|

市場調查報告書

商品編碼

2063293

馬達驅動積體電路:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Motor Driver IC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

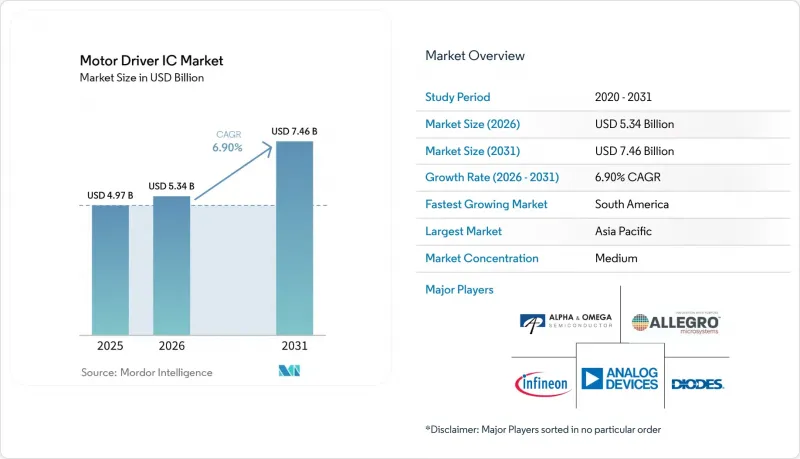

根據 Mordor Intelligence 預測,馬達驅動 IC 市場規模將從 2025 年的 49.7 億美元和 2026 年的 53.4 億美元成長到 2031 年的 74.6 億美元,2026 年至 2031 年的複合年成長率為 6.9%。

本報告按馬達類型(有刷直流驅動IC、碳化矽驅動IC等)、終端應用產業(汽車、工業自動化和機器人、醫療設備等)、電壓範圍(低於24V、25-48V、49-240V、高於240V)、半導體材料(矽、碳化矽(SiC)、Ga0V)、半導體材料(矽、碳化矽(SiC)、Ga0V)、半導體材料(矽、碳化矽(SiC)、N))。市場預測以美元(USD)為單位。

全球電機驅動IC市場趨勢與洞察

電動車主導對高壓驅動積體電路的需求

電池式電動車(BEV) 的生產正在迅速擴張,如今每個高壓牽引逆變器都需要能夠承受超過 175 度C結溫的多相閘極驅動器。碳化矽 (SiC) MOSFET 能夠在超出傳統 IGBT 驅動器的開關頻率下滿足此要求,從而使原始設備製造商 (OEM) 能夠減小冷卻迴路的面積和電纜橫截面積。加州和歐盟 (EU) 商用車的電氣化進一步拓展了市場機遇,因為 800V 電池組需要爬電距離超過 IEC 60664-1 標準的加強型隔離驅動器。儘管需求強勁,但經認證的 200mm SiC 晶圓的產能仍然緊張,導致前置作業時間超過六個月,裝置的平均售價 (ASP) 也隨之上漲。這種瓶頸使得擁有專有外延生產線的供應商更具優勢。

工業機器人和自動化領域的快速成長

協作機器人、自動導引運輸車)和高速數控加工中心正在推動馬達驅動 IC 市場的發展。這是因為每個關節都整合了一個三相伺服迴路。雖然中國、日本和韓國的工廠在裝機量方面佔據主導地位,但北美和歐洲正透過鼓勵提高生產效率的回流政策來縮小差距。除了透過整合安全轉矩關閉 (STO) 通道和 EtherCAT 相容性來節省邏輯基板空間外,ISO 13849 標準也對具有確定性關斷路徑的驅動 IC 更為青睞。能夠預先認證功能安全宏大型基地台的供應商可以確保其設計在競爭對手透過降低成本來測試原型之前就被市場接受。

汽車級安全認證的成本

為了獲得 AEC-Q100 1 級認證,供應商必須進行 1000 小時的高溫運行 (HTOL)、高溫熱負荷 (THB) 和靜電放電 (ESD) 測試。這些測試總合可能需要長達兩年的時間,每個產品線的成本超過 50 萬美元。此外,進行額外的 ISO 26262 ASIL-D 和 SAE J3061 網路安全檢查也給規模小規模的無廠半導體公司帶來了沉重的負擔,這些公司缺乏足夠的財力來承受反覆測試批次失敗的風險。因此,一級模組整合商傾向於選擇在汽車行業擁有悠久歷史的成熟公司,這導致採購能力集中,並扼殺了電機驅動 IC 市場小批量生產領域的創新。

細分市場分析

預計到2031年,碳化矽(SiC)驅動IC的複合年成長率將達到7.89%,超過馬達驅動IC整體市場的成長速度。隨著原始設備製造商(OEM)在800V牽引和重工業驅動領域追求更高的結溫和開關速度,基於SiC的馬達驅動IC市場規模正在擴大。無刷直流控制器仍是銷售主力產品,預計到2025年,其在消費性電子產品、暖通空調鼓風機和中低中功率工廠設備領域的銷售額將佔46.94%。

隨著無芯FET陣列成本持續下降,有刷直流馬達和步進馬達仍然是價格敏感型應用和傳統插座的可行選擇。然而,監管效率閾值正推動即使是低成本平台也向三相拓撲結構靠攏。隨著閘極驅動通道被整合到下一代汽車微控制器中,整合趨勢正在加速。這種轉變正在推動從分立元件向平均售價更高的單晶片裝置過渡。因此,碳化矽(SiC)將成為高階市場的標準,氮化鎵(GaN)將應用於48V配件,而有刷直流控制器將在維護和維修需求的長尾市場中佔據一席之地。

到2025年,汽車平台將佔總需求的37.53%,隨著純電動車(BEV)的日益普及,該細分市場將維持7.83%的複合年成長率。每輛純電動車通常配備15到25個驅動IC,用於驅動、電池溫度控管迴路、轉向和舒適性功能,使其成為馬達驅動IC市場中元件數量最多的產品類別之一。此外,在工業自動化領域,協作機器人和自動化倉庫的伺服迴路密度很高,需要先進的診斷功能和確定性的延遲。

從無線吸塵器到高階咖啡機,家用電子電器普遍採用無刷直流馬達(BLDC馬達)以追求靜音運轉和節能效果,這導致成本控制嚴格,訂單穩定且適中。醫療設備雖然產量較小,但由於生命維持系統和手術機器人需要通過ISO 13485認證,且首次故障率(FIT)必須低於個位數,因此利潤率仍然很高,這也提升了那些倡導採用醫用級製程管理的馬達驅動IC供應商的市場佔有率。

區域分析

預計到2025年,亞太地區將佔全球銷售額的52.53%。這主要得益於中國在電動車(BEV)生產領域的領先地位,而印度則推出了針對模擬元件的新型晶圓廠(製造工廠)激勵措施。日本和韓國的合資晶圓廠正在提高汽車級碳化矽(SiC)的產能,從而支持工業機器人和資訊娛樂模組出口的激增。如果國產驅動積體電路(IC)符合ISO 26262和IATF 16949認證要求,本地一級供應商將優先選擇國產驅動積體電路,有助於加強區域供應鏈並縮短設計週期回饋時間。

在北美和歐洲,政策主導的需求模式十分通用,例如,對車輛平均二氧化碳排放的限制迫使汽車製造商加快對電動車的投資。 《晶片與科學法案》撥款390億美元用於製造業補貼,並將類比多晶片模組列為優先類別。此外,德國30億歐元的半導體研發基金也為汽車電力電子領域提供津貼。這些資金的注入有助於電機驅動積體電路供應商在客戶工廠附近建立封裝和最終測試設施,從而抵消不斷上漲的人事費用並降低長期製造流程風險。

南美洲是成長最快的地區,複合年成長率高達 8.18%,主要得益於巴西的工業現代化融資和阿根廷大力推進礦業電氣化。無刷直流馬達 (BLDC) 和碳化矽 (SiC) 驅動組正被應用於礦用自動卸貨卡車、輸送機和製程泵浦中,以減少柴油消耗,每個裝置都整合了數十個高壓驅動積體電路 (IC)。在南美洲其他地區,從智利的阿塔卡馬太陽能走廊到沙烏地阿拉伯的智慧城市“NEOM”,電子整流泵和暖通空調 (HVAC) 系統正被應用於可再生能源大型企劃中,這進一步刺激了對電機驅動 IC 的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車對高壓驅動積體電路的需求

- 工業機器人和自動化領域的快速成長

- 無刷直流馬達在消費性電子和暖通空調領域的快速普及

- 向寬能隙(SiC、GaN)驅動積體電路過渡

- 嵌入式人工智慧預測性維護功能

- 透過車輛區域架構減少功率級材料清單(BOM)。

- 市場限制因素

- 汽車級安全認證的成本

- 半導體供應鏈的波動性

- 超小型無刷直流模組的熱極限

- 智慧馬達的整合正在蠶食低功耗積體電路的市場佔有率。

- 宏觀經濟因素對市場的影響

- 產業價值、供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依馬達類型

- 有刷直流驅動積體電路

- 無刷直流驅動積體電路

- 步進馬達驅動積體電路

- SiC驅動IC

- 其他馬達類型

- 產業最終用途

- 車

- 工業自動化與機器人技術

- 家用電子電器和家用電器

- 醫療設備

- 其他終端用戶產業

- 按電壓範圍

- 24伏或更低

- 25~48 V

- 49~240 V

- 240伏特或以上

- 透過半導體材料

- 矽

- 碳化矽(SiC)

- 氮化鎵(GaN)

- 其他半導體材料

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Allegro MicroSystems, Inc.

- Alpha & Omega Semiconductor Ltd.

- Analog Devices, Inc.

- Diodes Incorporated

- Infineon Technologies AG

- Maxim Integrated Products, Inc.

- Melexis NV

- Microchip Technology Incorporated

- Monolithic Power Systems, Inc.

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Panasonic Industry Co., Ltd.

- Power Integrations, Inc.

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Sanken Electric Co., Ltd.

- Silergy Corp.

- STMicroelectronics NV

- Texas Instruments Incorporated

- Toshiba Electronic Devices & Storage Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the motor driver IC market size is projected to expand from USD 4.97 billion in 2025 and USD 5.34 billion in 2026 to USD 7.46 billion by 2031, registering a CAGR of 6.9% between 2026 and 2031.

This report is Segmented by Motor Type (Brushed DC Driver IC, Sic Driver IC, and More), End-Use Industry (Automotive, Industrial Automation and Robotics, Healthcare Equipment and More), Voltage Range (Up To 24 V, 25-48 V, 49-240 V, and Above 240 V), Semiconductor Material (Silicon, Silicon Carbide (SiC), and Gallium Nitride (GaN), and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Motor Driver IC Market Trends and Insights

EV-Led Demand for High-Voltage Driver ICs

Battery-electric vehicle output is scaling quickly, and each high-voltage traction inverter now requires multi-phase gate drivers that tolerate junction temperatures above 175°C. Silicon-carbide MOSFETs satisfy this envelope at switching frequencies beyond what legacy IGBT drivers handle, letting OEMs downsize cooling loops and cable gauges. Commercial-vehicle electrification in California and the European Union further widens the opportunity because 800 V battery packs need reinforced-isolation drivers with creepage clearances exceeding IEC 60664-1 limits. Although demand is strong, qualified 200 mm SiC wafer capacity remains tight, extending lead times past half a year and inflating device ASPs, a bottleneck that entrenches suppliers with captive epitaxy lines.

Industrial Robotics and Automation Surge

Collaborative robots, automated guided vehicles, and high-speed CNC centers collectively drive the motor driver IC market, as each articulated joint embeds a three-phase servo loop. Factories in China, Japan, and South Korea dominate installation counts, yet North America and Europe are closing the gap with reshoring policies that reward productivity upgrades. Integrated safe-torque-off channels and EtherCAT-ready logic-shrinkboard real estate, while ISO 13849 compliance favors driver ICs with deterministic shutdown pathways. Vendors that can pre-certify functional-safety macrocells lock in design wins before value-engineering rivals can benchmark prototypes.

Automotive-Grade Safety Qualification Costs

Securing AEC-Q100 Grade 1 approval forces suppliers to perform 1 000-hour HTOL, THB, and ESD tests that collectively span up to two years and can cost more than USD 500 000 per product line. Layering ISO 26262 ASIL-D and SAE J3061 cybersecurity checks on top strains smaller fabless firms that lack the cash to absorb repeated test-lot failures. As a result, tier-1 module integrators gravitate toward incumbents with long automotive track records, consolidating purchasing power and throttling innovation at the low-volume edge of the motor driver IC market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of BLDC Motors in Consumer and HVAC

- Shift to Wide-Bandgap (SiC, GaN) Driver ICs

- Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SiC driver ICs headline the performance story, outpacing the overall motor driver IC market with a projected 7.89% CAGR through 2031. The motor driver IC market size for SiC-based solutions rises as OEMs chase higher junction temperatures and switching speeds in 800 V traction and heavy-industrial drives. Brushless DC controllers remain the workhorse in volume terms, holding 46.94% revenue in 2025 across appliances, HVAC blowers, and low-to-mid-power factory equipment.

Continued cost erosion in coreless FET arrays keeps brushed-DC and stepper options alive in price-sensitive or legacy sockets, yet regulatory efficiency floors nudge even budget platforms toward three-phase topologies. Integration trends deepen as next-generation automotive microcontrollers embed gate-driver channels, a shift that trades discrete sockets for higher ASP monolithic devices. SiC, therefore, becomes the benchmark in premium tiers, while GaN pilots service 48 V accessories, and brushed-DC controllers settle into a long tail of maintenance and refurbishment demand.

Automotive platforms absorbed 37.53% of 2025 demand, and escalating battery-electric penetration keeps the segment on a 7.83% CAGR path. Each BEV typically installs 15-25 driver ICs for traction, battery-thermal loops, steering, and comfort functions, sustaining one of the deepest bill-of-materials stacks in the motor driver IC market. Industrial automation follows, with collaborative robots and automated warehouses installing dense clusters of servo loops that command premium diagnostics and deterministic latency.

Consumer electronics from cordless vacuums to high-end coffee machines embrace BLDC motors for acoustic and energy gains, generating stable mid-volume orders albeit at fierce cost targets. Medical equipment, although smaller in units, maintains high-margin pricing because life-support and surgical robots need ISO 13485 documentation and failure rates below single-digit FIT, bolstering the motor driver IC market share of vendors touting medical-grade process discipline.

Geography Analysis

Asia-Pacific commanded 52.53% of 2025 revenue because China dominates battery-electric car production while India unlocks fresh fab incentives for analog components. Joint-venture fabs in Japan and South Korea add capacity for automotive-grade SiC, supporting surging export volumes of industrial robots and infotainment modules. Local tier-1s choose domestic driver ICs whenever ISO 26262 and IATF 16949 paperwork aligns, reinforcing regional supply loops and shortening design-cycle feedback.

North America and Europe share a policy-led demand pattern where fleet-average CO2 caps compel OEMs to front-load EV investments. The CHIPS and Science Act dedicates USD 39 billion to fabrication subsidies, with analog multichip modules listed as priority categories, and Germany's EUR 3 billion semiconductor R and D pool steers grants toward automotive power electronics. These cash injections offset higher labor costs and de-risk long builds for motor driver IC suppliers that co-locate packaging and final test near customer plants.

South America achieves the fastest regional climb at 8.18% CAGR, anchored by Brazil's industrial modernization loans and Argentina's move to electrify mineral extraction. Mining haul trucks, conveyor lines, and process-plant pumps adopt BLDC and SiC drive packs to curb diesel usage, each installation embedding dozens of high-voltage driver ICs. Elsewhere, renewable megaprojects from Chile's Atacama solar corridor to Saudi Arabia's NEOM smart city specify electronically commutated pumps and HVAC systems, importing incremental demand into the motor driver IC market.

- Allegro MicroSystems, Inc.

- Alpha & Omega Semiconductor Ltd.

- Analog Devices, Inc.

- Diodes Incorporated

- Infineon Technologies AG

- Maxim Integrated Products, Inc.

- Melexis NV

- Microchip Technology Incorporated

- Monolithic Power Systems, Inc.

- NXP Semiconductors N.V.

- ON Semiconductor Corporation

- Panasonic Industry Co., Ltd.

- Power Integrations, Inc.

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Sanken Electric Co., Ltd.

- Silergy Corp.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Toshiba Electronic Devices & Storage Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-led demand for high-voltage driver ICs

- 4.2.2 Industrial robotics and automation surge

- 4.2.3 Rapid adoption of BLDC motors in consumer and HVAC

- 4.2.4 Shift to wide-bandgap (SiC, GaN) driver ICs

- 4.2.5 Embedded AI-based predictive-maintenance features

- 4.2.6 Vehicle zonal-architecture reducing power stage BOM

- 4.3 Market Restraints

- 4.3.1 Automotive-grade safety qualification costs

- 4.3.2 Semiconductor supply-chain volatility

- 4.3.3 Thermal limits in ultra-compact BLDC modules

- 4.3.4 Smart-motor integration cannibalising low-power ICs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value, Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Brushed DC driver IC

- 5.1.2 Brushless DC driver IC

- 5.1.3 Stepper motor driver IC

- 5.1.4 SiC driver IC

- 5.1.5 Rest of Motor Type

- 5.2 By End-use Industry

- 5.2.1 Automotive

- 5.2.2 Industrial automation and robotics

- 5.2.3 Consumer electronics and appliances

- 5.2.4 Healthcare equipment

- 5.2.5 Rest of End-use Industry

- 5.3 By Voltage Range

- 5.3.1 Up to 24 V

- 5.3.2 25-48 V

- 5.3.3 49-240 V

- 5.3.4 Above 240 V

- 5.4 By Semiconductor Material

- 5.4.1 Silicon

- 5.4.2 Silicon Carbide (SiC)

- 5.4.3 Gallium Nitride (GaN)

- 5.4.4 Rest of Semiconductor Material

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Allegro MicroSystems, Inc.

- 6.4.2 Alpha & Omega Semiconductor Ltd.

- 6.4.3 Analog Devices, Inc.

- 6.4.4 Diodes Incorporated

- 6.4.5 Infineon Technologies AG

- 6.4.6 Maxim Integrated Products, Inc.

- 6.4.7 Melexis NV

- 6.4.8 Microchip Technology Incorporated

- 6.4.9 Monolithic Power Systems, Inc.

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 ON Semiconductor Corporation

- 6.4.12 Panasonic Industry Co., Ltd.

- 6.4.13 Power Integrations, Inc.

- 6.4.14 Renesas Electronics Corporation

- 6.4.15 ROHM Co., Ltd.

- 6.4.16 Sanken Electric Co., Ltd.

- 6.4.17 Silergy Corp.

- 6.4.18 STMicroelectronics N.V.

- 6.4.19 Texas Instruments Incorporated

- 6.4.20 Toshiba Electronic Devices & Storage Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

電機驅動IC市場分析及至2035年預測:依類型、產品類型、技術、組件、應用、形狀、材質類型、裝置、最終用戶及功能分類

電機驅動IC市場分析及至2035年預測:依類型、產品類型、技術、組件、應用、形狀、材質類型、裝置、最終用戶及功能分類 電機驅動IC市場機會、成長要素、產業趨勢分析及2026年至2035年預測

電機驅動IC市場機會、成長要素、產業趨勢分析及2026年至2035年預測 2026年全球馬達驅動積體電路(IC)市場報告

2026年全球馬達驅動積體電路(IC)市場報告 BLDC電機IC市場按相型、產品類型、輸出功率、分銷管道和應用分類-2026年至2032年全球預測

BLDC電機IC市場按相型、產品類型、輸出功率、分銷管道和應用分類-2026年至2032年全球預測 馬達驅動器市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

馬達驅動器市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測 汽車馬達驅動器市場規模、佔有率和成長分析(按額定電壓、應用和地區分類):產業預測(2026-2033 年)

汽車馬達驅動器市場規模、佔有率和成長分析(按額定電壓、應用和地區分類):產業預測(2026-2033 年) 全球馬達驅動IC市場

全球馬達驅動IC市場 全球無刷直流(BLDC)馬達驅動器市場:市場規模(按類型、轉速、最終用戶和地區)、未來預測

全球無刷直流(BLDC)馬達驅動器市場:市場規模(按類型、轉速、最終用戶和地區)、未來預測 BLDC馬達驅動器全球市場,2025-2029 年

BLDC馬達驅動器全球市場,2025-2029 年 全球馬達驅動板市場,2025-2029

全球馬達驅動板市場,2025-2029