|

市場調查報告書

商品編碼

2063505

醫療保健合約管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Healthcare Contract Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

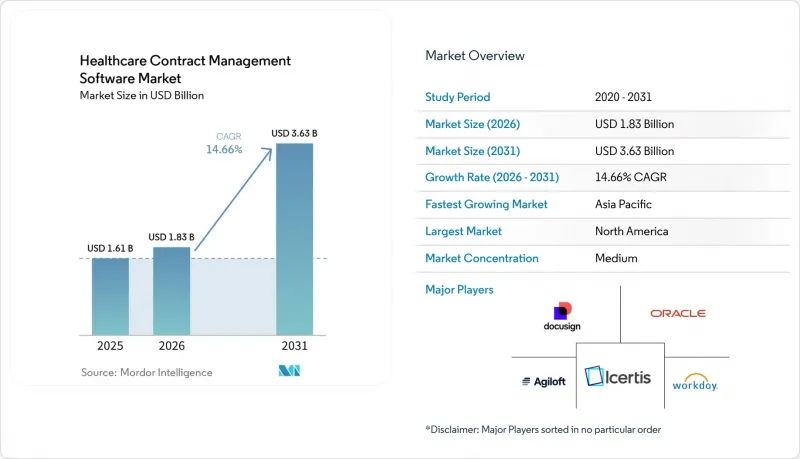

根據 Mordor Intelligence 預測,醫療保健合約管理軟體市場將從 2025 年的 16.1 億美元成長到 2026 年的 18.3 億美元,到 2031 年達到 36.3 億美元,2026 年至 2031 年的複合年成長率為 14.66%。

本報告按解決方案類型(合約生命週期管理、文件管理、供應商/供貨商系統及其他)、部署模式(雲端、本地部署)、最終用戶(服務提供者及其他)、組織規模(大型企業、中型企業、中小企業)和地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球醫療保健合約管理軟體市場趨勢與洞察

醫療保健產業的數位轉型以合規性為先(以 HIPAA/GDPR 為主導的CLM 實施)

隨著對機構隱私和安全監管力道的加大,標準化合約管治的壓力也日益增大。 HIPAA 法規的要求不斷提高,促使機構與雲端服務供應商、電子病歷 (EHR) 供應商、計費服務商和其他合作夥伴簽訂業務協議 (BAA) 的需求也隨之增加,以降低資料外洩的風險。隨著審計和事件報告要求的不斷提高,醫院和保險公司正逐步淘汰透過資料夾、共用磁碟機和電子郵件建立文件的方式,轉而採用集中式儲存庫,並配備基於角色的存取控制和不可篡改的稽核追蹤功能,記錄所有對敏感記錄的操作。自動化的合規性檢查和更新警報功能使團隊能夠在產生罰款之前識別未簽署的 BAA 和過期的條款。這不僅節省了時間用於更有價值的談判,還降低了審計期間違規的可能性。其他監管司法管轄區也面臨類似的管治壓力,這些地區正在強制執行嚴格的隱私和安全標準,進一步增加了醫療保健合約管理軟體市場對自動化條款庫、核准流程和證據收集的需求。隨著有關系統存取、身分管理和職責分離的政策日趨成熟,各組織正在協調其法律、合規、採購和 IT 部門,以維護有關合約和相關義務的“單一真相”,從而減少人工交接和潛在風險。

優先採用雲端技術和訂閱定價模式,使實施和投資回報率更容易實現。

SaaS平台無需專用硬體、資料庫管理和災害復原基礎設施,使資源有限的IT團隊能夠以可預測的營運成本和快速實現價值的方式部署企業級合約生命週期管理(CLM)。基於訂閱的定價模式和簡化的使用者體驗降低了門診診所和行為健康機構的進入門檻。同時,可擴展的租用戶環境和持續更新確保安全標準始終保持最新,無需漫長的修補週期。醫療團隊還能受益於整合的電子簽章、工作流程路由和身分管理服務,這些服務可與常用的辦公室套件和業務系統連接,從而簡化談判流程並確保文件完整。決策者在考慮各種方案時,會意識到基於雲端的CLM能夠加快核准流程、實現遠端協作,並提供週期時間和瓶頸分析的可見性,而這些在本地孤立的環境中難以量化。這些核心功能將進一步加速醫療合約管理軟體在市場上的普及,尤其對於那些尋求低風險現代化路徑的中小型企業而言。

傳統IT整合、資料遷移與安全挑戰

包含多個電子病歷 (EHR)、企業資源計畫 (ERP) 系統和客製化收入週期系統的異質環境會使資料映射和介面設計變得複雜,可能延長部署時間,並在遷移過程中造成並行處理負擔。團隊需要標準化遺留欄位、整理歸檔儲存庫並檢驗條款元元資料,以確保可靠的下游分析並能夠經受大規模審計。 HITRUST 和 SOC 2 II 型等安全認證通常是醫療保健採購的強制性要求,而過時的證據和控制結構可能導致供應商資格被取消或批准延遲。對於具有大量客製化和獨特數據需求的組織,部署週期可能會延長,由於員工需要在轉型和日常營運之間疲於奔命,因此可能會延遲短期投資回報率的實現。這些現實情況持續對醫療保健合約管理軟體市場構成挑戰,因為買家往往低估了整合分散文件並將其與臨床、財務和供應鏈工作流程整合所需的工作量。

細分市場分析

到2025年,合約生命週期管理軟體將佔據47.66%的市場佔有率,這反映了市場對涵蓋各類醫療保健合約的端到端起草、談判、執行和義務管理的需求。此類別應用廣泛,已成為法律和銷售團隊用於管理範本、條款庫和分析功能的控制中心,從而在醫療保健合約管理軟體市場中,為醫療服務提供者、支付方和供應商提供一致的管治。合約文件管理軟體預計將成為成長最快的細分市場,到2031年複合年成長率將達到14.74%。這部分歸因於許多中型醫院優先考慮具有人工智慧資訊擷取功能的中央儲存庫,力求將傳統的基於資料夾和電子郵件的儲存位置整合到一個搜尋且值得信賴的資訊來源中。供應商合約管理功能與ERP和採購系統整合,透過應用目錄定價和標記合約外支出以促使採取糾正措施,有助於控制成本支出並提高附加價值。以合規為中心的解決方案對於管理 BAA(商業協議)、根據公平市場價值基準檢查醫生薪酬以及在系統層面監控利益衝突和宣誓書仍然至關重要。

「其他」類別包括人工智慧驅動的分析模組,這些模組能夠分析條件規則並為基於價值的合約生成支付模擬;此外還包括採購整合平台,這些平台可為即時儀表板提供信息,以進行支出管治。生命科學領域的應用案例持續擴展,領先的製藥和醫療設備製造商正在大規模地實現扣回爭議帳款和回扣的自動化,並報告錯誤率降低,從而實現了快速的投資回報。 Contract Logix 和其他專業公司正在透過詳細的流程品管,支援製藥業長期以來用於追蹤複雜供應合約和回扣的工作流程。 DiliTrust 專注於 GxP 的功能和分析正在幫助歐洲製藥客戶縮短週期並降低成本,這表明結構化模板和管治如何使受監管的工作流程受益。隨著買家評估功能深度以匹配其成熟度和範圍,這些解決方案類型正在共同擴大醫療保健合約管理軟體市場。

預計到2025年,基於雲端的採用將佔營收的50.48%,複合年成長率(CAGR)為16.23%。這反映出向SaaS營運模式的轉變,該模式有助於更新、整合和安全標準的實施。團隊可以受益於彈性擴充性、託管服務和頻繁的功能發布,同時還能擴展對人工智慧功能和電子簽章工作流程的訪問,從而加速分散式醫療環境中的合約執行,並減輕內部IT部門的生命週期負擔。採用雲端技術的組織也在加速跨職能協作,因為法律、合規和銷售團隊可以透過共用系統處理任務,該系統可以記錄活動並提取分析數據,而無需人工核對。這些因素正在推動醫療合約管理軟體市場擴大其覆蓋範圍,以滿足醫療服務提供者和保險公司透過協調的工作流程實施基於價值的醫療(VBC)和採購政策的需求。

對於擁有舊有系統、區域部署需求或大規模客製化需求的組織而言,本地部署和混合模式仍然至關重要,因為這些因素可能會延長遷移過程。混合模式有助於將人力資源、財務和供應鏈模組與大規模系統中的現場臨床系統整合,從而減輕合約和商業管治現代化帶來的營運影響。無論選擇何種託管方案,能夠降低身分和存取風險、簡化核准流程並集中審計追蹤的整合藍圖在部署中仍然發揮核心作用。在整個預測期內,隨著各組織在追求標準化的同時避免本地環境帶來的巨額開銷,互通性需求和分散式工作模式預計將進一步增強醫療保健合約管理軟體市場的「雲端優先」趨勢。

區域分析

預計到2025年,北美將佔據45.56%的市場。這主要得益於嚴格的隱私法規的實施、電子健康記錄(EHR)的成熟應用,以及向基於價值的模式的早期轉型,這些都增加了對義務追蹤的需求。監管機構對商業協議(BAA)和安全認證的重視,推動了醫療服務提供者和支付方採用集中式儲存庫、自動化管理和詳細審計追蹤。與支付方模式連結的合約智慧,有助於美國機構解讀複雜的品質指標和支付結構,而不會延誤索賠和報銷流程。各機構也致力於簡化電子簽章和調整工作流程,以提高處理能力,減少紙本文件帶來的風險和浪費,這支撐著合約實踐的持續現代化。這些因素確保了醫療合約管理軟體市場在整合醫療服務網路和區域醫療系統的績效和合規工作中繼續佔據核心地位。

在歐洲,隱私、安全和互通性是重中之重,數位化進程正在國家和企業層面穩步推進。該地區的生命科學和醫療設備製造商正優先考慮符合GxP規範的管理架構、可隨時接受審計的系統以及能夠體現標準化條款庫和管治價值的分析能力。服務受監管行業的供應商提供多語言支援和根據區域要求量身定做的隱私認證,這有助於跨境部署和政策的一致性執行。隨著各組織在統一的管理架構下簡化與供應商、研究機構和合作夥伴的契約,電子簽章和整合工作流程的應用也在不斷擴展。這些功能正在增強醫療保健合約管理軟體市場,因為歐洲買家正在將其合約營運與更廣泛的數據管治計劃相協調。

預計到2031年,亞太地區將成為成長最快的地區,複合年成長率將達到15.3%。這主要得益於醫療系統積極推進數位化優先的醫療模式以及用於分析和人工智慧的數據基礎設施建設。區域夥伴關係關係凸顯了醫療服務提供者網路如何將合約與互聯醫療的目標相契合,包括協作設計人工智慧驅動的工作流程和預測性資料管理,以確保營運就緒。隨著各機構優先考慮標準化工作流程並逐步淘汰人工流程和紙本流程,電子簽章、集中式儲存庫和開箱即用的整合方案的應用日益普及。醫療合約管理軟體市場也從中受益,因為醫療服務提供者和支付方正在擴大其專案參與範圍和數位化運營,從而推動了對安全雲端平台、結構化元資料和強大分析功能的需求,以管理各種類型的合約。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 醫療保健產業的數位轉型以合規性為優先(以 HIPAA/GDPR 為驅動的 CLM 實施)

- 優先採用雲端技術和訂閱式定價模式,有助於部署並提高投資報酬率。

- 醫療服務提供者和保險公司需要提高營運效率並降低成本。

- 人工智慧驅動的合約分析、義務追蹤和風險評分

- 基於價值的醫療保健以及支付方和提供方之間合約的複雜性

- 採購與電子病歷/企業資源規劃系統整合:將合約條款與支出和報銷連結起來

- 市場限制因素

- 傳統IT整合、資料遷移與安全挑戰

- 實施和客製化成本高昂,且在變革管理方面面臨挑戰。

- 所有權分散在法律、供應鏈和合規部門之間,減緩了管治。

- 與收入周期重疊/支付方合約建模工具的替代發生

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按解決方案類型

- 合約生命週期管理軟體

- 合約文件管理軟體

- 供應商合約管理系統

- 合規與監理合約管理系統

- 其他

- 不同的發展

- 基於雲端的

- 現場

- 最終用戶

- 醫療服務提供方

- 醫療保健支付方

- 藥品和醫療設備

- 其他

- 按組織規模

- 大公司

- 中型公司

- 小規模企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Agiloft

- CobbleStone Software

- Compliatric

- Contract Logix

- ContractWorks

- Corcentric

- Coupa CLM

- DocuSign CLM

- FinThrive

- GHX

- Icertis

- Infor

- Infosys Helix

- Ironclad

- Ivalua

- JAGGAER

- Ntracts

- Oracle

- Premier Inc.

- SAP Ariba

- SirionLabs

- symplr

- Vizient

- Workday

- Zycus

第7章 市場機會與未來展望

According to Mordor Intelligence, the healthcare contract management software market size is expected to increase from USD 1.61 billion in 2025 to USD 1.83 billion in 2026 and reach USD 3.63 billion by 2031, growing at a CAGR of 14.66% over 2026-2031.

This report is Segmented by Solution Type (Contract Lifecycle Management, Document Management, Vendor/Supplier Systems, and, Others), Deployment (Cloud, On-Premises), End-User (Providers, and, Others), Organization Size (Large, Mid-Market, Small), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Value (USD).

Global Healthcare Contract Management Software Market Trends and Insights

Compliance-First Digitalization in Healthcare (HIPAA/GDPR-driven CLM adoption)

Heightened privacy and security oversight keeps pushing organizations to standardize contract governance, with HIPAA requirements elevating the need for executed Business Associate Agreements across cloud providers, EHR vendors, billing services, and other partners to reduce breach exposure.As audit and incident reporting expectations increase, hospitals and payers are phasing out folders, shared drives, and email-driven authoring in favor of centralized repositories with role-based access and immutable audit trails that document every action on sensitive records. Automated compliance checks and renewal alerts help teams surface missing BAAs and outdated clauses before they turn into penalties, which preserves time for higher-value negotiations and reduces the probability of non-compliance during reviews. The same governance pressures apply in other regulated jurisdictions that enforce strict privacy and security standards, which reinforces the case for automated clause libraries, approvals, and evidence capture across the healthcare contract management software market. As system access, identity management, and segregation of duties policies mature, organizations align legal, compliance, procurement, and IT to maintain a single version of truth for contracts and associated obligations, reducing manual handoffs and hidden risk.

Cloud-First Rollouts and Subscription Pricing Ease Deployment & ROI

SaaS platforms remove the need for dedicated hardware, database administration, and disaster recovery buildouts, which helps lean IT teams stand up enterprise-grade CLM with predictable operating spend and faster time to value. Subscription pricing and simplified UX lower barriers for ambulatory clinics and behavioral health organizations, while scalable tenancy and continuous updates keep security baselines current without lengthy patch cycles. Healthcare teams also benefit from integrated eSignature, workflow routing, and identity services that connect common productivity suites and line-of-business systems to keep negotiations moving and documentation complete. As decision-makers weigh alternatives, they see that cloud CLM accelerates approvals, enables remote collaboration, and surfaces analytics on cycle times and bottlenecks that were difficult to quantify with on-premises silos. These fundamentals support broader adoption of the healthcare contract management software market among mid-market and small enterprises seeking lower-risk modernization paths.

Legacy IT Integration, Data Migration, and Security Hurdles

Heterogeneous estates that include multiple EHRs, ERPs, and custom revenue-cycle systems complicate data mapping and interface design, which can extend rollouts and create parallel-process burdens during migration. Teams must normalize legacy fields, clean archival repositories, and validate clause metadata to ensure downstream analytics are reliable and auditable at scale. Security certifications such as HITRUST and SOC 2 Type II are often table stakes in healthcare procurement and can disqualify vendors or delay approvals if evidence and controls are not current. Implementation timelines may stretch for organizations with heavy customizations or sovereign data needs, which can slow near-term ROI as staff balance transformation with daily operations. These realities remain a headwind for the healthcare contract management software market when buyers underestimate the effort required to centralize scattered documents and align integrations with clinical, financial, and supply workflows.

Other drivers and restraints analyzed in the detailed report include:

- Operational Efficiency and Cost Containment Imperatives in Providers & Payers

- AI-Enabled Contract Analytics, Obligation Tracking, and Risk Scoring

- High Implementation/Customization Costs and Change Management Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contract Lifecycle Management Software held 47.66% in 2025, reflecting demand for end-to-end authoring, negotiation, execution, and obligation management across diverse healthcare agreements. The category's breadth positions it as the control center for templates, clause libraries, and analytics that legal and commercial teams use to scale consistent governance across providers, payers, and suppliers within the healthcare contract management software market. Contract Document Management Software is projected to grow the fastest at 14.74% CAGR to 2031, in part because many mid-market hospitals prioritize central repositories with AI-powered extraction to consolidate legacy folders and email-based storage into a searchable single source of truth. Vendor and supplier contract management capabilities that connect to ERP and purchasing systems increase value by enforcing catalog pricing and flagging off-contract spend for corrective action that curbs leakage. Compliance-oriented solutions remain essential for BAA management, physician compensation checks against fair-market-value benchmarks, and monitoring of conflicts and attestations at the system level.

"Others" includes AI-driven analytics modules that parse conditional rules and produce payout simulations for value-based arrangements as well as procurement-integrated platforms that feed real-time dashboards for spend governance. Life sciences use cases continue to grow, with large pharma and device companies automating chargebacks and rebates at scale and reporting error-rate reductions that translate into rapid ROI. Contract Logix and other specialists support long-standing pharmaceutical workflows for complex supply agreements and rebate tracking through granular line-item management. DiliTrust's GxP-focused features and analytics have been associated with cycle-time and cost improvements for European pharma clients, showing how regulated workflows benefit from structured templates and governance. These solution types collectively expand the healthcare contract management software market as buyers match capability depth to their maturity and scope.

Cloud-based deployments accounted for 50.48% of 2025 revenues and are growing at a 16.23% CAGR, which reflects a shift to SaaS operating models that ease updates, integration, and security baselines. Teams benefit from elastic scale, managed services, and frequent feature releases that reduce the lifecycle burden on internal IT while expanding access to AI features and eSignature workflows that accelerate contracting in distributed care settings. Cloud adopters also see faster cross-functional collaboration because legal, compliance, and commercial teams route work from a shared system that logs activity and extracts analytics without manual reconciliation. These factors help the healthcare contract management software market broaden reach among providers and payers that need to operationalize VBC and procurement policies through orchestrated workflows.

On-premises and hybrid models remain relevant for organizations with legacy estates, local residency mandates, or extensive customizations, which can extend migration paths. Hybrid approaches help large systems harmonize HR, finance, and supply chain modules with on-site clinical systems to reduce disruption as they modernize contracting and commercial governance. Integration blueprints that reduce identity and access risks, streamline approvals, and centralize audit artifacts remain central to adoption, regardless of hosting choice. Over the forecast period, interoperability requirements and distributed work models are expected to keep cloud-first momentum strong within the healthcare contract management software market as organizations pursue standardization without heavy on-premises overheads.

Geography Analysis

North America commanded 45.56% in 2025, supported by stringent privacy enforcement, mature EHR adoption, and early movement into value-based models that increase obligation tracking needs. Regulatory emphasis on BAAs and security certifications sustains adoption of centralized repositories, automated controls, and rich audit trails across providers and payers. Contract intelligence tied to payer models helps U.S. organizations interpret complex quality measures and payment structures without slowing claims or reimbursement timelines. Organizations also focus on streamlined eSignature and workflow orchestration to improve throughput and reduce paper-based risk and waste, which supports continued modernization of contracting practices. These factors keep the healthcare contract management software market central to performance and compliance initiatives across integrated delivery networks and regional systems.

Europe shows steady momentum as privacy, security, and interoperability priorities continue to advance digitization agendas at national and enterprise levels. Life sciences and device manufacturers in the region emphasize GxP-aligned controls, audit readiness, and analytics that demonstrate value from standardized clause libraries and governance. Vendors serving regulated industries offer multi-language support and privacy certifications that fit regional requirements, which encourages cross-border deployments and consistent policy execution. eSignature and integrated workflow adoption also expands as organizations streamline agreements with suppliers, research sites, and partners under unified controls. These capabilities strengthen the healthcare contract management software market as European buyers coordinate contracting alongside broader data governance programs.

Asia-Pacific is projected to be the fastest-growing region at 15.3% CAGR through 2031 as health systems pursue digital-first care models and data readiness for analytics and AI. Regional partnerships highlight how provider networks align contracting with connected-care objectives, such as initiatives to co-design AI-enabled workflows and predictive data management for operational readiness. Adoption of eSignature, centralized repositories, and out-of-the-box integrations grows as organizations eliminate manual routing and paper-heavy processes in favor of standardized workflows. As providers and payers scale program participation and digital operations, the healthcare contract management software market gains from demand for secure cloud platforms, structured metadata, and strong analytics to govern diverse agreements.

- Agiloft

- CobbleStone Software

- Compliatric

- Contract Logix

- ContractWorks

- Corcentric

- Coupa CLM

- DocuSign CLM

- FinThrive

- GHX

- Icertis

- Infor

- Infosys Helix

- Ironclad

- Ivalua

- JAGGAER

- Ntracts

- Oracle

- Premier

- SAP Ariba

- SirionLabs

- symplr

- Vizient

- Workday

- Zycus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compliance-First Digitalization in Healthcare (HIPAA/GDPR-driven CLM adoption)

- 4.2.2 Cloud-First Rollouts and Subscription Pricing Ease Deployment & ROI

- 4.2.3 Operational Efficiency and Cost Containment Imperatives in Providers & Payers

- 4.2.4 AI-Enabled Contract Analytics, Obligation Tracking, and Risk Scoring

- 4.2.5 Value-Based Care and Payer-Provider Contracting Complexity

- 4.2.6 Procurement-EHR/ERP Integration Linking Contract Terms to Spend & Reimbursement

- 4.3 Market Restraints

- 4.3.1 Legacy IT integration, Data Migration, and Security Hurdles

- 4.3.2 High Implementation/Customization Costs and Change Management Gaps

- 4.3.3 Fragmented Ownership Across Legal, Supply Chain, and Compliance Slows Governance

- 4.3.4 Overlap with Revenue-Cycle/Payer Contract Modeling Tools Creates Substitution

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 Contract Lifecycle Management Software

- 5.1.2 Contract Document Management Software

- 5.1.3 Vendor & Supplier Contract Management Systems

- 5.1.4 Compliance & Regulatory Contract Management Systems

- 5.1.5 Others

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By End-User

- 5.3.1 Healthcare Providers

- 5.3.2 Healthcare Payers

- 5.3.3 Pharmaceuticals & Medical Devices

- 5.3.4 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Mid-market Enterprises

- 5.4.3 Small Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Agiloft

- 6.3.2 CobbleStone Software

- 6.3.3 Compliatric

- 6.3.4 Contract Logix

- 6.3.5 ContractWorks

- 6.3.6 Corcentric

- 6.3.7 Coupa CLM

- 6.3.8 DocuSign CLM

- 6.3.9 FinThrive

- 6.3.10 GHX

- 6.3.11 Icertis

- 6.3.12 Infor

- 6.3.13 Infosys Helix

- 6.3.14 Ironclad

- 6.3.15 Ivalua

- 6.3.16 JAGGAER

- 6.3.17 Ntracts

- 6.3.18 Oracle

- 6.3.19 Premier Inc.

- 6.3.20 SAP Ariba

- 6.3.21 SirionLabs

- 6.3.22 symplr

- 6.3.23 Vizient

- 6.3.24 Workday

- 6.3.25 Zycus

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

CLM:不斷演進的經營模式PKI 和 CLM:CLM 在 PKI 的實施和增強中的作用

CLM:不斷演進的經營模式PKI 和 CLM:CLM 在 PKI 的實施和增強中的作用 2026年全球合約管理系統人工智慧(AI)市場報告2026年全球合約自動化軟體市場報告

2026年全球合約管理系統人工智慧(AI)市場報告2026年全球合約自動化軟體市場報告 企業合約管理市場:依解決方案、企業規模、部署類型和產業分類-2026-2032年全球市場預測

企業合約管理市場:依解決方案、企業規模、部署類型和產業分類-2026-2032年全球市場預測 全球合約生命週期管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)合約管理軟體市場:按組件、組織規模、部署模式、應用和產業分類-2026-2032年全球市場預測2026年全球合約生命週期管理市場報告2026年全球合約管理軟體市場報告

全球合約生命週期管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)合約管理軟體市場:按組件、組織規模、部署模式、應用和產業分類-2026-2032年全球市場預測2026年全球合約生命週期管理市場報告2026年全球合約管理軟體市場報告 合約生命週期管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和部署階段分類

合約生命週期管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和部署階段分類