|

市場調查報告書

商品編碼

2063513

光敏增白劑:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Optical Brighteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

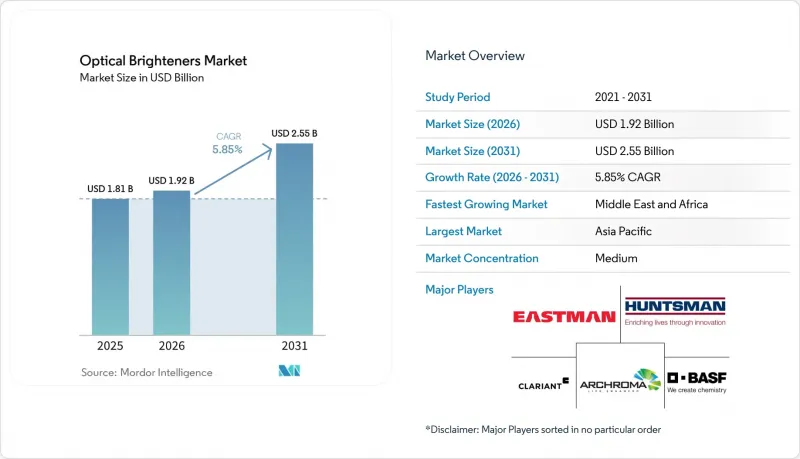

根據 Mordor Intelligence 預測,螢光增白劑的市場規模預計將從 2025 年的 18.1 億美元和 2026 年的 19.2 億美元成長到 2031 年的 25.5 億美元,2026 年至 2031 年的複合年成長率為 5.85%。

本報告按化學類型(三嗪/耆類衍生物、香豆素衍生物等)、應用領域(紡織品螢光增白劑、清潔劑螢光增白劑等)、終端用戶行業(紡織服裝、消費品、包裝及其他終端用戶行業)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球螢光增白劑市場趨勢及洞察

洗衣精中對螢光增白劑的需求增加

目前,液體清潔劑在全球家用洗滌劑市場收入中佔比超過一半,而濃縮型清潔劑的流行趨勢導致每次洗滌所需的螢光增白劑,但由於低溫洗滌和無磷助洗劑的使用,需要使用高純度的三嗪-芪類螢光增白劑(如CBS-X)來維持螢光。家用護理產品領域最大的四家跨國公司壟斷了約60%的清潔劑市場佔有率,這種寡頭壟斷的購買力迫使螢光增白劑供應商在不影響利潤率的前提下,滿足嚴格的生物分解標準。 Novonesys於2024年推出了Luminous,這是一款適用於液體和粉末兩種形式的跨基質螢光增白劑,標誌著該公司一項旨在減少跨國品牌庫存單位(SKU)的新研發計劃正式啟動。歐美零售商的高階自有品牌也開始採用螢光增白劑,以配合市場領導品牌的美學,為螢光增白劑市場建立了強大的銷售基礎。

亞太地區紡織服裝製造業的擴張

在越南、印度和孟加拉的區域價值鏈中,後表面處理工程的產能擴張速度遠超紡紗工序,導致螢光增白劑)的消耗轉移到下游的染色和洗滌環節。越南的「淨零排放藍圖」和印度的「功能性纖維生產連結獎勵計畫」(PLI)等政府計畫正在推動對螢光增白劑來恢復再生纖維加工過程中損失的白度。預計埃及索克納工業區自2026年起將新增1.5萬噸織物產量,進一步刺激中東地區的需求。由於顏色匹配和工藝故障排除仍然依賴合作關係,因此在這些叢集附近設立本地化技術服務實驗室的供應商可以在螢光增白劑市場獲得可觀的佔有率。

全球對耆類化合物的毒性和持久性制定了嚴格的法規。

2025年,歐盟委員會將UV-328列入(EU) 2019/1021號法規附件一,引入了微量含量標準,併計劃在2029年前逐步降至1毫克/公斤。中國環境保護部第12號令要求在2026年前公開配方,削弱了現有產品的智慧財產權保護。美國決定維持對來自中國大陸和台灣的耆類化合物徵收反傾銷稅,延長了供應鏈,並推高了接收成本。這些措施共同要求提交全面的雜質分析和生命週期文件,這對中小企業來說是一筆沉重的負擔,從而減緩了螢光增白劑市場的成長,而該市場原本有望健康發展。

細分市場分析

三嗪類耆類化合物憑藉其廣泛的配方相容性和高螢光量子產率,在2025年佔據了螢光增白劑市場58.15%的佔有率。其中,清潔劑級的CBS-X因其白度指數超過130且在pH值7至11範圍內保持穩定,繼續保持銷售量主導地位。香豆素類耆類化合物因其在化妝品和低熔點包裝塗料中加工溫度閾值低而備受混配商青睞,預計到2031年將以6.61%的複合年成長率成長。除上述兩大類外,苯並噁唑啉類芪類化合物(例如OB-1)在對熱穩定性要求較高的再生塑膠化合物應用中也佔據著穩固的市場佔有率,尤其是在280度C以上熱穩定性至關重要的領域。

第二類化學品,例如咪唑啉、二唑和吡唑啉,在特殊纖維整理劑領域,尤其是在耐氯運動服領域,通常佔據一定地位。江西省的一個中試規模微反應器計畫已實現了吡唑啉中間體96%的產率,這表明其在成本上具有與芪類化合物競爭的技術空間。隨著排放法規日益嚴格,能夠將現有裝置改造為連續流系統的供應商,或許可以透過銷售低碳產品線,進一步擴大其在螢光增白劑市場的佔有率。

區域分析

預計到2025年,亞太地區將佔全球螢光增白劑市場銷售額的58.76%。這主要得益於中國每年11.6萬噸的消費量以及優質化清潔劑的持續需求。江蘇和浙江兩省為實現「碳排放達峰和碳中和」目標以及更嚴格的廢水排放法規,已對產能進行合理化調整,導致區域供需更加緊張,據估計,已有12%的低價產品停產。在印度,Rossari Biotech計劃每年增產2.21萬噸,預計供應量將從2026年開始增加,其中大部分將分配給當地的紡織工業基地。在東協服飾,尤其是在越南,對先進後整理製程的投資不斷增加,推高了每米螢光增白劑的需求。

儘管歐洲和北美在螢光增白劑市場中所佔佔有率小規模,但它們的監管影響力卻極為顯著。美國反傾銷稅將持續到2030年,由此建立起一套有利於國內生產和多元化供應鏈的雙層定價體系。在歐盟,針對UV-328的附件一持久性有機污染物(POP)法規以及即將訂定的全氟烷基物質(PFAS)相關立法,正促使加工商對低遷移性的芪類替代品進行預認證,這使得擁有強大分析實驗室的生產商獲得了先發優勢。

預計中東和非洲地區將錄得最高成長率,到2031年複合年成長率將達到6.87%。這主要得益於沙烏地阿拉伯的「2030願景」紡織計畫和埃及的索克納地區。儘管該地區的成長基數較小,但越來越多的清潔劑工廠採用適合溫暖氣候的液體清潔劑,進一步加速了成長。巴西是南美洲需求的主要驅動力,索爾維公司位於聖安德烈工廠的2000萬美元現代化改造計畫旨在滿足市場對特種聚醯胺整理劑的需求,從而間接刺激該地區螢光增白劑市場的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 洗衣精中對螢光增白劑的需求增加

- 亞太地區紡織服裝製造業的擴張

- 對再生紙和包裝材料的白度要求不斷提高

- 採用這種方法來掩蓋再生塑膠流中的變色現象

- 在安全印刷和防偽油墨的應用

- 市場限制因素

- 全球對耆類化合物的毒性和持久性制定了嚴格的法規。

- 數位化導致印刷用紙的需求下降。

- 環境友善生物基替代品的研發成本

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依化學物質類型

- 三嗪/耆類化合物

- 香豆素

- 咪唑啉

- 二唑

- 苯並噁唑啉

- 其他化學品

- 透過使用

- 紡織品漂白劑

- 用於清潔劑的螢光增白劑

- 紙張光澤度提升

- 纖維增白

- 化妝品和個人護理

- 其他用途

- 按最終用戶行業分類

- 紡織服裝

- 消費品

- 包裝

- 其他終端用戶產業(安保、安全等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3V Sigma SpA

- Archroma

- Aron Universal Limited

- BASF

- Blankophor GmbH & Co. KG

- Brilliant Group Inc.

- CLARIANT

- DayGlo Color Corp.

- Deepak Nitrite Limited

- Eastman Chemical Company

- Huntsman International LLC

- Keystone Aniline Corp.

- KISCO(Kyung-In Synthetic Corp.)

- Kolorjet Chemicals Pvt Ltd

- Meghmani Organics Ltd

- Milliken & Company

- RPM International Inc.

- Sarex Chemicals

- Shandong Raytop Chemical Co. Ltd

- Teh Fong Min International Co. Ltd

- United Specialities Pvt Ltd

- Zhejiang Transfar Whyyon Chemical Co Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the optical brighteners market size is projected to expand from USD 1.81 billion in 2025 and USD 1.92 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 5.85% between 2026 to 2031.

This report is Segmented by Chemical Type (Triazine-Stilbenes, Coumarins, and More), Application (Textile Whitening, Detergent Brightener, and More), End-User Industry (Textile and Apparel, Consumer Products, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Optical Brighteners Market Trends and Insights

Rising Demand for Optical Brighteners in Laundry Detergents

Liquid detergents now generate more than half of global household laundry revenue, and the trend toward compact concentrates increases optical brightener intensity per wash. Formulators typically dose 0.1-0.5% by volume, yet colder cycles and phosphate-free builders require higher-purity triazine-stilbenes such as CBS-X to maintain fluorescence. The four largest home-care multinationals collectively command about 60% of detergent sales, creating oligopsonistic buying power that forces brightener suppliers to meet stringent biodegradability criteria without eroding margins. Novonesis introduced "Luminous" in 2024, a cross-matrix brightener designed for both liquids and powders, signaling renewed R&D aimed at reducing Stock Keeping Units (SKUs) for multinational brands. Retailers' private-label premium ranges in Europe and the U.S. are also adopting optical brighteners to match brand-leader aesthetics, cementing a durable volume base for the optical brighteners market.

Expansion of Textile and Apparel Manufacturing in Asia-Pacific

Regional value chains in Vietnam, India, and Bangladesh are scaling finishing capacity faster than spinning, shifting brightener consumption downstream into dyeing and wash-houses. Government programs such as Vietnam's net-zero road map and India's Production Linked Incentive for technical textiles are spurring investment in water-efficient dyeing lines that still depend on fluorescent agents to restore whiteness lost during recycled-fiber processing. Egypt's Sokhna industrial zone will add 15, 000 tons of fabric output from 2026, further widening Middle Eastern pull. Suppliers that localize technical-service labs near these clusters gain a defensible share of the optical brighteners market because shade matching and process troubleshooting remain relationship-driven.

Stringent Global Regulations on Stilbene Toxicity and Persistence

The European Commission added UV-328 to Annex I of Regulation (EU) 2019/1021 in 2025, introducing staged trace limits that cascade to 1 mg/kg by 2029. China's MEE Order 12 compels public disclosure of formulations by 2026, eroding intellectual-property shields for legacy products. The U.S. decision to retain antidumping duties on Chinese and Taiwanese stilbenes lengthens supply chains and raises landed costs. Collectively, these measures require comprehensive impurity profiling and life-cycle dossiers, expenses that smaller firms struggle to absorb, thereby tempering the optical brighteners market's otherwise healthy expansion.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Recycled-Paper and Packaging Brightness Requirements

- Adoption to Mask Discoloration in Recycled Plastics Streams

- Digitalization Cutting Printing-Paper Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Triazine-stilbenes captured 58.15% of the 2025 optical brighteners market share on the strength of broad formulary compatibility and high fluorescence quantum yields. Detergent-grade CBS-X can reach whiteness indexes above 130 and maintains stability from pH 7 to 11, ensuring continued volume leadership. Coumarins are forecast to advance at a 6.61% CAGR through 2031 as formulators prefer their lower-temperature processing thresholds for cosmetics and low-melt packaging coatings. Beyond the two headline groups, benzoxazolines such as OB-1 serve recycled-plastic compounding where more than 280 °C thermal stability is mandatory, sustaining a reliable niche.

Second-tier chemistries, such as imidazolines, diazoles, and pyrazolines, collectively keep a foothold in specialty textile finishing, especially chlorine-resistant sportswear. Pilot microreactor projects in Jiangxi Province demonstrate 96% yields for pyrazoline intermediates, suggesting technology headroom for cost parity with stilbenes. As emission caps tighten, suppliers able to retrofit legacy plants with continuous-flow systems may unlock incremental optical brighteners market share by marketing low-carbon product lines.

Geography Analysis

Asia-Pacific accounted for 58.76% of the global optical brighteners market revenue in 2025, driven by China's 116,000-ton annual consumption and sustained detergent premiumization. Capacity rationalization in Jiangsu and Zhejiang, spurred by dual-carbon targets and stricter wastewater rules, has already shuttered an estimated 12% of low-end output, tightening regional balances. India's ongoing 22,100 tonnes per annum (tpa) expansion by Rossari Biotech will provide incremental supply from 2026, yet is largely earmarked for local textile hubs. ASEAN's garments sector, especially in Vietnam, is investing in advanced finishing, which lifts per-meter brightener demand.

Europe and North America collectively hold a modest optical brighteners market share but wield outsized regulatory influence. The continuation of U.S. antidumping duties through 2030 locks in a two-tier price system that favors domestic output and diversified supply chains. In the EU, Annex I Persistent Organic Pollutants (POP) restrictions on UV-328 and impending Per- and Polyfluoroalkyl Substances (PFAS) legislation are persuading converters to prequalify low-migration stilbene replacements, granting early-mover advantage to producers with robust analytical labs.

The Middle-East and Africa post the fastest 6.87% CAGR to 2031, led by Saudi Arabia's woven-fabric projects under Vision 2030 and Egypt's Sokhna zone. Growth, though from a smaller base, is amplified by regional detergent factories that increasingly adopt liquid formats suitable for warmer climates. Brazil anchors South American demand, where Solvay's USD 20 million modernization of Santo Andre is designed to capture specialty polyamide finishing demand, indirectly stimulating the regional optical brighteners market volumes.

- 3V Sigma S.p.A.

- Archroma

- Aron Universal Limited

- BASF

- Blankophor GmbH & Co. KG

- Brilliant Group Inc.

- CLARIANT

- DayGlo Color Corp.

- Deepak Nitrite Limited

- Eastman Chemical Company

- Huntsman International LLC

- Keystone Aniline Corp.

- KISCO (Kyung-In Synthetic Corp.)

- Kolorjet Chemicals Pvt Ltd

- Meghmani Organics Ltd

- Milliken & Company

- RPM International Inc.

- Sarex Chemicals

- Shandong Raytop Chemical Co. Ltd

- Teh Fong Min International Co. Ltd

- United Specialities Pvt Ltd

- Zhejiang Transfar Whyyon Chemical Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for optical brighteners in laundry detergents

- 4.2.2 Expansion of textile and apparel manufacturing in Asia-Pacific

- 4.2.3 Growth in recycled-paper and packaging brightness requirements

- 4.2.4 Adoption to mask discoloration in recycled plastics streams

- 4.2.5 Use in security printing/anti-counterfeiting inks

- 4.3 Market Restraints

- 4.3.1 Stringent global regulations on stilbene-based toxicity and persistence

- 4.3.2 Digitalisation cutting printing-paper demand

- 4.3.3 R&D cost of eco-friendly bio-based substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chemical Type

- 5.1.1 Triazine-Stilbenes

- 5.1.2 Coumarins

- 5.1.3 Imidazolines

- 5.1.4 Diazoles

- 5.1.5 Benzoxazolines

- 5.1.6 Other Chemical Types

- 5.2 By Application

- 5.2.1 Textile Whitening

- 5.2.2 Detergent Brightener

- 5.2.3 Paper Brightening

- 5.2.4 Fiber Whitening

- 5.2.5 Cosmetics and Personal Care

- 5.2.6 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Textile and Apparel

- 5.3.2 Consumer Products

- 5.3.3 Packaging

- 5.3.4 Other End-user Industries (Security and Safety, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3V Sigma S.p.A.

- 6.4.2 Archroma

- 6.4.3 Aron Universal Limited

- 6.4.4 BASF

- 6.4.5 Blankophor GmbH & Co. KG

- 6.4.6 Brilliant Group Inc.

- 6.4.7 CLARIANT

- 6.4.8 DayGlo Color Corp.

- 6.4.9 Deepak Nitrite Limited

- 6.4.10 Eastman Chemical Company

- 6.4.11 Huntsman International LLC

- 6.4.12 Keystone Aniline Corp.

- 6.4.13 KISCO (Kyung-In Synthetic Corp.)

- 6.4.14 Kolorjet Chemicals Pvt Ltd

- 6.4.15 Meghmani Organics Ltd

- 6.4.16 Milliken & Company

- 6.4.17 RPM International Inc.

- 6.4.18 Sarex Chemicals

- 6.4.19 Shandong Raytop Chemical Co. Ltd

- 6.4.20 Teh Fong Min International Co. Ltd

- 6.4.21 United Specialities Pvt Ltd

- 6.4.22 Zhejiang Transfar Whyyon Chemical Co Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

螢光增白劑市場:2026-2032年全球市場預測(依產品類型、劑型、應用、終端用戶產業及通路分類)

螢光增白劑市場:2026-2032年全球市場預測(依產品類型、劑型、應用、終端用戶產業及通路分類) 全球螢光增白劑市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球螢光增白劑市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球螢光增白劑市場報告礦物濃縮收集器市場按類型、礦物、形態、應用和最終用途分類,全球預測(2026-2032年)

2026年全球螢光增白劑市場報告礦物濃縮收集器市場按類型、礦物、形態、應用和最終用途分類,全球預測(2026-2032年) 螢光增白劑市場規模、佔有率和成長分析(按化學類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測

螢光增白劑市場規模、佔有率和成長分析(按化學類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測 2032 年螢光增白劑市場預測:按類型、應用、最終用戶和地區進行的全球分析

2032 年螢光增白劑市場預測:按類型、應用、最終用戶和地區進行的全球分析 全球螢光增白劑市場規模、佔有率、趨勢分析報告:2025 年至 2032 年按應用、最終用途和地區分類的展望和預測

全球螢光增白劑市場規模、佔有率、趨勢分析報告:2025 年至 2032 年按應用、最終用途和地區分類的展望和預測 螢光增白劑市場報告:2031 年趨勢、預測與競爭分析

螢光增白劑市場報告:2031 年趨勢、預測與競爭分析 螢光增白劑市場規模、佔有率、趨勢分析報告:按應用、最終用途、地區、細分市場預測,2025-2030 年2024 年至 2031 年按類型、應用、最終用戶和地區劃分的光學螢光染料市場

螢光增白劑市場規模、佔有率、趨勢分析報告:按應用、最終用途、地區、細分市場預測,2025-2030 年2024 年至 2031 年按類型、應用、最終用戶和地區劃分的光學螢光染料市場