|

市場調查報告書

商品編碼

2063495

醫療設備標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Medical Device Labeling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

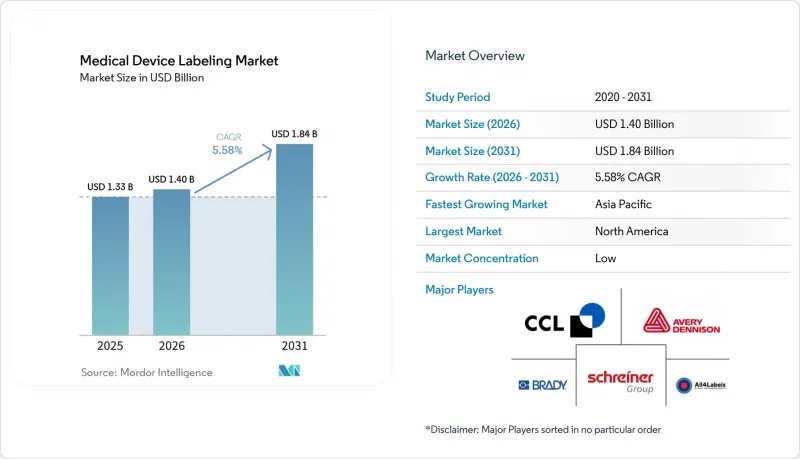

據 Mordor Intelligence 稱,醫療設備標籤市場在 2025 年的價值為 13.3 億美元,預計到 2031 年將達到 18.4 億美元,而 2026 年為 14 億美元,預測期(2026-2031 年)的複合年成長率為 5.58%。

本報告按標籤類型(壓敏黏著劑/自黏標籤、膠粘/濕膠標籤、熱縮套管標籤、套模)、應用領域(一次性耗材、監測和診斷設備、治療和手術器械)以及地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球醫療設備標籤市場趨勢及洞察

UDI 的全球強制性要求及其在資料庫中的註冊,正在擴大對標籤資料和雙格式條碼的要求。

美國FDA於2025年加強了GUDID的執行力度,對條碼內容與資料庫欄位不符的情況發出警告信,因此加工商現在需要檢驗尺寸小至10mm x 15mm的2D條碼標籤。中國於2024年完成了UDI的分階段實施,強制要求在I類醫療設備上顯示機讀識別碼。這迫使出口商重新設計標籤,以適應雙語文字和GS1或HIBC條碼方案。日本、新加坡、馬來西亞和巴西也採用了類似的框架,這可能導致同一型號的醫療設備出現五種以上的區域標籤版本。這些法規迫使醫療設備製造商遷移到基於雲端的標籤管理系統,以實現標籤版本控制和法規變更追蹤的自動化。

MDR/IVDR 的多語言和翻譯規則增加了 SKU 的數量和標籤上的內容。

根據2025年7月生效的歐盟法規2025/1234,商用醫療設備的紙本說明書將被電子版說明書(eIFU)取代,但這將導致庫存單位(SKU)數量翻倍,因為每種語言的標籤都必須有一個唯一的2D碼連結。即使是同一台輸液泵,在歐盟市場也可能需要24種不同的標籤設計,而且用德語印刷的庫存無法合法運往西班牙,這增加了庫存風險。據翻譯公司稱,自2024年以來,醫療設備標籤專案激增了30%,提供內部語言檢驗服務的翻譯公司透過縮短認證週期贏得了更多合約。

合規負擔和頻繁的監管更新正在增加標籤製造商的成本和上市時間。

歐盟在2021年至2025年間發布了89份指導文件,所有這些文件都可能改變標籤的內容。同時,認證機構的核准流程延誤長達12個月,迫使企業修改標籤設計,每次修改的成本在5,000美元至15,000美元之間。中國在2024年發布了14份單一來源識別(UDI)通知,但各省執行情況的不一致加劇了出口商的不確定性。中小型製造商在合規方面的支出佔銷售收入的很大一部分,而跨國公司這一比例僅為2%,這正在加速產業結構調整。

細分市場分析

截至2025年,感壓標籤標籤佔醫療設備標籤市場57.37%的佔有率。這主要歸功於其與每分鐘300-600個標籤的貼標線相容,以及其對伽馬射線、環氧乙烷和蒸氣滅菌的耐受性。丙烯酸或橡膠基黏合劑即使在暴露於50 kGy的輻射下,也能保持其黏合強度而不泛黃。預計到2031年,黏合劑標籤或濕膠標籤將以每年5.89%的速度成長,成為成長最快的標籤類型。這是因為藥廠在用注射液灌裝管瓶時,更重視標籤的永久黏合性,而非易撕易貼的便利性。濕膠黏合系統透過滲透基材形成機械黏合,防止低溫運輸中因冷凝而導致的分層,但需要10-15秒的保持時間,從而將生產線速度降低至每分鐘150-250個標籤。

到2025年,收縮套管將佔據相當大的銷售量,尤其適用於預填充式注射器等具有整合式安全針頭的複合材料產品。這些產品憑藉其360度圖形展示功能,價格溢價30-40%是合理的。套模標籤目前仍屬於小眾產品,但由於其在吹塑成型或射出成型檢體杯的過程中即可完成,因此無需後續的成型工序。歐盟的一次性塑膠指令將於2024年生效,該指令豁免了醫療設備,但鼓勵評估與容器樹脂相容的可回收表面材料。 UPM Raflatac將於2025年推出無內襯結構,透過減少15%的材料廢棄物和降低運輸成本,吸引永續性的製造商。

區域分析

到2025年,北美將佔據醫療設備標籤市場45.85%的佔有率,主要得益於FDA實施UDI標準以及GUDID同步要求。 2024年,FDA向國內外製造商發出14封警告信,原因是其不合規。加拿大於2024年將其醫療設備法規與FDA標準接軌,強制要求通報標籤相關的不利事件,並要求魁北克省使用法語和英語雙語標籤。墨西哥聯邦衛生風險防護委員會(COFEPRIS)於2025年採納了UDI標準,簡化了標籤設計,並根據美墨加協定(USMCA)的規定,在北美地區形成了一個監管聯盟,強制要求使用英語、法語和西班牙語三語標籤。

在歐洲,向醫療器材法規 (MDR) 和體外診斷醫療器材法規 (IVDR) 的過渡正在進行中。德國、法國、義大利、西班牙和波蘭已強制要求在醫療器材說明書中包含當地語言版本,並導致標籤 SKU 的細分。英國將於 2024 年強制使用 UKCA 標誌,這意味著除了符合歐盟 MDR 規定的北愛爾蘭標籤外,還需要為大不列顛地區單獨貼標籤,從而需要平行庫存管理。將於 2025 年 7 月生效的 2025/1234 號法規允許醫療器材使用者使用電子版使用說明書 (eIFU),但仍要求每種語言提供QR碼和網址,這增加了設計複雜性,卻並未降低印刷成本。

預計到2031年,亞太地區的複合年成長率將達到6.08%,在所有地區中最高。中國於2024年完成了UDI的實施,強制要求在國家藥品監督管理局(NMPA)資料庫中註冊I類醫療設備標識符,並推廣雙格式條碼的使用。印度的生產連結獎勵計畫計畫已向國內製造業注入14億美元,促進了本地標籤採購,並吸引了來自普納、艾哈默德巴德和清奈等地的跨國加工企業的投資。日本藥品和醫療器材管理局(PMDA)於2024年批准了電子使用說明書(eIFU),該說明書符合美國FDA和歐盟的先例,同時對標籤上日文字符和漢字的可讀性保持了嚴格的標準。 2025年,中東和非洲、南美洲以及亞太地區的小規模市場在整體銷售額中佔了相當大的佔有率。巴西國家衛生監督局(ANVISA)於2024年發布了UDI指南,強制要求III類和IV類醫療設備在2026年前採用GS1或HIBC編碼。澳洲藥品管理局(TGA)於2024年將其UDI要求與美國食品藥物管理局(FDA)和歐盟的框架接軌,簡化了太平洋地區的UDI設計。同時,韓國食品藥品安全部(MFDS)強制要求進口商品使用韓文標籤。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球 UDI 法規和資料庫註冊正在擴大對標籤資料和雙格式條碼的要求。

- MDR/IVDR 的多語言支援和翻譯規則增加了標籤上的 SKU 數量和內容量。

- 家庭醫療保健設備的日益普及以及穿戴式設備和即時檢測 (POCT) 設備的激增,推動了對耐用且便於患者使用的標籤的需求。

- 對召回和追蹤/追溯的需求日益成長,加速了 UDI 標籤的使用,而 UDI 標籤大量使用了2D條碼。

- 在外科手術包和植入。

- 滅菌工作流程提倡使用指示標籤和文件(SPD/CSSD)。

- 市場限制因素

- 合規負擔和頻繁的監管變化正在增加標籤製造商的成本和上市時間。

- 標籤加工產業日益分散,導致價格壓力巨大,利潤空間縮小。

- 直接部件標記 (UDI) 正在取代某些可重複使用醫療設備上的外部標籤。

- 電子使用說明書的引入將減少對紙本手冊和傳單的需求,以便展示有關商用設備的資訊。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 標籤類型

- 壓力敏感

- 黏合劑

- 收縮套

- 套模標籤

- 透過使用

- 免洗耗材

- 監測和診斷設備

- 治療/手術器械

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- All4Labels Group

- Avery Dennison

- Beontag

- Brady Corporation

- Brook & Whittle

- CCL Industries

- Cisper Electronics

- CleanMark Labels

- Domino Printing Sciences

- Fortis Solutions Group

- HERMA GmbH

- Inovar Packaging Group

- LINTEC Corporation

- Loftware

- Propper Manufacturing

- Resource Label Group

- RFiD Discovery

- SATO Holdings

- Schreiner Group

- Taylor Corporation

- UPM Raflatac

第7章 市場機會與未來展望

According to Mordor Intelligence, the medical device labeling market size was valued at USD 1.33 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Label Type (Pressure-sensitive/Self-adhesive, Glue-applied/Wet-glue, Shrink Sleeves, In-Mold), Application (Disposable Consumables, Monitoring & Diagnostic Equipment, Therapeutic & Surgical Instruments), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Device Labeling Market Trends and Insights

Global UDI Mandates and Database Submissions Expand Label Data and Dual-Format Barcode Requirements

The U.S. FDA intensified GUDID enforcement in 2025, issuing warning letters when barcode content and database fields diverged, so converters now validate 2D symbols down to 10 mm X 15 mm labels. China finished its phased UDI rollout in 2024, requiring Class I devices to carry machine-readable identifiers, driving exporters to redesign labels for bilingual text and GS1 or HIBC symbologies . Japan, Singapore, Malaysia, and Brazil adopted similar frameworks, meaning one device model may ship with five or more regional label variants. These mandates push device firms toward cloud label-management systems that automate artwork versioning and regulatory change tracking.

MDR/IVDR Multi-Language and Translation Rules Increase Label SKUs and Content Volume

Under EU Regulation 2025/1234, effective July 2025, professional-use devices may replace paper booklets with eIFU, but each language still needs a unique QR link on the label, multiplying SKUs . A single infusion pump can require 24 label designs for the bloc, inflating inventory risk because German-printed stock cannot legally ship to Spain. Translation suppliers report a 30% surge in device-label projects since 2024, and converters that offer in-house language validation win contracts by shortening certification timelines.

Compliance Burden and Frequent Regulatory Updates Raise Cost/Time-to-Market for Labelers

The EU issued 89 guidance documents between 2021 and 2025, each potentially altering label content, while notified-body backlogs stretch to 12 months, forcing multiple artwork revisions that cost USD 5,000-15,000 per iteration. China published 14 UDI circulars in 2024, and inconsistent provincial enforcement adds uncertainty for exporters. Small manufacturers spend up to a notable share of sales on regulatory affairs versus 2% for multinationals, accelerating industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Rising Home-Use, Wearable, and POCT Devices Elevate Demand for Durable, Patient-Friendly Labels

- Increased Recall and Track-and-Trace Needs Accelerate 2D-Barcode-Rich UDI Labeling

- Fragmented Label-Converting Landscape Intensifies Pricing Pressure and Margin Squeeze

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure-sensitive labels held 57.37% of the medical device labeling market in 2025, driven by compatibility with 300-600 labels-per-minute application lines and gamma, ethylene-oxide, and steam sterilization. Acrylic or rubber adhesives maintain bond strength through 50 kGy irradiation without yellowing. Glue-applied or wet-glue labels are forecast to grow at 5.89% through 2031, the fastest rate, as pharmaceutical firms package liquid injectables in glass vials where permanent adhesion outweighs peel-and-reseal convenience. Wet-glue systems create mechanical bonds by penetrating substrates, preventing lift during cold-chain condensation, yet they require 10-15 second dwell times that slow lines to 150-250 units per minute.

Shrink sleeves represented a notable share of volume in 2025, favored for combination products such as pre-filled syringes with integrated safety needles, where 360-degree graphics justify a 30-40% premium. In-mold labels remain niche, applied during blow or injection molding of specimen cups, eliminating post-molding steps. The EU Single-Use Plastics Directive, effective in 2024, exempts medical devices but has prompted evaluation of recyclable face stocks that match container resin. UPM Raflatac launched a linerless construction in 2025 that cuts material waste by 15% and lowers freight costs, appealing to sustainability-focused manufacturers.

Geography Analysis

North America held 45.85% of the medical device labeling market share in 2025, anchored by FDA UDI enforcement and GUDID synchronization requirements. The agency issued 14 warning letters in 2024 for non-compliance, targeting domestic and foreign manufacturers. Canada aligned its Medical Devices Regulations with FDA standards in 2024 and introduced mandatory label-related adverse-event reporting, compelling bilingual French-English labeling for Quebec. Mexico's COFEPRIS adopted UDI in 2025, creating a North American regulatory bloc that simplifies design yet imposes trilingual English-French-Spanish obligations for USMCA distribution.

Europe navigates MDR and IVDR transitions that mandate local-language instructions in Germany, France, Italy, Spain, and Poland, fragmenting label SKUs. The UK's UKCA marking, mandatory in 2024, requires separate labels for Great Britain versus Northern Ireland, which follows EU MDR, forcing parallel inventories. Regulation 2025/1234, effective July 2025, permits eIFU for professional devices but retains QR-code and URL requirements for each language, multiplying designs without reducing print costs.

Asia-Pacific is forecast to grow at 6.08% through 2031, the fastest regional CAGR. China completed UDI rollout in 2024, mandating Class I device identifiers in the NMPA database and driving dual-format barcode adoption. India's Production Linked Incentive scheme channels USD 1.4 billion into domestic manufacturing, favoring local label procurement and attracting multinational converter investment in Pune, Ahmedabad, and Chennai. Japan's PMDA accepted eIFU in 2024, aligning with FDA and EU precedents, yet retained strict on-label Japanese-language and kanji legibility standards. Middle East and Africa, South America, and smaller Asia-Pacific markets collectively represented notable share of revenue in 2025. Brazil's ANVISA published UDI guidelines in 2024, requiring GS1 or HIBC coding for Class III and IV devices by 2026. Australia's TGA harmonized UDI requirements with FDA and EU frameworks in 2024, simplifying Pacific-region design, while South Korea's MFDS mandated Korean-language labeling for imports.

- All4Labels Group

- Avery Dennison

- Beontag

- Brady Corporation

- Brook & Whittle

- CCL Industries

- Cisper Electronics

- CleanMark Labels

- Domino Printing Sciences

- Fortis Solutions Group

- HERMA GmbH

- Inovar Packaging Group

- LINTEC Corporation

- Loftware

- Propper Manufacturing

- Resource Label Group

- RFiD Discovery

- SATO Holdings

- Schreiner Group

- Taylor Corporation

- UPM Raflatac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global UDI Mandates and Database Submissions Expand Label Data and Dual-Format Barcode Requirements

- 4.2.2 MDR/IVDR Multi-Language and Translation Rules Increase Label SKUs And Content Volume

- 4.2.3 Rising Home-Use/Wearable and POCT Devices Elevate Demand for Durable, Patient-Friendly Labels

- 4.2.4 Increased Recall and Track-And-Trace Needs Accelerate 2D Barcode-Rich UDI Labeling

- 4.2.5 Adoption Of RFID/NFC Smart Labels for Item-Level Traceability in Surgical Kits and Implants

- 4.2.6 Sterile Processing Workflows Boost Usage of Indicator Labels and Documentation (SPD/CSSD)

- 4.3 Market Restraints

- 4.3.1 Compliance Burden and Frequent Regulatory Updates Raise Cost/Time-To-Market for Labelers

- 4.3.2 Fragmented Label Converting Landscape Intensifies Pricing Pressure and Margin Squeeze

- 4.3.3 Direct Part Marking (Permanent UDI) Displaces Some External Labels for Reusable Instruments

- 4.3.4 eIFU Adoption Reduces Paper Booklet/Leaflet Labeling for Professional-Use Devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Label Type

- 5.1.1 Pressure-sensitive

- 5.1.2 Glue-applied

- 5.1.3 Shrink sleeves

- 5.1.4 In-mold labels

- 5.2 By Application

- 5.2.1 Disposable consumables

- 5.2.2 Monitoring & diagnostic equipment

- 5.2.3 Therapeutic & surgical instruments

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 All4Labels Group

- 6.3.2 Avery Dennison

- 6.3.3 Beontag

- 6.3.4 Brady Corporation

- 6.3.5 Brook & Whittle

- 6.3.6 CCL Industries

- 6.3.7 Cisper Electronics

- 6.3.8 CleanMark Labels

- 6.3.9 Domino Printing Sciences

- 6.3.10 Fortis Solutions Group

- 6.3.11 HERMA GmbH

- 6.3.12 Inovar Packaging Group

- 6.3.13 LINTEC Corporation

- 6.3.14 Loftware

- 6.3.15 Propper Manufacturing

- 6.3.16 Resource Label Group

- 6.3.17 RFiD Discovery

- 6.3.18 SATO Holdings

- 6.3.19 Schreiner Group

- 6.3.20 Taylor Corporation

- 6.3.21 UPM Raflatac

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

全球自動高壓清洗機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球自動高壓清洗機市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 自主資料標註市場預測至2034年-按組件、標註類型、部署模式、組織規模、技術、最終用戶和地區分類的全球分析資料標註市場預測至2034年-按資料類型、標註方法、部署模式、標註類型、應用、最終使用者和地區分類的全球分析

自主資料標註市場預測至2034年-按組件、標註類型、部署模式、組織規模、技術、最終用戶和地區分類的全球分析資料標註市場預測至2034年-按資料類型、標註方法、部署模式、標註類型、應用、最終使用者和地區分類的全球分析 非洲和中東標籤市場(2026 年)

非洲和中東標籤市場(2026 年) 2026年全球容器用照片標籤市場報告智慧低溫運輸指示標籤和記錄器市場預測——全球產品類型、包裝形式、銷售管道、技術、應用、最終用戶和地區分析——2034年永續標籤市場預測至2034年—全球標籤類型、材料類型、黏合劑類型、應用、最終用途產業、分銷管道和區域分析

2026年全球容器用照片標籤市場報告智慧低溫運輸指示標籤和記錄器市場預測——全球產品類型、包裝形式、銷售管道、技術、應用、最終用戶和地區分析——2034年永續標籤市場預測至2034年—全球標籤類型、材料類型、黏合劑類型、應用、最終用途產業、分銷管道和區域分析 2026-2030年全球標籤市場

2026-2030年全球標籤市場 時間和溫度標籤市場:按類型、技術、標籤資訊、最終用戶和地區分類人工智慧資料標註市場預測至2034年-按資料類型、組件、部署模式、技術、最終使用者和地區分類的全球分析

時間和溫度標籤市場:按類型、技術、標籤資訊、最終用戶和地區分類人工智慧資料標註市場預測至2034年-按資料類型、組件、部署模式、技術、最終使用者和地區分類的全球分析