出尖端模型能夠輕鬆整合到現有流程中。隨著企業越來越重視先進技術的無縫部署,這種整合是擴大人工智慧程式碼產生市場佔有率的關鍵因素。混合配置正以37.99%的複合年成長率成長,主要得益於企業尋求在資料主權和持續模型升級優勢之間取得平衡。隨著各組織努力最佳化其營運框架,這一趨勢在人工智慧程式碼生成市場規模的組成中佔據越來越重要的地位。

雲端優先供應商憑藉著每週更新模型、基於代幣的收費和即時上線等優勢,正日益受到青睞,成為新計畫的首選。然而,金融服務、國防和醫療保健等行業正擴大選擇Tabnine和Rosetic等解決方案,這些方案提供單一租戶或空氣間隙環境的部署。這些方案尤其具有吸引力,因為它們能夠滿足GDPR和HIPAA等嚴格法規的要求。多供應商策略也正在興起,即低風險的內部工具部署在雲端,而關鍵工作負載的生產程式碼則在本地編譯。能夠跨雲端和本地環境整合遙測、策略和收費的供應商,透過有效滿足多樣化的客戶需求,在更廣泛的AI程式碼產生市場中佔據有利地位,從而贏得市場佔有率。

預計到2025年,程式碼產生和自動補全功能將佔總支出的46.33%,成為人工智慧程式碼產生市場功能細分領域的基礎要素。這些功能對開發人員而言仍然至關重要,能夠顯著提高效率並減少手動編碼工作。同時,儘管基於代理商的編配市佔率較小,但其複合年成長率卻高達38.59%。這一成長趨勢凸顯了重新定義團隊如何從人工智慧驅動的編碼工具中獲取價值的潛力。調試、測試生成和文件編寫等傳統功能正擴大整合到更廣泛的平台中,而不是作為獨立解決方案提供。這種轉變正在削弱單一功能工具的競爭優勢,迫使供應商不斷創新並擴展其服務範圍,以在不斷變化的市場格局中保持競爭力。

Reflection AI 和 GitHub 的程式碼代理程式等先進工具正在透過自動化整個開發生命週期(從規劃和編碼到測試和拉取請求)中的流程來變革工作流程。這些功能使企業能夠實現以前認為不可能的大幅裁員。如今,企業優先考慮那些能夠結合編配和強大管治功能的平台,以確保合規性和營運效率。這一趨勢迫使單一功能供應商要麼拓展自身功能,要麼面臨商品化的風險。因此,AI 程式碼生成產業正在向整合基本程式碼補全和高階自主工作流程的綜合套件轉型,以滿足對端到端解決方案日益成長的需求。

區域分析

北美預計將成為人工智慧程式碼產生市場的商業性中心,預計到2025年將佔全球需求的39.37%。該地區擁有多項結構性優勢,包括高密度的創業投資投資、許多超大規模資料中心業者中心以及重視創新的企業文化。在美國,聯邦政府計畫正積極推動人工智慧在國防和私營部門的應用,從而顯著促進了該領域的成長。相較之下,加拿大和墨西哥的人工智慧程式碼產生技術應用進展較為緩慢,主要原因是與美國相比,這兩個國家的人才儲備較少,資源也較為有限。

亞太地區正崛起為成長最快的地區,年複合成長率高達37.94%。這項成長主要得益於印度約500萬開發者的龐大人才庫以及中國強大的國家主導人工智慧計畫。像DeepSeek這樣的公司正在部署符合中國資料本地化政策並確保遵守當地法規的成本效益型人工智慧模型。在印度,大型外包公司正在採用人工智慧驅動的編碼助手,透過大幅縮短交付給西方客戶的周期來提高營運效率。此外,在日本和韓國,由於面臨勞動力萎縮的挑戰,人工智慧編碼工具的應用正在不斷擴展,以此作為提高生產力和解決人手不足的一種手段。

在歐洲,人工智慧程式碼生成市場呈現出穩定成長與監管引領並存的平衡態勢。 《一般資料保護規則》(GDPR) 和即將訂定的歐盟人工智慧法案正在建立全球合規標準,為早期獲得認證的供應商創造了商機。這些法規不僅塑造市場格局,也促進了合規供應商的創新。在中東和非洲,市場仍在發展中,但隨著各國政府投資於數位技能學院等計畫以培養面向未來的人才,市場已顯現出成長跡象。這些區域趨勢共同構成了多元化的成長軌跡,實現了收入來源的多元化,並為人工智慧程式碼產生市場的供應商創造了更多機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加快企業採用人工智慧輔助開發工具。

- 大規模語言模型的快速發展使得上下文感知程式碼產生成為可能。

- 全球熟練軟體開發人員短缺問題日益嚴重。

- 將人工智慧助理整合到主流IDE和DevOps流程中

- 基於代理的工作流程的出現,實現了多階段編碼任務的自動化。

- 降低資料主權障礙的裝置端/邊緣程式碼產生模型

- 市場限制因素

- 人工智慧產生的程式碼相關的智慧財產權和授權問題不確定性

- 受監管行業的資料隱私和安全問題

- 與傳統建構系統和工具鏈整合的複雜性。

- 導致隱藏安全漏洞的模型錯覺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 雲

- 現場

- 混合

- 按功能

- 程式碼產生和自動完成

- 調試和錯誤檢測

- 程式碼審查和最佳化

- 測試生成

- 文件生成

- 基於代理的工作流程編配

- 按最終用戶行業分類

- 獨立開發者與自由工作者

- 新創企業和小型企業

- 大公司

- 教育機構

- 政府機構和非營利組織

- 透過使用

- 軟體開發

- DevOps 和 CI/CD

- 資料科學與分析

- 嵌入式和物聯網開發

- 低程式碼/無程式碼開發

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OpenAI LLC

- Anthropic PBC

- GitHub, Inc.

- GitLab Inc.

- Replit, Inc.

- JetBrains sro

- Tabnine Ltd.

- Sourcegraph, Inc.

- Codeium AI, Inc.

- CodiumAI Ltd.

- Cursor AI, Inc.

- DeepCode AG

- Hugging Face, Inc.

- Mistral AI SAS

- DeepSeek AI Technology Co., Ltd.

- Blackbox AI, Inc.

- CodeRabbit Inc.

- Cogram GmbH

- Sourcegraph, Inc.

- TabbyML, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI code generation market size is expected to grow from USD 11.8 billion in 2025 to USD 16.13 billion in 2026 and is forecast to reach USD 78.97 billion by 2031 at 37.39% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Function (Code Generation and Autocompletion, and More), End-User Industry (Individual Developers and Freelancers, and More), Application (Software Development, Devops and CI/CD, Data Science and Analytics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Code Generation And Developer Assistant Market Trends and Insights

Accelerating Enterprise Adoption Of AI-Assisted Development Tools

Enterprise procurement surged in 2025 and 2026 as businesses sought faster release cycles to counter limited headcount. Microsoft disclosed 15 million Microsoft 365 Copilot seats and 4.7 million GitHub Copilot paid subscribers by the second quarter of 2026, demonstrating board-level endorsement of automated coding platforms. Replit reported that 85% of Fortune 500 firms now use its workspace, proving that adoption has moved beyond pilot programs. Companies that embed assistants into day-to-day workflows record 55% faster code completion on average, but legal and compliance reviews are lengthening procurement cycles. Vendors responding with explicit IP indemnities and usage analytics are gaining favor, especially in regulated sectors. The net effect is a short-term surge in revenue concentration among players offering enterprise-grade governance features.

Rapid Advances In Large Language Models Enabling Context-Aware Code Generation

The release of GPT-5.4 in early 2026 lifted reasoning accuracy and expanded context windows, allowing assistants to span entire repositories in a single prompt. GitHub integrated the upgrade within hours, which immediately translated into higher solution rates for multi-file edits and automatic test generation. Anthropic's Claude 3.5 Sonnet, already woven into Replit's Agent, triggered a tenfold revenue jump for the platform in the months after launch. Frontier-model vendors are pivoting from pure inference services toward differentiated reasoning APIs, opening a premium tier that cost-sensitive firms may find prohibitive. Smaller open-source models lag, leaving the market divided between elite paid offerings and value-oriented alternatives.

Intellectual-Property And Licensing Uncertainty Around AI-Generated Code

The class-action suit alleging Copilot training infringed copyrighted repositories remains unresolved, producing board-level hesitancy in sectors with strict IP stewardship. Tabnine counters by training solely on permissive licenses and offering broad indemnity clauses. Legal clarity is unlikely before 2027, so many companies insist on human review of every AI contribution and audit trails linking code snippets to prompts. Vendors with transparent dataset provenance and contractual indemnity are capturing finance and healthcare accounts, while opaque models face elongated sales cycles.

Other drivers and restraints analyzed in the detailed report include:

- Growing Shortage Of Skilled Software Developers Worldwide

- Integration Of AI Assistants Into Popular IDEs And DevOps Pipelines

- Data-Privacy And Security Concerns In Regulated Industries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud slice accounted for 63.71% of the 2025 value, reflecting the ease with which frontier models can be integrated into existing pipelines. This integration has become a cornerstone of the AI code-generation market-share narrative, as businesses increasingly prioritize the seamless adoption of advanced technologies. Hybrid configurations are advancing at a 37.99% CAGR, driven by enterprises seeking to balance data sovereignty with the benefits of continuous model upgrades. This trend is adding a significant wedge to the AI code generation market size calculation, as organizations aim to optimize their operational frameworks.

Cloud-first vendors are gaining traction by offering weekly model refreshes, pay-per-token billing, and instantaneous onboarding, making them the preferred choice for green-field projects. However, industries such as financial services, defense, and healthcare are increasingly opting for solutions like Tabnine or Rosetic, which provide single-tenant or air-gapped installations. These options are particularly appealing due to their compliance with stringent regulations such as GDPR and HIPAA. Multi-vendor strategies are also emerging, where low-risk internal tools remain in the cloud, while production code for critical workloads is compiled on-premises. Providers capable of unifying telemetry, policy, and billing across both cloud and on-premises environments are well positioned to gain market share in the broader AI code generation market by effectively addressing their clients' diverse needs.

Code generation and autocompletion accounted for 46.33% of 2025 spending, establishing themselves as the foundational components of the AI code generation market size for functional segments. These features remain critical for developers, offering significant efficiency gains and reducing manual coding efforts. However, agentic orchestration, while representing a smaller share of the market, is growing at an impressive 38.59% CAGR. This growth trajectory highlights its potential to redefine how teams derive value from AI-driven coding tools. Traditional functionalities, such as debugging, test generation, and documentation, are increasingly integrated into broader platforms rather than being offered as stand-alone solutions. This shift is diminishing the competitive edge of single-function tools, pushing vendors to innovate and expand their offerings to remain relevant in the evolving market landscape.

Advanced tools like Reflection AI and GitHub's coding agents are transforming workflows by automating processes across the entire development lifecycle, from planning and coding to testing and pull-request stages. These capabilities enable enterprises to achieve significant headcount savings, which were previously considered unattainable. Organizations are now prioritizing platforms that combine orchestration capabilities with robust governance features, ensuring compliance and operational efficiency. This trend is creating pressure on single-function vendors to diversify their capabilities or risk being commoditized. As a result, the AI code generation industry is increasingly consolidating around comprehensive suites that integrate basic code-completion capabilities with advanced autonomous workflows, catering to the growing demand for end-to-end solutions.

Geography Analysis

North America accounted for 39.37% of projected demand in 2025, establishing itself as the commercial anchor of the AI code-generation market. The region benefits from several structural advantages, including a high density of venture capital investments, the presence of hyperscalers, and an enterprise culture that prioritizes innovation. In the United States, federal programs actively promote AI adoption across both defense and civilian agencies, driving significant growth. Meanwhile, Canada and Mexico are experiencing a more gradual uptake of AI code generation technologies, primarily due to smaller talent pools and limited resources compared to the United States.

Asia-Pacific is emerging as the fastest-growing region, with a remarkable compound annual growth rate (CAGR) of 37.94%. This growth is fueled by India's extensive developer workforce, which numbers approximately 5 million, and China's robust sovereign AI programs. Companies like DeepSeek are introducing cost-efficient AI models that align with Chinese data-localization policies, ensuring compliance with local regulations. In India, major outsourcing firms are integrating AI-powered coding assistants to significantly reduce turnaround times for their Western clients, enhancing operational efficiency. Additionally, Japan and South Korea, both facing challenges related to shrinking workforces, are increasingly adopting AI coding tools as a means to boost productivity and address labor shortages.

Europe demonstrates a balance between moderate growth and regulatory leadership in the AI code generation market. The General Data Protection Regulation (GDPR) and the forthcoming EU AI Act are setting global benchmarks for compliance, creating opportunities for vendors that achieve early certification. These regulations not only shape the market but also encourage innovation among compliant vendors. In the Middle East and Africa, the market is still nascent but is showing signs of growth as governments invest in initiatives such as digital skills academies to build a future-ready workforce. Collectively, these regional dynamics contribute to a multi-polar growth trajectory, diversifying revenue streams and creating opportunities for vendors operating in the AI code generation market.

- OpenAI L.L.C.

- Anthropic P.B.C.

- GitHub, Inc.

- GitLab Inc.

- Replit, Inc.

- JetBrains s.r.o.

- Tabnine Ltd.

- Sourcegraph, Inc.

- Codeium AI, Inc.

- CodiumAI Ltd.

- Cursor AI, Inc.

- DeepCode AG

- Hugging Face, Inc.

- Mistral AI SAS

- DeepSeek AI Technology Co., Ltd.

- Blackbox AI, Inc.

- CodeRabbit Inc.

- Cogram GmbH

- Sourcegraph, Inc.

- TabbyML, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Enterprise Adoption of AI-Assisted Development Tools

- 4.2.2 Rapid Advances in Large Language Models Enabling Context-Aware Code Generation

- 4.2.3 Growing Shortage of Skilled Software Developers Worldwide

- 4.2.4 Integration of AI Assistants into Popular IDEs and DevOps Pipelines

- 4.2.5 Emergence of Agentic Workflows Automating Multi-Step Coding Tasks

- 4.2.6 On-Device/Edge Code-Gen Models Reducing Data-Sovereignty Barriers

- 4.3 Market Restraints

- 4.3.1 Intellectual-Property and Licensing Uncertainty Around AI-Generated Code

- 4.3.2 Data-Privacy and Security Concerns in Regulated Industries

- 4.3.3 Integration Complexity with Legacy Build Systems and Toolchains

- 4.3.4 Model Hallucination Leading to Hidden Security Vulnerabilities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Function

- 5.2.1 Code Generation and Autocompletion

- 5.2.2 Debugging and Error Detection

- 5.2.3 Code Review and Optimization

- 5.2.4 Test Generation

- 5.2.5 Documentation Generation

- 5.2.6 Agentic Workflow Orchestration

- 5.3 By End-User Industry

- 5.3.1 Individual Developers and Freelancers

- 5.3.2 Start-ups and SMEs

- 5.3.3 Large Enterprises

- 5.3.4 Educational Institutions

- 5.3.5 Government and Non-Profit Organizations

- 5.4 By Application

- 5.4.1 Software Development

- 5.4.2 DevOps and CI/CD

- 5.4.3 Data Science and Analytics

- 5.4.4 Embedded and IoT Development

- 5.4.5 Low-Code / No-Code Development

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI L.L.C.

- 6.4.2 Anthropic P.B.C.

- 6.4.3 GitHub, Inc.

- 6.4.4 GitLab Inc.

- 6.4.5 Replit, Inc.

- 6.4.6 JetBrains s.r.o.

- 6.4.7 Tabnine Ltd.

- 6.4.8 Sourcegraph, Inc.

- 6.4.9 Codeium AI, Inc.

- 6.4.10 CodiumAI Ltd.

- 6.4.11 Cursor AI, Inc.

- 6.4.12 DeepCode AG

- 6.4.13 Hugging Face, Inc.

- 6.4.14 Mistral AI SAS

- 6.4.15 DeepSeek AI Technology Co., Ltd.

- 6.4.16 Blackbox AI, Inc.

- 6.4.17 CodeRabbit Inc.

- 6.4.18 Cogram GmbH

- 6.4.19 Sourcegraph, Inc.

- 6.4.20 TabbyML, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年貝葉斯最佳化工具全球市場報告

2026年貝葉斯最佳化工具全球市場報告 AI編碼助理市場:按產品、功能、部署、模型類型、程式語言、價格範圍、組織規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035)

AI編碼助理市場:按產品、功能、部署、模型類型、程式語言、價格範圍、組織規模和最終用戶產業分類-市場規模、產業動態、機會分析和預測(2026-2035) 綠色 DevOps 和碳意識 CI/CD 軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)AI代碼工具:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

綠色 DevOps 和碳意識 CI/CD 軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)AI代碼工具:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人工智慧驅動的軟體開發和編碼自動化市場預測至2034年:按交付、營運、部署、技術、應用、最終用戶和地區分類的全球分析人工智慧程式碼開發工具市場預測至2034年:按交付方式、營運、部署方式、技術、應用、最終用戶和地區分類的全球分析

人工智慧驅動的軟體開發和編碼自動化市場預測至2034年:按交付、營運、部署、技術、應用、最終用戶和地區分類的全球分析人工智慧程式碼開發工具市場預測至2034年:按交付方式、營運、部署方式、技術、應用、最終用戶和地區分類的全球分析 AI代碼助理市場規模、佔有率和趨勢分析報告:按組件、部署模式、應用、最終用戶、地區和細分市場預測(2026-2033年)人工智慧程式碼產生工具市場預測至2034年-全球分析(按組件、程式語言、組織規模、技術、應用、最終用戶和地區分類)

AI代碼助理市場規模、佔有率和趨勢分析報告:按組件、部署模式、應用、最終用戶、地區和細分市場預測(2026-2033年)人工智慧程式碼產生工具市場預測至2034年-全球分析(按組件、程式語言、組織規模、技術、應用、最終用戶和地區分類) 2026-2030年全球人工智慧模型最佳化工具市場人工智慧模型最佳化市場預測至2034年-全球分析(按組件、模型類型、方法論、部署模式、企業規模、最終用戶和地區分類)

2026-2030年全球人工智慧模型最佳化工具市場人工智慧模型最佳化市場預測至2034年-全球分析(按組件、模型類型、方法論、部署模式、企業規模、最終用戶和地區分類)