|

市場調查報告書

商品編碼

2063267

印度汽車照明市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Automotive Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

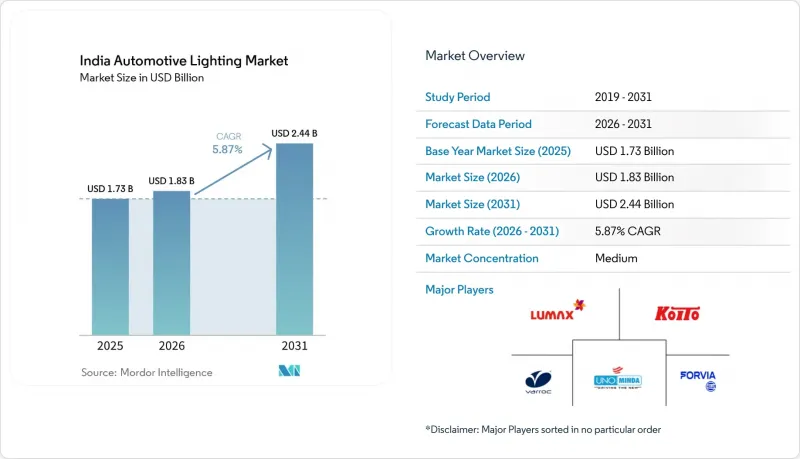

據 Mordor Intelligence 稱,2025 年印度汽車照明市值為 17.3 億美元,高於 2026 年的 18.3 億美元,預計到 2031 年將達到 24.4 億美元,2026 年至 2031 年的複合年成長率為 5.87%。

本報告按車輛類型(乘用車、輕型商用車、中重型商用車、摩托車)、應用領域(外觀和內裝)、技術(鹵素燈、氙氣/HID燈、LED燈、雷射燈、OLED燈)和銷售管道(OEM和售後市場)進行分類。市場預測以貨幣價值(美元)和銷售(輛)兩種形式呈現。

印度汽車照明市場趨勢與洞察

降低LED價格和提高能源效率的法規

零件成本的下降以及印度能源效率局 (BEE)基準值的實施,使得 LED 燈成為各個價位段的標準配備。目前,即使是入門級踏板車,OEM 合約也指定使用 LED 燈,以滿足坎德拉 (cd) 要求,且不會產生熱損耗。已根據生產關聯激勵計劃 (PLI) 投資建設自動化表面黏著技術線的國內供應商正從這一轉變中獲益,而鹵素燈的需求則逐漸萎縮,轉向傳統的替換管道。這種良性的成本-銷售循環正在將 LED 模組的價格壓縮到與鹵素燈組件相同的水平,從而有效地淘汰了鹵素燈組件。

實施AIS-008/AIS-012安全規程

2025年,車頭燈和號誌燈的型式認證審核將更加嚴格。擁有內部光強度測量隧道的一級供應商能夠輕鬆達到標準,而灰色市場組裝難以獲得產品認證。目前,執法部門已採取措施,從都市區零售店下架多種不合規的售後市場燈具。隨著持續監管,預計未經認證的燈泡將被徹底淘汰,從而提高印度道路上的流明穩定性和顏色一致性。

先進照明模組的高額消費稅和進口關稅

對成品雷射和矩陣式LED組件進口徵收超過40%的總合課稅,阻礙了整車製造商在量產車領域廣泛採用這些技術。雖然只有豪華品牌承擔了提供遠端雷射遠光燈的額外成本,但本土合資企業正在加速子組件的本地化生產。他們的目標是在不增加關稅負擔的情況下,讓高階功能更經濟實惠。

細分市場分析

到2025年,乘用車將佔據印度汽車照明市場48.41%的最大佔有率,反映出掀背車和轎車廣泛採用LED燈。相比之下,二輪車預計將以6.01%的複合年成長率成長,成為成長最快的市場。這主要歸功於新型踏板車和摩托車配備了自動頭燈啟動功能,使得可靠的固態燈具成為必需品。針對不同細分市場的法規正在推動照明設備的擴張,而摩托車正成為重要的銷售驅動力。

這些監管利多因素正促使供應商為摩托車訂製緊湊型LED模組,以滿足印度的抗季風標準。模組化燈罩縮短了OEM廠商的設計週期,使品牌能夠每年更新其設計。雖然乘用車在以金額為準方面仍然佔據市場主導地位,但踏板車電動化的加速發展鞏固了摩托車細分市場在長期成長格局中的地位,在不影響單位盈利的前提下,維持了均衡的市場組成。

到2025年,外部照明將佔印度汽車照明市場的63.21%。日間行車燈、主動式轉向頭燈和貫穿式尾燈條鞏固了這一主導地位,這些燈具同時也是獨特的品牌專屬設計。汽車製造商設計師將頭燈視為車輛的“眼睛”,必須將其與雕塑般的前臉完美融合,同時滿足嚴格的光束截止線法規。這項雙重要求使得外部照明系統在設計決策中成為預算分配的重中之重,確保即使是沿用現有車型也能逐步升級。外部照明燈具預計6.11%的複合年成長率也反映了計劃引入更寬的連續照明燈條,以提高黃昏和季風暴雨期間的能見度。

儘管規模仍然相對較小,但車內照明如今已成為聯網汽車和電動車座艙中一種觸覺上的差異化元素。多區域RGB燈條可讓駕駛將氣氛照明與資訊娛樂系統的主題同步,從而將座艙氛圍轉變為軟體定義的體驗。供應商正在積極回應,推出即插即用的LED燈條,將擴散器和CAN總線控制器整合到一個纖薄的機殼中,從而縮短生產線組裝時間。雖然外部訂單系統仍然佔據總價值的大部分,但隨著高階配置車型的普及,以及座艙個人化選項的不斷豐富,內裝照明訂單也在穩步成長。供應商認為這兩種趨勢並非相互競爭,而是相輔相成,因為他們可以透過單一LIN匯流排閘道器同時控制頭燈高度調節和腳部氛圍照明。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- LED價格下降和能源效率法規

- 實施AIS-008/AIS-012安全規程

- FAME-LI 推動電氣化,加速了摩托車和汽車採用 LED 燈的進程。

- 一級在地化獎勵(PLI - 自動和規格)

- 高階汽車製造商對具備ADAS功能的自我調整照明系統的需求日益成長。

- 實現車聯網互聯照明的智慧走廊示範項目

- 市場限制因素

- 先進照明模組的高額消費稅和進口關稅

- 仿冒品汽車燈泡氾濫

- LED驅動器用半導體供不應求

- 二、三線城市消費者意識較低

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 摩托車

- 透過使用

- 外部的

- 頭燈

- 尾燈

- 日間行車燈(DRL)

- 霧燈

- 內部的

- 環境/腳部空間

- 屋頂/穹頂

- 外部的

- 透過技術

- 鹵素

- 氙氣燈/HID燈

- LED

- 雷射

- OLED

- 按銷售管道

- 目的地設備製造商 (OEM)

- 售後市場

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Koito Manufacturing Co. Ltd.

- Lumax Industries Limited

- Varroc Group

- HELLA GmbH & Co. KGaA

- UNO Minda Ltd.

- Valeo Lighting Systems India

- Marelli Automotive Lighting India

- Hyundai Mobis Co. Ltd.

- Osram India

- Philips Automotive Lighting India

- SL Corporation

- Motherson Sumi Systems(Samvardhana)

- JW Speaker

- Magneti Marelli Parts & Services India

- Bosch Limited-Lighting ECUs

- Texas Instruments India

第7章 市場機會與未來展望

According to Mordor Intelligence, the indian automotive lighting market size was valued at USD 1.73 billion in 2025 and is expected to increase from USD 1.83 billion in 2026 to reach USD 2.44 billion by 2031, growing at a CAGR of 5.87% over 2026-2031.

This report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, and Two-Wheelers), Application (Exterior and Interior), Technology (Halogen, Xenon/HID, LED, Laser, and OLED), and Sales Channel (OEM and Aftermarket). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

India Automotive Lighting Market Trends and Insights

LED Price Erosion and Energy-Efficiency Mandates

Declining component costs coupled with Bureau of Energy Efficiency thresholds have made LEDs the default fitment across price bands. OEM contracts now specify LEDs even for entry-level scooters to meet candela requirements without thermal penalties. Domestic suppliers that invested in automated surface-mount lines under the PLI scheme are capturing this shift, while halogen demand retreats to legacy replacement channels. The virtuous cost-volume cycle is compressing LED module prices toward parity with halogen assemblies, sealing the latter's obsolescence.

AIS-008 / AIS-012 Safety Regulations Enforcement

Type-approval audits for headlamps and signaling devices became more stringent in 2025. Tier-one suppliers with in-house photometric tunnels readily comply, whereas gray-market assemblers struggle to certify their products. Enforcement actions have already removed several non-conforming aftermarket lamps from urban retail shelves. Over time, sustained surveillance is expected to marginalize uncertified bulbs, improving lumen stability and color consistency on Indian roads.

High GST Slab and Import Duty on Advanced Lighting Modules

Combined levies exceeding 40% on imported complete units of laser and matrix-LED assemblies are dampening OEM enthusiasm for widespread adoption in the mass segment. While only luxury brands are shouldering the extra costs to provide long-range laser high beams, local joint ventures are hurrying to localize sub-assemblies. Their goal is to make premium features more affordable without the burden of duty inflation.

Other drivers and restraints analyzed in the detailed report include:

- Electrification Push Under FAME-LI Boosting 2-W and 4-W LED Fitment

- Tier-1 Localisation Incentives (PLI-Auto and Specs)

- LED-Driver Semiconductor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars constituted the largest 48.41% share of the Indian automotive lighting market in 2025, reflecting broad LED adoption across hatchbacks and sedans. In contrast, two-wheelers will grow the fastest, at a 6.01% CAGR, as newer scooters and motorcycles now feature automatic headlamp-on functions that mandate reliable solid-state lamps. Segment-specific regulations continue to elevate lighting content, making motorcycles a critical volume driver.

The regulatory tailwind encourages suppliers to customize compact LED modules for motorcycles that also meet splash-resistance norms for Indian monsoons. OEM design cycles have therefore shortened, as modular lamp housings allow brands to refresh aesthetics annually. While passenger cars continue to dominate value terms, accelerating scooter electrification firmly embeds two-wheelers in long-term growth narratives, balancing the market's segment mix without diluting unit profitability.

Exterior functions captured 63.21% of the Indian automotive lighting market in 2025, a lead cemented by daytime running lamps, adaptive front-lighting, and full-width tail bars that double as unmistakable brand signatures. OEM designers treat headlamps as "eyes" that must meet strict beam cutoff regulations while still packaging seamlessly into sculpted fascias. That dual imperative keeps exterior systems at the top of budget lists when engineering choices are made, ensuring incremental upgrades even in carry-over models. The 6.11% CAGR projected for exterior lamps also reflects planned rollouts of wider light bars whose continuous illumination improves conspicuity at dusk and during monsoon downpours.

Interior illumination, although smaller, now serves as a tactile differentiator in connected vehicles and electric cab-ins. Multi-zone RGB strips enable drivers to sync mood lighting with infotainment themes, turning the cabin ambiance into a software-defined experience. Vendors respond by shipping plug-and-play LED rails that integrate diffusers and CAN bus controllers into a single, slim form factor, reducing line assembly time. While exterior systems still dominate total value, expanding cabin-personalization menus ensure that interior orders rise in lockstep with higher trim penetrations. Suppliers see the two streams as complementary rather than competitive, since a single LIN-bus gateway can orchestrate both headlamp leveling and foot-well ambiance.

List of Companies Covered in this Report:

- Koito Manufacturing Co. Ltd.

- Lumax Industries Limited

- Varroc Group

- HELLA GmbH & Co. KGaA

- UNO Minda Ltd.

- Valeo Lighting Systems India

- Marelli Automotive Lighting India

- Hyundai Mobis Co. Ltd.

- Osram India

- Philips Automotive Lighting India

- SL Corporation

- Motherson Sumi Systems (Samvardhana)

- J.W. Speaker

- Magneti Marelli Parts & Services India

- Bosch Limited - Lighting ECUs

- Texas Instruments India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED-Price Erosion & Energy-Efficiency Mandates

- 4.2.2 AIS-008 / AIS-012 Safety Regulations Enforcement

- 4.2.3 Electrification Push Under Fame-LI Boosting 2-W & 4-W Led Fitment

- 4.2.4 Tier-1 Localization Incentives (PLI-Auto & Specs)

- 4.2.5 ADAS-Ready Adaptive Lighting Demand From Premium Oems

- 4.2.6 Smart-Corridor Pilots Enabling V2I-Linked Lighting

- 4.3 Market Restraints

- 4.3.1 High GST Slab & Import Duty On Advanced Lighting Modules

- 4.3.2 Prevalence Of Counterfeit Aftermarket Bulbs

- 4.3.3 LED-Driver Semiconductor Shortages

- 4.3.4 Low Consumer Awareness In Tier-2/3 Cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium & Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.1.1 Headlamps

- 5.2.1.2 Taillights

- 5.2.1.3 Daytime Running Lights (DRLs)

- 5.2.1.4 Fog Lamps

- 5.2.2 Interior

- 5.2.2.1 Ambient / Footwell

- 5.2.2.2 Roof / Dome

- 5.2.1 Exterior

- 5.3 By Technology

- 5.3.1 Halogen

- 5.3.2 Xenon / HID

- 5.3.3 LED

- 5.3.4 Laser

- 5.3.5 OLED

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Koito Manufacturing Co. Ltd.

- 6.4.2 Lumax Industries Limited

- 6.4.3 Varroc Group

- 6.4.4 HELLA GmbH & Co. KGaA

- 6.4.5 UNO Minda Ltd.

- 6.4.6 Valeo Lighting Systems India

- 6.4.7 Marelli Automotive Lighting India

- 6.4.8 Hyundai Mobis Co. Ltd.

- 6.4.9 Osram India

- 6.4.10 Philips Automotive Lighting India

- 6.4.11 SL Corporation

- 6.4.12 Motherson Sumi Systems (Samvardhana)

- 6.4.13 J.W. Speaker

- 6.4.14 Magneti Marelli Parts & Services India

- 6.4.15 Bosch Limited - Lighting ECUs

- 6.4.16 Texas Instruments India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車照明市場報告:按技術、車輛類型、銷售管道、應用和地區分類(2026-2034 年)

汽車照明市場報告:按技術、車輛類型、銷售管道、應用和地區分類(2026-2034 年) 2026年全球汽車輔助照明市場報告

2026年全球汽車輔助照明市場報告 汽車照明市場:2026-2032年全球市場預測(依產品類型、技術、車輛類型、應用和銷售管道分類)汽車周邊照明市場:依技術、銷售管道、車輛類型及應用分類-2026-2032年全球市場預測汽車外飾LED照明市場:依產品類型、安裝位置、乘用車及銷售管道分類-2026-2032年全球市場預測汽車高位煞車燈市場:按光源、車輛類型、驅動系統和銷售管道分類-2026-2032年全球市場預測下一代汽車照明市場:按產品類型、技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測

汽車照明市場:2026-2032年全球市場預測(依產品類型、技術、車輛類型、應用和銷售管道分類)汽車周邊照明市場:依技術、銷售管道、車輛類型及應用分類-2026-2032年全球市場預測汽車外飾LED照明市場:依產品類型、安裝位置、乘用車及銷售管道分類-2026-2032年全球市場預測汽車高位煞車燈市場:按光源、車輛類型、驅動系統和銷售管道分類-2026-2032年全球市場預測下一代汽車照明市場:按產品類型、技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測 道路反光器市場:按材料、應用和地區分類汽車鹵素燈泡市場:依產品類型、應用、車輛類型和通路分類,全球預測,2026-2032年

道路反光器市場:按材料、應用和地區分類汽車鹵素燈泡市場:依產品類型、應用、車輛類型和通路分類,全球預測,2026-2032年 汽車氣氛照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車氣氛照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)