|

市場調查報告書

商品編碼

2063611

實驗室溫度控制設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Laboratory Temperature Control Units - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

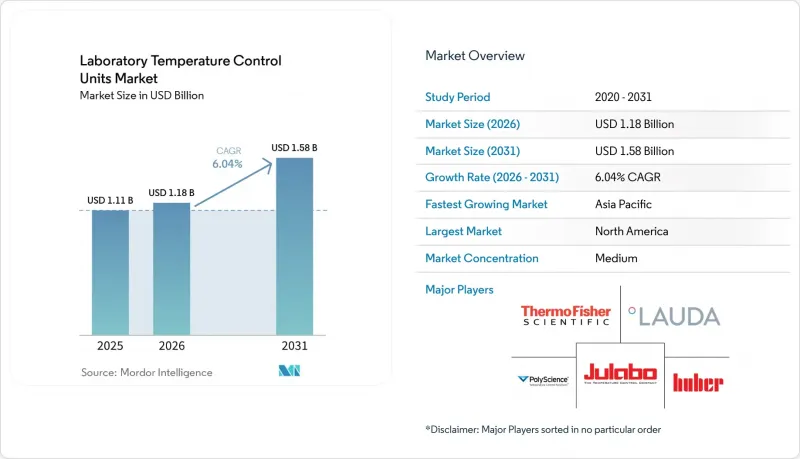

預計實驗室溫度控制設備的市場規模將從 2025 年的 11.1 億美元和 2026 年的 11.8 億美元成長到 2031 年的 15.8 億美元,2026 年至 2031 年的複合年成長率為 6.04%。

本報告按產品類型(例如循環式冷卻器)、冷卻技術(例如風冷)、溫度範圍(例如低於-40 度C)、容量(小於0.5 kW,其他)、最終用戶(製藥/生物技術,其他)、應用(分析儀器,其他)、外形規格、配銷通路和地區進行細分。市場預測以美元計價。

全球實驗室溫度控制設備。

製藥和生技領域研發投入的活性化,推動了對精確溫度控制的需求。

研發管線壓力和專利到期問題迫使生物製藥公司在2026年維持或擴大實驗室資本投入,從而導致精密冷卻和加熱系統的部署量增加,這些系統對於將高價值檢測維持在嚴格的容差範圍內至關重要。受訪的研發負責人強調,在2025年透過實驗室現代化改造來提高處理能力並降低誤差率是關鍵,而這些優先事項如今正轉化為採購規範,要求更嚴格的設定點控制和檢驗的資料登錄,以保護受監管實驗室的數據完整性。隨著資金流入生物製藥、細胞療法和下一代治療方法,冷卻需求正轉向動態溫度控制,以適應比傳統工作流程更窄的反應速率和穩定性窗口,這導致實驗室溫度控制設備市場對高級產品的需求增加。 2025年和2026年在中國達成的經營團隊正將交易量轉移到正在擴建新實驗室和分析核心設施的地區,從而擴大了亞太地區溫度控制的潛在部署基礎。

印度的「生物沙克蒂」(Bio SHAKTI)計劃,預算撥款約10.8億美元,為期五年,正隨著國家藥物教育與研究學院、臨床試驗設施和生物類似藥生產能力的升級改造於2026年全面啟動而逐步實施。這將推動合成、驗證和配製流程中對循環冷卻器、冷凍循環器和水浴的需求成長。這些措施將提高每個實驗室的設備規格密度,並延長實驗室溫度控制設備(TCU)市場的更換週期。

由於亞太地區實驗室的建造和設備的引進,部署的TCU數量正在增加。

預計2026年中國藥品產量將成長6.6%,高於2025年的3.6%。這將促使資本預算轉向生物製藥相關研發管線,進而增加從研發到品質控制各階段對溫度控制的需求。台灣工業技術研究院(工程院)於2026年2月開始興建12吋半導體中試生產線,計畫於2027年底完工。這將擴大對微影術、蝕刻和測量設備等精密冷卻設備的需求,這些設備需要低於0.1 度C的品管。 2026年,印度多個擴建項目正在進行中,包括Alkem公司位於烏賈因的製劑工廠和Lupin公司位於達巴薩的肽類產能提升項目,這些項目均採用集中式或模組化溫度控制架構來管理已驗證的生產線內多個反應器的熱線。

亞太地區分析儀器的日益普及推動了對具備整合數位控制和網路連接功能的緊湊型冷卻器的現場需求,從而擴大了實驗室溫度控制設備市場的機會。上海、蘇州、海德拉巴和新竹叢集潔淨室和設備的密度不斷增加,提高了每個站點溫度控制單元(TCU)的採用率。製藥和半導體專案的並存使得亞太地區的整合商能夠將產品規格與全球驗證標準接軌,縮短合規單元的前置作業時間,並加速實驗室溫度控制設備的普及。

因新的氟化氣體/全球暖化潛勢 (GWP) 法規而產生的合規成本和重新設計費用

向天然冷媒的過渡對易燃性和高壓設計提出了更高的要求,這增加了中小容量設備的成本和複雜性,從而擠壓了小型供應商的利潤空間。使用A3冷媒受到限制的實驗室設施必須設計通風系統和安全聯鎖裝置,或選擇其他替代方案,但這仍然會增加安裝面積和電力消耗,從而延緩了一些過渡過程。 2025年9月,美國環保署(EPA)指出,由於安全標準在時間和性能方面存在差距,某些應用需要一定的合規寬限期。這凸顯了精密設備領域仍需解決的設計複雜性問題。歐洲的指導意見和2025-2026年的行業發展趨勢表明,收緊配額和對高全球暖化潛值(GWP)冷媒的新禁令將增加維護成本,並使一些現有設備無法使用。這可能導致更早決定報廢設備,或由於買家考慮各種選擇而推遲短期採購。

在每個地區對多個 SKU 進行認證並將其整合到最嚴格的平台標準中,可能會延長產品上市時間並給供應商的生產流程帶來壓力。雖然這些因素可能會在 2026 年部分抑制訂單,但不可否認的是,在中期內,整個實驗室溫度控制設備市場對符合標準的替代方案仍有需求。

細分市場分析

到2025年,循環冷卻器將佔實驗室溫度控制設備市場22.45%的佔有率。這主要得益於品管(QC)實驗室、合約測試以及需要封閉回路型穩定性和檢驗記錄的儀器系統連續運作的需求。這些設備透過外部熱交換器循環水、乙二醇或蒸氣,具有寬廣的容量範圍和高穩定性,適用於受控工作流程和標準化設施。冷卻和加熱循環器結合了加熱元件和蒸汽壓縮冷卻技術,支援在單次運行中跨越環境溫度和低於環境溫度的設定方案。加熱循環器用於高於環境溫度的應用,在蒸發、蒸餾和夾套容器等不需要低於環境溫度控制的工作流程中仍有需求。水浴和搖床水浴因其操作簡單、成本低廉,常用於細胞培養、反應動力學和溶解度測試。

高動態範圍溫度控制系統市場預計到2031年將以8.85%的複合年成長率成長,因為快速升溫和精確的過衝控制對於反應量熱法、中試規模製程和半導體開發中的安全性和產量提升至關重要。實驗室溫度控制設備市場持續受益於控制器技術的進步,這些控制器能夠與實驗室資訊系統和建築管理儀錶板整合。供應商正在整合多點感測器、冗餘電路和警報邏輯,以確保GMP環境下的運作。產品藍圖重點介紹了天然冷媒和變頻壓縮機的應用,以平衡能耗與穩態穩定性,並通過認證測試。

到2025年,風冷系統仍將保持領先地位,佔據實驗室溫度控制設備市場46.22%的佔有率,這主要得益於其易於安裝和運作,無需建築管道或冷凍水循環系統。水冷式冷卻器可以降低房間的熱負荷,通常能實現更高的性能係數(COP),但需要建築整合和水處理系統,而某些設施可能不具備這些條件。熱電或珀爾帖平台預計將以8.03%的複合年成長率成長,因為它們在微流體、晶片器官和活細胞成像等領域具有無振動、無冷媒運行和精確設定點控制的優勢。低溫和二氧化碳輔助系統滿足了冷凍乾燥和冷凍保存中低於-80 度C的超低溫需求,它們專注於特定製程,而非通用的實驗室冷卻。由於維護複雜和空間佔用較大,混合系統在實驗室中仍然很少見。從採用曲線可以看出,熱電系統在低負載範圍內正在擴張,而空冷和水冷平台在高負載範圍內正在佔據主導地位,這表明兩者之間存在互補關係。

風扇和壓縮機控制技術的進步提高了季節性能效,同時在各種環境條件下保持了穩定性。配備乙太網路和RS232介面的控制器選項以及資料登錄功能,支援稽核追蹤和警報路由,這在高度監管的環境中至關重要。在半導體和成像實驗室中,低噪音性能(以減少振動和聲學干擾)是首要考慮因素,這推動了對配備自適應風扇的高品質風冷機組的需求。在採用中央迴路的系統中,從能源效率和溫度控管角度來看,水冷機組仍然是可行的選擇。隨著供應商逐步過渡到天然冷媒,性能要求將更加嚴格,尤其是在穩定性指標方面。這些變化意味著,容量、雜訊、面積和整合性等方面的應用適用性將繼續是實驗室溫度控制設備市場的關鍵因素。

預計到2025年,0至+100 度C的溫度範圍將佔需求的39.80%。這是因為大多數分析儀器、細胞培養和夾套反應器都在此溫度範圍內運作,以達到中等穩定性。隨著超低溫冰箱、冷凍乾燥和環境測試在生物製程和材料實驗室的應用日益廣泛,預計到2031年,低於-40 度C的系統將以9.39%的複合年成長率成長。多級冷凍和二氧化碳級聯策略正在取代傳統的冷媒混合物,以滿足歐盟過渡法規的要求,同時維持低溫性能目標。在製藥和環境測試領域,接近環境溫度的控制仍然是檢測器冷卻、柱溫箱和溶離度試驗箱的主要應用場景。從低於環境溫度到高溫的寬廣溫度範圍內,冷卻或加熱循環器仍然是首選。為了符合ICH穩定性測試和驗證方案的要求,品管(QC)環境中對記錄和控制功能的需求正在不斷成長,以支援審計合規性。

在溫度高於 100 度C 的範圍內,油冷循環器能夠滿足需要在高溫設定點下保持穩定的材料和聚合物製程需求。在此領域,能夠減少溫度過衝並改善溫度追蹤,從而保障安全性和資料品質的控制演算法至關重要。隨著越來越多的方案將室溫加熱和室溫加熱相結合,買家傾向於選擇覆蓋範圍廣、穩定性高的平台。隨著供應商完成重新設計並納入安全考量,天然冷媒平台正在這些類別中不斷擴展。對於需要在設備更換後進行工作流程重新認證的實驗室而言,驗證套件和校準服務會影響其購買決策。這些趨勢使得實驗室控制設備市場保持強勁的更換速度。

區域分析

預計到2025年,北美將佔據實驗室溫度控制設備市場34.82%的佔有率。這主要得益於受監管的製藥企業、頂尖研究型大學的儀器設備需求,以及檢驗的工作流程對運作保證和服務合約需求的增加。針對冷卻器的能源和性能法規正在推動對配備變速組件和板式熱交換器的高效設備的支出,這與加拿大和美國的採購文件相符。

預計到2031年,亞太地區的複合年成長率將達到10.48%,反映出製藥和半導體產業產能的擴張,從而增加了精密冷卻系統的部署數量。 2026年中國藥品產量的成長以及向高價值生物製藥的廣泛轉型,將增強從研發到品管的各個環節的需求。在台灣,工研院試驗線將於2026年投入使用,Rigaku Corporation測量中心將於2025年投入使用,這將擴大測量和製程研發中對嚴格溫度控制的需求。在印度,包括Alchem和Lupin等專案在內的製造業擴張,將推動集中式和模組化TCU架構在經過驗證的套件中的部署,從而帶動現場和工廠整合應用的需求。

在歐洲,儘管現有冷媒應用基礎已較為成熟,但嚴格的冷媒法規正迫使企業盡可能快速地過渡到R-290、R-744和固體熱力控制技術。歐盟的氟化氣體法規包括在2027年和2032年實施基於容量的短期禁令,這將加速系統改造和採購向合規系統的轉變。在此背景下,擁有天然冷媒產品系列和完善的檢驗支援的供應商將具有顯著優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 製藥和生物技術領域研發投入的活性化,推動了精密溫度控制的需求成長。

- 由於亞太地區實驗室擴建和設備安裝,TCU 的部署數量正在增加。

- 法規向低全球暖化潛勢冷媒的轉變正在加速產品的重新設計和維修。

- 實驗室永續性:能源和水資源效率標準正在推動從單一途徑冷卻系統轉向循環冷卻系統的轉變。

- 隨著處理能力和運作的增加,分析儀器(LC/GC-MS、EM)對冷卻的需求也在成長。

- 熱電/珀爾帖控制在微流體、晶片器官成像和活細胞成像的應用。

- 市場限制因素

- 與新的氟碳氣體法規和全球暖化潛勢限制相關的合規成本和重新設計

- 實驗室空間有限情況下的總擁有成本 (TCO) 限制(電力、熱負荷、噪音)

- 新實驗室向集中式設備和封閉回路型系統的轉變,在一定程度上減少了對桌上型冷卻器的需求。

- 低全球暖化潛勢冷媒的技術人員認證和維護的複雜性

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品

- 循環冷卻器

- 冷卻和加熱循環器

- 加熱循環罐

- 先進的動態溫度控制系統

- 實驗室溫度控制器

- 水浴和搖水浴

- 其他(微型溫度控制設備、反應器溫度控制設備等)

- 按類型分類的冷卻技術

- 空冷式

- 水冷

- 熱電(珀爾帖)

- 低溫/液態氮或二氧化碳輔助

- 其他(混合式蒸氣壓縮型、吸收式冷凍系統)

- 按溫度範圍

- 低於攝氏零下40度C

- -40~-20°C

- -20~0°C

- 0~+100°C

- 其他(+100 至 +300 度C,高於 +300 度C)

- 按產能

- 小於0.5千瓦

- 0.5~2 kW

- 2~5 kW

- 超過5千瓦

- 最終用戶

- 製藥和生物技術

- 學術研究機構

- 臨床和診斷

- 其他(CRO、CDMO)

- 透過使用

- 用於分析儀器(液相層析/氣相層析-質譜聯用、核磁共振、電鏡)

- 實驗反應器和製程開發

- 樣品製備和熱測試

- 生物製程與低溫運輸實驗室

- 微流體和活細胞成像

- 其他(試劑製備和儲存條件管理、疫苗研發和製劑測試)

- 按外形規格

- 工作檯面

- 固定式 固定式

- 機架安裝型

- 整合/OEM模組

- 其他類型(台下式、可攜式)

- 透過分銷管道

- 直銷

- 銷售代理

- 電子商務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Applied Thermal Control

- ATS Automation Tooling Systems Inc.

- Avantor, Inc.

- BUCHI

- Cole-Parmer Instrument Company, LLC

- Eaton

- EURODIFROID

- Filtrine

- FRYKA Refrigeration Technology

- Grant Instruments

- Haskris

- Heidolph Instruments

- IKA

- JULABO GmbH

- LabTech Srl

- LAUDA

- Peter Huber Kaltemaschinenbau SE

- PolyScience

- Thermo Fisher Scientific Inc.

- Yamato Scientific co., ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the laboratory temperature control units market size is projected to expand from USD 1.11 billion in 2025 and USD 1.18 billion in 2026 to USD 1.58 billion by 2031, registering a CAGR of 6.04% between 2026 to 2031.

This report is Segmented by Product (Recirculating Chillers, and More), Cooling Technology (Air-Cooled, and More), Temperature Range (Below -40 °C, and More), Capacity (<0. 5 KW, and More), End User (Pharmaceuticals & Biotechnology, and More), Application (Analytical Instruments Support, and More), Form Factor, Distribution Channel, and Geography. Market Forecasts in Value USD.

Global Laboratory Temperature Control Units Market Trends and Insights

Pharma And Biotech R&D Intensification Boosts Precision Thermal Control Demand

Pipeline pressure and patent cliffs are forcing biopharma to maintain or raise laboratory capital spending in 2026, which increases the installed base of precision cooling and heating systems needed to keep high-value assays within tight tolerances. Surveyed R&D leaders highlighted throughput and error-rate gains from lab modernization in 2025, and those priorities now cascade into procurement specifications that call for tighter setpoint control and validated data logging that protect data integrity in regulated labs. As capital flows to biologics, cell therapy, and next-generation modalities, cooling requirements shift toward dynamic temperature control for reaction kinetics and stability windows that are narrower than legacy workflows, which expands premium adoption in the Laboratory Temperature Control Units market. Executive partnerships in China during 2025 and 2026 redirected deal value to sites that are scaling new labs and analytical cores, which expands the addressable installed base for thermal control in APAC hubs.

India's Bio SHAKTI allocation of approximately USD 1.08 billion over five years is being executed in 2026 as upgrades to National Institutes of Pharmaceutical Education and Research, clinical trial sites, and biosimilar capacity come online, which raises demand for recirculating chillers, refrigerated circulators, and water baths across synthesis, validation, and staging workflows. This set of actions lifts specification density per lab and expands refresh cycles in the laboratory temperature control units market.

APAC Lab Build-Out And Instrument Installs Expand Installed Base For TCUs

China's pharmaceutical production rose 6.6% in 2026 compared to 3.6% in 2025, which aligns capital budgets with more biopharma-oriented pipelines that intensify temperature control needs at each step from R&D to QC. Taiwan's Industrial Technology Research Institute broke ground on a 12-inch semiconductor pilot line in February 2026 with completion targeted by end-2027, which expands precision cooling demand around lithography, etch, and metrology tools that require sub-0.1 °C stability. Multiple Indian expansions in 2026, including Alkem's formulations site at Ujjain and Lupin's peptide capacity at Dabhasa, are embedding centralized or modular temperature control architectures to manage multi-reactor thermal loads in validated suites.

A growing base of analytical instruments in APAC is also raising point-of-use demand for compact chillers that integrate over digital controls and can be networked for alarms, which broadens entry points for the laboratory temperature control units market. Cleanroom and instrument density are increasing across Shanghai, Suzhou, Hyderabad, and Hsinchu clusters, which supports higher per-site TCU penetration. That mix of pharma and semiconductor projects narrows lead times for compliant units as APAC integrators synchronize specifications to global validation standards, which raises the installed base growth rate in the laboratory temperature control units market.

Compliance Costs And Redesigns Driven By New F Gas/GWP Limits

Transitioning to natural refrigerants imposes flammability or high-pressure design requirements that add cost and complexity to small and mid-capacity units, which erodes margins for vendors without scale. Laboratory campuses with restrictions on A3 refrigerants must either engineer ventilation and safety interlocks or opt for alternatives that still complicate footprint and power, which slows some conversions. The EPA noted in September 2025 that certain applications required compliance extensions due to safety-standard timing and performance gaps, which confirms the engineering complexity still being resolved for precision categories. European guidance and industry notes from 2025 through 2026 signaled that tightening quotas and new bans on high-GWP refrigerants would raise servicing costs and strand some installed equipment, which accelerates end-of-life decisions but can delay near-term purchases as buyers evaluate options.

The need to qualify multiple SKUs by region or converge on the strictest platform reduces speed to market, which can compress vendor pipelines. These factors temper some 2026 ordering but do not change the medium-term need for compliant replacements across the laboratory temperature control units market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift To Low GWP Refrigerants Accelerates Product Refresh And Retrofits

- Lab Sustainability, Energy And Water Efficiency Standards Replace Single Pass Cooling With Recirculating Systems

- Total Cost Of Ownership Constraints In Constrained Lab Spaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recirculating chillers commanded 22.45% of the laboratory temperature control units market size in 2025, driven by continuous-duty use in QC labs, contract testing, and instrument clusters that require closed-loop stability and validated logging. These units circulate water-glycol or silicone oil to external heat exchangers and cover broad capacity ranges with tight stability, which aligns with regulated workflows and standardized facilities. Refrigerated or heating circulators combine heater elements with vapor-compression cooling, which supports protocols that pass through ambient and sub-ambient setpoints during one run. Heating circulators serve applications above ambient and remain attractive in evaporation, distillation, and jacketed vessel workflows that do not require sub-ambient control. Water baths and shaking water baths are common in cell culture, kinetics, and dissolution testing based on familiarity and ease of use at lower price points.

Highly dynamic temperature control systems are projected to grow at an 8.85% CAGR through 2031 as reaction calorimetry, pilot-scale processing, and semiconductor development lean on fast ramps and precise overshoot control for safety and yield. The laboratory temperature control units market continues to benefit from controller improvements that integrate with laboratory information systems and building management dashboards. Vendors are embedding multi-point sensors, redundant circuits, and alarm logic that support uptime guarantees in GMP environments. Product roadmaps highlight natural-refrigerant adoption and inverter-driven compressors that balance energy use with steady-state stability to pass qualification tests.

Air-cooled systems led with 46.22% of laboratory temperature control units market share in 2025, supported by simple installation and the ability to operate without building plumbing or chilled-water loops. Water-cooled chillers reduce in-room heat load and often deliver higher coefficients of performance, but they require building integration and treatment regimes that some sites lack. Thermoelectric or Peltier platforms are set to grow at an 8.03% CAGR as microfluidics, organ-on-chip, and live-cell imaging benefit from vibration-free and refrigerant-free operation with precise setpoint control. Cryogenic and CO2-assisted systems serve ultra-low-temperature needs below -80 °C in freeze-drying and cryopreservation, which keeps them focused on specific protocols rather than general lab cooling. Hybrid approaches are still rare in labs due to maintenance complexity and space requirements. The adoption curve shows complementary roles as thermoelectric expands at the low end and air- or water-cooled platforms handle higher loads.

Advances in fan and compressor control improve seasonal efficiency while maintaining stability under varied ambient conditions. Controller options with Ethernet or RS232 and data logging support audit trails and alarm routing, which matters in regulated environments. Semiconductor and imaging labs prize low-noise profiles that reduce vibration and acoustic artifacts, which reinforces demand for premium air-cooled units with adaptive fans. Where central plant loops exist, water-cooled units remain compelling due to energy efficiency and heat management. As vendors complete natural-refrigerant conversions, performance characteristics will continue to tighten around stability metrics. This set of changes keeps the laboratory temperature control units market focused on application fit across capacity, noise, footprint, and integration.

The 0 to +100 °C band accounted for 39.80% of 2025 demand as most analytical instruments, cell culture, and jacketed reactors operate in that span with moderate stability goals. Systems below -40 °C are forecast to expand at a 9.39% CAGR through 2031 as ultra-low-temperature freezers, freeze-drying, and environmental testing scale in bioprocessing and materials labs. Multi-stage refrigeration and CO2 cascade strategies are displacing legacy blends to meet EU transition rules while sustaining low-temperature performance targets. Near-ambient control remains the dominant use case for detector cooling, column ovens, and dissolution baths across pharmaceutical and environmental testing. Wider spans that move from sub-ambient to elevated temperatures continue to back refrigerated or heating circulators. Compliance with ICH stability and validation protocols drives demand for logging and control features that support audit readiness in QC environments.

Above +100 °C, oil-based circulators enable materials and polymer processes that require stability at elevated setpoints. This area benefits from control algorithms that reduce overshoot and improve ramp tracking for safety and data quality. As more protocols combine sub-ambient segments with heating above ambient, buyers often consolidate on platforms that span a wider range with strong stability. Natural-refrigerant platforms are expanding into more of these categories as vendors complete redesigns and address safety considerations. Validation kits and calibration services influence purchase decisions in labs that must re-qualify workflows after equipment changes. These trends sustain a strong replacement and upgrade cadence in the laboratory temperature control units market.

Geography Analysis

North America captured 34.82% of the laboratory temperature control units market size in 2025, driven by regulated pharmaceutical operations, instrument clusters across leading research universities, and validated workflows that raise demand for uptime guarantees and service contracts. Energy and performance rules for chillers concentrate spend on efficient units with variable-speed components and plate heat exchangers, which align with procurement documents in Canada and the United States.

Asia-Pacific is projected to record a 10.48% CAGR through 2031, reflecting pharmaceutical and semiconductor capacity expansions that multiply the installed base for precision cooling. China's 2026 production gains in pharmaceuticals and a broader reorientation to higher-value biopharma reinforce demand from R&D to QC. Taiwan's ITRI pilot line in 2026 and Rigaku's metrology center in 2025 expand demand for tight temperature control in metrology and process R&D. India's manufacturing expansions in 2026, including Alkem and Lupin projects, incorporate centralized and modular TCU architectures in validated suites, which raises both point-of-use and plant-integrated demand.

Europe maintains a mature installed base but faces binding refrigerant rules that push rapid transitions to R-290, R-744, and solid-state thermal control where feasible. The EU F-Gas pathways set near-term bans in 2027 and 2032 by capacity, which accelerates redesigns and procurement shifts to compliant systems. That environment rewards suppliers with natural-refrigerant portfolios and established validation support.

- Applied Thermal Control

- ATS Automation Tooling Systems Inc.

- Avantor

- BUCHI

- Cole-Parmer

- Eaton

- EURODIFROID

- Filtrine

- FRYKA Refrigeration Technology

- Grant Instruments

- Haskris

- Heidolph Instruments

- IKA

- JULABO GmbH

- LabTech S.r.l.

- LAUDA

- Peter Huber Kaltemaschinenbau SE

- PolyScience

- Thermo Fisher Scientific

- Yamato Scientific co., ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharma and Biotech R&D Intensification Boosts Precision Thermal Control Demand

- 4.2.2 APAC Lab Build-Out And Instrument Installs Expand Installed Base For TCUs

- 4.2.3 Regulatory Shift To Low-GWP Refrigerants Accelerates Product Refresh And Retrofits

- 4.2.4 Lab Sustainability: Energy And Water Efficiency Standards Replace Single-Pass Cooling With Recirculating Systems

- 4.2.5 Rising Cooling Needs For Analytical Instruments (LC/GC-MS, EM) With Higher Throughput And Uptime

- 4.2.6 Thermoelectric/Peltier Control Adoption In Microfluidics, Organ-On-Chip, And Live-Cell Imaging

- 4.3 Market Restraints

- 4.3.1 Compliance Costs And Redesigns Driven By New F-Gas/GWP Limits

- 4.3.2 Total Cost Of Ownership Constraints (Power, Heat Load, Noise) In Constrained Lab Spaces

- 4.3.3 Migration To Central Plant/Closed Loops In New Labs Reduces Some Benchtop Chiller Demand

- 4.3.4 Technician Certification And Low-GWP Refrigerant Servicing Complexity

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Recirculating Chillers

- 5.1.2 Refrigerated/Heating Circulators

- 5.1.3 Heating Circulators

- 5.1.4 Highly Dynamic Temperature Control Systems

- 5.1.5 Laboratory Temperature Controllers

- 5.1.6 Water Baths & Shaking Water Baths

- 5.1.7 Others (Micro-temperature Control Units, Reactor Temperature Control Units, etc.)

- 5.2 By Cooling Technology

- 5.2.1 Air-cooled

- 5.2.2 Water-cooled

- 5.2.3 Thermoelectric (Peltier)

- 5.2.4 Cryogenic/LN2 or CO2-assisted

- 5.2.5 Others (Hybrid vapor-compression, Absorption Cooling Systems)

- 5.3 By Temperature Range

- 5.3.1 Below -40 °C

- 5.3.2 -40 to -20 °C

- 5.3.3 -20 to 0 °C

- 5.3.4 0 to +100 °C

- 5.3.5 Others (+ 100 to +300 °C, Above +300 °C)

- 5.4 By Capacity

- 5.4.1 < 0.5 kW

- 5.4.2 0.5 - 2 kW

- 5.4.3 2 - 5 kW

- 5.4.4 > 5 kW

- 5.5 By End User

- 5.5.1 Pharmaceuticals & Biotechnology

- 5.5.2 Academic & Research Institutes

- 5.5.3 Clinical & Diagnostics

- 5.5.4 Others (CROs, CDMOs)

- 5.6 By Application

- 5.6.1 Analytical Instruments Support (LC/GC-MS, NMR, EM)

- 5.6.2 Lab Reactors & Process Development

- 5.6.3 Sample Conditioning & Thermal Testing

- 5.6.4 Bioprocessing & Cold-Chain Labs

- 5.6.5 Microfluidics & Live-cell Imaging

- 5.6.6 Others (Reagent Preparation & Storage Conditioning, Vaccine Development & Formulation Testing)

- 5.7 By Form Factor

- 5.7.1 Benchtop

- 5.7.2 Floor-standing

- 5.7.3 Rack-mounted

- 5.7.4 Integrated/OEM Modules

- 5.7.5 Others (Under-counter Units, Portable)

- 5.8 By Distribution Channel

- 5.8.1 Direct Sales

- 5.8.2 Distributors

- 5.8.3 e-Commerce

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Mexico

- 5.9.2 Europe

- 5.9.2.1 Germany

- 5.9.2.2 United Kingdom

- 5.9.2.3 France

- 5.9.2.4 Italy

- 5.9.2.5 Spain

- 5.9.2.6 Rest of Europe

- 5.9.3 Asia-Pacific

- 5.9.3.1 China

- 5.9.3.2 India

- 5.9.3.3 Japan

- 5.9.3.4 Australia

- 5.9.3.5 South Korea

- 5.9.3.6 Rest of Asia-Pacific

- 5.9.4 Middle East and Africa

- 5.9.4.1 GCC

- 5.9.4.2 South Africa

- 5.9.4.3 Rest of Middle East and Africa

- 5.9.5 South America

- 5.9.5.1 Brazil

- 5.9.5.2 Argentina

- 5.9.5.3 Rest of South America

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Applied Thermal Control

- 6.3.2 ATS Automation Tooling Systems Inc.

- 6.3.3 Avantor, Inc.

- 6.3.4 BUCHI

- 6.3.5 Cole-Parmer Instrument Company, LLC

- 6.3.6 Eaton

- 6.3.7 EURODIFROID

- 6.3.8 Filtrine

- 6.3.9 FRYKA Refrigeration Technology

- 6.3.10 Grant Instruments

- 6.3.11 Haskris

- 6.3.12 Heidolph Instruments

- 6.3.13 IKA

- 6.3.14 JULABO GmbH

- 6.3.15 LabTech S.r.l.

- 6.3.16 LAUDA

- 6.3.17 Peter Huber Kaltemaschinenbau SE

- 6.3.18 PolyScience

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Yamato Scientific co., ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment