|

市場調查報告書

商品編碼

2063245

太陽能電力控制系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Solar Sunlight Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

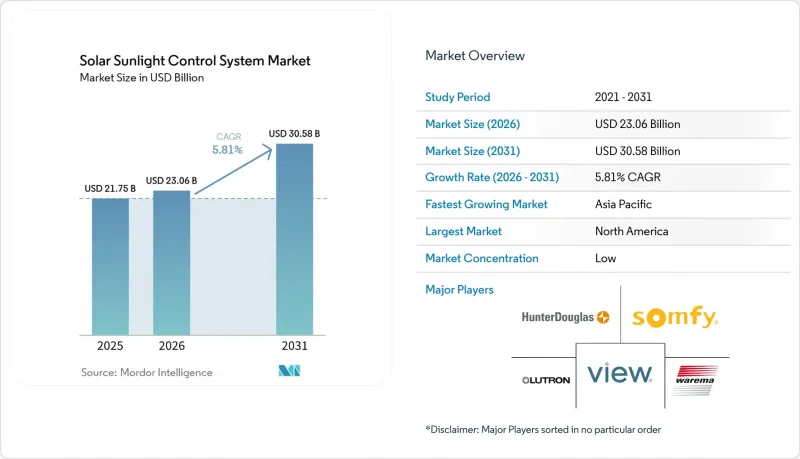

據 Mordor Intelligence 稱,2025 年太陽能控制系統市場規模為 217.5 億美元,預計到 2031 年將達到 305.8 億美元,而 2026 年為 230.6 億美元,預測期(2026-2031 年)複合年成長率為 5.81%。

本報告按產品類型(例如,手動太陽能控制系統)、技術(例如,光電感測器)、組件(例如,執行器)、安裝類型(新建和維修)、應用(例如,住宅)以及地區(北美、歐洲、亞太地區以及中東和非洲)進行細分。市場預測以美元計價。

全球太陽能控制系統市場趨勢及洞察

綠色建築更嚴格的能源標準提高了對採光和外觀的性能要求。

全球建築法規現已納入日光照明指標和太陽熱增益限制,實際上強制要求採用動態遮陽和電致變色玻璃。 ASHRAE 90.1-2022 提高了可見光透射率基準值,而歐盟修訂後的《建築能源性能指令》將維修目標提高了一倍,並將自動遮陽納入國家建築標準。中國的 GB/T 50378-2019 高度重視採用智慧太陽輻射控制的項目,這表明太陽能控制系統市場正逐漸確立其地位,不再僅僅是可選的升級選項,而是核心設計考量。

商業地產向動態嵌裝玻璃過渡,提升健康水平和能源效率

隨著動態嵌裝玻璃取代百葉窗,房東們反映租金上漲,入住率也更快。 GREYSTAR 的「Exo Apartments」公寓在安裝了 View 的智慧窗戶後,入住率達到 100% 的時間縮短了 80%,無眩光的自然光提升了公寓對租戶的吸引力。 Kilroy Realty 透過利用 View 的網路平台,每年為其旗下所有物業節省了 100 萬美元的能源成本。聖戈班的「SageGlass RealTone」智慧玻璃將於 2025 年推出,其四個調光區域的設計將滿足居住者對更清晰視野的需求,進一步推動智慧玻璃的普及。

智慧玻璃和電動簾子的初始成本較高

電致變色玻璃比普通Low-E低輻射鍍膜玻璃貴15%到25%,這意味著外觀預算每平方英尺要增加50到150美元,這阻礙了中檔專案的實施。手動百葉窗每扇窗戶的成本為50到150美元,而電動簾子每扇窗戶的成本為300到800美元,這導致東南亞和南美的開發商為了降低成本而將其排除在設計之外。雖然總擁有成本(TCO)模型顯示投資回收期為5到10年,但對前期成本的敏感度仍是一個障礙。

細分市場分析

預計到2025年,自動遮陽系統將佔銷售額的45.3%,顯示電氣化已提前成為主流。同時,智慧控制系統預計到2031年將以12.0%的複合年成長率成長,是整個太陽能控制系統市場成長率的兩倍多。如今,買家不僅關注功能,也關注預測智慧,智慧產品線融合了雲端分析、人工智慧演算法和開放API,從而實現了SaaS收費。因此,傳統的手動產品目前僅在對價格敏感的維修項目和電力供應不穩定的地區仍有需求。

智慧平台也正在改變毛利率結構,因為軟體年費的成長速度超過了硬體成本的下降速度。例如,Lutron 的 Athena 雲端服務按平方英尺收取訂閱費,其費用甚至超過了其馬達攤銷後的成本。這清楚地表明,未來利潤的基礎將是分析能力,而非機械部件。隨著專案規範越來越要求與 BACnet、Matter 或藍牙 Mesh 相容,智慧控制供應商在確保互通性和網路安全方面正獲得優勢。

由於光電感測器易於使用且物料清單成本低,預計到2025年將佔銷售額的40.0%。但隨著建築物業主越來越需要從單一設備獲取熱載入資料和人員佔用數據,預計到2031年,紅外線感測器的年複合成長率將達到11.1%。 IEEE在2025年進行的現場試驗表明,基於LoRa的紅外線節點在保持99.2%網路運轉率的同時,將電池壽命延長了80%,直接解決了曾經限制無線技術普及的維護問題。

此外,紅外線陣列可將即時熱圖資料傳輸至人工智慧引擎,在使用者感到不適前幾秒調整遮陽簾。因此,成組的熱感測器可以緩解暖通空調(冷暖氣空調)系統由此產生的負載激增。正因如此,儘管單價上漲了10%,生命科學實驗室和資料中心仍在採用它們。 Matter和Zigbee 3.0等無線協定在晶片層面整合了安全金鑰,促使買家接受無線技術的可靠性,並進一步縮小了有線光電環路的市場佔有率。

區域分析

預計到2025年,北美將佔全球銷售額的33.4%。稅額扣抵成為主流配置。加州和紐約州嚴格的州級建築規範收緊了太陽能熱增益的年度上限,這推動了太陽能控制系統市場在強制性性能標準下持續成長。稅收政策的確定性(直至2032年)有利於更長期的開發平臺,而豐富的智慧建築專業知識正在加速維修專案的轉型。

預計到2031年,亞太地區的複合年成長率將達到6.7%,成為所有地區中成長最快的地區。這主要歸功於中國、印度和東南亞國協將日光照明標準納入建築許可。中國的GB/T 50378-2019標準對具備智慧遮陽功能的專案給予最高評級,各大開發人員都在競相獲得此項認證以確保更高的租金。在印度,將於2024年實施的修訂版《節能建築標準》規定,炎熱乾燥地區的新建辦公大樓的太陽熱增益係數必須低於0.25,這實際上強制要求採用動態嵌裝玻璃。隨著都市化進程的推進和高層建築數量的增加,自動化帷幕牆解決方案正變得至關重要。

在歐洲,旨在2030年將大規模維修數量翻倍的「翻新浪潮」舉措正在進行中。聖戈班的「波爾多智慧校園」等計畫展現了電致變色技術的擴充性,而不斷上漲的人事費用使得自動化遮陽系統比手動百葉窗更具成本效益。拉丁美洲和中東地區仍維持著個位數的中段成長率,但低於全球平均。在沙烏地阿拉伯和阿拉伯聯合大公國,不斷上漲的空調能源成本推動了遮陽自動化的發展,而在巴西和阿根廷,經濟不穩定限制了其大規模應用。整體而言,在全球區域政策趨於一致、氣候目標與經濟獎勵日益契合的推動下,太陽能控制系統市場呈現上升趨勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 綠建築能源標準的日益嚴格提高了對採光和外觀的性能要求。

- 為了提高健康和節約能源,商業房地產正在轉型為動態嵌裝玻璃。

- 住宅維修期間,節能窗簾的需求激增。

- 美國《通貨膨脹控制法》規定,電致變色智慧窗戶稅額扣抵(ITC)。

- 人工智慧驅動的預測性遮陽軟體可在不到 3 年的時間內實現投資回報。

- 以健康為中心的認證系統(WELL、Fitwel)評估晝夜節律照明管理

- 市場限制因素

- 智慧玻璃和電動簾子的初始成本較高

- 複雜維修工程缺乏技術純熟勞工

- 多層智慧薄膜的可回收性低,導致其在使用過程中出現責任問題。

- 物聯網連接的遮陽網路面臨的網路安全威脅

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 手動太陽輻射控制系統

- 自動太陽輻射控制系統

- 智慧控制系統

- 透過技術

- 光電感測器

- 熱感應器

- 紅外線感測器

- 無線技術

- 按組件

- 執行器

- 控制器

- 感應器

- 軟體解決方案

- 其他

- 按安裝類型

- 新安裝

- 維修工程

- 透過使用

- 住宅

- 商業的

- 產業

- 農業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Hunter Douglas

- Somfy Systems

- Lutron Electronics

- Warema Renkhoff SE

- View Inc.

- Saint-Gobain(SageGlass)

- 3M Company

- Eastman Chemical(LLumar/Solar Gard)

- Guardian Industries

- Kawneer Company

- Griesser AG

- ABB Ltd.

- Siemens AG

- Johnson Controls International

- Skyco Shading Systems

- Pleotint LLC

- EControl-Glas GmbH

- Smartglass International

- Heliotrope Technologies

- Renson Sun Protection Screens

第7章 市場機會與未來展望

According to Mordor Intelligence, the solar sunlight control system market size was valued at USD 21.75 billion in 2025 and is estimated to grow from USD 23.06 billion in 2026 to reach USD 30.58 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031).

This report is Segmented by Product Type (Manual Solar Control Systems and More), Technology (Photoelectric Sensors, and More), Component (Actuators, and More), Installation Type (New Installations and Retrofit Installations), Application (Residential, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Solar Sunlight Control System Market Trends and Insights

Stricter Green-Building Energy Codes Elevating Daylight & Facade Performance Requirements

Building regulations worldwide now embed daylight metrics and solar-heat-gain caps, effectively mandating dynamic shading or electrochromic glazing. ASHRAE 90.1-2022 raises visible-transmittance thresholds, while the EU's Energy Performance of Buildings Directive recast doubles renovation targets and pushes automated shading into national codes. China's GB/T 50378-2019 awards higher ratings to projects with intelligent sunlight control, locking the Solar sunlight control system market into core design considerations rather than optional upgrades.

Commercial Real-Estate Shift Toward Dynamic Glazing for Wellness & Energy Savings

Landlords report rent premiums and faster lease-ups when dynamic glazing replaces blinds. GREYSTAR's Exo Apartments reached full occupancy 80% faster after installing View Smart Windows, linking glare-free daylight to tenant appeal. Kilroy Realty cut annual energy spend by USD 1 million across properties using View's networked platform. Saint-Gobain's 2025 launch of SageGlass RealTone with four tint zones satisfies occupant preference for view clarity, further boosting adoption.

High Upfront Cost of Smart Glass & Motorized Shading

Electrochromic glazing commands a 15%-25% premium over static low-E glass, adding USD 50-USD 150 per ft2 to facade budgets and deterring mid-market projects. Motorized shades cost USD 300-USD 800 per window versus USD 50-USD 150 for manual blinds, prompting developers in Southeast Asia and South America to value-engineer them out. Although total-cost-of-ownership models yield 5- to 10-year paybacks, first-cost sensitivity remains a hurdle.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Residential Retrofits Seeking Energy-Efficient Window Coverings

- U.S. Inflation Reduction Act's 30%-50% ITC for Electrochromic Smart Windows

- Skilled-Labour Shortage for Complex Retrofit Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated shading captured 45.3% of 2025 revenue, illustrating the early mainstreaming of motorization, yet smart control systems are forecast to expand at a 12.0% CAGR to 2031, more than twice the overall Solar sunlight control system market pace. Buyers now judge value on predictive intelligence rather than motion alone, and the smart tier embeds cloud analytics, AI algorithms, and open APIs that unlock SaaS billing. Consequently, legacy manual products remain relevant only in price-sensitive retrofits and regions with unreliable power.

Smart platforms also reshape gross-margin profiles because annual software fees rise faster than hardware costs fall. Lutron's Athena cloud service, for example, charges per-square-foot subscriptions that exceed the amortized cost of its motors, underscoring how analytics rather than mechanics anchor future profits. As project specifications increasingly require BACnet, Matter, or Bluetooth mesh compatibility, smart control vendors win on interoperability and cybersecurity assurances.

Photoelectric sensors held 40.0% of 2025 revenue because of familiarity and low BOM costs, but infrared sensing will climb at an 11.1% CAGR through 2031 as building owners demand thermal-load and occupancy data in one device. A 2025 IEEE field trial showed LoRa-based infrared nodes sustaining 99.2% network uptime while extending battery life by 80%, directly addressing maintenance concerns that once limited wireless adoption.

Infrared arrays also feed real-time heat-map data to AI engines, enabling shading adjustments seconds before occupants perceive discomfort. Thermal-sensor bundles therefore reduce HVAC spikes, which is why life-science laboratories and data centers specify them despite the 10% unit premium. As wireless protocols such as Matter and Zigbee 3.0 embed security keys at the silicon level, buyers accept wireless reliability, further tipping the share away from wired photoelectric loops.

Geography Analysis

North America retained 33.4% of 2025 revenue as the IRA's 30%-50% investment tax credit pushed electrochromic glazing into mainstream specifications. State-level stretch codes in California and New York tighten solar-heat-gain caps annually, ensuring the Solar sunlight control system market continues to grow on mandated performance thresholds. Tax certainty through 2032 encourages longer development pipelines, and abundant smart-building expertise accelerates retrofit conversions.

Asia-Pacific will record a 6.7% CAGR to 2031, the fastest regional trajectory, because China, India, and ASEAN economies embed daylight metrics into occupancy permits. China's GB/T 50378-2019 standard awards premium ratings to projects with intelligent shading, and tier-1 developers chase that label to secure higher lease rates. India's 2024 update of the Energy Conservation Building Code forces new offices in hot-dry zones to achieve solar-heat-gain coefficients below 0.25, effectively mandating dynamic glazing. As urbanization pushes skyscraper counts higher, automated facade solutions become indispensable.

Europe benefits from the Renovation Wave initiative, which aims to double deep retrofit rates by 2030. Projects such as Saint-Gobain's Smart Campus Bordeaux showcase electrochromic scalability, while high labor costs make automation more cost-effective than manual blinds. Latin America and the Middle East trail global averages yet still log mid-single-digit growth; cooling-energy premiums in Saudi Arabia and the UAE motivate shade automation, whereas economic volatility tempers large-scale adoption in Brazil and Argentina. Collectively, regional policy convergence places the Solar sunlight control system market on a worldwide upswing that aligns climate targets with financial incentives.

- Hunter Douglas

- Somfy Systems

- Lutron Electronics

- Warema Renkhoff SE

- View Inc.

- Saint-Gobain (SageGlass)

- 3M Company

- Eastman Chemical (LLumar/Solar Gard)

- Guardian Industries

- Kawneer Company

- Griesser AG

- ABB Ltd.

- Siemens AG

- Johnson Controls International

- Skyco Shading Systems

- Pleotint LLC

- EControl-Glas GmbH

- Smartglass International

- Heliotrope Technologies

- Renson Sun Protection Screens

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter green-building energy codes elevating daylight & facade performance requirements

- 4.2.2 Commercial real-estate shift toward dynamic glazing for wellness & energy savings

- 4.2.3 Surge in residential retrofits seeking energy-efficient window coverings

- 4.2.4 U.S. Inflation Reduction Act's 30-50 % ITC for electrochromic smart windows

- 4.2.5 AI-driven predictive shading software delivering <3-year payback

- 4.2.6 Health-centric certifications (WELL, Fitwel) rewarding circadian-light management

- 4.3 Market Restraints

- 4.3.1 High upfront cost of smart glass & motorised shading

- 4.3.2 Skilled-labour shortage for complex retrofit installations

- 4.3.3 Limited recyclability of multi-layer smart films creating EoL liabilities

- 4.3.4 Cyber-security threats to IoT-connected shading networks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Manual Solar Control Systems

- 5.1.2 Automated Solar Control Systems

- 5.1.3 Smart Control Systems

- 5.2 By Technology

- 5.2.1 Photoelectric Sensors

- 5.2.2 Thermal Sensors

- 5.2.3 Infrared Sensors

- 5.2.4 Wireless Technology

- 5.3 By Component

- 5.3.1 Actuators

- 5.3.2 Controllers

- 5.3.3 Sensors

- 5.3.4 Software Solutions

- 5.3.5 Others

- 5.4 By Installation Type

- 5.4.1 New Installations

- 5.4.2 Retrofit Installations

- 5.5 By Application

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.5.4 Agriculture

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Hunter Douglas

- 6.4.2 Somfy Systems

- 6.4.3 Lutron Electronics

- 6.4.4 Warema Renkhoff SE

- 6.4.5 View Inc.

- 6.4.6 Saint-Gobain (SageGlass)

- 6.4.7 3M Company

- 6.4.8 Eastman Chemical (LLumar/Solar Gard)

- 6.4.9 Guardian Industries

- 6.4.10 Kawneer Company

- 6.4.11 Griesser AG

- 6.4.12 ABB Ltd.

- 6.4.13 Siemens AG

- 6.4.14 Johnson Controls International

- 6.4.15 Skyco Shading Systems

- 6.4.16 Pleotint LLC

- 6.4.17 EControl-Glas GmbH

- 6.4.18 Smartglass International

- 6.4.19 Heliotrope Technologies

- 6.4.20 Renson Sun Protection Screens

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

太陽輻射控制玻璃市場:全球市場按產品類型、銷售管道和應用分類的預測,2026-2032年

太陽輻射控制玻璃市場:全球市場按產品類型、銷售管道和應用分類的預測,2026-2032年 太陽輻射控制玻璃市場報告:按玻璃類型、鍍膜方法、性能、應用和地區分類(2026-2034 年)

太陽輻射控制玻璃市場報告:按玻璃類型、鍍膜方法、性能、應用和地區分類(2026-2034 年) 全球調光玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球調光玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球調光玻璃市場報告

2026年全球調光玻璃市場報告 太陽能鏡市場 - 全球產業規模、佔有率、趨勢、機會、預測(按技術、最終用戶、地區和競爭格局分類),2021-2031年

太陽能鏡市場 - 全球產業規模、佔有率、趨勢、機會、預測(按技術、最終用戶、地區和競爭格局分類),2021-2031年 全球太陽能蓋板玻璃市場

全球太陽能蓋板玻璃市場 調光玻璃市場報告:趨勢、預測和競爭分析(至2031年)

調光玻璃市場報告:趨勢、預測和競爭分析(至2031年) 2025-2029年全球太陽能蓋板玻璃市場

2025-2029年全球太陽能蓋板玻璃市場 2030 年調光玻璃市場預測:按玻璃類型、特性、塗層類型、最終用戶和地區進行的全球分析

2030 年調光玻璃市場預測:按玻璃類型、特性、塗層類型、最終用戶和地區進行的全球分析 調光玻璃市場規模、佔有率、成長分析,按類型、技術、應用、地區分類 - 產業預測,2024-2031 年

調光玻璃市場規模、佔有率、成長分析,按類型、技術、應用、地區分類 - 產業預測,2024-2031 年