|

市場調查報告書

商品編碼

2063286

3D安全支付認證:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)3D Secure Pay Authentication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

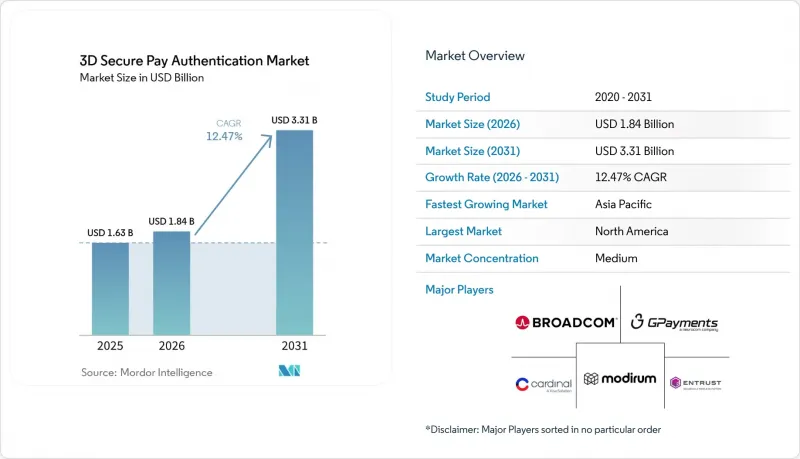

根據 Mordor Intelligence 預測,3D Secure 支付認證市場規模將從 2025 年的 16.3 億美元成長到 2026 年的 18.4 億美元,然後在 2031 年達到 33.1 億美元,2026 年至 2031 年的複合年成長率為 12.47%。

本報告按組件(存取控制伺服器、3D 安全伺服器和商家外掛程式等)、部署模式(本地部署、雲端部署、混合式部署)、認證流程類型(無縫流程等)、最終用戶(銀行和發卡機構、商家和付款閘道、支付服務供應商等)以及地區進行細分。市場預測以美元計價。

全球3D安全支付認證市場趨勢與洞察

電子商務的蓬勃發展和非面對面信用卡詐欺的增加。

預計到2025年,電子商務詐騙將達到創紀錄的480億美元,其中信用卡詐欺交易佔所有卡片詐騙的73%。這使得強客戶身份驗證成為損失預防的主要手段。預計到2026年,扣回爭議帳款詐騙將達到281億美元。如果將商品成本、運費和手續費都計算在內,美國商家目前每因詐欺損失1美元,就要承擔4.61美元的成本。 EMV 3-D Secure的責任轉移規則意味著,如果身分驗證被拒絕,發卡銀行將承擔扣回爭議帳款,這促使銀行提高其驗證率。經過驗證的付款可以將詐欺相關的扣回爭議帳款減少60%至80%,這一效果足以抵銷每筆交易0.05至0.15美元的手續費。因此,雖然詐欺的增加推動了3D Secure支付身份驗證市場提供商的交易量成長,但他們也被迫在安全性和便利的用戶體驗之間尋求平衡。

監管要求縮短了合規期限。

支付服務指令2 (PSD2) 在歐洲阻止了約200億歐元(223億美元)的欺詐性使用,但豁免範圍的縮小以及發卡機構拒絕低風險請求,導致需要身份驗證的交易量增加。印度2025年9月發布的指南,自2026年4月起,所有國內交易必須至少使用一種動態身分驗證因素,並要求發卡機構賠償因違規造成的客戶損失。巴西第506號決議規定,Pix匯款和終端註冊必須進行生物識別,促使當地金融機構加大基礎設施投資。 Visa自2025年10月起對身分驗證率低於網路閾值的收購方進行處罰,導致美國自2026年1月起身分驗證數量增加。多個地區的法規設定了合規標準,這些標準構成了自然需求的下限,即使在商戶此前可選擇是否採用3D Secure支付身份驗證的地區,也加速了該支付身份驗證市場的擴張。

整合成本和複雜性阻礙了中小型加盟商的發展。

雖然每次驗證的費用看似不高,但小規模商家面臨一次性整合專案、終端測試和持續投訴處理的挑戰,所有這些都會加劇他們有限的資源壓力。 EnterSekt 的 Orkestrate 承諾部署速度提升 85%,登入流暢度高達 98%,但目前技術的普及仍主要集中在大型銀行。監管要求即使是小額交易也必須進行嚴格的客戶身份驗證,一些商家正在遊說政府,爭取基於風險的豁免,這削弱了防詐欺帶來的益處。雖然對於平均交易量高的企業來說,成本效益差距會縮小,但許多小規模企業仍寧願承擔扣回爭議帳款,也不願客戶流失的風險。因此,3D Secure 支付身分驗證市場在分散的長尾細分市場中受到的阻礙最為嚴重。

細分市場分析

隨著發卡機構將生物識別和金鑰流程原生整合到其行動應用中,SDK 和整合服務預計將在 3D Secure 支付認證市場中獲得更大的收入佔有率。 「3D Secure 伺服器和商家插件」類別預計到 2025 年將保持 42.53% 的市場佔有率,這反映了現有的部署情況,但市場正在向模組化軟體套件轉變,這些套件可以加快設備配對速度並減少維護工作。 Visa 的支付金鑰服務和 Noon Payments 的全球推廣表明,卡組織有意透過託管服務提供即插即用的 FIDO2 認證,這推動了 SDK 支出預計以 12.91% 的複合年成長率成長。目錄伺服器作為路由元件仍然很重要,但許多目錄伺服器現在被捆綁到更廣泛的編配平台中,而不是單獨銷售。整合預算也正在轉向委託認證功能,這使得商家能夠主動評估風險,並僅在必要時呼叫發卡機構的存取控制伺服器。

基於雲端的交付模式正在推動進一步成長。 Utimaco 在 IBM 雲端上推出的「支付 HSM 即服務」就是一個典型的例子,它體現了從資本密集硬體轉向高彈性加密能力的轉變。萬事達卡的令牌服務現在包含身份驗證元資料,減少了對單獨伺服器呼叫的需求,並模糊了令牌化和身份驗證元件之間的界限。在印度等行動優先市場,生物識別和金鑰預計將成功率提高 2-3 個百分點,從而推動金融科技和「先買後付」平台對 SDK 的需求成長。因此,SDK 和編配工具正在推動 3D 安全支付身分驗證市場的發展,而不會增加支付過程中的摩擦。

到 2025 年,基於雲端的部署將佔 3D Secure 支付認證市場 51.18% 的佔有率,預計到 2031 年將以每年 12.83% 的速度成長。諸如 IBM Cloud 上的 Utimaco Payment HSM 和 Microsoft Azure Payment HSM 等託管服務無需實體金鑰管理硬體,即可為中型發卡機構提供企業級安全保障。用於計算風險評分的即時機器學習模型現在可以在雲端環境中持續更新,而這對於固定部署的本機設備來說難以實現。 Visa 的智慧授權平台於 2026 年 3 月在歐洲推出,承諾 99.999% 的運轉率和 96.3% 的授權準確率,這些指標充分展現了雲端的強大韌性。

在資料居住要求必須進行本地處理的情況下,本地部署系統仍然普遍存在,尤其是在南美和亞太地區的受監管銀行。混合架構透過在雲端部署事件流分析,同時將金鑰庫保留在本地,從而為滿足合規性要求搭建了橋樑。靈活的定價模式進一步增強了雲端的優勢。付費使用制,折舊免稅額。詐欺行為的激增以及合成身分的威脅(已給美國金融機構造成高達 350 億美元的損失)加劇了對可擴展分析的需求,鞏固了雲端在 3D Secure 支付認證市場的主導地位。

區域分析

2025年,北美地區維持了40.55%的市場佔有率,在收入方面位居榜首。這主要歸功於Visa和萬事達卡最佳化了交換費,以及2025年10月實施的績效懲罰措施,該措施促使發卡機構對更高比例的電子商務流量進行身份驗證。該地區強大的雲端基礎設施使收購方能夠快速實施風險評分,從而實現了比全球任何其他地區都更高的網路代幣採用率。

亞太地區是成長的主要驅動力,預計2031年年複合成長率(CAGR)將達到13.11%。印度將於2026年4月強制實施動態雙因素認證,而中國跨境電商需求的激增也迫使發卡機構大規模採用EMV 3-D Secure 2.x認證。到2026年,全球將有超過126億個網路代幣運作,其中亞太地區將佔據絕大部分,這主要歸功於該地區行動錢包的日常交易量佔比很高。然而,認證成功率仍存在差異。預計到2026年,英國的認證成功率將達到95%,而印度僅72%,巴西則只有36%,凸顯了供應商在準備工作上需要解決的差距。

在歐洲,PSD2實施的成熟度使其認證成功率位居全球最高,英國為95%,義大利為93%,荷蘭為92%。儘管市場已趨於飽和,但交易量依然居高不下,這得益於交易風險分析豁免要求的不斷收緊。中東、非洲和南美洲在絕對值上落後於歐洲,但隨著阿拉伯聯合大公國和沙烏地阿拉伯的規則與卡片組織標準接軌,以及巴西的Pix生物識別要求推動消費支出成長,這些地區的3D安全支付認證市場正在快速發展。因此,發卡機構能力的區域差異正在為3D安全支付認證市場的快速擴張創造機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 電子商務和非面對面卡片詐騙的激增

- 監理要求(PSD2 SCA、印度儲備銀行、巴西中央銀行)

- 遷移到 EMV 3-D Secure 2.X 協議

- 行動錢包和應用程式內支付的蓬勃發展

- WebAuthn 和密碼整合

- 基於雲端的HSM即時風險評分

- 市場限制因素

- 整合成本和複雜性

- 在非強制性區域,結帳過程中的摩擦會增加。

- 新興市場發行人準備程度的差異

- 限制資料共用的隱私法規(RbA)

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 存取控制伺服器(ACS)

- 3D 安全伺服器/商家插件

- 目錄伺服器

- SDK 和整合服務

- 其他規則

- 部署模式

- 現場

- 基於雲端的

- 混合

- 身份驗證流程類型

- 無摩擦流

- 挑戰流程

- 帶外/解耦流

- 委託認證

- 最終用戶

- 銀行/發卡公司

- 商家和付款閘道

- 支付服務供應商(PSP)

- 金融科技與先買後付平台

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GPayments Pty Ltd.

- CardinalCommerce Corporation

- Modirum Oy

- Broadcom Inc.

- Entrust Corporation

- RSA Security LLC

- Fiserv, Inc.

- Decta Limited

- Marqeta, Inc.

- Bluefin Payment Systems LLC

- Entersekt(Pty)Ltd.

- Thales Group

- Netcetera AG

- Worldline SA

- Adyen NV

- ACI Worldwide Inc.

- Mastercard Incorporated

- Visa Inc.

- American Express Company

- JCB Co., Ltd.

- Discover Financial Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the 3D secure pay authentication market size is expected to grow from USD 1.63 billion in 2025 to USD 1.84 billion in 2026 and is forecast to reach USD 3.31 billion by 2031 at 12.47% CAGR over 2026-2031.

This report is Segmented by Component (Access Control Server, 3-D Secure Server and Merchant Plug-In, and More), Deployment Mode (On-Premises, Cloud-Based, and Hybrid), Authentication Flow Type (Frictionless Flow, and More), End User (Banks and Issuers, Merchants and Payment Gateways, Payment Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global 3D Secure Pay Authentication Market Trends and Insights

Surge in E-Commerce and Card-Not-Present Fraud

Record USD 48 billion in e-commerce fraud during 2025 pushed card-not-present abuse to 73% of total card fraud, making strong customer authentication the primary loss-prevention lever. Chargeback fraud losses are projected at USD 28.1 billion during 2026, and every fraudulent dollar now costs U.S. merchants USD 4.61 when merchandise, shipping, and fees are included. EMV 3-D Secure liability shift rules place chargeback responsibility on issuers once authentication is declined, encouraging banks to raise challenge rates. Authenticated checkouts cut fraud-coded chargebacks by 60-80%, a return that offsets per-call fees of USD 0.05-0.15. Fraud escalation, therefore, fuels volume growth for 3D Secure Pay Authentication market providers while forcing them to balance security with friction-free experiences.

Regulatory Mandates Compress Compliance Timelines

Payment Services Directive 2 prevented an estimated EUR 20 billion (USD 22.3 billion) in European fraud, but narrower exemptions and issuer denial of low-risk requests now drive mandatory authentication volumes. India's September 2025 directions require at least one dynamic factor for every domestic transaction from April 2026, and issuers must reimburse customers for non-compliance losses. Brazil's Resolution 506 requires biometric confirmation for Pix transfers and device registration, increasing infrastructure spending among local institutions. Visa began penalizing acquirers in October 2025 when authentication rates fell below network thresholds, lifting U.S. authentication volume from January 2026 onward. Rules in multiple regions create a compliance floor beneath organic demand, accelerating the 3D Secure Pay Authentication market even where merchant adoption was previously discretionary.

Integration Cost and Complexity Deter Mid-Market Merchants

Per-authentication fees appear modest, yet small merchants face one-time integration projects, device testing, and ongoing dispute management that strain limited resources. Entersekt's Orkestrate promises 85% faster deployment and 98% frictionless logins, but adoption remains skewed toward tier-one banks. Regulatory mandates force even low-value transactions into strong customer authentication, pushing some sellers to lobby for risk-based exemptions that dilute fraud benefits. The cost-benefit gap narrows where average ticket values are high, yet many micro-merchants still choose to absorb chargebacks rather than risk abandonment. The drag on the 3D Secure Pay Authentication market is therefore most acute in fragmented long-tail segments.

Other drivers and restraints analyzed in the detailed report include:

- Migration to EMV 3-D Secure 2.x Unlocks Frictionless and Delegated Flows

- Mobile-Wallet and In-App Payment Boom Expands Authentication Surface

- Checkout Friction in Non-Mandate Regions Caps Voluntary Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SDK and Integration Services are set to capture a growing share of the 3D Secure Pay Authentication market revenue as issuers embed biometric and passkey flows natively in mobile apps. The 3D Secure Server and Merchant Plug-in category kept a 42.53% share in 2025, reflecting legacy installs, yet the preference is shifting toward modular software kits that speed device binding and reduce maintenance. Visa's Payment Passkey Service and Noon Payments' global launch illustrate the card network's intention to deliver plug-and-play FIDO2 through managed services, which supports the 12.91% forecast CAGR for SDK spend. Directory Servers retain their importance as routing components, yet most are bundled into broader orchestration platforms rather than sold standalone. Integration budgets are also flowing toward delegated authentication capability, letting merchants pre-score risk and call issuer Access Control Servers only when needed.

Cloud delivery models further catalyze growth. Utimaco's Payment HSM as a Service on IBM Cloud exemplifies a move away from capital-intensive hardware toward elastic cryptography functions. Mastercard token services now append authentication metadata, reducing the need for separate server calls and blurring the lines between tokenization and authentication components. As mobile-first markets such as India expect biometrics and passkeys to lift success rates 2-3 percentage points, SDK demand intensifies across fintech and Buy Now Pay Later platforms. Consequently, SDKs and orchestration tools reinforce the 3D Secure Pay Authentication market's momentum without adding checkout friction.

Cloud-based deployment accounted for 51.18% of the 3D Secure Pay Authentication market size in 2025 and will grow at 12.83% through 2031. Managed services such as Utimaco Payment HSM on IBM Cloud and Microsoft Azure Payment HSM remove the need for physical key-management hardware, opening enterprise-grade security to mid-tier issuers. Real-time machine learning models that calculate risk scores now update continuously in cloud environments, a feat hard to match on fixed on-premises appliances. Visa's Intelligent Authorization platform, launched in Europe during March 2026, pledges 99.999% uptime and 96.3% approval accuracy, metrics that showcase cloud resilience.

On-premises systems persist where data residency mandates require local processing, especially among regulated banks in South America and the Asia-Pacific. Hybrid architectures place event-stream analytics in the cloud while retaining key stores locally, offering a compliance bridge. Variable pricing further favors cloud: paying USD 0.05-0.15 per authentication on a usage basis is simpler than depreciating capital hardware over five years. Fraud surge and synthetic identity threats costing U.S. institutions up to USD 35 billion reinforce the need for scalable analytics, anchoring the cloud's leadership within the 3D Secure Pay Authentication market.

Geography Analysis

North America remained the revenue leader in 2025 with 40.55% share, as Visa and Mastercard interchange optimization, plus October 2025 performance penalties, drove issuers to authenticate a higher portion of e-commerce traffic. The region's abundant cloud infrastructure lets acquirers implement risk scoring quickly, and network token penetration exceeds any other global zone.

Asia-Pacific is the growth engine, with a 13.11% CAGR projected through 2031. India's April 2026 mandate for dynamic two-factor checks and China's booming cross-border e-commerce demand compel issuers to deploy EMV 3-D Secure 2.x at scale. More than 12.6 billion network tokens were active worldwide in 2026, with Asia-Pacific accounting for a disproportionate slice because mobile wallets dominate daily transactions. Authentication success gaps persist, however: India reached only 72% and Brazil 36% in 2026 compared with the United Kingdom's 95%, highlighting readiness disparities that vendors must bridge.

Europe enjoys the world's highest authentication success due to mature PSD2 rollouts, registering 95% in the United Kingdom, 93% in Italy, and 92% in the Netherlands. Continued tightening of transaction-risk analysis exemptions keeps volume elevated even in saturated markets. The Middle East and Africa and South America trail on absolute dollars but post step-change adoption as the United Arab Emirates and Saudi Arabia align rules with card-network standards, and Brazil's biometric Pix requirements escalate spend. Geographic divergence in issuer capabilities therefore shapes a multi-speed expansion path for the 3D Secure Pay Authentication market.

- GPayments Pty Ltd.

- CardinalCommerce Corporation

- Modirum Oy

- Broadcom Inc.

- Entrust Corporation

- RSA Security LLC

- Fiserv, Inc.

- Decta Limited

- Marqeta, Inc.

- Bluefin Payment Systems LLC

- Entersekt (Pty) Ltd.

- Thales Group

- Netcetera AG

- Worldline SA

- Adyen N.V.

- ACI Worldwide Inc.

- Mastercard Incorporated

- Visa Inc.

- American Express Company

- JCB Co., Ltd.

- Discover Financial Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Surge In E-Commerce and Card-Not-Present Fraud

- 4.3.2 Regulatory Mandates (PSD2 SCA, India RBI, Brazil BCB)

- 4.3.3 Migration to EMV 3-D Secure 2. X Protocols

- 4.3.4 Mobile-Wallet and In-App Payment Boom

- 4.3.5 Webauthn and Passkey Integration

- 4.3.6 Cloud HSM-Powered Real-Time Risk Scoring

- 4.4 Market Restraints

- 4.4.1 Integration cost and complexity

- 4.4.2 Checkout friction in non-mandate regions

- 4.4.3 Inconsistent issuer readiness in EMs

- 4.4.4 Privacy rules limiting data-sharing (RbA)

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Buyer Power

- 4.8.2 Supplier Power

- 4.8.3 Threat of Substitutes

- 4.8.4 Threat of New Entrants

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Access Control Server (ACS)

- 5.1.2 3-D Secure Server / Merchant Plug-in

- 5.1.3 Directory Server

- 5.1.4 SDK and Integration Services

- 5.1.5 Other Component

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Authentication Flow Type

- 5.3.1 Frictionless Flow

- 5.3.2 Challenge Flow

- 5.3.3 Out-of-Band / Decoupled Flow

- 5.3.4 Delegated Authentication

- 5.4 By End User

- 5.4.1 Banks / Issuers

- 5.4.2 Merchants and Payment Gateways

- 5.4.3 Payment Service Providers (PSPs)

- 5.4.4 FinTechs and BNPL Platforms

- 5.4.5 Other End User

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GPayments Pty Ltd.

- 6.4.2 CardinalCommerce Corporation

- 6.4.3 Modirum Oy

- 6.4.4 Broadcom Inc.

- 6.4.5 Entrust Corporation

- 6.4.6 RSA Security LLC

- 6.4.7 Fiserv, Inc.

- 6.4.8 Decta Limited

- 6.4.9 Marqeta, Inc.

- 6.4.10 Bluefin Payment Systems LLC

- 6.4.11 Entersekt (Pty) Ltd.

- 6.4.12 Thales Group

- 6.4.13 Netcetera AG

- 6.4.14 Worldline SA

- 6.4.15 Adyen N.V.

- 6.4.16 ACI Worldwide Inc.

- 6.4.17 Mastercard Incorporated

- 6.4.18 Visa Inc.

- 6.4.19 American Express Company

- 6.4.20 JCB Co., Ltd.

- 6.4.21 Discover Financial Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

3D安全支付認證市場規模、佔有率和成長分析:按組件、認證類型、部署模式、應用、最終用戶、企業規模和地區分類-2026-2033年產業預測

3D安全支付認證市場規模、佔有率和成長分析:按組件、認證類型、部署模式、應用、最終用戶、企業規模和地區分類-2026-2033年產業預測 3D安全支付認證市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

3D安全支付認證市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 3D安全支付認證市場:按組件、支付類型、部署模式、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測

3D安全支付認證市場:按組件、支付類型、部署模式、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測 3D 安全支付認證市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球3D安全支付認證市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

3D 安全支付認證市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球3D安全支付認證市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 3D安全支付認證市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、應用、地區和競爭格局分類,2021-2031年)

3D安全支付認證市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、應用、地區和競爭格局分類,2021-2031年) 2032 年 3D 安全支付認證市場預測:按組件、認證類型、支付介面、應用、最終用戶和地區進行的全球分析

2032 年 3D 安全支付認證市場預測:按組件、認證類型、支付介面、應用、最終用戶和地區進行的全球分析 3D安全支付認證的全球市場

3D安全支付認證的全球市場 3D安全支付認證市場規模、佔有率、趨勢、產業分析報告:依組件、應用、地區、市場預測,2025-2034

3D安全支付認證市場規模、佔有率、趨勢、產業分析報告:依組件、應用、地區、市場預測,2025-2034 全球 3D 安全支付認證市場規模研究,按組件(存取控制伺服器、商家外掛程式等)、應用程式(銀行、商家和支付閘道器)和 2022-2032 年區域預測

全球 3D 安全支付認證市場規模研究,按組件(存取控制伺服器、商家外掛程式等)、應用程式(銀行、商家和支付閘道器)和 2022-2032 年區域預測