|

市場調查報告書

商品編碼

2063370

磷化氫燻蒸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Phosphine Fumigation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

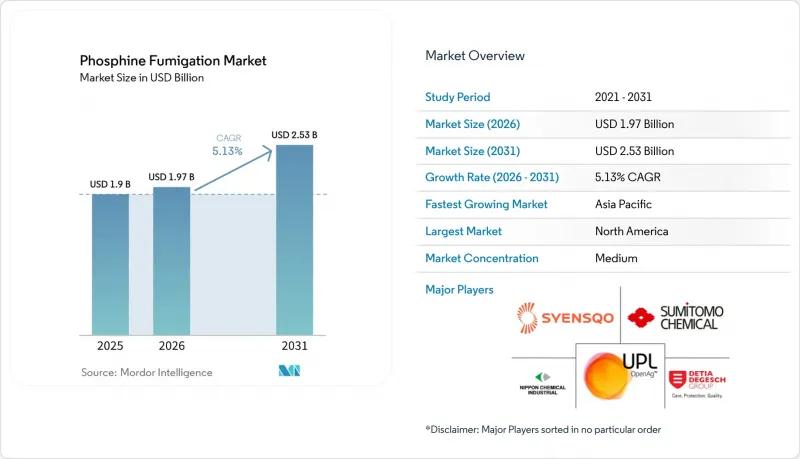

據 Mordor Intelligence 稱,2025 年磷化氫燻蒸市場價值 19 億美元,預計將從 2026 年的 19.7 億美元成長到 2031 年的 25.3 億美元,2026 年至 2031 年的複合年成長率為 4.9%。

本報告按產品類型(磷化鋁、磷化鎂及其他)、形態(固體、液態及其他)、作物類型(穀物、油籽及其他)、倉儲設施(農場筒倉及其他)、最終用戶(農場糧食儲存業者及其他)和地區(北美、歐洲及其他)進行細分。市場預測以美元計價。

全球磷化氫燻蒸市場趨勢及洞察

擴大糧倉及散裝商品儲存能力

筒倉和散裝儲存能力的擴張直接推動了磷化氫燻蒸的需求,因為定期庫存保護的需求日益成長。新建的穀倉、儲存設施和集中式倉庫需要定期進行燻蒸處理,以確保長期存放的安全。對於那些正轉向以糧食安全為重點的有序儲存系統的地區而言,這一趨勢至關重要。聯合國糧食及農業組織(糧農組織)強調,儲存基礎設施對於糧食系統的韌性至關重要,這進一步凸顯了專業燻蒸的必要性。此外,新設施採用更嚴格的氣密性標準,促進了鋼瓶氣體和受監控噴灑方法的使用,進一步鞏固了磷化氫燻蒸市場。

加強糧食和油籽出口的植物檢疫合規性

植物檢疫標準的日益嚴格增加了磷化氫燻蒸市場對經認證燻蒸的需求。進口國現在要求提供詳細的文件、熟練的工人以及遵守既定程序的證明。 《國際植物保護公約》(IPPC)制定了燻蒸作為植物檢疫措施的標準,以確保國際貿易的一致性。美國農業部(USDA)農業市場服務局透過其燻蒸手冊執行這些標準,不合規可能導致重新加工、延誤或拒收貨物。因此,磷化氫燻蒸已成為貿易流通中必不可少的常規要求,從而支撐了穩定的市場需求。

對工人接觸、認證和燻蒸等方面的文件記錄有嚴格的要求。

磷化氫燻蒸市場受到嚴格的工人接觸法規和許可要求的阻礙,例如美國聯邦法規第40篇第171條的規定,該條強制要求進行培訓、記錄保存和監督。同樣,德國也實施嚴格的監管,聯邦風險評估實驗室報告稱,2022年至2024年間共發生109起磷化鋁中毒事件。這些法規增加了合規成本,使得在糧食處理高峰期難以找到合格的工人,並最終導致受監管地區的市場成長放緩,儘管市場需求不斷成長。

細分市場分析

預計2025年,磷化鋁將在磷化氫燻蒸市場佔據54%的市場佔有率,成為市場主導產品。這主要得益於其成本低廉、獲得監管部門批准以及在各種儲存環境中易於操作。磷化鋁在農場級倉儲設施、商業倉庫和港口相關糧食設施中的廣泛應用,最大限度地降低了替代風險;此外,操作人員長期以來對其使用的熟悉程度也進一步鞏固了其市場地位。

預計2026年至2031年間,磷化鎂的複合年成長率將達到5.95%,其成長勢頭強勁,因為它能夠滿足貨櫃燻蒸和檢疫作業對更短處理週期的需求。另一方面,磷化鈣的應用仍局限於小眾領域,市場仍依賴磷化鋁進行大量生產。為了佐證這一趨勢,《農業》(Agriculture)雜誌2025年的一項研究強調了Detia Freyberg GmbH公司的「磷化氫抗性測試」是早期檢測主要甲蟲物種抗性的關鍵工具。這項診斷技術的進步增強了業界最佳化磷化氫使用的能力,確保了磷化鋁等成熟產品對市場穩定和成長的重要性。

截至2025年,固態製劑將佔據最大的市場佔有率,佔磷化氫燻蒸市場佔有率的59.2%。其領先地位得益於其易用性、高效的應用以及對加工設備的低投資要求。此外,中國LS/T 1201-2020和德國TRGS 512等既定的糧食儲存標準也進一步鞏固了這一地位,這些標準持續推薦常規使用片劑和顆粒劑。液體製劑是成長最快的細分市場,預計2026年至2031年將以6.2%的複合年成長率成長。這主要歸功於倉儲業者日益重視磷化氫控制釋放、更清潔的加工流程以及在經審核的食品級設施中更高的合規性。

劑型細分市場的剩餘佔有率由粉末製劑佔據,儘管其市場佔有率較小,但仍佔據重要地位。這些產品主要用於表面塗覆和滲透到片劑或液體製劑難以有效放置的結構中(例如平坦的倉庫地面、狹窄的設備縫隙等)。它們的應用仍然較為專業化,旨在滿足特定儲存佈局和設備條件下的加工需求。隨著市場的發展,這種結構表明固體製劑仍然是需求的基礎,液體製劑的成長速度最快,而粉末製劑則繼續彌補其他劑型無法完全解決的某些操作難題。

區域分析

到2025年,北美將佔據磷化氫燻蒸市場35.8%的佔有率。這主要得益於美國的強勁成長,美國擁有大型的平板式倉儲設施、圓柱形料倉和終端筒倉,能夠支援大規模、連續的加工處理。此外,美國嚴格的施藥人員認證和燻蒸程序法規也維持了對專業服務供應商和更嚴格管控的氣體供應形式的需求。加拿大仍然是穩定的第二大市場,在歷史低點的阻力下,傳統的加工方式依然表現良好。在墨西哥,隨著植物檢疫加工認證在正規的糧食處理和倉儲作業中日益重要,市場需求也穩定成長。

亞太地區預計將成為成長最快的地區,2026年至2031年的複合年成長率將達到6.8%,透過系統性地擴大倉儲設施以及在印度、中國和東南亞建立標準化的加工流程,推動全球糧食加工量的成長。為加強國家生物安全並應對日益嚴重的病蟲害抗藥性問題,中國國家糧食儲備公司(中糧集團)計劃在2024年底前完成旗下900個倉庫的數位化基礎設施現代化改造,實現自動化封閉回路型磷化氫燻蒸和即時氣體監測的標準化。這凸顯了該公司的重要性。儘管澳洲擁有專業的市場,但仍面臨抗藥性挑戰;而東南亞則受益於不斷擴建的倉儲基礎設施,確保了農產品出口的安全處理。

預計2026年至2031年間,歐洲和非洲將維持穩定成長,這主要得益於歐洲對合規導向專業服務的重視,以及非洲糧食安全措施和倉儲設施升級。中東地區透過加強進口倉儲系統,進一步加速了這一趨勢;而以巴西和阿根廷主導的南美洲,則繼續在大規模糧食和油籽倉儲網路的定期燻蒸方面發揮著至關重要的作用。在全部區域,為了滿足不斷變化的監管和營運需求,全球範圍內向有組織的倉儲和先進燻蒸技術的轉變已日益明顯。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大糧倉及散裝商品儲存能力

- 加強糧食和油籽出口的植物檢疫規定

- 在農業檢疫程序中,使用溴甲烷作為替代方案正在逐步推廣。

- 減少穀物、豆類和油籽收穫後損失的需求日益成長。

- 在糧食儲存中引入磷化氫鋼瓶、循環利用和數位氣體監測

- 專注於農場燻蒸方案和糧食品質保證工作流程。

- 市場限制因素

- 對工人接觸、認證和燻蒸等方面的文件記錄有嚴格的要求。

- 主要儲糧和種子害蟲對磷化氫的抗性增強

- 透過密封儲存和非化學糧食保藏方法減少加工頻率。

- 限制在有機農業和殘留物問題嚴重的農業領域使用燻蒸劑。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 磷化鋁

- 磷化鎂

- 磷化鈣

- 按形式

- 固體的

- 液體

- 粉末

- 按作物類型

- 穀類和穀類食品

- 油籽

- 豆科植物

- 經濟作物及人工林產品

- 透過倉儲設施

- 農場筒倉和糧食儲存

- 商業散裝筒倉

- 平板堆疊式倉庫和袋裝貨物倉庫

- 糧倉和臨時糧食儲存系統

- 出口貨櫃

- 最終用戶

- 農糧倉儲營運商

- 糧食升降機和散裝貨物處理設施

- 農業倉庫和貨物存儲公司

- 種子企業與種子加工廠

- 農產品出口商和檢疫服務提供商

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- UPL Limited

- Detia Freyberg GmbH(Detia Degesch Group)

- Syensqo SA

- Nippon Chemical Industrial Co., Ltd.

- Sumitomo Chemical Company Limited

- Douglas Products and Packaging Company, LLC(Brightstar Capital Partners)

- Intech Organics Limited

- Rentokil Initial plc

- National Fumigants Pty Ltd.

- Ikeda Kogyo Co., Ltd.

- Specialty Gases Pty Ltd.

- Fumigation Service and Supply, Inc.

- Industrial Fumigant Company, LLC

- Agri-Treat Solutions Pty Ltd.

- Sandhya Organic Chemicals Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the phosphine fumigation market size is valued at USD 1.9 billion in 2025 and is anticipated to grow from USD 1.97 billion in 2026 to USD 2.53 billion by 2031, registering a CAGR of 4.9% through 2026 to 2031.

This report is Segmented by Product Type (Aluminum Phosphide, Magnesium Phosphide, and More), by Form (Solid, Liquid, and More), by Crop Type (Cereals, Oilseeds, and More), by Storage Structure (Farm Silos and Grain Bins, and More), by End-User (On-Farm Grain Storage Operators, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Phosphine Fumigation Market Trends and Insights

Expansion of Grain Silo and Bulk Commodity Storage Capacity

The expansion of silo and bulk storage capacity directly drives the demand for phosphine fumigation by increasing the need for regular inventory protection. New grain elevators, reserve facilities, and centralized warehouses require consistent treatment cycles to ensure long-term storage safety. This trend is critical in regions focusing on food security and transitioning to organized storage systems. The Food and Agriculture Organization of the United Nations (FAO) highlights storage infrastructure as vital for food system resilience, further validating the need for professional fumigation. Moreover, the adoption of tighter sealing standards in new facilities enhances the use of cylinderized gas and monitored application methods, strengthening the phosphine fumigation market.

Tighter Phytosanitary Compliance for Grain and Oilseed Exports

Stricter phytosanitary compliance is driving the need for certified treatment in the phosphine fumigation market. Importing countries now require detailed documentation, skilled operators, and proof of adherence to established procedures. The International Plant Protection Convention (IPPC) sets the standards for fumigation as a phytosanitary measure, ensuring consistency in international trade. The United States Department of Agriculture (USDA) Agricultural Marketing Service enforces these standards through its fumigation handbook, with non-compliance leading to re-treatment, delays, or cargo rejection. As a result, phosphine fumigation has become an essential and routine requirement in trade flows, reinforcing stable market demand.

Stringent Operator Exposure, Certification, and Fumigation Documentation Requirements

The phosphine fumigation market is constrained by strict worker exposure regulations and licensing requirements, such as those under Title 40 Code of Federal Regulations Part 171 in the United States, which mandate training, record-keeping, and supervision. Similarly, Germany enforces strict oversight, with 109 cases of aluminum phosphide poisoning reported by the Federal Institute for Risk Assessment between 2022 and 2024. These regulations increase compliance costs and reduce the availability of certified workers during seasonal peaks in grain handling, ultimately slowing market growth in regulated regions despite rising demand.

Other drivers and restraints analyzed in the detailed report include:

- Ongoing Methyl Bromide Substitution in Agricultural Quarantine Treatments

- Rising Need to Reduce Post-Harvest Losses in Cereals, Pulses, and Oilseeds

- Rising Phosphine Resistance in Major Stored Grain and Seed Pests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum phosphide, held the largest share of 54% of the phosphine fumigation market in 2025, remains the dominant product due to its low cost, regulatory acceptance, and ease of handling in various storage environments. Its widespread use in farm-level storage, commercial warehouses, and port-linked grain facilities ensures minimal replacement risk, while operator familiarity with its long-standing application further solidifies its position.

Magnesium phosphide, with a projected CAGR of 5.95% during 2026-2031, is gaining momentum as it addresses the need for short turnaround times in container fumigation and quarantine operations. While calcium phosphide serves niche applications, the market continues to rely on aluminum phosphide for high-volume usage. Supporting this trend, a 2025 study in Agriculture highlighted the Phosphine Tolerance Test by Detia Freyberg GmbH as a key tool for early detection of resistance in major beetle species. This diagnostic advancement strengthens the industry's ability to optimize phosphine use, ensuring established products like Aluminum Phosphide remain integral to market stability and growth.

Solid formulations held the largest share and accounted for 59.2% of the phosphine fumigation market share in 2025, maintaining their lead due to ease of use, efficient distribution, and low capital requirements for treatment setups. This position is also reinforced by established grain storage standards such as China's LS/T 1201-2020 and Germany's TRGS 512, which continue to support the routine use of tablets and pellets. Liquid formulations are the fastest-growing segment, projected to expand at a 6.2% CAGR during 2026-2031, as storage operators increasingly value controlled phosphine release, cleaner treatment processes, and stronger compliance performance in audited food-grade facilities.

The remaining share of the form segment comes from powder formulations, which serve a smaller but still relevant role in the market. These products are mainly used in surface dusting and in structural penetration areas where tablets or liquid systems are harder to place effectively, including flat warehouse floors and narrow equipment voids. Their use remains more specialized because they address treatment needs that are limited to certain storage layouts and equipment conditions. As the market evolves, this structure shows that while solid products still anchor volume demand and liquid systems capture the fastest growth, powders continue to support specific operational gaps that other formats do not fully address.

Geography Analysis

In 2025, North America held 35.8% of the phosphine fumigation market share, driven by the United States, where flat storage, cylindrical bins, and terminal silos support large recurring treatment volumes. The United States also operates under strict applicator certification and fumigation procedure rules, which sustain demand for specialized service providers and higher-control gas delivery formats. Canada remains a stable secondary center where conventional treatment still performs well under lower historical resistance pressure. Mexico adds steady demand as phytosanitary treatment certification gains importance in formal grain handling and warehouse operations

Asia-Pacific, the fastest-growing region with a projected CAGR of 6.8% during 2026-2031, leads global volumes due to expanding organized storage and formalized treatment practices in India, China, and Southeast Asia. To enforce strict national biosecurity and combat rising pest resistance, China's state grain reserve corporation, Sinograin, modernized its digital infrastructure across 900 depots in late 2024, standardizing automated, closed-loop phosphine fumigation and real-time gas monitoring, highlight its significance. Australia, despite its professionalized market, faces challenges with resistance, while Southeast Asia's growing warehousing infrastructure supports the reliable handling of agricultural exports.

Europe and Africa are projected to grow steadily during 2026-2031, with Europe emphasizing compliance-driven professional services and Africa benefiting from food security initiatives and storage upgrades. The Middle East adds to this trend by strengthening import storage systems, while South America, led by Brazil and Argentina, remains vital for recurring fumigation in large grain and oilseed storage networks. Together, these regions underscore the global shift toward organized storage and advanced fumigation practices to meet evolving regulatory and operational demands.

- UPL Limited

- Detia Freyberg GmbH (Detia Degesch Group)

- Syensqo SA

- Nippon Chemical Industrial Co., Ltd.

- Sumitomo Chemical Company Limited

- Douglas Products and Packaging Company, LLC (Brightstar Capital Partners)

- Intech Organics Limited

- Rentokil Initial plc

- National Fumigants Pty Ltd.

- Ikeda Kogyo Co., Ltd.

- Specialty Gases Pty Ltd.

- Fumigation Service and Supply, Inc.

- Industrial Fumigant Company, LLC

- Agri-Treat Solutions Pty Ltd.

- Sandhya Organic Chemicals Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of grain silo and bulk commodity storage capacity

- 4.2.2 Tighter phytosanitary compliance for grain and oilseed exports

- 4.2.3 Ongoing methyl bromide substitution in agricultural quarantine treatments

- 4.2.4 Rising need to reduce post-harvest losses in cereals, pulses, and oilseeds

- 4.2.5 Adoption of cylinderized phosphine, recirculation, and digital gas monitoring in grain storage

- 4.2.6 Professionalization of on-farm fumigation programs and grain quality assurance workflows

- 4.3 Market Restraints

- 4.3.1 Stringent operator exposure, certification, and fumigation documentation requirements

- 4.3.2 Rising phosphine resistance in major stored grain and seed pests

- 4.3.3 Hermetic storage and non-chemical grain protection alternatives reducing treatment frequency

- 4.3.4 Organic and residue-sensitive agricultural channels limiting fumigant use

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Aluminum Phosphide

- 5.1.2 Magnesium Phosphide

- 5.1.3 Calcium Phosphide

- 5.2 By Form

- 5.2.1 Solid

- 5.2.2 Liquide

- 5.2.3 Powder

- 5.3 By Crop Type

- 5.3.1 Cereals and Grains

- 5.3.2 Oilseeds

- 5.3.3 Pulses and Legumes

- 5.3.4 Commercial Crops and Plantation Produce

- 5.4 By Storage Structure

- 5.4.1 Farm Silos and Grain Bins

- 5.4.2 Commercial Bulk Silos

- 5.4.3 Flat Warehouses and Bagged Commodity Stores

- 5.4.4 Bunkers and Temporary Grain Storage Systems

- 5.4.5 Export Containers

- 5.5 By End User

- 5.5.1 On-farm Grain Storage Operators

- 5.5.2 Grain Elevators and Bulk Handlers

- 5.5.3 Agri-warehousing and Commodity Storage Companies

- 5.5.4 Seed Companies and Seed Processing Facilities

- 5.5.5 Agricultural Exporters and Quarantine Service Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 UPL Limited

- 6.4.2 Detia Freyberg GmbH (Detia Degesch Group)

- 6.4.3 Syensqo SA

- 6.4.4 Nippon Chemical Industrial Co., Ltd.

- 6.4.5 Sumitomo Chemical Company Limited

- 6.4.6 Douglas Products and Packaging Company, LLC (Brightstar Capital Partners)

- 6.4.7 Intech Organics Limited

- 6.4.8 Rentokil Initial plc

- 6.4.9 National Fumigants Pty Ltd.

- 6.4.10 Ikeda Kogyo Co., Ltd.

- 6.4.11 Specialty Gases Pty Ltd.

- 6.4.12 Fumigation Service and Supply, Inc.

- 6.4.13 Industrial Fumigant Company, LLC

- 6.4.14 Agri-Treat Solutions Pty Ltd.

- 6.4.15 Sandhya Organic Chemicals Pvt. Ltd.

7 Market Opportunities and Future Outlook

磷化氫燻蒸市場:按類型、形態、應用方法、技術、用途、最終用戶、通路分類,全球預測(2026-2032)

磷化氫燻蒸市場:按類型、形態、應用方法、技術、用途、最終用戶、通路分類,全球預測(2026-2032) 磷化氫燻蒸市場 - 全球產業規模、佔有率、趨勢、機會、預測:依燻蒸劑類型、作物類型、配方、應用、地區和競爭格局分類,2021-2031年

磷化氫燻蒸市場 - 全球產業規模、佔有率、趨勢、機會、預測:依燻蒸劑類型、作物類型、配方、應用、地區和競爭格局分類,2021-2031年