|

市場調查報告書

商品編碼

2063284

礦業資訊與通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Mining TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

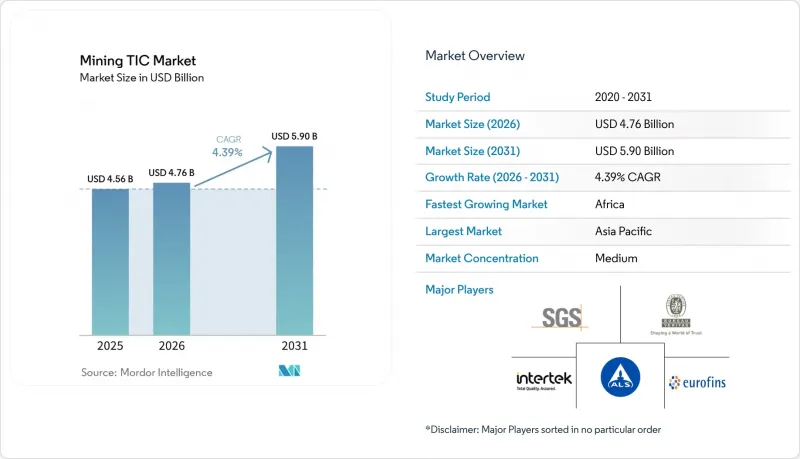

據 Mordor Intelligence 稱,2025 年礦業 TIC(測試、檢驗和認證)市場價值為 45.6 億美元,預計將從 2026 年的 47.6 億美元成長到 2031 年的 59 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按服務類型(測試、檢驗、認證)、採購方式(內部、外包)、服務交付方式(現場、異地/實驗室、遠端/數位化)以及地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球礦業TIC市場趨勢及洞察

電池礦產探勘領域資本投資激增

2025年,非洲電池礦產預算成長了11%。這表明,隨著汽車製造商和電池製造商簽訂承購協議,中小探勘公司的資金籌措風險得以降低,此前三年基底金屬支出持續下降的趨勢已經結束。創業投資人和策略投資者向津巴布韋的鋰礦計畫和剛果民主共和國的鈷礦計畫投入了28億美元,促使分析實驗室採用感應耦合電漿質譜(ICP-MS)和X光衍射(XRD)等分析方法,這些方法比傳統的火法分析方法價格高出20-30%。 2026年4月, 突波 Battery Metals委託ALS Limited進行氫氧化鋰浸出試驗。該試驗延長了處理時間,並凸顯了複雜濕式冶金分析中長期存在的產能瓶頸問題。 2026年2月,Century Lithium進行了一項可行性研究,鑽探了12,000米,並提交了4,500個分析樣品。這表明,隨著專案從探勘階段推進到初步可行性研究階段,分析量將顯著增加。下游需求也十分旺盛,例如,Electra Battery Materials公司將於2025年7月進行硫酸鈷純度檢驗,以滿足汽車產業標準,這將進一步吸引礦業TIC市場的參與企業進入化學工程領域。

加強ESG合規要求

根據歐盟《企業永續發展報告指令》和國際永續發展標準理事會(ISSB)的規定(將於2026年1月生效),礦業公司將被要求揭露範圍3排放,包括來自外包實驗室和樣品物流的排放。英美資源集團於2026年1月至3月期間完成了其三個營運場所的「負責任採礦保障舉措」(IRMA)監控審核,並對其測試、檢驗和認證(TIC)供應商實施了ISO 14064溫室氣體清單和ISO 50001能源管理系統的要求。 2026年4月,雅寶公司在其阿塔卡馬鹽沼工廠也達到了類似的標準,凸顯了其電池礦物供應鏈與檢驗的ESG績效之間日益緊密的聯繫。 TÜV Nord於2026年1月推出的CERA 4合1認證方案,將環境、社會、可追溯性和循環性審核整合到一份合約中,降低了中型生產商的合規成本,並參與企業創造了新的、持續的收入來源。作為回應,必維集團進一步拓展了認證機會,推出了「礦業ESG審核」服務,該服務將「邁向永續採礦」協議與ISO 26000的社會指南相結合。

大宗商品價格波動給探勘預算帶來了壓力。

從2024年初到2025年底,碳酸鋰價格下跌了46%,鎳下跌了37%,鈷下跌了41%。這導致專門從事電池礦物分析的檢測實驗室的分析量下降了15%至20%。冶金煤價格下跌27%後,必和必拓減少了資本投資,並將業務重心從新建礦區(待開發區)轉向價值分析需求較低的礦場周邊作業。佔外包需求80%以上的中小型探勘公司被迫延後2025年下半年12億美元的資金籌措,導致鑽探里程減少25%至30%,迫使檢測實驗室延長付款期限。轉向低風險專案降低了對優質稀土元素和鉑族金屬(其盈利是普通礦山的3倍)分析的需求,給礦業TIC市場的利潤率帶來了壓力。

細分市場分析

到2025年,分析將佔礦業TIC市場佔有率的48.31%,這反映了地球化學分析和冶金測試在資源估算中的核心作用。認證雖然規模較小,但正以4.48%的複合年成長率成長,因為環境、社會和治理(ESG)壓力日益促使礦業公司尋求第三方監管鏈認證。檢驗介於兩者之間,隨著自動化降低單次檢驗成本和技術範圍的擴大,檢驗業務穩定成長。目前,檢驗量仍然很高。一個中等規模的金礦計畫可能會產生2萬個檢體,每個檢體的成本為30至80美元,這為檢驗機構提供了可預測的現金流基礎。英美資源集團、雅寶公司和其他公司將「負責任採礦保證舉措」(IRMA)納入其年度審核週期,正在加速對認證的需求,這表明認證將成為認證機構的長期收入來源,而非臨時收入。

檢測實驗室正在升級至高通量感應耦合電漿質譜儀,以處理鋰、鈷和稀土元素分析工作流程,確保處理能力能夠滿足電池礦物不斷成長的預算需求。 TUV NORD 的「CERA 4in1」提供一站式 ESG 認證解決方案,吸引了許多中型生產商的關注,他們希望避免多次重複審查。 SGS 收購 MsMin 後,實現了基於無人機的露天礦場巡檢和基於探測車的礦堆調查,在不增加人員的情況下延長了檢查週期並提高了利潤率。 ISO IWA 45:2024 的實施造成了認證積壓,導致礦業公司提前一年預訂審核員名額。這一趨勢為礦業檢測與認證 (TIC) 市場的參與企業帶來了強勁的訂單前景。

區域分析

2025年,亞太地區佔礦業TIC市場收入的38.28%。這主要得益於中國稀土元素精煉審核、澳洲鐵礦石品位控制協議以及印度煤炭出口檢驗。 Eurofins和SGS正在中國部署密集的檢驗網路,以滿足下游磁鐵製造商對純度和可追溯性檢驗的要求。 SGS還在2025年1月於皮爾巴拉地區運作了一座檢測中心,該中心每天可處理多達1000個鐵礦石樣品,並保證在四小時內為主要生產商提供檢測結果。澳洲金礦開採作業中攜帶式X光螢光分析儀的引入,正在減少對異地分析的依賴,這反映出決策方式正向即時決策轉變。 Cotecna公司2025年的港口合約也反映了印度鐵礦石貨物第三方檢驗的趨勢,顯示該地區越來越重視中立檢驗。

非洲是成長最快的地區,預計到2031年將以5.22%的複合年成長率成長,這主要得益於津巴布韋鋰礦的發現和剛果民主共和國鈷產能的擴張。儘管全球價格波動,但由於策略投資者註入了新的資金,2025年的探勘預算仍增加了11%。 SGS透過在奈米比亞開設實驗室(計劃於2025年9月開業)並引進感應耦合電漿質譜法(ICP-MS)來滿足稀土元素分析的需求,從而彰顯其在新興市場的先鋒地位。隨著汽車製造商提出更嚴格的規格要求,硫酸鈷純度測試的需求日益成長,推動了銅纜地區對高階分析的需求。物流挑戰依然嚴峻。樣品空運成本可能高達每次2000美元,而且考慮到外匯波動,為了確保供應商的獲利能力,通常採用美元計價的合約。

北美和歐洲是礦業檢測與認證(TIC)市場成熟但仍在成長的地區。預計到2029年,美國地質科學領域將出現13萬人才缺口,促使檢測實驗室加速自動化投資。 2026年4月,SGS與魁北克省的相關人員合作,擴大其鋰和鎳的檢測能力,以配合加拿大在電池供應鏈方面的雄心壯志。歐洲的《企業永續性報告指令》(SDR)於2026年1月生效,這將推動對範圍3排放的需求,而TUV Nord部署的CERA 4in1認證體系則為旨在進入歐盟市場的生產商提供統一的認證流程。中東正崛起為一個新興的成長區域,SGS於2025年10月在沙烏地阿拉伯開設的檢測中心旨在抓住「2030願景」下的礦業投資機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強ESG合規要求

- 礦體深度和複雜度不斷增加

- 引入數位岩心取樣和自動化

- 用於電池應用的礦產探勘投資激增。

- 遠端和自主測試的迅速普及

- 中小礦業公司對TIC外包的需求日益成長

- 市場限制因素

- 大宗商品價格的波動週期給探勘預算帶來了壓力。

- 合格地球化學家和檢驗員短缺

- 碎片化的全球管理體制

- 向偏遠地區運送檢體的成本不斷上升。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 測試

- 檢查

- 認證

- 依採購類型

- 內部

- 外包

- 按服務交付方式

- 現場

- 異地/實驗室

- 遠端/數位

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- ALS Limited

- Eurofins Scientific SE

- TUV SUD AG

- Applus Services SA

- Element Materials Technology Group Limited

- DNV AS

- TUV Rheinland AG

- Kiwa NV

- Mistras Group, Inc.

- Cotecna Inspection SA

- Core Laboratories NV

- China Certification and Inspection Group CCIC

- PetroCanada Laboratories Ltd.

- Alex Stewart International Corporation

- Inspectorate Griffith Australia Pty Ltd.

- Mitra SK Private Limited

- Poni International Inspection Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the mining testing, inspection, and certification (TIC) market size was valued at USD 4.56 billion in 2025 and is estimated to grow from USD 4.76 billion in 2026 to USD 5.90 billion by 2031, at a CAGR of 4.39% from 2026 to 2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Mining TIC Market Trends and Insights

Surge in Battery-Mineral Exploration Capital

Battery-mineral budgets climbed 11% across Africa in 2025, reversing a three-year slide in base-metal spending as automakers and battery manufacturers locked in offtake agreements that reduced funding risk for junior explorers. Venture and strategic investors directed USD 2.8 billion into Zimbabwe lithium and Democratic Republic of the Congo cobalt projects, prompting laboratories to add inductively coupled plasma mass spectrometry and X-ray diffraction workflows that command 20% to 30% price premiums over conventional fire assays. Surge Battery Metals awarded ALS Limited a lithium-hydroxide leach-testing program in April 2026, extending turnaround times and highlighting chronic capacity constraints for complex hydrometallurgical analysis. Century Lithium drilled 12,000 meters and submitted 4,500 assay samples during its February 2026 feasibility study, illustrating the step change in assay volume when projects advance from exploration to pre-feasibility. Downstream pull is also visible, with Electra Battery Materials validating cobalt sulfate purity for automotive specifications in July 2025, drawing Mining TIC market participants deeper into chemical-engineering domains.

Heightened ESG Compliance Requirements

The European Union Corporate Sustainability Reporting Directive and International Sustainability Standards Board rules, effective January 2026, require miners to disclose Scope 3 emissions that encompass contracted laboratories and sample logistics. Anglo American completed Initiative for Responsible Mining Assurance surveillance audits at three operations between January and March 2026, cascading ISO 14064 greenhouse-gas inventories and ISO 50001 energy management requirements to testing, inspection and certification (TIC) providers. Albemarle met the same standard at its Salar de Atacama facility in April 2026, highlighting the tightening link between battery-mineral supply chains and verifiable ESG credentials. TUV NORD's CERA 4in1 scheme, launched in January 2026, bundles environmental, social, traceability, and circularity audits into a single engagement, trimming compliance costs for mid-tier producers and creating a new avenue of recurring revenue for Mining TIC market participants. Bureau Veritas responded by introducing an integrated Mine ESG Audit service that merges Towards Sustainable Mining protocols with ISO 26000 social guidance, further widening the certification opportunity set.

Volatile Commodity Price Cycles Curtailing Exploration Budgets

Lithium carbonate prices dropped 46% between early 2024 and late 2025, while nickel slid 37% and cobalt 41%, leading to a 15% to 20% fall in assay volumes at laboratories focused on battery minerals. BHP pared capital spending after a 27% decline in metallurgical coal prices, shifting from greenfield to near-mine work that needs fewer, lower-value assays. Junior explorers, which drive more than 80% of outsourced demand, lost USD 1.2 billion in committed financing during 2H 2025, forcing drilling meterage cuts of 25% to 30% and pushing laboratories toward extended payment terms. The pivot to lower-risk programs reduces the need for premium rare-earth or platinum-group-metal assays, which can be 3 times as lucrative as routine work, compressing Mining TIC market margins.

Other drivers and restraints analyzed in the detailed report include:

- Digital Core Sampling and Automation Adoption

- Rapid Uptake of Remote and Autonomous Inspections

- Shortage of Qualified Geochemists and Inspectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing controlled 48.31% of the Mining TIC market share in 2025, reflecting the centrality of geochemical assays and metallurgical testwork to resource estimation. Certification, although smaller, is expanding at a 4.48% CAGR as ESG pressures draw miners toward third-party chain-of-custody credentials. Inspection sits between the two, growing steadily as automation lowers per-inspection cost and expands technical scope. Testing volume intensity remains high; a mid-tier gold campaign can generate 20,000 samples at USD 30 to USD 80 each, underpinning predictable cash flow for laboratories. Certification demand accelerated after Anglo American, Albemarle, and others embedded the Initiative for Responsible Mining Assurance into annual audit cycles, signaling a structural, not episodic, revenue stream for accredited bodies.

Laboratory operators are upgrading to high-throughput inductively coupled plasma mass spectrometry rigs that accommodate lithium, cobalt, and rare-earth workflows, aligning capacity with surging battery-mineral budgets. TUV NORD's CERA 4in1 launch offers a one-stop ESG credential, attracting mid-tier producers that wish to avoid multiple overlapping audits. Drone-assisted pit inspections and rover-based stockpile surveys, gained via SGS's MsMin acquisition, are extending inspection cycles without adding headcount, boosting contribution margins. As ISO IWA 45:2024 rolls out, certification backlogs are forming, prompting miners to reserve auditor slots a year in advance, a pattern that underpins robust order visibility for Mining TIC market participants.

Geography Analysis

Asia-Pacific generated 38.28% of Mining TIC market revenue in 2025, anchored by China's rare-earth refining audits, Australia's iron-ore grade-control protocols, and India's coal export inspections. Eurofins and SGS operate dense laboratory networks in China to meet purity and traceability checks demanded by downstream magnet manufacturers. SGS also commissioned a Pilbara facility in January 2025 to process up to 1,000 iron-ore samples daily, ensuring a four-hour turnaround for major producers. Portable X-ray fluorescence adoption across Australian gold campaigns is reducing reliance on off-site assays, reflecting a shift toward real-time decision-making. India's move toward third-party verification of iron-ore cargo, evident in Cotecna's 2025 port contracts, reflects the region's growing preference for neutral validation.

Africa is the fastest-expanding region, projected to grow at 5.22% CAGR through 2031, driven by lithium finds in Zimbabwe and cobalt capacity in the Democratic Republic of the Congo. Exploration budgets rose 11% in 2025 as strategic investors committed fresh capital despite global price volatility. SGS opened a Namibia laboratory in September 2025 and is adding inductively coupled plasma mass spectrometry to meet demand for rare-earth assays, underscoring its first-mover advantage in nascent jurisdictions. Cobalt sulfate purity testing is intensifying as automakers impose stricter specs, driving premium assay demand in the Copperbelt. Logistics hurdles remain acute; sample flights can cost USD 2,000 per shipment, and currency swings prompt USD-denominated contracts to protect provider margins.

North America and Europe represent mature yet still-growing pockets of the Mining TIC market. The United States faces a 130,000-position gap in geoscience by 2029, motivating labs to accelerate automation investments. SGS partnered with Quebec stakeholders in April 2026 to expand lithium and nickel testing capacity, aligning with Canada's ambitions for the battery supply chain. Europe's Corporate Sustainability Reporting Directive, effective January 2026, is pushing demand for Scope 3 emission inventories, while TUV NORD's CERA 4in1 rollout offers a harmonized certification path for producers seeking European Union market access. The Middle East is emerging as a niche growth pocket, and SGS's October 2025 Saudi Arabia opening is designed to capture Vision 2030 mining investments.

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- ALS Limited

- Eurofins Scientific SE

- TUV SUD AG

- Applus Services S.A.

- Element Materials Technology Group Limited

- DNV AS

- TUV Rheinland AG

- Kiwa N.V.

- Mistras Group, Inc.

- Cotecna Inspection SA

- Core Laboratories N.V.

- China Certification and Inspection Group CCIC

- PetroCanada Laboratories Ltd.

- Alex Stewart International Corporation

- Inspectorate Griffith Australia Pty Ltd.

- Mitra SK Private Limited

- Poni International Inspection Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened ESG Compliance Requirements

- 4.2.2 Increasing Depth and Complexity of Ore Bodies

- 4.2.3 Digital Core Sampling and Automation Adoption

- 4.2.4 Surge in Battery-Mineral Exploration Capital

- 4.2.5 Rapid Uptake of Remote and Autonomous Inspections

- 4.2.6 Growing Demand for Outsourced TIC in Junior Mining Firms

- 4.3 Market Restraints

- 4.3.1 Volatile Commodity Price Cycles Curtailing Exploration Budgets

- 4.3.2 Shortage of Qualified Geochemists and Inspectors

- 4.3.3 Fragmented Global Regulatory Regimes

- 4.3.4 Rising Cost of On-site Sample Logistics in Remote Regions

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 Intertek Group plc

- 6.4.4 ALS Limited

- 6.4.5 Eurofins Scientific SE

- 6.4.6 TUV SUD AG

- 6.4.7 Applus Services S.A.

- 6.4.8 Element Materials Technology Group Limited

- 6.4.9 DNV AS

- 6.4.10 TUV Rheinland AG

- 6.4.11 Kiwa N.V.

- 6.4.12 Mistras Group, Inc.

- 6.4.13 Cotecna Inspection SA

- 6.4.14 Core Laboratories N.V.

- 6.4.15 China Certification and Inspection Group CCIC

- 6.4.16 PetroCanada Laboratories Ltd.

- 6.4.17 Alex Stewart International Corporation

- 6.4.18 Inspectorate Griffith Australia Pty Ltd.

- 6.4.19 Mitra SK Private Limited

- 6.4.20 Poni International Inspection Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment