|

市場調查報告書

商品編碼

2063432

企業代理基礎設施:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Enterprise Agent Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

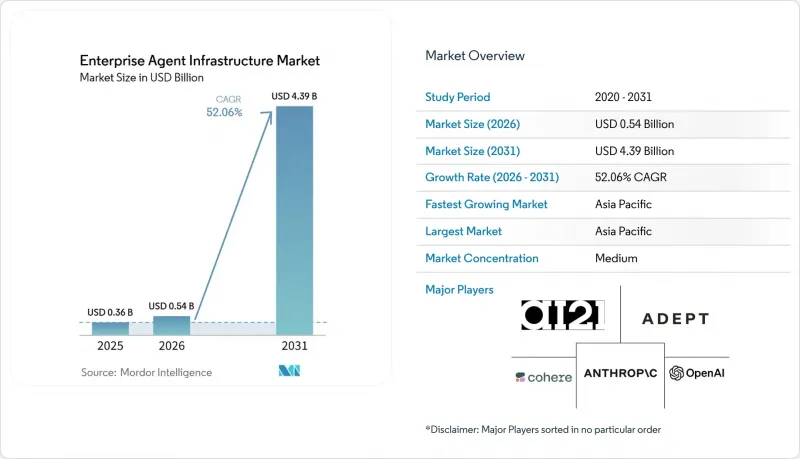

根據 Mordor Intelligence 預測,企業代理基礎設施市場規模預計將在 2025 年達到 3.6 億美元,2026 年達到 5.4 億美元,到 2031 年達到 43.9 億美元。預計從 2026 年到 2031 年,該市場將以 52.06% 的複合年成長率成長。

本報告按部署模式(雲端、本地部署、混合部署)、組件(軟體和服務)、企業規模(大型企業、中小企業)、產業(IT與電信、銀行、金融服務和保險、醫療保健與生命科學、零售與電子商務、製造業及其他)和地區進行細分。市場預測以美元計價。

全球企業代理基礎設施市場趨勢與洞察

快速採用雲端原生人工智慧基礎設施

企業正在將代理工作負載遷移到更具彈性的雲端環境,從而引進週期從幾季縮短到幾週。 Databricks 預計到 2025 年,其年收入將超過 40 億美元,其中超過 10 億美元將來自其人工智慧產品,這些產品在一個統一的平台上整合了編配、向量儲存和管治。公共雲端供應商現在提供 GPU 存取、託管向量資料庫和監控儀表板,這增加了轉換成本並加深了供應商鎖定。在無法完全依賴公共雲端的受監管產業中,混合雲架構正在被採用,這反映出各產業基礎設施策略的兩極化。微服務架構支援分階段部署,IT 團隊可以在擴展規模之前檢驗投資報酬率,從而加速其普及應用。

互動式人工智慧的應用正在快速成長。

互動式智慧體已從基礎聊天機器人發展成為能夠執行交易和協調後端系統的情境感知編配。 Anthropic 的「Claude Code」在 2026 年 2 月的年收入突破 25 億美元,其企業訂閱量在不到兩個月的時間內翻了四倍。歐洲企業正在尋求在地化的替代解決方案,例如 Mistral 的 Magistral 模型,以滿足有關資料主權的監管要求。插件式「Claude Cowork」的出現引發了傳統軟體股票的大規模拋售,因為投資者意識到自主對話式智慧體可能會蠶食傳統的 SaaS 收入來源。如今,各組織正在根據推理品質、上下文視窗長度、延遲和每百萬代幣成本來評估智慧體平台。

計算成本和能耗高

與一次性模型訓練相比,持續運作的智慧體通常具有更高的推理成本,這給IT預算帶來了壓力。隨著企業運作持續運作,預計日本資料中心將使國內電力需求增加高達20%。模型供應商正積極降價應對,例如Mistral模型的價格降至每百萬代幣2美元(相比之下,GPT-4o模型的價格為5美元),這使得多模型路由成為一個極具吸引力的選擇。一些組織報告稱,透過將Mistral模型用於日常推理,並與用於複雜任務的高階模型結合,成本節省高達65%。然而,GPU短缺和能源價格上漲仍然限制了可擴展性。此外,日本都市區土地稀缺和冷卻能力不足意味著超大規模資料中心將遠離最終用戶,導致延遲方面的權衡,並可能限制某些應用場景。

細分市場分析

預計到2026年,混合架構將在企業代理基礎設施市場佔據更大的市場佔有率,並持續以27.64%的複合年成長率成長至2031年。即使到了2025年,雲端仍然佔據企業代理基礎設施市場64.49%的佔有率,這反映了Pinecone的無伺服器推理服務和Databricks整合堆疊的吸引力。國防和生命科學等受監管行業需要本地控制來管理敏感數據,同時也需要用於訓練和推理的突發容量。

混合模式允許企業將敏感工作負載保留在私有資料中心,同時將運算密集型任務卸載到公共雲端GPU,從而最佳化成本和合規性。 Cohere 為 Oracle 和 Dell 等客戶提供的「本地優先」策略,以及其成功完成的 5 億美元資金籌措,都表明投資者堅信自主部署將繼續發揮至關重要的作用。富士通和 NVIDIA 在 CPU-GPU 堆疊方面的合作,凸顯了他們致力於將本地管治與雲端的突發彈性相結合的決心。

預計服務市場將以 26.23% 的複合年成長率成長,這反映出各行各業對整合、微調和可觀測性解決方案的需求日益成長。推動這一成長的因素是企業尋求透過先進的服務交付來提高營運效率並簡化工作流程。同時,到 2025 年,軟體將佔企業代理基礎設施市場規模的 44.39%,提供諸如編配框架、向量資料庫和 API 存取等關鍵工具,這些工具對於無縫營運和資料管理至關重要。

Accenture旗下擁有25,000名員工的Databricks業務集團,凸顯了系統整合商將管治、培訓和持續最佳化等附加服務與軟體授權捆綁銷售的趨勢。這種方式使企業能夠在滿足複雜部署需求的同時,最大限度地發揮軟體投資的價值。例如,Databricks的AppKit透過減少樣板程式碼簡化了開發,但受監管的部署仍然需要專業服務來確保合規性和效率。越來越多的企業選擇託管服務,以實現平穩升級、安全的資料管道和最佳化的搜尋參數。這些服務使企業內部團隊能夠專注於發揮自身專長,而無需花費時間管理複雜的平台基礎設施,最終推動更好的績效和創新。

區域分析

預計到2025年,北美將佔據企業代理基礎設施市場25.82%的佔有率。這主要得益於豐富的GPU供應、聯邦政府的採購獎勵以及創業投資的集中。企業在利用雲端運算的經濟效益的同時,也面臨著不斷上漲的電力成本,這促使超大規模資料中心業者資料中心營運商將資料中心遷至北美大陸成本較低的地區。監管,例如各州的隱私法,迫使企業實施精細化的資料居住管理。這增加了複雜性,並最終將刺激對合規代理框架的需求。

以日本、中國、印度和韓國為主導的亞太地區預計到2031年將以24.26%的複合年成長率成長。 2026年3月的一項調查發現,日本年收入超過1兆日圓(約67億美元)的企業中,80%已採用生成式人工智慧,顯示自動化已成為一種自上而下的趨勢。儘管日本的資料中心容量需要在2030年加倍,到2040年成長九倍,但電力基礎設施擴張緩慢可能會造成基礎設施瓶頸,從而阻礙成長。在印度和東南亞國家,為了滿足不同語言市場的需求,多語言模式正在被採用,並得到了來自美國和中東投資者的大規模投資支持。

歐洲的人工智慧格局受「人工智慧法」的影響,該法規定了審計追蹤和透明度要求。雖然合規負擔可能會延緩早期採用,但明確的指導方針最終將降低大型企業的採購風險。 Mistral 和 Aleph Alpha 等供應商正透過資料居住和可解釋性來凸顯其符合區域監管要求的解決方案。在中東和非洲地區,他們正利用主權雲夥伴關係關係,特別是 OpenAI 和 G42 之間的合作,來開拓阿拉伯語市場。同時,他們在南美的業務主要集中在巴西和阿根廷,在那裡,對話式代理商正在實現葡萄牙語和西班牙語客戶支援的自動化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速採用雲端原生人工智慧基礎設施

- 對話式人工智慧的應用正在快速成長。

- 加大對自主IT代理的投資

- 向量資料庫互通性標準的出現

- 受監管產業合規代理框架的興起

- 用於實現邊緣代理的設備端 AI 加速器

- 市場限制因素

- 計算成本和能耗高

- 資料隱私法規限制了編配。

- 代理協議標準的破壞

- 多方協調和安全的人員短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 按組件

- 軟體

- 服務

- 按公司規模

- 大公司

- 小型企業

- 按行業分類

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 能源公用事業

- 政府/公共部門

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OpenAI OpCo, LLC

- Anthropic PBC

- Cohere Inc.

- AI21 Labs Ltd.

- Adept AI Labs, Inc.

- Reka AI, Inc.

- LangChain Inc.

- Pinecone Systems, Inc.

- Weaviate BV

- Hugging Face SAS

- Mistral AI SAS

- Aleph Alpha GmbH

- Stability AI Ltd.

- Scale AI, Inc.

- Anyscale, Inc.

- Replit, Inc.

- LlamaIndex LLC

- Contextual AI, Inc.

- Runway AI, Inc.

- Databricks, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the enterprise agent infrastructure market size is projected to be USD 0.36 billion in 2025, USD 0.54 billion in 2026, and reach USD 4.39 billion by 2031, growing at a CAGR of 52.06% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and ECommerce, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Agent Infrastructure Market Trends and Insights

Rapid Adoption of Cloud-Native AI Infrastructure

Enterprises are lifting and shifting agent workloads into elastic cloud environments, reducing deployment cycles from quarters to weeks. Databricks surpassed USD 4 billion annualized revenue in 2025, with more than USD 1 billion coming from AI products that bundle orchestration, vector storage, and governance on a unified platform. Public cloud providers now offer GPU access, managed vector databases, and monitoring dashboards, creating switching costs that deepen vendor lock-in. Regulated sectors that cannot rely solely on public clouds are embracing hybrid stacks, reflecting a bifurcation of infrastructure strategies by industry. Microservice architectures enable incremental rollouts, allowing IT teams to validate return on investment before scaling and thereby accelerating adoption.

Surge in Conversational AI Deployments

Conversational agents have evolved from basic chatbots into context-aware assistants capable of executing transactions and orchestrating back-end systems. Anthropic's Claude Code passed a USD 2.5 billion run rate in February 2026, with enterprise subscriptions quadrupling in less than two months. European firms are pursuing regional alternatives, such as Mistral's Magistral models, to meet data-sovereignty mandates. The debut of Claude Cowork with plug-ins triggered a broad sell-off in legacy software stocks as investors recognized that autonomous conversational agents could cannibalize traditional SaaS revenue streams. Organizations now benchmark agent platforms on reasoning quality, context-window length, latency, and cost per million tokens.

High Compute Costs and Energy Consumption

Continuous-running agents often incur higher inference expenses than one-time model training, tightening IT budgets. Japanese data centers will lift national electricity demand by up to 20% as enterprises run always-on agents. Model vendors are responding through aggressive price cuts, such as Mistral's USD 2 per million tokens versus GPT-4o's USD 5, making multi-model routing attractive. Organizations report 65% cost savings by combining Mistral for routine inference with premium models for complex tasks, yet GPU scarcity and rising energy prices still constrain scalability. Japan's shortage of urban land and cooling capacity is pushing hyperscale facilities far from end users, creating latency trade-offs that could limit certain use cases.

Other drivers and restraints analyzed in the detailed report include:

- Increased Investment in Autonomous IT Agents

- Emergence of Vector Database Interoperability Standards

- Data Privacy Regulations Limiting Orchestration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures accounted for a growing slice of the Enterprise Agent Infrastructure market in 2026 and are forecast to expand at a 27.64% CAGR through 2031. Cloud still represented 64.49% of the Enterprise Agent Infrastructure market share in 2025, reflecting the appeal of serverless inference services from Pinecone and unified stacks from Databricks. Regulated sectors such as defense and life sciences require on-premise control for sensitive data, yet they also need burst capacity for training and inference.

Hybrid models let enterprises keep confidential workloads in private data centers while offloading compute-intensive tasks to public-cloud GPUs, optimizing both cost and compliance. Cohere's on-premises-first strategy with customers Oracle and Dell, and its USD 500 million raise, signal investor conviction that sovereignty-friendly deployments will remain pivotal. Fujitsu's partnership with NVIDIA on CPU-GPU stacks underscores efforts to blend on-premise governance with cloud-burst elasticity.

Services are projected to expand at a 26.23% CAGR, reflecting the growing need for integration, fine-tuning, and observability solutions across industries. This growth is driven by enterprises seeking to enhance operational efficiency and streamline workflows through advanced service offerings. Software, on the other hand, accounted for 44.39% of the Enterprise Agent Infrastructure market size in 2025, providing essential tools such as orchestration frameworks, vector databases, and API access, which are critical for enabling seamless operations and data management.

Accenture's 25,000-person Databricks business group highlights the trend of system integrators bundling software licenses with additional services like governance, training, and continuous optimization. This approach ensures that enterprises can maximize the value of their software investments while addressing complex deployment requirements. For instance, Databricks' AppKit simplifies development by reducing boilerplate code; however, regulated deployments still necessitate professional services to ensure compliance and efficiency. Enterprises are increasingly opting for managed services that facilitate smooth upgrades, secure data pipelines, and optimize retrieval parameters. These services allow internal teams to concentrate on leveraging their domain expertise rather than managing the intricacies of platform infrastructure, ultimately driving better outcomes and innovation.

Geography Analysis

North America commanded 25.82% of the Enterprise Agent Infrastructure market in 2025, benefiting from dense GPU availability, federal procurement incentives, and venture capital concentration. Enterprises leverage favorable cloud economics but face rising electricity costs, prompting hyperscalers to locate data centers in lower-cost regions within the continent. Regulatory scrutiny, such as state-level privacy statutes, forces organizations to implement granular data-residency controls that add complexity yet ultimately stimulate demand for compliance-ready agent frameworks.

Asia-Pacific is forecast to expand at a 24.26% CAGR through 2031, propelled by Japan, China, India, and South Korea. A March 2026 survey reported that 80% of Japanese firms with revenue above JPY 1 trillion (USD 6.7 billion approximately) had deployed generative AI, signaling top-down mandates for automation. Japan's data-center capacity must double by 2030 and increase ninefold by 2040, exposing infrastructure bottlenecks that could moderate growth if power upgrades lag. India and Southeast Asian economies adopt multilingual models to serve diverse linguistic markets, supported by hyperscale investments from U.S. and Middle Eastern investors.

Europe's outlook is shaped by the AI Act, which imposes audit-trail and transparency requirements. While compliance overhead slows early adoption, clear guardrails ultimately de-risk procurement for large enterprises. Vendors such as Mistral and Aleph Alpha position themselves as regionally compliant options, differentiating on data residency and explainability. The Middle East and Africa region leverages sovereign cloud partnerships, most notably the OpenAI-G42 alliance, to serve Arabic-language markets, while South America's activity centers on Brazil and Argentina, where conversational agents automate Portuguese and Spanish customer support.

- OpenAI OpCo, LLC

- Anthropic PBC

- Cohere Inc.

- AI21 Labs Ltd.

- Adept AI Labs, Inc.

- Reka AI, Inc.

- LangChain Inc.

- Pinecone Systems, Inc.

- Weaviate BV

- Hugging Face SAS

- Mistral AI SAS

- Aleph Alpha GmbH

- Stability AI Ltd.

- Scale AI, Inc.

- Anyscale, Inc.

- Replit, Inc.

- LlamaIndex LLC

- Contextual AI, Inc.

- Runway AI, Inc.

- Databricks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Native AI Infrastructure

- 4.2.2 Surge in Conversational AI Deployments

- 4.2.3 Increased Investment in Autonomous IT Agents

- 4.2.4 Emergence of Vector Database Interoperability Standards

- 4.2.5 Rise of Compliance-Ready Agent Frameworks for Regulated Industries

- 4.2.6 On-Device AI Accelerators Enabling Edge Agents

- 4.3 Market Restraints

- 4.3.1 High Compute Costs and Energy Consumption

- 4.3.2 Data Privacy Regulations Limiting Orchestration

- 4.3.3 Fragmentation of Agent Protocol Standards

- 4.3.4 Scarcity of Talent for Multi-Agent Alignment and Safety

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and eCommerce

- 5.4.5 Manufacturing

- 5.4.6 Energy and Utilities

- 5.4.7 Government and Public Sector

- 5.4.8 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI OpCo, LLC

- 6.4.2 Anthropic PBC

- 6.4.3 Cohere Inc.

- 6.4.4 AI21 Labs Ltd.

- 6.4.5 Adept AI Labs, Inc.

- 6.4.6 Reka AI, Inc.

- 6.4.7 LangChain Inc.

- 6.4.8 Pinecone Systems, Inc.

- 6.4.9 Weaviate BV

- 6.4.10 Hugging Face SAS

- 6.4.11 Mistral AI SAS

- 6.4.12 Aleph Alpha GmbH

- 6.4.13 Stability AI Ltd.

- 6.4.14 Scale AI, Inc.

- 6.4.15 Anyscale, Inc.

- 6.4.16 Replit, Inc.

- 6.4.17 LlamaIndex LLC

- 6.4.18 Contextual AI, Inc.

- 6.4.19 Runway AI, Inc.

- 6.4.20 Databricks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球工作流程市場報告

2026年全球工作流程市場報告 勞動力編配平台市場預測至2034年-按平台類型、部署模式、技術、應用、最終用戶和地區分類的全球分析人工智慧市場預測:智慧流程自動化的全球分析(至2034年),涵蓋流程、組件、技術、應用、最終用戶和區域。智慧流程自動化平台市場預測至2034年—按組件、技術、部署模式、應用、最終用戶和地區分類的全球分析2026年全球多模型編配市場報告

勞動力編配平台市場預測至2034年-按平台類型、部署模式、技術、應用、最終用戶和地區分類的全球分析人工智慧市場預測:智慧流程自動化的全球分析(至2034年),涵蓋流程、組件、技術、應用、最終用戶和區域。智慧流程自動化平台市場預測至2034年—按組件、技術、部署模式、應用、最終用戶和地區分類的全球分析2026年全球多模型編配市場報告 2026-2030年全球AI GPU編配平台市場2026 年全球大規模語言模型 (LLM) 訪問中介 (AB) 市場報告2026年全球大型語言模型閘道市場報告

2026-2030年全球AI GPU編配平台市場2026 年全球大規模語言模型 (LLM) 訪問中介 (AB) 市場報告2026年全球大型語言模型閘道市場報告 AI編配市場:按組件、技術、部署模式、組織規模和最終用途分類-2026-2032年全球市場預測2026年全球函數呼叫編配市場報告

AI編配市場:按組件、技術、部署模式、組織規模和最終用途分類-2026-2032年全球市場預測2026年全球函數呼叫編配市場報告