|

市場調查報告書

商品編碼

2063260

電容器組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Capacitor Bank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

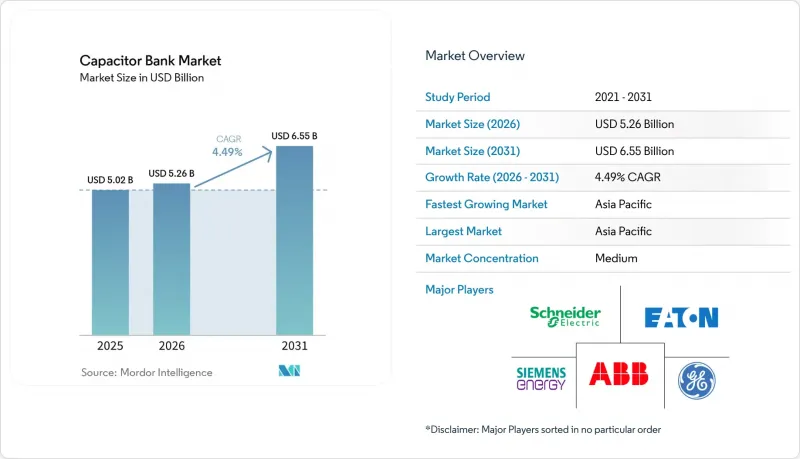

根據 Mordor Intelligence 預測,電容器組市場預計將從 2025 年的 50.2 億美元成長到 2026 年的 52.6 億美元,到 2031 年達到 65.5 億美元,2026 年至 2031 年的複合年成長率為 4.49%。

本報告按類型(戶外變電站、其他)、電壓等級(10 kV 以下低壓、10–69 kV 中壓、69 kV 以上高壓)、應用(功率因數校正、其他)、最終用戶(公共產業、商業、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球電容器組市場趨勢與洞察

電網現代化和分散式能源(DER)的引入

全球電力公司正在加強電網建設,以適應來自屋頂太陽能、社區儲能系統和大型可再生能源的雙向電流。光是MISO的2025年計畫就撥款123億美元用於432個項目,其中包括在明尼蘇達州和愛荷華州的變電站新增或遷移97兆瓦時的電容器容量。南加州愛迪生公司正在其配電饋線上部署自動化電容器組控制設備,以管理分散式太陽能發電帶來的日間電壓突波。 EverSource Energy已在2028年前累計162億美元,部分用於升級無功功率調度系統,以實現二次電平切換,從而適應來自表後儲能系統的電力注入。這些項目正在將電容器組市場從“更新周期”轉變為“擴展週期”,因為現在每個新的饋線段都需要現場無功功率支援。提供帶有SCADA介面以及狀態監測和診斷功能的承包機殼的供應商,在與電網營運商簽訂多年合約方面佔據優勢。

電動車充電基礎設施快速成長

快速充電樁的功率因數僅0.85,迫使電力公司在連接負載超過1兆瓦時強制要求現場補償。 IEEE現場測試表明,一台350千瓦的充電樁會消耗100千伏安的無功功率,相當於20戶家庭的無功功率需求。加州獨立系統營運商(CAISO)2025-2026年的調查報告指出,需要在灣區的兩條70千伏特線路上安裝串聯電容器,以解決充電所造成的電壓下降問題。因此,房地產開發商正在購買低壓電容器櫃,這些電容器櫃無需等待電力公司調查即可在數週內運作。Schneider Electric和伊頓公司在這個細分市場展開了激烈的交付競賽。隨著電動車普及速度的加快,兩個市場機會正在湧現:電力公司正在採購中壓電容器組用於饋線電壓穩定,而充電網路營運商則正在採購模組化單元用於充電站安裝。

MLCC供應鏈的波動也對薄膜電容器造成了影響。

對人工智慧伺服器的需求推動多層陶瓷電容器(MLCC)的生產轉向更高容量等級,導致薄膜電容器的金屬化產能下降。 Supplyframe 的數據顯示,MLCC 的前置作業時間在 2024 年初將達到 52 週,而 TTI 的報告顯示,薄膜電容器的前置作業時間將在 2025 年底達到 19 週。這比疫情前水準增加了 46%。沒有戰略採購合約的小規模電容器組組裝正面臨元元件短缺和專案運作延誤的問題。雙重採購和長期批量採購合約是緩解這一問題的關鍵,但這些優勢只有一級供應商才能享有,區域性專業製造商難以獲得。

細分市場分析

預計到2025年,金屬機殼組件在電容器組中的市場佔有率將擴大,年複合成長率將達到5.7%,因為都市區電力公司優先考慮緊湊型、防火設備。由於農村變電站土地資源豐富,戶外安裝仍佔所有安裝量的42.7%,但由於環境法規日益嚴格,其成長速度正在放緩。電線杆裝置在農村饋線中仍然很受歡迎,因為電力線路工人無需進行基礎施工即可維護。其他移動式或貨櫃式電容器組則用於建築工地和礦山的臨時電網擴容,從而為可在幾天內完成安裝的即插即用型櫃體創造了一個利基市場。

加州、德國和新加坡的城市化進程正在加速對與開關設備安裝在同一位置的室內設計方案的需求。在加州普萊恩菲爾德變電站,為了符合野火法規,2026年3月新增了兩個5兆乏的金屬封閉式電容器組。這表明,更高的資本投入可以透過避免設置防火來帶來抵銷。供應商正透過不銹鋼機殼、電弧故障排氣功能和整合式繼電器面板來凸顯自身優勢。雖然類型選擇通常基於電壓,但將室外電抗器與封閉式電容器組結合的混合變電站正逐漸成為兼顧成本最佳化的中間方案。

預計到2025年,中壓電容器組(10 kV至69 kV)的銷售額將佔總銷售額的47.9%,複合年成長率(CAGR)為4.8%。這反映了它們在饋線電壓調節和風電場電力收集系統中的重要作用。低壓電容器組(10 kV以下)主要應用於資料中心和醫院等建築級電壓校正,在這些場所,設施管理人員而非電力工程師主導採購決策。隨著STATCOM和串聯電容器在輸電線路走廊的應用日益普及,高壓電容器組(69 kV以上)的成長速度將放緩,但在電力電子設備維護基礎設施匱乏的偏遠變電站,其需求依然強勁。

隨著分散式能源(DER)資源日益豐富,中壓設備用電容器組的市場規模預計將穩步擴大,因為每個新增饋線都需要多級電容器組來穩定電壓。同時,在人口稀少的沙漠和山區等STATCOM經濟效益不高的地區,高壓電容器組仍佔有重要地位。隨著電力公司在現有IEC 60871標準的基礎上增加新的規範,提供具有增強抗震設計和網路安全措施的控制器的供應商正在不斷擴大市場佔有率。

區域分析

預計到2025年,亞太地區將佔全球銷售額的45.2%,並在2031年之前維持5.2%的複合年成長率,這主要得益於中國超高壓電網的擴建以及印度可再生能源走廊的建設。位於中國的嘉峪關-寧盛混合儲能專案於2025年12月投入運作,該專案正是混合儲能趨勢的典型例證,其採用電容器組管理穩態無功功率,並利用超級電容處理瞬態無功功率。印度電網公司與日立能源公司簽署的30台765千伏變壓器採購契約,凸顯了印度電網的持續擴容,而電網擴容需要大量的並聯容量。

在北美,中壓自動補償器(STATCOM)的應用基礎已較為成熟,但由於受監管的公共產業核准流程漫長,其成長速度較為緩慢。中西部獨立系統營運商(MISO)2025年123億美元的擴建計畫仍包括數十個中壓電容器組,而太平洋煤氣電力公司(PG&E)的普萊恩菲爾德計畫將新增10兆瓦時的室內裝置容量,以滿足野火預防法規的要求。德克薩斯州和維吉尼亞的資料中心建設催生了對低壓自動補償器的需求,但輸電線路走廊中STATCOM的替換限制了這項需求的成長。

儘管動態補償器是歐洲離岸風力發電網的首選,但德國和斯堪的納維亞的都市區電力公司仍在為空間受限的變電站購買中壓電容器組。英國天然氣和電力市場管理局(Ofgem)將網路收費翻倍,迫使英國工業用戶安裝現場電容器組以避免罰款。 L&T參與北海高壓直流輸電樞紐項目,預示未來換流站並聯電容器的訂單將會增加。

南美洲和中東仍是小眾市場,主要受巴西可再生能源競標和沙烏地阿拉伯儲能競標的推動。由於受價格規定推遲續約,供應商正專注於工業電氣化專案和電池儲能夥伴關係,並將無功補償支援整合到EPC總承包方案中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電網現代化和分散式能源(DER)引入的擴大

- 電動車充電基礎設施快速成長

- 熱密集型產業的電氣化

- 加重對違反電力品質標準的電力公司的處罰。

- 幹聚丙烯薄膜的技術進步

- 人工智慧驅動的電容器組預測性切換

- 市場限制因素

- MLCC供應鏈的波動也對薄膜電容器造成了影響。

- 價格管制地區公共產業投資週期放緩

- 油浸電容器火災後的恢復

- STATCOM 和 SVC 之間的競爭加劇

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 戶外變電站

- 金屬密封變電站

- 電線杆安裝型

- 其他

- 電壓等級

- 低電壓(低於10千伏特)

- 中壓(10-69千伏特)

- 高壓(69千伏特或更高)

- 透過使用

- 功率因數改善

- 諧波濾波器

- 電壓調節

- 可再生能源的整合

- 工業應用

- 資料中心

- 其他

- 最終用戶

- 公用事業

- 商業

- 產業

- 住宅

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- ABB Ltd

- Siemens Energy AG

- Schneider Electric SE

- Eaton Corporation plc

- General Electric Co.

- Arteche Group

- Larsen & Toubro Limited

- Hitachi Energy Ltd

- Mitsubishi Electric Corp.

- Toshiba Energy Systems & Solutions

- CG Power & Industrial Solutions

- Hyosung Heavy Industries

- Nissin Electric Co. Ltd

- Trench Group(Siemens)

- Kondas Elektrik Kapasitor

- ZEZ Silko sro

- FRANKLIN Grid Solutions

- Enerlux Power SRL

- Samwha Electric Co. Ltd

- Cooper Power Systems(Eaton)

第7章 市場機會與未來展望

According to Mordor Intelligence, the capacitor bank market size is expected to increase from USD 5.02 billion in 2025 to USD 5.26 billion in 2026 and reach USD 6.55 billion by 2031, growing at a CAGR of 4.49% over 2026-2031.

This report is Segmented by Type (Open Air Substation, Others), Voltage Class (Low-Voltage Below 10 KV, Medium-Voltage 10 To 69 KV, High-Voltage Above 69 KV), Application (Power Factor Correction, Others), End-User (Utilities, Commercial, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Capacitor Bank Market Trends and Insights

Grid-modernization & DER build-out

Utilities worldwide are hardening grids to accommodate bidirectional flows from rooftop solar, community batteries, and utility-scale renewables. MISO's 2025 plan alone earmarks USD 12.3 billion for 432 projects that include 97 MVAr of new or relocated capacitor capacity across Minnesota and Iowa substations. Southern California Edison is embedding automated capacitor-bank controllers across its distribution feeders to manage midday voltage climb caused by distributed photovoltaics. Eversource Energy has budgeted USD 16.2 billion through 2028, with a portion dedicated to var-dispatch upgrades that allow second-level switching in response to behind-the-meter storage injections. These programs convert the capacitor bank market from a replacement cycle to an expansion cycle because each new feeder section now needs local var support. Suppliers offering turnkey enclosures with SCADA interfaces and health-monitoring diagnostics are positioned to win multiyear framework agreements with transmission system operators.

Surge in EV Charging Infrastructure

Fast chargers impose lagging power factors as low as 0.85, forcing utilities to mandate on-site compensation when connected load exceeds 1 MW. IEEE field tests show a 350 kW charger can draw 100 kVAr, equivalent to the reactive demand of 20 homes. CAISO's 2025-2026 study specifies series-capacitor insertion on two 70 kV corridors to counteract Bay-Area charging-related voltage sag. Property developers, therefore, purchase low-voltage capacitor cabinets that commission in weeks without utility studies, a niche where Schneider Electric and Eaton compete on delivery speed. As vehicle adoption accelerates, a dual-channel opportunity emerges: utilities procure medium-voltage banks for feeder stiffening, while charging-network operators buy modular units for depot installations.

MLCC supply-chain volatility spilling into film capacitors

AI-server demand pulled multilayer ceramic capacitor (MLCC) production toward high-capacitance grades, reducing metallization capacity for film devices. Supplyframe recorded 52-week MLCC lead times in early 2024, and TTI reported film-capacitor lead times stretching to 19 weeks in late 2025, up 46% from pre-pandemic norms. Smaller capacitor-bank assemblers without strategic sourcing contracts face component shortages that delay project commissioning. Mitigation hinges on dual-sourcing and long-term volume agreements, advantages enjoyed by Tier 1 vendors but not readily available to regional specialists.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Heat-Intensive Industries

- Rising Power-Quality Penalties from Utilities

- Slow Utility Cap-Ex Cycles in Price-Controlled Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal-enclosed assemblies accounted for a growing slice of the capacitor bank market in 2025 and are projected to grow at a 5.7% CAGR as urban utilities prioritize compact, fire-rated gear. Open-air yards still represent 42.7% of installations because rural substations have ample land, but their growth lags under tightening environmental constraints. Pole-mounted units remain popular in rural feeders where linemen can service equipment without pad construction. Other mobile or containerized banks address temporary grid reinforcement at construction sites and mines, creating a niche for plug-and-play cabinets that deploy within days.

Urban densification in California, Germany, and Singapore accelerates demand for indoor-rated designs that co-locate with switchgear. The Plainfield substation in California added two 5 MVAr metal-enclosed banks in March 2026 to meet wildfire regulations, illustrating how the capital premium is offset by avoided containment berms. Suppliers differentiate through stainless-steel housings, arc-fault venting, and integrated relay panels. Although type choice often aligns with voltage, hybrid yards that mix open-air reactors with enclosed capacitor steps are emerging as a cost-optimized middle ground.

Medium-voltage banks (10 kV-69 kV) generated 47.9% of revenue in 2025 and are forecast to expand at 4.8% CAGR, reflecting their role in feeder voltage regulation and wind-farm collector systems. Low-voltage units (< 10 kV) dominate building-level corrections in data centers and hospitals, where facility managers rather than utility engineers drive purchase decisions. High-voltage banks (> 69 kV) grow slowly as STATCOMs and series capacitors gain favor in transmission corridors, yet they persist in remote substations lacking the maintenance bandwidth for power electronics.

The capacitor bank market size for medium-voltage equipment is projected to rise steadily because each new DER-rich feeder requires multi-step banks to stabilize voltage. Conversely, high-voltage banks defend pockets where STATCOM economics falter, such as sparsely populated deserts or mountain passes. Vendors offering seismic-rated designs and cybersecurity-hardened controllers capture share as utilities layer new specifications onto legacy IEC 60871 compliance.

Geography Analysis

Asia-Pacific generated 45.2% of 2025 revenue and will sustain a 5.2% CAGR through 2031 as China extends its ultra-high-voltage network and India builds renewable corridors. China's Jiayuguan NingSheng hybrid storage project, commissioned in December 2025, illustrates the hybridization trend in which capacitor banks manage steady-state vars while supercapacitors address transients. India's Power Grid contract with Hitachi Energy for 30 units of 765 kV transformers underscores continued grid expansion that necessitates substantial shunt capacitance.

North America grows more slowly because the installed base is mature, and regulated utilities follow lengthy approval cycles. MISO's USD 12.3 billion 2025 expansion plan still contains dozens of medium-voltage banks, and PG&E's Plainfield project adds 10 MVAr of enclosed capacity to meet wildfire-hardening rules. Data-center buildouts in Texas and Virginia create demand for low-voltage automatic banks, but STATCOM substitution limits upside in transmission corridors.

Europe favors dynamic compensators for offshore wind integration, yet urban utilities in Germany and the Nordics still procure medium-voltage banks for space-constrained substations. Ofgem's doubled network charges push U.K. industrial customers to install on-site banks and avoid penalties. L&T's involvement in North Sea HVDC hubs signals future orders for converter-station shunt capacitors.

South America and the Middle East remain niche, driven by renewable auctions in Brazil and storage tenders in Saudi Arabia. Tariff-constrained utilities defer replacements, so vendors focus on industrial electrification projects and battery-storage partnerships that bundle var support into EPC packages.

- ABB Ltd

- Siemens Energy AG

- Schneider Electric SE

- Eaton Corporation plc

- General Electric Co.

- Arteche Group

- Larsen & Toubro Limited

- Hitachi Energy Ltd

- Mitsubishi Electric Corp.

- Toshiba Energy Systems & Solutions

- CG Power & Industrial Solutions

- Hyosung Heavy Industries

- Nissin Electric Co. Ltd

- Trench Group (Siemens)

- Kondas Elektrik Kapasitor

- ZEZ Silko s.r.o.

- FRANKLIN Grid Solutions

- Enerlux Power SRL

- Samwha Electric Co. Ltd

- Cooper Power Systems (Eaton)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-modernisation & DER build-out

- 4.2.2 Surge in EV charging infrastructure

- 4.2.3 Electrification of heat-intensive industries

- 4.2.4 Rising power-quality penalties from utilities

- 4.2.5 Breakthroughs in dry-type polypropylene film

- 4.2.6 AI-enabled predictive switching of capacitor banks

- 4.3 Market Restraints

- 4.3.1 MLCC supply-chain volatility spilling into film capacitors

- 4.3.2 Slow utility cap-ex cycles in price-controlled regions

- 4.3.3 Fire-event recalls in oil-impregnated banks

- 4.3.4 Increasing competition from STATCOMs & SVCs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Open air substation

- 5.1.2 Metal enclosed substation

- 5.1.3 Pole mounted

- 5.1.4 Others

- 5.2 By Voltage Class

- 5.2.1 Low-Voltage (Below 10 kV)

- 5.2.2 Medium-Voltage (10 to 69 kV)

- 5.2.3 High-Voltage (Above 69 kV)

- 5.3 By Application

- 5.3.1 Power factor correction

- 5.3.2 Harmonic filter

- 5.3.3 Voltage regulation

- 5.3.4 Renewable integration

- 5.3.5 Industrial application

- 5.3.6 Data centers

- 5.3.7 Others

- 5.4 By End-User

- 5.4.1 Utilities

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Residential

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Siemens Energy AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Eaton Corporation plc

- 6.4.5 General Electric Co.

- 6.4.6 Arteche Group

- 6.4.7 Larsen & Toubro Limited

- 6.4.8 Hitachi Energy Ltd

- 6.4.9 Mitsubishi Electric Corp.

- 6.4.10 Toshiba Energy Systems & Solutions

- 6.4.11 CG Power & Industrial Solutions

- 6.4.12 Hyosung Heavy Industries

- 6.4.13 Nissin Electric Co. Ltd

- 6.4.14 Trench Group (Siemens)

- 6.4.15 Kondas Elektrik Kapasitor

- 6.4.16 ZEZ Silko s.r.o.

- 6.4.17 FRANKLIN Grid Solutions

- 6.4.18 Enerlux Power SRL

- 6.4.19 Samwha Electric Co. Ltd

- 6.4.20 Cooper Power Systems (Eaton)

7 Market Opportunities & Future Outlook

全球電容器組市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電容器組市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球電容器組市場報告(2026 年)

全球電容器組市場報告(2026 年) 電容器組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按電壓、類型、安裝方式、應用、地區和競爭格局分類,2021-2031年)

電容器組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按電壓、類型、安裝方式、應用、地區和競爭格局分類,2021-2031年) 全球電容器組市場:市場規模、佔有率、趨勢分析(按電壓、應用和地區)、展望和預測(2025-2032 年)

全球電容器組市場:市場規模、佔有率、趨勢分析(按電壓、應用和地區)、展望和預測(2025-2032 年) 全球中壓電容器組市場中壓電容器組市場 - 全球產業規模、佔有率、趨勢、機會和預測,按階段、按類型、按應用、按冷卻方法、按地區、按競爭進行細分,2020-2030 年全球低壓電容器組市場全球電容器組市場

全球中壓電容器組市場中壓電容器組市場 - 全球產業規模、佔有率、趨勢、機會和預測,按階段、按類型、按應用、按冷卻方法、按地區、按競爭進行細分,2020-2030 年全球低壓電容器組市場全球電容器組市場 低壓電容器組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

低壓電容器組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2032 年電容器組市場預測:按類型、電壓、安裝、連接類型、應用、最終用戶和地區進行的全球分析

2032 年電容器組市場預測:按類型、電壓、安裝、連接類型、應用、最終用戶和地區進行的全球分析