|

市場調查報告書

商品編碼

2063263

風力發電機基礎:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Wind Turbine Foundation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

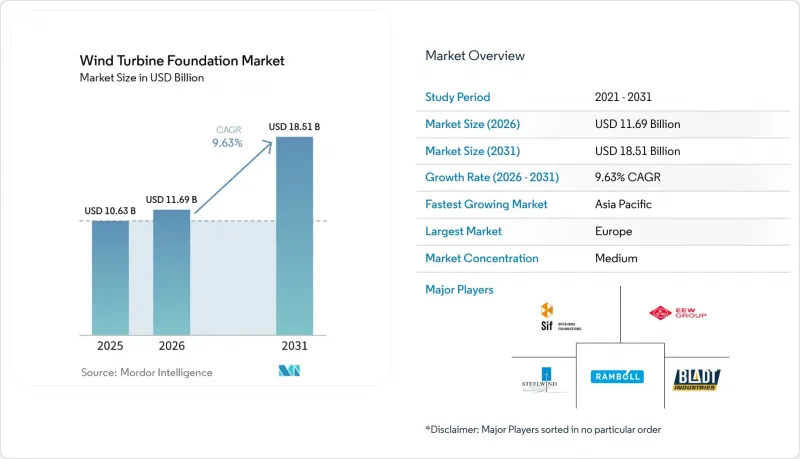

據 Mordor Intelligence 稱,2025 年風力發電機基礎市場價值為 106.3 億美元,預計到 2031 年將達到 185.1 億美元,而 2026 年為 116.9 億美元,預測期(2026-2031 年)的複合年成長率為 9.63%。

本報告按基礎類型(重力式結構、其他)、材質(混凝土、鋼材、複合材料/混合材料)、安裝地點(陸上、其他)、渦輪機額定功率(小於2兆瓦、其他)、最終用途(公用事業規模、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球風力發電機基礎市場趨勢及洞察

在全球淨零排放目標下,離岸風力發電電場建設快速擴張

2025年至2026年間,除2024年已運作的83吉瓦離岸風電裝置容量外,各國政府為實現2050年碳中和目標,拍賣了約100吉瓦的離岸風力發電裝置容量。光是歐洲的「REPowerEU」計畫就設定了2050年實現300吉瓦離岸風電裝置容量的目標,而美國《通貨膨脹控制法案》對清潔能源的獎勵,則使專案的內部收益率(IRR)提高了3個百分點。中國的「十四五」規劃目標是到2030年實現50吉瓦的離岸風力發電,這推動了國內離岸風電建設項目規模超過產能。為此,超大型單樁的前置作業時間已延長至 24 個月,迫使開發商必須提前預訂到 2029 年的工期。像 Sif Group 這樣擁有自動化生產線和深水碼頭的製造商正在獲得高價,其 2026 會計年度的 EBITDA 預測顯示,其同比成長率將達到 181%。

15兆瓦或以上的渦輪機需要超大型的基礎。

新一代風力渦輪機產生的推力負荷比10兆瓦機型高出40%,迫使單樁基礎的尺寸擴大到直徑10公尺、長度120公尺、重量2400噸。港口深度成為瓶頸,目前只有埃斯比雅爾、不來梅港、阿布爾西頓和馬斯弗拉克特二號港口能夠容納超過10公尺的單樁基礎。 EEW和CS Wind提前交付了Nordlicht 1專案的首批單樁基礎,證明機器人焊接能夠在100公尺的長度上將尺寸公差控制在5毫米以內。目前,該領域的競爭力取決於能夠軋延厚度超過120毫米鋼板的鋼廠以及整合即時品管的製造商。 RWE公司計劃在2028年獲得32萬噸鋼板,這表明大規模買家正在迅速鎖定有限的產能。

深海浮體式解決方案需要高額資本投資。

浮體式基礎的成本約為每兆瓦340萬歐元,其中平台製造和運輸費用高達140萬美元,安裝和錨碇費用高達450萬美元。由於船舶租賃費用為每天23.4萬美元至35.1萬美元,且每個單元的安裝需要10至15天,因此安裝成本比固定式項目高出50%至70%。目前浮體式電站的平準化發電成本超過每千瓦時0.20美元,DNV預測到2050年,這一成本將逐步下降至每兆瓦時67美元,這意味著短期內資金籌措困難仍將持續。港口維修將進一步增加成本。光是在美國西岸,在開始大規模組裝工作之前,就需要至少12億美元用於新建綜合碼頭和起重設施。在總資本成本降至每兆瓦 292 萬美元以下之前,大多數浮體式項目仍將局限於日本、蘇格蘭和加州的補貼試點地區。

細分市場分析

至2025年,單樁基礎將佔風力發電機基礎市場55.4%的佔有率,證明其在水深60公尺以內的水域具有成本效益。然而,隨著水深超過100公尺的浮動式風力發電的擴展,半潛式基礎預計將以27.8%的複合年成長率成長。

導管架基礎在亞太地區日益受到關注,在沃旭能源(Orsted)的「大燦華」計畫中,導管架基礎成功將工期縮短了20%。在挪威,重力式基礎正在復興,目標是減少80%的二氧化碳排放。浮體式基礎,例如日本11.7吉瓦的競標和蘇格蘭BW Ideol公司的管道驅動項目,目前已投入運作中234兆瓦,另有244吉瓦正在規劃中。 BW Ideol公司的「傾卸池」和Principle Power公司的「風力浮體」等創新技術,將效率提高並縮短安裝時間高達60%,標誌著基礎技術的重大變革。

截至2025年,鋼材將佔風力發電機基礎市場67.1%的佔有率,反映出其成熟的供應鏈和高強度重量比。然而,鋼板價格飆升(2026年3月達到每短噸1115美元)以及碳邊境調節稅(到2027年將額外增加每噸58至93美元的負擔),正促使開發商轉向更環保的材料。複合材料和混合基礎雖然目前佔比不高,但在歐盟循環經濟法規的推動下,預計到2031年將以14.4%的複合年成長率成長。歐盟循環經濟法規要求在退役時回收70%的材料。混合鋼-混凝土半潛式結構,例如BW Ideol公司的“阻尼池”,可減少40%的隱含排放,並簡化退役後的拆除工作。 REFRESH 測試表明,回收的玻璃纖維氈的性能與原生材料相當,可作為吸收劑,用於吸收預計到 2050 年將產生的 2500 萬噸刀片廢棄物。

重力式混凝土基礎正重新受到關注。模組化模板允許在內陸進行澆築,隨後透過駁船拖運,從而避免了超大型單樁因吃水深度限制而導致的物流難題。 Peikko 的「Cage Rock」岩石錨定系統在 Flatnahagi 風力發電機組中減少了 15% 的混凝土用量和 17% 的鋼筋用量,提高了小規模島嶼地區電網的經濟效益。 Dillinger 的「PURE STEEL+」系列產品計劃於 2027-2028 年發布,旨在與傳統鋼板相比減少 55-60% 的二氧化碳排放,這表明即使是老牌鋼鐵製造商也在向低碳供應轉型。隨著碳定價的收緊,開發商將權衡初始成本與未來的碳排放回收額度,從而擴大採購選擇。因此,儘管鋼材仍將保持其數量優勢,但複合材料和混合解決方案將推動風力發電機基礎市場的下一階段成長。

區域分析

到2025年,歐洲將佔全球風力發電機基礎市場37.2%的佔有率。這得歸功於北海地區風電建設的增加以及埃斯比耶和不來梅港港口設施的擴建。在埃斯比耶,航道加深至12.8公尺並擴建了聯合碼頭,使得裝載直徑超過10公尺的單樁成為可能。德國的Gennaker和Windanker計畫共需80多個超大型(XXL)基礎,而英國的Dogger Bank和Hornsea 3計畫則需要250多個。 Sif集團位於馬斯弗拉克特第二期的工廠每年生產200個單樁,確保歐洲在2030年之前擁有充足的產能。 OustEd公司在大彰化地區引入的吸力桶式導管架目前正在考慮應用於對噪音敏感的北海地區。

亞太地區是成長最快的地區,預計到2031年將以13.6%的複合年成長率成長,穩步擴大風力發電機基礎市場規模。在中國,廣東省已運作23.5吉瓦風電,江蘇省已投入營運11.3吉瓦風電,兩省均在向15兆瓦及以上的大型風力發電機過渡,需要厚度超過120毫米的鋼板。 2026年1月,台灣在大莊化2b和4號風電場完成了66個吸水桶導管架的建造,顯示當地船廠能夠承建複雜的網狀結構。日本在2025年獲得了四個區域共11.7吉瓦的發電裝置容量,並計劃在水深超過100公尺的海域採用半潛式結構。韓國GS Entec公司計劃在2026年初將其單樁產能翻番,以滿足來自越南和菲律賓的出口訂單。

儘管北美在裝置容量方面落後於其他地區,但其沿美國東海岸擁有5.8吉瓦的強勁項目儲備,並且該地區正在擴大其在風力發電機基礎市場的佔有率。 Empire Wind和維吉尼亞 Offshore Wind計畫在2025年前聯合安裝230個超大型單樁基礎,但由於聯邦政府的停工令,建設工作暫時中止,導致資金籌措差距擴大。加州一個4.6吉瓦的浮體式租賃計畫將使需求轉向半潛式平台,其成本約為每兆瓦397萬美元。加拿大計畫在2030年實現5吉瓦的離岸風力發電裝置容量,而巴西和摩洛哥已分別獲得超過1吉瓦的環境許可。這些新興項目表明,北美和一些新興市場正在穩步縮小與成熟的歐洲和亞洲中心之間的差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在全球淨零排放目標下,離岸風力發電建設快速擴張

- 渦輪機輸出功率超過 15MW 時,需要 XXL 尺寸的基礎。

- 平準化能源成本的下降提高了開發商的投資報酬率。

- 大量生產的模組化混凝土基礎消除了港口瓶頸。

- 利用數位雙胞胎進行岩地工程建模正在加速客製化設計。

- 對可回收基礎材料的需求

- 市場限制因素

- 用於深海應用的浮體式解決方案需要高資本投入

- 全球範圍內,厚度超過120毫米的鋼板供不應求。

- 因水深港導致超大型單樁工程物流延誤

- 殘值責任不明確推高了資金籌措成本。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依基礎類型

- 重力結構

- 單樁

- 夾克

- 三腳架

- 半潛式

- 其他

- 材料類型

- 具體的

- 鋼

- 複合材料/混合材料

- 按安裝位置

- 陸上

- 離岸

- 固定離岸

- 浮體式海上

- 渦輪機額定功率(容量)

- 小於2兆瓦

- 2~5 MW

- 超過5兆瓦

- 按最終用途

- 公用事業規模

- 商業和工業用途

- 住宅及微電網

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 芬蘭

- 瑞典

- Tukey

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 越南

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 埃及

- 摩洛哥

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- Ramboll Group A/S

- Sif Group

- Bladt Industries A/S

- EEW Group

- BW Ideol

- Principle Power, Inc.

- DEME Offshore

- Boskalis

- Navantia-Windar

- Harland & Wolff

- Peikko Group

- Balltec Ltd.

- BFG International

- Steelwind Nordenham GmbH

- Seaway 7

- Van Oord

- Jan De Nul

- Lamprell

- Smulders

第7章 市場機會與未來展望

According to Mordor Intelligence, the wind turbine foundation market size was valued at USD 10.63 billion in 2025 and is estimated to grow from USD 11.69 billion in 2026 to reach USD 18.51 billion by 2031, at a CAGR of 9.63% during the forecast period (2026-2031).

This report is Segmented by Foundation Type (Gravity-Based Structure, Others), Material Type (Concrete, Steel, Composite/Hybrid), Installation Site (Onshore, Others), Turbine Rating (Below 2 MW, Others), End-Use Application (Utility-Scale, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wind Turbine Foundation Market Trends and Insights

Rapid Offshore Wind-Farm Build-Out Under Global Net-Zero Targets

Governments pursuing mid-century carbon neutrality auctioned roughly 100 GW of offshore wind capacity during 2025-2026 on top of the 83 GW already operating in 2024. Europe's REPowerEU blueprint alone eyes 300 GW by 2050, while the U.S. Inflation Reduction Act's clean-energy incentives lift project IRRs by up to three percentage points. China's 14th Five-Year Plan calls for 50 GW of offshore wind by 2030, fueling a domestic build programme that eclipses fabrication capacity. In response, lead times for XXL monopiles have stretched to 24 months, pushing developers to reserve slots through 2029. Fabricators with automated lines and deep-water quays, such as Sif Group, whose FY 2026 EBITDA guidance jumped 181% year on year, are securing premium pricing.

Turbine Ratings ≥15 MW Demanding XXL Foundations

Next-generation turbines generate thrust loads 40% above 10 MW models, forcing monopiles to 10 m diameters, 120 m lengths, and 2,400 t weights. Port depth is the chokepoint; only Esbjerg, Bremerhaven, Able Seaton, and Maasvlakte II currently handle >10 m monopiles. EEW and CS Wind delivered early Nordlicht 1 monopiles ahead of schedule, confirming that robotized welding keeps dimensional tolerances within 5 mm across 100 m lengths. The segment's competitive edge now rests on mills able to roll >120 mm plate and fabricators that integrate real-time QC. RWE's reservation of 320,000 t of plate through 2028 illustrates how large buyers are vacuuming up scarce capacity.

High CAPEX for Deep-Water Floating Solutions

Floating foundations cost about EUR 3.4 million per megawatt, of which platform fabrication and transport represent up to USD 1.4 million, and installation plus mooring add as much as EUR 4.5 million. Vessel charters range from USD 234,000 to USD 351,000 per day and can last 10-15 days per unit, so installation expenses run 50-70% above fixed-bottom projects. Current floating levelized energy prices exceed USD 0.20 per kilowatt-hour, and DNV foresees only a gradual fall to USD 67 per megawatt-hour by 2050, keeping bankability challenging in the near term. Port upgrades intensify the bill; the U.S. West Coast alone needs at least USD 1.2 billion for new integration quays and crane capacity before large-scale assembly can start. Until total capital costs drop below USD 2.92 million per megawatt, most floating projects will remain limited to subsidized pilot zones in Japan, Scotland, and California.

Other drivers and restraints analyzed in the detailed report include:

- Falling LCOE Boosting Developer ROI

- Mass-Produced Modular Concrete Bases Cutting Port Bottlenecks

- Limited Global Supply of Greater than 120 mm Steel Plate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The monopile segment accounted for 55.4% of the wind turbine foundation market size in 2025, underscoring its cost efficiency in depths to 60 m. Semi-submersibles, however, are poised to register a 27.8% CAGR as floating wind scales in >100 m waters.

Jacket foundations are gaining traction in Asia-Pacific, with Orsted's Greater Changhua project achieving 20% faster schedules. Gravity-based structures are resurging in Norway, targeting an 80% carbon reduction. Floating foundations, driven by Japan's 11.7-gigawatt auction and Scotland's BW Ideol pipeline, represent 234 megawatts operationally, with a 244-gigawatt pipeline. Innovations like BW Ideol's Damping Pool and Principle Power's WindFloat enhance efficiency, reducing installation time by up to 60%, signaling a significant shift in foundation technologies.

Steel owned 67.1% of the wind turbine foundation market share in 2025, reflecting mature supply chains and high strength-to-weight performance. Yet escalating steel-plate prices that hit USD 1,115 per short ton in March 2026 and carbon-border levies that will add USD 58-93/t by 2027 are nudging developers toward greener mixes. Composite and hybrid foundations, though smaller in absolute volume, are forecast to grow at a 14.4% CAGR to 2031, driven by EU circular-economy rules that demand 70% material recovery at decommissioning. Hybrid steel-concrete semi-submersibles such as BW Ideol's Damping Pool offer 40% lower embodied emissions and simplified end-of-life dismantling. REFRESH trials showed recycled glass-fiber mats that match virgin properties and create a sink for the 25 Mt blade waste expected by 2050.

Concrete gravity bases are gaining a fresh lease because modular molds allow inland casting followed by barge tow-out, which bypasses draft limits that hamper XXL monopile logistics. Peikko's Cage Rock rock-anchored system cut concrete volume 15% and reinforcement 17% at Flatnahagi, improving economics for small island grids. Dillinger's PURE STEEL+ line, launching 2027-2028, targets 55-60% CO2 reduction relative to conventional plate, signaling that even incumbent steel players are hedging with low-carbon supply. As carbon pricing tightens, developers will weigh upfront cost against future salvage credits, leading to a broader procurement palette. Consequently, while steel keeps its numeric lead, composite and hybrid solutions will carve the next leg of growth in the wind turbine foundation market.

Geography Analysis

Europe commanded 37.2% of the global wind turbine foundation market share in 2025, underpinned by the North Sea build-out and upgraded ports in Esbjerg and Bremerhaven. Esbjerg deepened its fairway to 12.8 m and expanded the Combi-Terminal, enabling load-out of monopiles larger than 10 m in diameter. Germany's Gennaker and Windanker projects together need more than 80 XXL foundations, while the United Kingdom's Dogger Bank and Hornsea 3 require over 250 units. Sif Group's Maasvlakte II plant produces 200 monopiles a year, giving Europe ample fabrication headroom through 2030. Suction-bucket jackets deployed at Orsted's Greater Changhua site are now being evaluated for noise-sensitive North Sea zones.

Asia-Pacific is the fastest-growing region, advancing at a 13.6% CAGR to 2031 and steadily lifting the wind turbine foundation market size. China already operates 23.5 GW in Guangdong and 11.3 GW in Jiangsu, both shifting to 15 MW and larger turbines that need plates thicker than 120 mm. Taiwan completed 66 suction-bucket jackets at Greater Changhua 2b & 4 in January 2026, proving that local yards can handle complex lattice work. Japan awarded 11.7 GW of capacity across four zones in 2025 and is counting on semi-submersibles for depths beyond 100 m. South Korea's GS Entec is doubling monopile capacity by early 2026 to serve export orders to Vietnam and the Philippines.

North America trails in installations yet holds a robust 5.8 GW pipeline along the U.S. East Coast, giving the region a growing share of the wind turbine foundation market size. Empire Wind and Coastal Virginia Offshore Wind together installed 230 XXL monopiles in 2025, but federal stop-work orders briefly halted construction and raised financing spreads. California's 4.6 GW of floating leases will pivot demand toward semi-submersible platforms that cost about USD 3.97 million per megawatt. Canada plans 5 GW of offshore capacity by 2030, while Brazil and Morocco have each cleared over 1 GW in environmental permits. These emerging pipelines suggest that North America and selected frontier markets will steadily close the gap with established European and Asian hubs.

- Ramboll Group A/S

- Sif Group

- Bladt Industries A/S

- EEW Group

- BW Ideol

- Principle Power, Inc.

- DEME Offshore

- Boskalis

- Navantia-Windar

- Harland & Wolff

- Peikko Group

- Balltec Ltd.

- BFG International

- Steelwind Nordenham GmbH

- Seaway 7

- Van Oord

- Jan De Nul

- Lamprell

- Smulders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid offshore wind-farm build-out under global net-zero targets

- 4.2.2 Turbine ratings Above 15 MW demanding XXL foundations

- 4.2.3 Falling LCOE boosting developer ROI

- 4.2.4 Mass-produced modular concrete bases cutting port bottlenecks

- 4.2.5 Digital-twin geotechnical modelling accelerating custom design

- 4.2.6 Demand for recyclable foundation materials

- 4.3 Market Restraints

- 4.3.1 High CAPEX for deep-water floating solutions

- 4.3.2 Limited global supply of greater than 120 mm steel plate

- 4.3.3 Shallow-draft ports delaying XXL monopile logistics

- 4.3.4 Unclear salvage liability inflating finance costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Foundation Type

- 5.1.1 Gravity-Based Structure

- 5.1.2 Monopile

- 5.1.3 Jacket

- 5.1.4 Tripod

- 5.1.5 Semi-submersible

- 5.1.6 Others

- 5.2 By Material Type

- 5.2.1 Concrete

- 5.2.2 Steel

- 5.2.3 Composite/Hybrid

- 5.3 By Installation Site

- 5.3.1 Onshore

- 5.3.2 Offshore

- 5.3.2.1 Fixed-Bottom Offshore

- 5.3.2.2 Floating Offshore

- 5.4 By Turbine Rating (Capacity)

- 5.4.1 Below 2 MW

- 5.4.2 2 to 5 MW

- 5.4.3 Above 5 MW

- 5.5 By End-Use Application

- 5.5.1 Utility-Scale

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential and Micro-grid

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Russia

- 5.6.2.6 Finland

- 5.6.2.7 Sweden

- 5.6.2.8 Tukey

- 5.6.2.9 Netherlands

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Vietnam

- 5.6.3.7 Rest of Asia Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Egypt

- 5.6.5.4 Morocco

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ramboll Group A/S

- 6.4.2 Sif Group

- 6.4.3 Bladt Industries A/S

- 6.4.4 EEW Group

- 6.4.5 BW Ideol

- 6.4.6 Principle Power, Inc.

- 6.4.7 DEME Offshore

- 6.4.8 Boskalis

- 6.4.9 Navantia-Windar

- 6.4.10 Harland & Wolff

- 6.4.11 Peikko Group

- 6.4.12 Balltec Ltd.

- 6.4.13 BFG International

- 6.4.14 Steelwind Nordenham GmbH

- 6.4.15 Seaway 7

- 6.4.16 Van Oord

- 6.4.17 Jan De Nul

- 6.4.18 Lamprell

- 6.4.19 Smulders

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment