|

市場調查報告書

商品編碼

2063265

高速公路駕駛輔助系統:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Highway Driving Assist - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

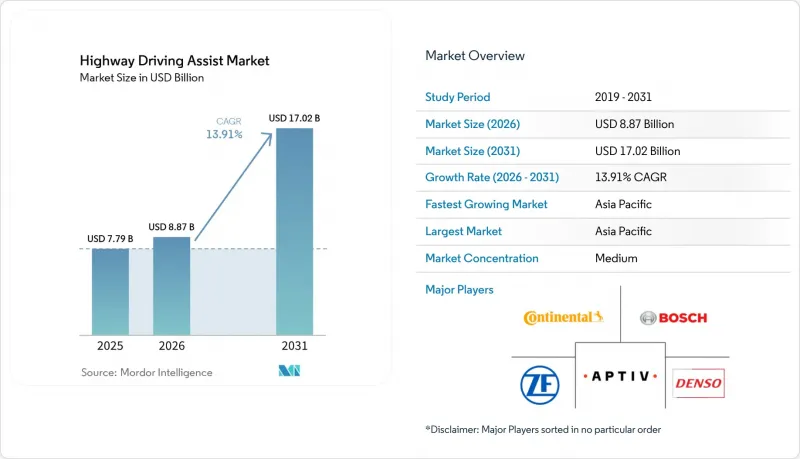

據 Mordor Intelligence 稱,2025 年高速公路駕駛輔助市場價值為 77.9 億美元,預計 2026 年將達到 88.7 億美元,到 2031 年將達到 170.2 億美元,2026 年至 2031 年的複合年成長率為 13.91%。

本報告按技術(主動式車距維持定速系統、車道維持系統等)、車輛類型(乘用車、輕型商用車等)、組件(感測器、攝影機系統、控制單元、軟體、雷達系統等)、應用(個人用途、車隊管理、共乘服務等)和地區進行細分。市場預測以價值(美元)表示。

全球高速公路駕駛輔助市場趨勢與洞察

監管安全要求和NCAP標準正在提高。

歐洲新車安全評鑑協會(Euro NCAP)將於2025年開始對駕駛輔助系統評級,這實際上強制要求主流車輛項目必須包含L2+等級的功能。美國國家公路交通安全管理局(NHTSA)的2024-2033年藍圖也遵循類似的路徑,將車道維持輔助和主動式車距維持定速系統添加到其基本的碰撞避免功能清單中。在中國,工業和資訊化部(工信部)已公佈2027年L3級安全法規草案,該草案符合ISO 21434和UNECE R155的要求,從而減輕了各國的工程負擔。 UNECE第29工作小組正在最終確定L3/L4框架,以協調60多個成員市場的型式認證。這些措施共同作用,將高速公路駕駛輔助功能從可選的便利功能轉變為強制性合規項目,從而縮短全球價值鏈的產品規劃週期。

汽車製造商對 L2/L2+ 功能的部署

在更嚴格的法規生效之前,製造商們正競相在其所有產品線中推廣L2級自動駕駛功能,高速公路駕駛輔助功能也正從高階配置轉變為展示室標配。領先採用者可以受益於通用平台間的軟體復用,從而實現從豪華旗艦車型到量產跨界車的快速過渡,而無需從頭開始重新設計整個車輛週期。基於訂閱的儀錶板可以顯示哪些駕駛輔助功能最受用戶歡迎,並驅動OTA空中升級,即時最佳化轉向和距離控制行為。這種回饋循環增強了工程優先順序與消費者體驗的契合度,並幫助品牌在硬體利潤率下降的情況下確保持續的數位收入。同時,標準化的功能集為保險公司提供了一致的遙測數據,透過增強折扣方案,進一步提高了原廠系統的採用率。

初始系統成本高

即使感測器價格下降,冗餘處理、高解析度地圖和網路安全認證的總成本仍可能使車輛價格增加數千美元,這給新興市場的可負擔價格帶來了壓力。入門級買家往往被迫在舒適性配置和高級駕駛輔助套件之間做出選擇,這減緩了高階市場以外的普及速度。車隊管理人員正在權衡微薄的營運利潤和投資回報,推遲部署,直到保險折扣和監管激勵措施能夠抵消資本支出。汽車製造商正在嘗試模組化方法,將基本的車道保持功能作為標準配置,而對自動變換車道等功能收費,但這種分級方法會割裂用戶體驗,並使行銷更加複雜。在系統總成本與大眾市場的價格水準相符之前,各地區的部署速度可能會持續存在差異。

細分市場分析

到2025年,主動式車距維持定速系統(ACC)將在高速公路駕駛輔助市場的技術構成比中佔比38.48%。其廣泛應用得益於雷達技術的通用性以及監管機構將縱向控制定位為基本安全層的努力。供應商目前正將此功能整合到成本最佳化的模組中,這些模組可與動力傳動系統和煞車ECU無縫整合,從而降低了在大眾市場平台上的整合門檻。隨著該功能成為標配,汽車製造商正將行銷重點從單純的技術規格轉向駕駛員監控的準確性和可靠的道路邊緣檢測。同時,先進的地圖介面支援持續的雲端校準,即使是入門車型也能保持符合不斷發展的車道居中標準。

自動變換車道功能正以17.62%的複合年成長率成長,是各技術領域中成長最快的。高階車型依靠此功能,透過免手動超車和協同併道邏輯來脫穎而出。在多車道場景中檢驗橫向自動駕駛的複雜性促使人們引入新的模擬工作流程,以在確保安全性的同時減少實際駕駛距離。隨著邊緣人工智慧的成熟,雲端部署的軟體堆疊也支援從基本的車道保持到預測性車道選擇的空中下載(OTA)功能增強。因此,市場呈現出兩極化的趨勢:傳統功能逐漸商品化,而訂閱式功能則維持了利潤率。

到2025年,乘用車將佔據高速公路駕駛輔助系統68.15%的市場。這主要歸功於大規模潛在市場中私人車輛的普遍擁有。該細分市場對高速公路駕駛輔助系統的採用,受到消費者對便利性的需求以及與風險評分掛鉤的保險獎勵不斷增加的雙重驅動。汽車製造商正利用現有的資訊娛樂管道,提升銷售更高級駕駛輔助模式的月度訂閱服務,從而在售後保持與客戶參與。隨著法規逐步強制要求在新車型中配備基礎型ADAS(高級駕駛輔助系統),消費者對某種形式的駕駛輔助系統的期望也日益增強。這些因素正在為半自動駕駛功能的普及奠定基礎。

中重型商用車市場以14.45%的複合年成長率快速發展,顯示車隊經濟效益正在加速技術進步。高速公路駕駛輔助系統能夠減少疲勞駕駛事故(長途運輸車輛的一項主要成本因素),並使車輛符合基於遠端資訊處理技術的保費折扣資格。可改裝的感測器模組使現有牽引車無需重新設計整個平台即可配備車道維持輔助和協同巡航控制功能,從而減少停機時間。駕駛員短缺進一步推動了這項技術的應用,因為自動駕駛功能可以在符合法律安全標準的前提下延長允許的駕駛時間。因此,供應商正在開發可與通用遠端資訊處理閘道整合的模組化套件,高速公路輔助功能已成為總擁有成本 (TCO) 規劃中的關鍵要素。

區域分析

預計到2025年,亞太地區將佔據高速公路駕駛輔助市場36.98%的佔有率,並將以15.09%的複合年成長率(CAGR)實現最快成長,直至2031年。在中國,路側V2X單元的部署以及對基於ISO標準的網路安全法規的遵守,正在減輕本地化的負擔並加速功能認證。日本正致力於為老年駕駛提供輔助,當地汽車製造商正在改進駕駛員交接警報系統,以反映人口結構的實際情況。韓國正利用其覆蓋全國的5G網路,在高速公路上推廣協同駕駛,這表明基礎設施建設是廣泛應用的基礎。在印度等新興市場,隨著本土製造商將成本最佳化的感測器陣列整合到熱門SUV車型中,大眾市場滲透的早期徵兆像已經顯現。

在北美,由美國國家公路交通安全管理局 (NHTSA)主導的標準協調工作正將核心駕駛輔助功能整合到主流安全設備中。訂閱經濟正在主導策略對話,各大汽車製造商正以試用付費轉換率作為關鍵指標來最佳化定價結構。保險公司正在降低檢驗的車道居中和駕駛員監控遙測數據的車輛的保費,從而形成良性循環,提高安裝率。與加拿大標準的跨境協調正在最大限度地減少型式認證的負擔,並實現北美地區統一的車輛規格。同時,售後改裝方案也正在獲得監管部門的批准,為老舊車隊加入高速公路駕駛輔助市場提供了新的途徑。

在歐洲,通用安全法規 (GSR) 的實施正取得進展,該法規強制要求新車型配備智慧速度輔助系統 (ISA) 和車道維持輔助系統 (LKA)。歐洲新車安全評鑑協會 (Euro NCAP) 評估標準的擴展鼓勵製造商追求超越標準的性能,以期獲得市場優勢。區域性汽車製造商正在封閉道路上試點 L3 級擁塞管理功能,利用地理圍欄技術收集使用數據,以便在符合監管規定的前提下進行未來擴展。與半導體供應狀況相關的供應鏈壓力促使企業與國內晶片製造商合作,並就供應鏈韌性問題展開對話。儘管歐洲的成長速度落後於亞太地區,但清晰的政策正在支持成員國的穩定發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 監管安全要求和NCAP標準正在提高。

- 汽車製造商引入L2/L2+功能。

- 降低雷達和攝影機的成本

- 訂閱式HDA服務的收入

- 利用群眾外包方式為車隊產生 5G 高清地圖

- 基於里程的保險(UBI)獎勵

- 市場限制因素

- 初始系統成本高

- 網路安全和OTA合規負擔

- ADAS人員短缺導致檢驗延誤。

- 惡劣天氣/車道品質造成的性能差異

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 主動式車距維持定速系統

- 車道維持輔助

- 自動變換車道

- 交通堵塞援助

- 避免碰撞

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 按組件

- 感應器

- 網路攝影系統

- 控制單元

- 軟體

- 雷達系統

- 按最終用途

- 個人使用

- 車隊管理

- 共乘服務

- 地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 西班牙

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- Mobileye Global Inc.

- Magna International

- Hyundai Mobis

- Aisin Corporation

- Autoliv Inc.

- Mando Corporation

- Infineon Technologies

- NVIDIA Corporation

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Hitachi Astemo

- Samsung Electronics

- Veoneer

第7章 市場機會與未來展望

According to Mordor Intelligence, the highway driving assist market size was valued at USD 7.79 billion in 2025, is projected to reach USD 8.87 billion in 2026, and is expected to reach USD 17.02 billion by 2031, growing at a CAGR of 13.91% from 2026 to 2031.

This report is Segmented by Technology (Adaptive Cruise Control, Lane Keeping Assist, and More), Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Component (Sensors, Camera System, Control Units, Software, and Radar Systems), End-Use (Personal Use, Fleet Management, and Ride-Sharing Service), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Highway Driving Assist Market Trends and Insights

Regulatory Safety Mandates and NCAP Upgrades

Euro NCAP started grading assisted-driving systems in 2025, effectively forcing Level 2+ capability into mainstream vehicle programs. NHTSA's 2024-2033 roadmap follows a similar path by adding Lane Keeping Assist and Adaptive Cruise Control to its baseline crash-avoidance menu. In China, draft Level 3 rules issued by MIIT for 2027 mirror the requirements of ISO 21434 and UNECE R155, reducing country-specific engineering overhead. UNECE Working Party 29 is finalizing Level 3/4 frameworks to harmonize homologation across more than 60 contracting markets. Together, these measures shift highway driving assist from an optional convenience to an essential compliance item, compressing product-planning cycles across the global value chain.

Automaker Roll-out of L2/L2+ Features

Manufacturers are racing to blanket their product lines with Level 2 functionality before stricter rules take effect, turning highway-assist from a premium perk into a showroom staple. Early movers benefit from software reuse across shared platforms, enabling rapid migration from luxury flagships to high-volume crossovers without restarting design cycles from scratch. Subscription dashboards also reveal which driver-assist elements attract the most engagement, guiding over-the-air updates that refine steering and distance-keeping behavior in real time. This feedback loop tightens alignment between engineering priorities and consumer experience, helping brands secure recurring digital revenue as hardware margins erode. In parallel, standardized feature sets provide insurers with consistent telemetry, reinforcing discounts that further stimulate take rates for factory-installed systems.

High Upfront System Cost

Even with cheaper sensors, the complete bill for redundant compute, high-definition maps, and cybersecurity certification can add thousands of dollars to a vehicle, straining affordability in emerging markets. Buyers of entry trims often confront a stark choice between comfort options and advanced assist packages, which tempers penetration outside premium segments. Fleet managers weigh the investment against tight operating margins, delaying adoption until insurance discounts or regulatory credits offset capital outlay. Automakers experiment with modular offerings that keep basic lane-keeping standard while paywalling automated lane change, but this tiering fragments the user experience and complicates marketing. Until total system cost aligns with mass-market price points, rollout speed will remain uneven across regions.

Other drivers and restraints analyzed in the detailed report include:

- Falling Radar and Camera Costs

- Subscription-based HDA Service Revenues

- Cyber-security and OTA Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adaptive Cruise Control accounted for 38.48% of the technology slice of the highway driving assist market in 2025. Its ubiquity stems from radar commoditization and regulatory nudges that treat longitudinal control as a baseline safety layer. Suppliers now embed the feature in cost-optimized modules that integrate seamlessly with power-train and braking ECUs, reducing integration friction for mass-market platforms. As the function becomes standard, automakers are shifting their marketing focus away from raw specifications toward driver-monitoring fidelity and robust road-edge detection. In parallel, advanced mapping interfaces allow continuous cloud calibration, keeping even entry vehicles compliant with evolving lane-center standards.

Automated Lane Change is growing at a 17.62% CAGR, the fastest pace within the technology hierarchy. Premium trims rely on the feature to distinguish themselves through hands-free overtaking and cooperative merge logic. The complexity of validating lateral autonomy across multi-lane scenarios has prompted new simulation workflows that cut physical-drive mileage while preserving safety claims. Cloud-deployed software stacks also enable over-the-air expansion from basic lane-keeping to predictive lane selection once edge AI maturity allows. Consequently, a bifurcated pattern is emerging where legacy functions commoditize, while subscription-gated capabilities sustain margin headroom.

Passenger cars accounted for 68.15% of the highway driving assist market share in 2025, owing to the dominance of private ownership in large addressable markets. Highway driving assist adoption in this segment mirrors consumer appetite for convenience, blended with rising insurance incentives tied to risk scores. Automakers leverage established infotainment channels to upsell monthly subscriptions that unlock higher-order assist modes, maintaining engagement well past the initial sale. As regulations progressively require basic ADAS in new models, consumer expectations are also normalizing around some form of hands-on driver support. This baseline sets the stage for increased acceptance of semi-autonomous capabilities.

Medium and heavy commercial vehicles, advancing at a 14.45% CAGR, illustrate how fleet economics can accelerate technology turnover. Highway assist reduces fatigue-related incidents, a major cost factor for long-haul operators, and qualifies assets for telematics-based insurance rebates. Retrofit-ready sensor pods enable existing tractors to gain lane-keeping and cooperative cruise control without a full platform redesign, reducing downtime. Driver-shortage pressures further strengthen the case as automated functions extend allowable operating hours within legal safety envelopes. As a result, suppliers are curating modular kits that integrate with prevalent telematics gateways, turning highway assist into a line item in total-cost-of-ownership planning.

Geography Analysis

Asia-Pacific held 36.98% of the highway driving assist market in 2025 and is set to post the fastest climb at a 15.09% CAGR through 2031. China's rollout of roadside V2X units and its alignment with ISO-based cybersecurity rules reduce localization burdens and unlock rapid feature certification. Japan focuses on elderly-driver assistance, prompting local OEMs to refine takeover alerts that resonate with demographic realities. South Korea scales cooperative cruise on expressways using nationwide 5G coverage, illustrating how infrastructure readiness underpins adoption. Emerging economies such as India see early signs of mass-market penetration as domestic manufacturers integrate cost-optimized sensor suites into popular SUV lines.

North America benefits from NHTSA-driven harmonization that inserts core assist functions into the safety mainstream. Subscription economics dominate strategic dialogues, with major automakers using trial-to-paid conversion metrics to refine pricing ladders. Insurers lower premiums for vehicles that provide verifiable lane-centering and driver-monitoring telemetry, creating a virtuous feedback loop that boosts installation rates. Cross-border alignment with Canadian standards minimizes homologation overhead, enabling unified North American vehicle specifications. Meanwhile, aftermarket retrofits gain regulatory recognition, opening a secondary channel for older vehicle fleets to join the momentum of the highway driving assist market.

Europe advances under the General Safety Regulation, which mandates Intelligent Speed Assistance and Lane Keeping Assist on new vehicle types. Euro NCAP's expanded metrics spur manufacturers to exceed baseline compliance in pursuit of marketing leverage. Regional OEMs pilot Level 3 traffic-jam features on controlled-access roads, using geofencing to stay within regulatory comfort zones while collecting usage data for future expansions. Supply-chain stresses related to semiconductor availability encourage partnerships with domestic chipmakers and foster dialogue on resilience. Although growth trails Asia-Pacific, Europe's policy clarity underpins steady scale-up across member states.

- Robert Bosch

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- Mobileye Global Inc.

- Magna International

- Hyundai Mobis

- Aisin Corporation

- Autoliv Inc.

- Mando Corporation

- Infineon Technologies

- NVIDIA Corporation

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Hitachi Astemo

- Samsung Electronics

- Veoneer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Safety Mandates and NCAP Upgrades

- 4.2.2 Automaker Roll-out of L2/L2+ Features

- 4.2.3 Falling Radar and Camera Costs

- 4.2.4 Subscription-based HDA Service Revenues

- 4.2.5 5G HD-map Crowd-sourcing for Fleets

- 4.2.6 Usage-based-insurance (UBI) Incentives

- 4.3 Market Restraints

- 4.3.1 High Upfront System Cost

- 4.3.2 Cyber-security and OTA Compliance Burden

- 4.3.3 ADAS Talent Shortage Delaying Validation

- 4.3.4 Poor-weather / Lane-quality Performance Gaps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Technology

- 5.1.1 Adaptive Cruise Control

- 5.1.2 Lane Keeping Assist

- 5.1.3 Automated Lane Change

- 5.1.4 Traffic Jam Assist

- 5.1.5 Collision Avoidance

- 5.2 By Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Light Commercial Vehicle

- 5.2.3 Medium and Heavy Commercial Vehicle

- 5.3 By Component

- 5.3.1 Sensors

- 5.3.2 Camera System

- 5.3.3 Control Units

- 5.3.4 Software

- 5.3.5 Radar Systems

- 5.4 By End-Use

- 5.4.1 Personal Use

- 5.4.2 Fleet Management

- 5.4.3 Ride-Sharing Service

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 Spain

- 5.5.3.4 Italy

- 5.5.3.5 France

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Aptiv PLC

- 6.4.6 Valeo SA

- 6.4.7 Mobileye Global Inc.

- 6.4.8 Magna International

- 6.4.9 Hyundai Mobis

- 6.4.10 Aisin Corporation

- 6.4.11 Autoliv Inc.

- 6.4.12 Mando Corporation

- 6.4.13 Infineon Technologies

- 6.4.14 NVIDIA Corporation

- 6.4.15 NXP Semiconductors

- 6.4.16 Texas Instruments

- 6.4.17 Renesas Electronics

- 6.4.18 Hitachi Astemo

- 6.4.19 Samsung Electronics

- 6.4.20 Veoneer

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

高速公路駕駛輔助市場:2026-2032年全球市場預測(依感測器類型、自動化程度、車輛類型、應用和銷售管道)摩托車主動式車距維持定速系統市場:按感測器類型、車輛類型、安裝類型和最終用戶分類-2026-2032年全球市場預測

高速公路駕駛輔助市場:2026-2032年全球市場預測(依感測器類型、自動化程度、車輛類型、應用和銷售管道)摩托車主動式車距維持定速系統市場:按感測器類型、車輛類型、安裝類型和最終用戶分類-2026-2032年全球市場預測 2026年全球主動車距控制巡航系統和盲點偵測市場報告2026年全球高速公路駕駛輔助市場報告主動式車距維持定速系統系統市場:按感測器類型、車輛類型、技術類型和銷售管道分類 - 2026-2032年全球預測2026年全球車道居中控制系統市場報告智慧車載駕駛員監控系統市場:按組件、技術、安裝類型、車輛類型和應用分類,全球預測(2026-2032年)車道維持系統控制設備市場按車輛類型、組件、感測器類型、分銷管道和自動化程度分類 - 全球預測(2026-2032 年)

2026年全球主動車距控制巡航系統和盲點偵測市場報告2026年全球高速公路駕駛輔助市場報告主動式車距維持定速系統系統市場:按感測器類型、車輛類型、技術類型和銷售管道分類 - 2026-2032年全球預測2026年全球車道居中控制系統市場報告智慧車載駕駛員監控系統市場:按組件、技術、安裝類型、車輛類型和應用分類,全球預測(2026-2032年)車道維持系統控制設備市場按車輛類型、組件、感測器類型、分銷管道和自動化程度分類 - 全球預測(2026-2032 年) 高速公路駕駛輔助系統市場規模、佔有率和成長分析(按技術、組件、車輛類型、銷售管道和地區分類)—產業預測(2026-2033 年)

高速公路駕駛輔助系統市場規模、佔有率和成長分析(按技術、組件、車輛類型、銷售管道和地區分類)—產業預測(2026-2033 年) 自適應巡航控制和盲點偵測市場-全球產業規模、佔有率、趨勢、機會和預測(按車輛類型、銷售管道、地區和競爭格局分類)。 2021-2031年預測

自適應巡航控制和盲點偵測市場-全球產業規模、佔有率、趨勢、機會和預測(按車輛類型、銷售管道、地區和競爭格局分類)。 2021-2031年預測