|

市場調查報告書

商品編碼

2063285

醫藥TIC:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Pharmaceutical TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

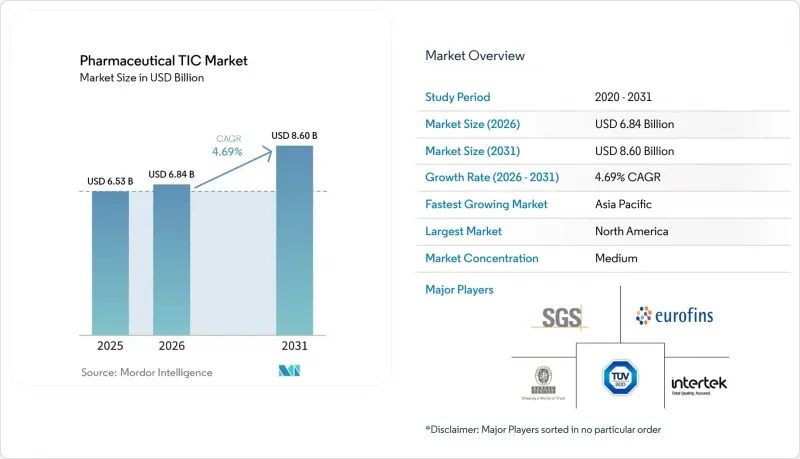

據 Mordor Intelligence 稱,2025 年醫藥 TIC 市值為 65.3 億美元,預計將從 2026 年的 68.4 億美元成長到 2031 年的 86 億美元,2026 年至 2031 年的複合年成長率為 4.69%。

本報告按服務類型(測試、檢驗、認證)、採購類型(內部、外包)、服務交付方式(現場、異地/實驗室、遠端/數位化)和地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球醫藥TIC市場趨勢與洞察

更嚴格的全球GMP法規

2025年,美國食品藥物管理局(FDA)發出的警告信數量創下近20年來新高。主要原因是資料完整性不足和無菌性缺陷,導致製造商要求對無菌填充線和電子記錄進行第三方檢驗。歐洲藥品管理局(EMA)2022年修訂的附件1實施了更嚴格的污染控制規定,目前全部區域對無塵室定期認證的需求日益成長。世界衛生組織(WHO)將預先認證範圍擴大到87個場所,要求每個場所每兩年接受一次由認可的檢測、檢驗和認證(TIC)實驗室進行的審核。 FDA的PreCheck試驗計畫的初步結果顯示,在獲得認可的TIC實驗室的保證後,檢測前置作業時間已縮短至60天。所有這些進展共同鞏固了外部檢測和認證作為製藥營運基礎的地位。

加快需要複雜測試的生物製藥產品的研發進程。

2024年,FDA核准了16種生技藥品,其中大部分是單株抗體;同年,EMA核准了11種生物相似藥。生技藥品需要複雜的檢測方法,例如糖譜分析和宿主細胞蛋白質定量,但很少公司具備這些內部檢測能力。 2024年修訂的ICH Q5E迫使許多製造商透過獲得ISO/IEC 17025認證的合作夥伴重新檢驗檢測法。隨著細胞和基因治療產品線的擴展,載體效力測試和可重複病毒測試正被納入服務範圍。隨著產品系列日益細分為利基藥物和個人化醫療,擁有生物製藥領域深厚專業知識的合約檢測實驗室正成為不可或缺的合作夥伴。

新興市場缺乏熟練的審計師

印度中央藥品標準控制組織(CDSCO)報告稱,到2025年,檢驗員空缺率將達到40%。亞太地區62%的實驗室表示,在招募高技能生物製劑負責人面臨挑戰。培訓不足以及人才流失到高薪的製藥業,導致審核延遲4至6週。領先的檢測、檢驗和認證(TIC)公司正透過與區域性院校和大學合作來應對這一問題,但人才的穩定成長仍需數年時間,這限制了在快速成長地區服務的快速擴張。

細分市場分析

至2025年,檢測服務佔銷售額的43.19%,在醫藥檢測與認證(TIC)市場各服務類別中佔最大佔有率。這項需求源自於單株抗體和細胞/基因療法的複雜檢測,這些檢測需要昂貴且專業的設備,而許多內部實驗室並不具備這些設備。認證領域雖然規模較小,但成長速度最快,複合年成長率達4.71%,因為企業尋求ISO 13485和世衛組織預認證以開拓出口管道。隨著全球互認協議的推進,與認證相關的醫藥檢測與認證市場規模預計將穩定成長。

在檢測服務領域,遠端平台的日益普及導致現場工作時間縮短,利潤率受到擠壓,但持續生產和資料完整性方面的專家審核仍保持著定價權。包含 ISO 13485、ISO 9001 和 GDP 審核的多年認證方案為偵測服務商帶來了持續的收入。此外,數據豐富的檢測工作流程正在分析領域創造長期商機,使檢測實驗室除了提供合規性方面的建議外,還能就流程最佳化提供諮詢。

區域分析

2025年,北美地區佔全球收入的34.41%,這主要歸功於馬薩諸塞州、新澤西州和北卡羅來納州的生物製藥產業叢集對第三方驗證的依賴。該地區監管力度加大,2025年共發出112封警告信,促使無菌填充線和電子記錄的認證測試幾乎全面實施。 2026年的PreCheck試驗計畫將透過數位雙胞胎和即時數據流進一步加強外部審查。加拿大和墨西哥正在擴大區域供應的生產規模,並透過為世衛組織預先認證和出口證書創造新的競標機會,逐步提振需求。

亞太地區是成長最快的區域,預計到2031年將以5.54%的複合年成長率成長,這主要得益於印度總額達1500億盧比(約合1200萬美元)的生產連結獎勵計畫以及中國在2024年批准的48種生物製藥製劑。預計到2025年,印度製藥公司將接受87次FDA上市前檢查,較2020年顯著增加,因此,企業擴大使用技術檢驗中心(TIC)進行準備性檢查。中國進入曲妥珠單抗和Adalimumab生物相似藥市場進一步刺激了分析需求,而日本基於風險的GMP體系則優先考慮持續的生產審計。韓國和澳洲則透過出口導向生物製藥和疫苗工廠來滿足小眾市場的需求。

在歐洲,受2022年EMA附件1(污染控制條例)的推動,市場需求依然強勁。德國、法國和英國支持生物製藥的生產,這些生物製藥需要進行大量的填充變體和功效測試。儘管歐盟和美國之間的相互認可緩解了監管重疊,但製造商仍需要與當地的TIC合作夥伴合作,以確保跨境保障。中東地區的情況仍然較為分散。沙烏地阿拉伯正在推動與「2030願景」一致的各項舉措,而阿拉伯聯合大公國和土耳其則已採納了各自的框架,這導致對跨司法管轄區諮詢的需求增加。南美洲和非洲目前對收入的貢獻不大,但它們正在投資產能以減少對進口的依賴,為2028年後TIC的進一步滲透奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球嚴格執行GMP

- 生物製藥研發管線的加速發展以及隨之而來的複雜測試需求。

- 製藥廠向連續生產過渡

- 美國FDA和EMA增加了上市前檢查的頻率。

- 遠端檢測中數位雙胞胎技術的引入

- 綠色化學的強制性檢驗

- 市場限制因素

- 新興市場缺乏熟練的審計師

- 先進分析設備高成本

- 中東地區法律規範碎片化

- 連網實驗室設備的網路安全風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 測試

- 檢查

- 認證

- 依採購類型

- 內部

- 外包

- 按服務交付方式

- 現場

- 異地/檢查室

- 遠端/數位

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SGS SA

- Eurofins Scientific SE

- Bureau Veritas SA

- TUV SUD AG

- Intertek Group plc

- Applus Services, SA

- UL Solutions Inc.

- DNV AS

- TUV Rheinland AG

- ALS Limited

- Pace Analytical Services LLC

- NSF International

- Charles River Laboratories International, Inc.

- Element Materials Technology Group Limited

- Microbac Laboratories, Inc.

- Labstat International Inc.

- AmSpec LLC

- BSI Group(The British Standards Institution)

- Labcorp Drug Development, Inc.

- Pharmaron Beijing Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the pharmaceutical TIC market was valued at USD 6.53 billion in 2025 and is estimated to grow from USD 6.84 billion in 2026 to USD 8.60 billion by 2031, at a CAGR of 4.69% from 2026 to 2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical TIC Market Trends and Insights

Stringent Global GMP Enforcement

The FDA, in 2025, issued its highest number of warning letters in two decades, largely for data-integrity lapses and aseptic errors, prompting manufacturers to seek third-party validation of sterile-fill lines and electronic records. The European Medicines Agency's 2022 Annex 1 update imposed prescriptive contamination-control rules that now drive demand for routine clean-room certification across the region. WHO expanded prequalification to 87 sites by end-2025, each requiring biennial audits by approved testing, inspection, and certification (TIC) bodies. Early results from the FDA PreCheck pilot indicate inspection lead times are shrinking to 60 days when accredited TIC assurances are in place. Collectively, these moves embed external testing and certification into baseline pharmaceutical operations.

Accelerating Biologics Pipeline Requiring Complex Testing

The FDA cleared 16 biologics in 2024, with monoclonal antibodies dominating approvals, while the EMA authorized an additional 11 biosimilars the same year. Biologics demand advanced assays such as glycosylation profiling and host-cell protein quantification that few in-house labs possess. The 2024 revision of ICH Q5E pushed many manufacturers to revalidate methods via ISO/IEC 17025-accredited partners. Growing cell-and-gene therapy pipelines add vector potency and replication-competent virus testing to the services mix. As product portfolios fragment into niche and personalized medicines, contract laboratories with deep biologics expertise become indispensable allies.

Scarcity of Skilled Auditors in Emerging Markets

India's CDSCO reported a 40% vacancy rate among inspectors in 2025, and 62% of Asia-Pacific labs cited hiring challenges for advanced biologics analysts. Limited training pipelines and talent migration into higher-paying pharma roles lengthen audit backlogs by 4 to 6 weeks. Leading TIC firms have responded with regional academies and university partnerships, yet tangible workforce growth is several years off, constraining rapid service expansion in high-growth geographies.

Other drivers and restraints analyzed in the detailed report include:

- Rising Pre-approval Inspection Frequency by US FDA and EMA

- Shift Toward Continuous Manufacturing in Pharma Plants

- High Cost of Advanced Analytical Instrumentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing generated 43.19% of 2025 revenue, marking the largest pharmaceutical TIC market share among service types. Demand stems from complex assays for monoclonal antibodies and cell-and-gene therapies that require costly, specialized instrumentation, which is unavailable in many in-house labs. Certification, though smaller, is rising fastest at a 4.71% CAGR as firms pursue ISO 13485 and WHO prequalification to unlock exports. The pharmaceutical TIC market size linked to certification is expected to widen steadily alongside global mutual recognition agreements.

Margin pressure is sharper in inspection services as remote platforms shorten on-site work, yet specialized audits for continuous manufacturing and data integrity retain pricing power. Bundled multi-year certification contracts that combine ISO 13485, ISO 9001, and GDP audits position TIC providers for recurring revenue. Data-rich testing workflows also generate long-tail opportunities in analytics, enabling laboratories to advise on process optimization alongside compliance.

Geography Analysis

North America accounted for 34.41% of 2025 revenue as biologics clusters in Massachusetts, New Jersey, and North Carolina relied heavily on third-party validations. The region's strict oversight, reinforced by 112 warning letters in 2025, has driven near-universal adoption of accredited testing across sterile-fill lines and electronic records. The 2026 PreCheck pilot further entrenches external audits through digital twins and real-time data streams. Canada and Mexico add incremental volume as both scale production for regional supply, creating new bids for WHO prequalification and export certificates.

Asia-Pacific is the fastest-growing area, advancing at a 5.54% CAGR through 2031, buoyed by India's INR 150 billion (USD 12 million) production-linked incentives and China's 48 biologic approvals in 2024. Indian facilities faced 87 FDA pre-approval inspections in 2025, up sharply from 2020, prompting widespread engagement of TIC firms for readiness checks. China's push into trastuzumab and adalimumab biosimilars further lifts analytical demand, while Japan's risk-based GMP regime prioritizes continuous-manufacturing audits. South Korea and Australia contribute niche volumes through export-oriented biologics and vaccine plants.

Europe maintains a sizable demand on the back of its 2022 EMA Annex 1 contamination-control rules. Germany, France, and the United Kingdom anchor biologics output that necessitates extensive charge-variant and potency testing. Although EU-US mutual recognition eases regulatory duplication, manufacturers still retain local TIC partners for cross-border assurance. The Middle East remains fragmented; Saudi Arabia aligns toward Vision 2030, while the UAE and Turkey operate distinct frameworks, boosting multi-jurisdiction consulting. South America and Africa presently contribute modest revenue but are investing in capacity to cut import reliance, setting the stage for greater TIC penetration after 2028.

- SGS SA

- Eurofins Scientific SE

- Bureau Veritas SA

- TUV SUD AG

- Intertek Group plc

- Applus Services, S.A.

- UL Solutions Inc.

- DNV AS

- TUV Rheinland AG

- ALS Limited

- Pace Analytical Services LLC

- NSF International

- Charles River Laboratories International, Inc.

- Element Materials Technology Group Limited

- Microbac Laboratories, Inc.

- Labstat International Inc.

- AmSpec LLC

- BSI Group (The British Standards Institution)

- Labcorp Drug Development, Inc.

- Pharmaron Beijing Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global GMP Enforcement

- 4.2.2 Accelerating Biologics Pipeline Requiring Complex Testing

- 4.2.3 Shift Toward Continuous Manufacturing in Pharma Plants

- 4.2.4 Rising Pre-approval Inspection Frequency by US FDA and EMA

- 4.2.5 Digital Twin Adoption for Remote Inspection

- 4.2.6 Green Chemistry Validation Mandates

- 4.3 Market Restraints

- 4.3.1 Scarcity of Skilled Auditors in Emerging Markets

- 4.3.2 High Cost of Advanced Analytical Instrumentation

- 4.3.3 Fragmented Regulatory Frameworks Across Middle East

- 4.3.4 Cybersecurity Risks in Connected Lab Equipment

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Eurofins Scientific SE

- 6.4.3 Bureau Veritas SA

- 6.4.4 TUV SUD AG

- 6.4.5 Intertek Group plc

- 6.4.6 Applus Services, S.A.

- 6.4.7 UL Solutions Inc.

- 6.4.8 DNV AS

- 6.4.9 TUV Rheinland AG

- 6.4.10 ALS Limited

- 6.4.11 Pace Analytical Services LLC

- 6.4.12 NSF International

- 6.4.13 Charles River Laboratories International, Inc.

- 6.4.14 Element Materials Technology Group Limited

- 6.4.15 Microbac Laboratories, Inc.

- 6.4.16 Labstat International Inc.

- 6.4.17 AmSpec LLC

- 6.4.18 BSI Group (The British Standards Institution)

- 6.4.19 Labcorp Drug Development, Inc.

- 6.4.20 Pharmaron Beijing Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

鉑奈米顆粒市場規模、佔有率和成長分析:按應用、粒徑、終端用戶產業、分銷方式和地區分類-2026-2033年產業預測

鉑奈米顆粒市場規模、佔有率和成長分析:按應用、粒徑、終端用戶產業、分銷方式和地區分類-2026-2033年產業預測 二氧化鈦奈米顆粒市場:按產品類型、製造流程、應用和最終用途產業分類-2026-2032年全球市場預測奈米粒子追蹤與分析設備市場:依產品類型、應用、最終用戶和通路分類-2026年至2032年全球市場預測金屬氧化物奈米顆粒市場:按類型、製造方法、形態、粒徑、終端用戶產業和應用分類-2026-2032年全球市場預測

二氧化鈦奈米顆粒市場:按產品類型、製造流程、應用和最終用途產業分類-2026-2032年全球市場預測奈米粒子追蹤與分析設備市場:依產品類型、應用、最終用戶和通路分類-2026年至2032年全球市場預測金屬氧化物奈米顆粒市場:按類型、製造方法、形態、粒徑、終端用戶產業和應用分類-2026-2032年全球市場預測 2026年全球奈米顆粒分析市場報告

2026年全球奈米顆粒分析市場報告 2034年電子設備用銀奈米顆粒市場預測:按產品類型、應用、最終用戶和地區分類的全球分析脂質奈米顆粒製劑市場(按脂質類型、製劑類型、給藥途徑、奈米顆粒尺寸、治療領域、應用和最終用戶分類),全球預測,2026-2032年

2034年電子設備用銀奈米顆粒市場預測:按產品類型、應用、最終用戶和地區分類的全球分析脂質奈米顆粒製劑市場(按脂質類型、製劑類型、給藥途徑、奈米顆粒尺寸、治療領域、應用和最終用戶分類),全球預測,2026-2032年 奈米顆粒分析市場分析與預測(至2035年):按類型、產品類型、服務、技術、應用、材料類型、最終用戶、功能、安裝類型、解決方案分類奈米顆粒製劑市場分析與預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能

奈米顆粒分析市場分析與預測(至2035年):按類型、產品類型、服務、技術、應用、材料類型、最終用戶、功能、安裝類型、解決方案分類奈米顆粒製劑市場分析與預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能 全球二硫化鎢奈米顆粒市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球二硫化鎢奈米顆粒市場規模、佔有率、趨勢和成長分析報告(2026-2034)