|

市場調查報告書

商品編碼

2063243

住宅發電機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Residential Generators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

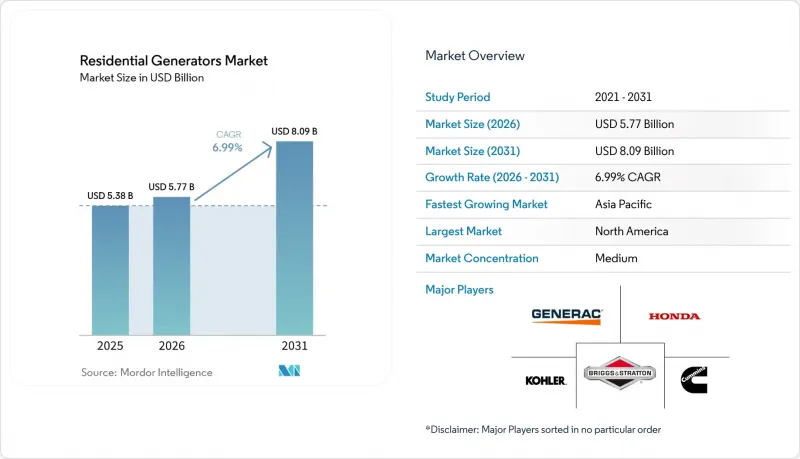

據 Mordor Intelligence 稱,2025 年住宅發電機市場價值為 53.8 億美元,預計到 2031 年將從 2026 年的 57.7 億美元成長至 80.9 億美元,預測期(2026-2031 年)的複合年成長率預計為 6.99%。

本報告按燃料類型(例如柴油)、功率輸出(例如小於3kW)、相數(單相、三相)、類型(可攜式、備用式、逆變器式)、技術(傳統型、逆變器型、混合型)、應用(例如緊急備用電源)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球住宅發電機市場趨勢及洞察

極端天氣導致停電頻率增加

從2000年到2023年,美國80.1%的停電是由強烈風暴造成的,2022年主要停電的平均持續時間為229分鐘,是10年前平均恢復時間的兩倍。預計到2025年,全球範圍內也將出現類似的趨勢。智利全國範圍內的停電以及伊拉克因熱浪引發的停電凸顯了多種氣候壓力因素疊加會如何使運作已接近負荷極限的電網不堪崩壞。縣級調查證實,當風雨交加且氣溫超過攝氏32.2度時,停電事故會激增,導致加州、德克薩斯州和美國東南部地區的家庭對能夠應對持續數天停電的自啟動解決方案的需求增加。隨著冷藏庫、空調系統和通訊設備變得必不可少,消費者擴大選擇具有更長運作和遠端監控功能的備用或混合動力發電機。因此,隨著備用電源成為住宅緊急應變計畫的核心要素,住宅發電機市場正經歷持續成長。

老化的輸配電基礎設施

目前,美國約70%的輸電線路和大型變壓器已使用超過25年。這種運作與極端溫度下更高的故障率密切相關。計劃在2025年投資4800億美元、2035年投資5.8兆美元用於電網加固,預計最終將緩解負載壓力,但授權和勞動力短缺導致完工日期推遲,使未來十年住宅面臨風險。北美地區的可靠性評估已表明,23個地區中有13個地區的風險增加,儘管電力公司進行了投資,但對備用發電機組的需求仍然強勁。西歐也存在類似的設備更換延誤問題,那裡也面臨基礎設施老化和電氣化負載不斷增加的挑戰。因此,住宅發電機市場受益於清晰的長期需求前景,製造商正在加速拓展分銷網路、資金籌措管道和混合產品線。

加強小型引擎排放氣體法規

美國環保署第二階段排放標準、加州小型非道路引擎法規以及歐盟第五階段排放標準均強制要求使用顆粒物過濾器、催化還原系統和先進噴射系統,這使得20千瓦以下機組的零件成本增加了15%至20%。為了在日益嚴格的法規下維持市場進入,像科勒這樣的供應商正在透過推出氫氣和氫化植物油相容產品來規避風險。合規成本對可攜式和入門級緊急發電機的影響最大,擠壓了利潤空間,並促使消費者轉向更安靜的逆變器和電池供電解決方案,以避免燃燒限制。監管的影響雖然溫和但持續存在,導致住宅發電機市場的預期複合年成長率下降了0.8個百分點。

細分市場分析

2025年,天然氣發電機在住宅發電機市場佔有34.8%的佔有率,這主要得益於管道基礎設施、便利的自動啟動以及每千瓦時較低的燃料成本。安大略省和美國陽光地帶電網的持續擴建擴大了目標基本客群,並支撐了穩定的銷售。預計到2031年,隨著安裝方式從手動傳輸開關轉向覆蓋全屋的全自動系統,住宅發電機市場中天然氣發電機組的市場規模將達到32億美元。同時,太陽能和電池混合動力發電機以11.0%的複合年成長率成長,憑藉補貼價格和靜音運行,吸引了對噪音敏感的都市區用戶。柴油發電機在需要數天自給自足電力供應的農村離網住宅中仍然發揮重要作用,但由於排放氣體法規的限制,系統成本正在上升。汽油可攜式發電機仍處於入門級小眾市場,其市場佔有率正被更安全、更運作的液化石油氣雙燃料發電機蠶食。能夠提供雙燃料和三燃料產品的製造商可以最有效地佔領混合基礎設施市場,可靠性機構已指出,冬季管道壓力可能會降低。

可再生能源的普及將塑造未來的選擇。在屋頂太陽能滲透率超過20%的地區,人們越來越依賴混合系統,這些系統白天自充電,晚上則利用電池滿足電力高峰。相較之下,在天然氣管網完善的郊區,人們更傾向於使用能夠滿足空調和電動車充電等用電需求的燃油緊急發電機組。因此,策略定位應著重於在品牌生態系統內同時提供零排放和雙燃料選項,並允許客戶根據政策和價格趨勢的變化添加或更換組件。

功率在3-10kW範圍內的發電機佔了42.1%的市場佔有率,是冷藏庫、空調鼓風機、照明和在家工作電子設備的主流選擇。儘管混合動力發電機興起,但由於其每千瓦的安裝成本合理且佔地面積小,適合單戶住宅,因此出貨量依然居高不下。預計到2031年,該輸出範圍的住宅發電機市場面積將達到35億美元,但由於大型住宅帶來的升級需求以及電動車充電的日益普及,其市場佔有率預計將略有下降。 10-20kW頻寬的發電機成長最快,複合年成長率達7.7%,這反映了二級充電器的普及和電熱泵的日益普及。功率低於3kW的可攜式電源憑藉其安靜的室內電池,滿足了露營和戶外聚會的需求,正在蠶食小型汽油發電機的市場佔有率。雖然功率超過 20kW 的型號仍然是小眾產品,主要針對豪華住宅、農場和小規模企業,但如果 V2G(車輛到電網)法規允許電力銷售收入抵消高額資本投資,則市場可能會擴大。

在容量規劃中,熱泵和電動車充電器的尖峰時段啟動負載正日益受到重視,其重要性超過了平均功耗,而且越來越多的家庭選擇更大容量的型號。製造商正著重研發能夠動態調節電器的負載管理模組,以運作15kW的連接負載,在擴大最佳運轉範圍的同時降低成本。

區域分析

到2025年,北美將佔全球銷售額的37.0%,其主導地位得益於成熟的天然氣管網、簡化的應急設備安裝許可程序以及與認證備用系統掛鉤的保險折扣。颶風、野火和冰暴等災害頻傳,持續引發消費者的高度關注。 Enbridge公司在加拿大安大略省的擴建將擴大管道覆蓋範圍,到2027年將為另外2,200戶農村家庭提供天然氣備用電源,從而擴大住宅發電機市場。在墨西哥,由於在低收入地區的可攜式發電機普及,安裝量的成長速度超過了銷售量的成長速度。 2035年的停電風險評估顯示,MISO、PJM、ERCOT和WECC等地區的電力資源供應短缺,預示長期需求將持續成長。

在亞太地區,全球經濟成長速度最快,年複合成長率達8.5%,但各國狀況差異顯著。印度農村地區頻繁的停電推動了可攜式發電機的普及。本田將於2026年啟動的UPS租賃業務將搶佔這一價格適中的細分市場。在日本,由於颱風季節和電網老化,備用電源需求不斷成長;而在澳洲的颶風帶,雙燃料可攜式發電機的銷售量也在成長。在中國當地,由於農村地區電力供應不均衡,每週都會停電,這支撐了低成本汽油發電機的銷售。在印尼和菲律賓,由於授權核准和燃料物流問題,備用發電機的普及速度緩慢,但在有噪音管制的密集都市區地區,逆變式可攜式發電機的市場佔有率正在擴大。

在歐洲,可再生能源日益成長的間歇性問題,加上嚴格的排放法規和不斷增加的停電風險,使得情況更加複雜。歐盟第五階段排放標準的合規成本促使買家轉向逆變器和混合動力發電機組,而市政噪音法規則傾向於噪音水平低於60分貝的設備。 2025年襲擊愛爾蘭電網的「伊歐文」風暴,揭露了即使是先進電網的脆弱性。德國、義大利和西班牙推出了慷慨的上網電價補貼(FIT)計劃,以推廣太陽能和電池混合動力系統,這給短期發電機需求帶來了壓力。在南美洲,需求集中在巴西和阿根廷,但經濟波動限制了高階產品的銷售。在中東,柴油發電在電網不穩定的地區仍然是主要電源,黎巴嫩80%的柴油發電市場佔有率就證明了這一點,但高收入水準也維持了發電機的大量出貨。撒哈拉以南非洲每年售出 250 萬台可攜式電源站,反映出電網發展速度跟不上都市化,導致南非在 2023 年計劃停電 200 天。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 極端天氣導致停電頻率增加

- 老化的輸配電基礎設施

- 住宅天然氣供應網擴建

- 「隨時隨地辦公」解決方案的廣泛普及推動了家用基本電子設備需求的激增。

- 結合太陽能發電、儲能和電力生產的混合韌性方案。

- 住宅們越來越擔心電網網路安全漏洞。

- 市場限制因素

- 小型引擎更嚴格的排放氣體法規(歐盟第五階段法規、加州空氣資源委員會法規)

- 地方政府噪音管制條例/分區條例

- 家用鋰離子電池成本更低

- 保險折扣有利於零排放車輛。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按燃料類型

- 柴油引擎

- 天然氣

- 汽油

- 太陽能和電池儲能混合

- 其他

- 額定功率

- 小於3千瓦

- 3~10 kW

- 10~20 kW

- 超過20千瓦

- 按階段

- 單相

- 三相

- 按類型

- 可攜式發電機

- 緊急發電機

- 逆變發電機

- 透過技術

- 傳統的

- 逆變器

- 混合

- 透過使用

- 緊急備用

- 主/連續

- 休閒/戶外活動

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Generac Holdings Inc.

- Kohler Co.

- Briggs & Stratton Corp.

- Cummins Inc.

- Honda Motor Co., Ltd.

- Atlas Copco AB

- Caterpillar Inc.

- Yamaha Motor Co., Ltd.

- Champion Power Equipment Inc.

- Wacker Neuson SE

- Honeywell(Home Standby Licensing)

- Westinghouse Electric Corp.

- Hyundai Power Products

- FG Wilson(Caterpillar)

- DEUTZ AG

- Wartsila Corp.

- Rolls-Royce plc(MTU Power Systems)

- Siemens Energy AG

- PRAMAC Group

- Ingersoll Rand Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the residential generators market size was valued at USD 5.38 billion in 2025 and is estimated to grow from USD 5.77 billion in 2026 to reach USD 8.09 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (Diesel, and More), Power Rating (Below 3 KW, and More), Phase (Single-Phase, Three-Phase), Type (Portable, Standby, Inverter), Technology (Conventional, Inverter, Hybrid), Application (Emergency Backup, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Residential Generators Market Trends and Insights

Growing frequency of extreme-weather-related outages

Severe storms generated 80.1% of U.S. power interruptions between 2000 and 2023, and the average major event lasted 229 minutes in 2022, double the restoration windows common a decade earlier . Similar patterns emerged worldwide in 2025 when Chile's nationwide outage and Iraq's heat-wave blackout underscored how compound climate stressors topple grids already operating near capacity. County-level studies confirm that days above 32.2 °C combined with wind or precipitation sharply elevate outage counts, pushing households in California, Texas, and the Southeast toward automatic-start solutions that can cover multi-day disruptions. As refrigerators, HVAC systems, and connectivity equipment all become mission-critical, buyers increasingly select standby or hybrid units featuring long runtime and remote monitoring. The outcome is a sustained uplift in the Residential generators market as backup power becomes a core element of household resilience planning.

Aging transmission & distribution infrastructure

Roughly 70% of U.S. transmission lines and large transformers now exceed 25 years of service, a lifespan bracket correlated with higher failure rates during extreme temperatures . Planned grid-hardening investments of USD 480 billion in 2025 and USD 5.8 trillion through 2035 will ease the strain eventually, but permitting delays and labor shortages stretch completion timelines, leaving homeowners exposed for the next decade. North American reliability assessments already flag 13 of 23 regions at elevated risk, so demand for backup generation persists even as utilities invest. Similar replacement lags characterize Western Europe, where legacy infrastructure meets rising electrification loads. Consequently, the Residential generators market benefits from a long, visible demand horizon that encourages manufacturers to expand dealer networks, financing options, and hybrid product lines.

Tightening small-engine emission limits

EPA Tier 2, California's small off-road engine rules, and EU Stage V standards demand particulate filters, catalytic reduction, and advanced injection systems that add 15-20% to the bill of materials for sub-20 kW sets . Vendors such as Kohler hedge with hydrogen-compatible and HVO-ready products to preserve market access as thresholds tighten. Compliance costs hit portable and entry-level standby models hardest, compressing margins and nudging buyers toward quieter inverter or battery solutions that sidestep combustion limits. The regulatory drag is moderate yet persistent, shaving 0.8 percentage points off forecast CAGR in the Residential generators market.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid Solar-Storage-Generator Resilience Packages

- Work-from-Anywhere Surge in Home Critical Electronics

- Falling Lithium-Ion Home-Battery Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural-gas units accounted for 34.8% Residential generators market share in 2025 on the back of pipeline availability, automatic-start ease, and lower fuel cost per kWh. Ongoing grid expansions in Ontario and the U.S. Sun Belt widen the addressable base, supporting steady volume. The Residential generators market size for natural-gas sets is projected to reach USD 3.2 billion by 2031 as installations migrate from manual transfer switches to fully automated whole-home coverage. Meanwhile, solar-battery hybrids log an 11.0% CAGR, luring urban, noise-sensitive buyers with rebate-driven economics and silent operation. Diesel remains relevant for rural, off-grid properties requiring multi-day autonomy, but emission compliance raises system cost. Gasoline portables cling to entry-level niches yet lose share to dual-fuel LPG models that store safer and run cleaner. Manufacturers hedging across dual- and tri-fuel capabilities best capture mixed-infrastructure markets flagged by reliability agencies where winter pipeline pressure can drop.

Renewables adoption steers future preferences. Regions crossing 20% rooftop solar penetration lean heavily toward hybrids that self-charge daily and ride through evening peaks on batteries. In contrast, suburban tracts with mature natural-gas grids prefer fuel-based standby sets sized for HVAC and EV-charger loads. Strategic positioning, therefore, revolves around offering both zero-emission and dual-fuel pathways inside branded ecosystems so customers can add or swap modules as policy or price signals evolve.

With 42.1% share, 3-10 kW generators represent the mainstream choice for refrigerators, HVAC blowers, lighting, and home-office electronics. Their installed cost per kW and footprint suit single-family dwellings, keeping shipment volume high even as hybrids gain ground. The Residential generators market size tied to this band is forecast to climb to USD 3.5 billion by 2031, though share inches down as larger homes and EV charging drive upgrades. The 10-20 kW bracket grows fastest at 7.7% CAGR, reflecting Level 2 charger prevalence and rising adoption of electric heat pumps. Portable power stations under 3 kW eat into small gasoline generator demand thanks to silent, indoor-safe batteries that meet camping and tailgating needs. Units above 20 kW remain niche-luxury estates, farms, and small businesses-but could scale if vehicle-to-grid rules allow export revenues that offset higher capex.

Capacity planning increasingly accounts for peak-start loads of heat pumps and EV chargers rather than average draw, nudging households to size up. Manufacturers emphasize load-management modules that orchestrate appliances dynamically, letting a 10 kW generator run a 15 kW connected load sequentially, stretching the sweet spot while containing costs.

Geography Analysis

North America anchored 37.0% of 2025 revenue, a leadership position sustained by mature natural-gas grids, streamlined permitting for standby installations, and insurance discounts tied to certified backup systems. Chronic hurricane, wildfire, and ice-storm activity keeps consumer awareness high. Canada's Enbridge expansions in Ontario broaden pipeline coverage and enlarge the Residential generators market as gas standbys become feasible for another 2,200 rural homes by 2027. Mexico shows faster unit growth than revenue growth because portable sets dominate in lower-income regions. Outage-risk assessments through 2035 flag resource adequacy shortfalls in MISO, PJM, ERCOT, and WECC, pointing to a long demand runway.

Asia-Pacific, the quickest riser at an 8.5% CAGR, features highly varied national profiles. India's tier-2 cities endure frequent blackouts, boosting portable uptake; Honda's 2026 UPS leasing rollout captures this affordability-focused niche. Japan's typhoon seasons and aging grid elevate standby demand, while Australia's cyclone belt fuels dual-fuel portable sales. Mainland China's rural electrification gaps still prompt weekly outages, sustaining low-price gasoline generator volume. Permitting hurdles and fuel-logistics issues slow standby penetration in Indonesia and the Philippines, but inverter portables gain share where noise limits apply in dense urban areas.

Europe blends strict emission policies with growing outage risk as renewable intermittency rises. EU Stage V compliance costs push buyers toward inverter and hybrid sets, and municipal sound ordinances drive less than 60 dBA equipment preference. Storm Eowyn's 2025 damage to Ireland's network showed that even advanced grids remain vulnerable. Germany, Italy, and Spain use generous feed-in tariffs to promote solar-battery hybrids, eating into short-duration generator demand. South America clusters demand in Brazil and Argentina, though economic volatility caps high-end sales. The Middle East relies on diesel prime power where grids falter, evidenced by Lebanon's 80% diesel share, yet income levels support sizeable unit shipments. Sub-Saharan Africa's 2.5 million annual portable sales reflect urbanization outpacing grid build-out, with South Africa recording 200 load-shedding days in 2023.

- Generac Holdings Inc.

- Kohler Co.

- Briggs & Stratton Corp.

- Cummins Inc.

- Honda Motor Co., Ltd.

- Atlas Copco AB

- Caterpillar Inc.

- Yamaha Motor Co., Ltd.

- Champion Power Equipment Inc.

- Wacker Neuson SE

- Honeywell (Home Standby Licensing)

- Westinghouse Electric Corp.

- Hyundai Power Products

- FG Wilson (Caterpillar)

- DEUTZ AG

- Wartsila Corp.

- Rolls-Royce plc (MTU Power Systems)

- Siemens Energy AG

- PRAMAC Group

- Ingersoll Rand Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing frequency of extreme-weather-related outages

- 4.2.2 Aging transmission & distribution infrastructure

- 4.2.3 Expansion of residential natural-gas grids

- 4.2.4 "Work-from-anywhere" surge in home load-critical electronics

- 4.2.5 Hybrid solar-storage-generator resilience packages

- 4.2.6 Grid-cybersecurity breach concerns among homeowners

- 4.3 Market Restraints

- 4.3.1 Tightening small-engine emission limits (EU Stage V, CARB)

- 4.3.2 Municipal noise / zoning restrictions

- 4.3.3 Falling Li-ion home-battery costs

- 4.3.4 Insurance rebates favouring zero-emission backup

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Diesel

- 5.1.2 Natural Gas

- 5.1.3 Gasoline

- 5.1.4 Solar-Battery Hybrid

- 5.1.5 Others

- 5.2 By Power Rating

- 5.2.1 Below 3 kW

- 5.2.2 3 to 10 kW

- 5.2.3 10 to 20 kW

- 5.2.4 Above 20 kW

- 5.3 By Phase

- 5.3.1 Single-Phase

- 5.3.2 Three-Phase

- 5.4 By Type

- 5.4.1 Portable Generators

- 5.4.2 Standby Generators

- 5.4.3 Inverter Generators

- 5.5 By Technology

- 5.5.1 Conventional

- 5.5.2 Inverter

- 5.5.3 Hybrid

- 5.6 By Application

- 5.6.1 Emergency Backup

- 5.6.2 Prime/Continuous

- 5.6.3 Recreational / Outdoor

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Generac Holdings Inc.

- 6.4.2 Kohler Co.

- 6.4.3 Briggs & Stratton Corp.

- 6.4.4 Cummins Inc.

- 6.4.5 Honda Motor Co., Ltd.

- 6.4.6 Atlas Copco AB

- 6.4.7 Caterpillar Inc.

- 6.4.8 Yamaha Motor Co., Ltd.

- 6.4.9 Champion Power Equipment Inc.

- 6.4.10 Wacker Neuson SE

- 6.4.11 Honeywell (Home Standby Licensing)

- 6.4.12 Westinghouse Electric Corp.

- 6.4.13 Hyundai Power Products

- 6.4.14 FG Wilson (Caterpillar)

- 6.4.15 DEUTZ AG

- 6.4.16 Wartsila Corp.

- 6.4.17 Rolls-Royce plc (MTU Power Systems)

- 6.4.18 Siemens Energy AG

- 6.4.19 PRAMAC Group

- 6.4.20 Ingersoll Rand Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment