|

市場調查報告書

商品編碼

2063239

頁岩振動篩:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Shale Shakers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

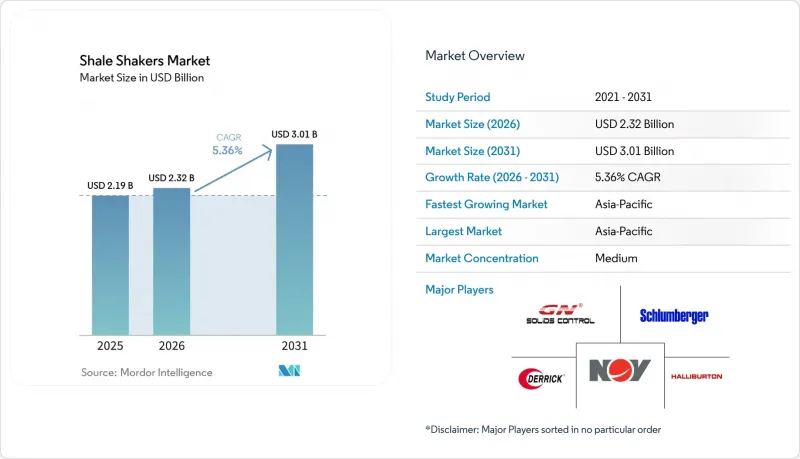

根據 Mordor Intelligence 預測,頁岩振動篩市場規模預計將在 2025 年達到 21.9 億美元,2026 年達到 23.2 億美元,到 2031 年達到 30.1 億美元,2026 年至 2031 年的複合年成長率為 5.36%。

本報告按產品類型(例如,直線運動式)、技術(單層、雙層、三層)、驅動系統(電動、皮帶驅動)、安裝類型(新安裝、改造)、應用(例如,洗煤)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球頁岩振動篩市場趨勢與洞察

水平和定向頁岩鑽井活動迅速增加

2026年2月,海恩斯維爾的天然氣鑽井鑽機數量達到64座。這主要是由於天然氣日產量目標提高,2026年達到12億立方英尺,2027年達到16億立方英尺,而這又受到液化天然氣出口成長和資料中心電力需求增加的推動。每口水平井排放的鑽井液高達2000桶,這些鑽井液必須經過振動篩處理才能重複使用。平均長度為10000至12000英尺的水平井,固態含量增加了40%,迫使營運商將單層平台升級為三層平台,以維持每分鐘800加侖的循環量。美國地面平台鑽井技術已引入阿根廷瓦卡穆埃爾塔和沙烏地阿拉伯賈夫拉,在這些地區,攜帶式的高容量平台能夠以7.5G的加速度處理每秒28公升的鑽井液。自主重力控制技術可根據井下遙測資料調節振動幅度,使篩網堵塞率降低了20%,篩網壽命延長至55小時,單井耗材成本降低了8,000美元。井產能提升、水平井延伸和自動化帶來的綜效,使得年複合成長率達1.5%。

採用高G值泥漿方案的深海井數量增加

雪佛龍公司的安克爾計畫於2024年投產,井眼壓力為20,000磅/平方英吋(psi)。本工程採用合成泥漿,對鑽井平台施加6.5G的重力加速度。由於傳統的線性運動振動篩難以在不造成流體損失的情況下去除小於10微米的重晶石,因此平衡式橢圓振動篩的應用日益廣泛,其固態去除率可達80%,同時還能保護200目篩網。阿布達比國家石油公司鑽井公司(ADNOC Drilling)於2025年訂購了兩座自升式鑽井和三座島式鑽機,所有平台均配備人工智慧三級振動篩,設計處理能力為每加侖18磅泥漿。鑽機,阿拉伯鑽井公司(Arabian Drilling)也重新啟用了三座鑽機,每座平台均配備三級振動篩,以應付高壓儲存。巴西和西非深海鑽井作業的擴張將推動該方法在全球的應用,並有望為長期運作貢獻0.8%。

原油價格波動抑制了對新鑽機的投資。

到2026年初,西德德克薩斯中質原油(WTI)的平均價格將達到每桶62美元,這將迫使北美獨立石油公司削減鑽井預算,並依靠40%的產能提升來實現產量目標。新鑽機的減少將導致新安裝振動篩的需求下降,儘管維修工作將部分抵消這一降幅。業者正在推遲採購,直到油價維持在每桶70美元以上,這將使2028年之前的複合年成長率下降0.9個百分點。

細分市場分析

預計到2025年,直線運動設計將佔銷售額的68.6%,並以每年5.6%的速度成長至2031年。此細分市場的優勢在於能夠產生高達0.25英吋的強勁單向振動,加速度可達4G,從而推動高黏度的海恩斯維爾泥漿通過篩網。現場測試表明,NOV公司的Brandt Alpha系列產品在米德蘭盆地減少了37%的廢棄物,每個平台節省了45,000美元的成本。平衡橢圓運動設計因其能夠保護細篩免受6.5G泥漿作業的影響,而更受海上作業的青睞。同時,在煤炭洗選領域,由於其操作簡便性至關重要,圓形設計仍然佔據主導地位。

受傳統鑽井和大型固態處理作業的廣泛應用所推動,線性振動篩市場預計將持續成長至2031年。自主重力控制系統的引入,使篩網壽命從約40小時延長至約55小時,使作業者每口井可節省約8,000美元的耗材成本。在中東鑽井專案中,符合API RP 13C標準(D100切割粒度為75-150微米)仍然是採購的首要考慮因素,這鞏固了該細分市場在整體振動篩需求中的重要作用。

即使到了2025年,單層篩分機仍以54.2%的市佔率佔據最大佔有率,這主要歸功於其較低的初始成本。然而,三層篩分機平台以6.3%的複合年成長率位居榜首,因為它們將粗篩、中篩和細篩檢整合在一個框架內,無需單獨的除砂器和乾燥器。 Brightway的設計可減少40%的面積和50%的組裝時間。

受業者為遵守北海嚴格的零排放法規(規定殘油含量低於1%)而採取的措施推動,預計到2031年,三層振動篩系統將實現顯著成長。在多層篩面上整合數位雙胞胎感測器,可增強運行資料擷取,實現基於機器學習的軸承磨損預測,並提高設備的整體運轉率。雖然單層篩裝置在煤炭和採礦應用中仍佔據主導地位,但在北美,三層篩配置正日益成為高性能鑽井鑽機的首選。

區域分析

2025年,北美將佔頁岩振動篩市場收入的40.1%,預計到2031年將以6.2%的年均成長率成長。到2026年2月,海恩斯維爾地區的鑽機數量增加至64台,即使在低油價時期,二疊紀盆地的鑽機總數也維持在255台左右。康斯托克資源公司計畫於2026年在海恩斯維爾鑽探43口井,每口井都將配備一台高容量的三級振動篩。為了應對科羅拉多和亞伯達省日益嚴格的噪音法規,精密鑽井公司正在維修其變頻驅動裝置(VFD),以配合一項利用數位雙胞胎技術的運轉率改進計劃,該計劃已將停機時間減少了30%。

中東地區正經歷最強勁的投資動能。阿布達比國家石油公司(ADNOC)已訂購價值超過19億美元的鑽井鑽機,目標是在2025年前購置,並強制要求配備人工智慧固態控系統。同時,沙烏地阿拉伯的石油業者維持著每日1,300萬桶的產能。配備永磁馬達(PMAC)和API RP 13C篩網的三級振動篩已成為沙烏地阿拉伯和阿拉伯聯合大公國新鑽井船隊的標準配備。在受OSPAR零排放法規約束的歐洲北海,採用具備真空脫水功能的閉合迴路系統已成為主流。在挪威大陸棚的油井中,殘油含量低於1%已成為普遍現象。

亞太地區的成長更為穩定。中國煤炭洗滌業務對GN固控經濟型振動篩的需求持續旺盛,但長期需求受到中國可再生能源目標的限制。印度克里希納-戈達瓦里油田的深井需要更高的處理能力,但鑽機總數僅為北美的三分之一。在南美,受巴西鹽層下下層和阿根廷頁岩層的推動,北美式的井下鑽井作業方法正在推廣,該方法採用可攜式設備,處理能力為每秒28升,重力加速度為7.5G,但由於外匯風險,部分訂單有所延遲。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 水平和定向頁岩鑽井活動迅速增加

- 採用高G值泥漿方案的超深水油井數量增加

- 排放制定了嚴格的規定(例如,北海的OSPAR協議)

- 透過引入鑽機的數位雙胞胎,實現了振動篩的預測性維護。

- 採用自主重力控制來最佳化ROP

- 需要超精細切削控制的高鋰含量地熱井

- 市場限制因素

- 原油價格波動抑制了對新鑽機的資本投資。

- 高擁有成本與無振動過濾過濾替代方案的比較。

- 稀土元素合金導致符合API標準的網狀物供應瓶頸

- 對挖掘現場振動引起的甲板噪音進行ESG監測

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 直線運動式頁岩振動台

- 平衡式橢圓振動篩

- 圓週運動式頁岩振動篩

- 透過技術

- 單層甲板

- 雙層甲板

- 三層甲板

- 透過驅動系統

- 電動驅動

- 皮帶驅動

- 按安裝類型

- 新安裝

- 改裝

- 透過使用

- 洗煤

- 石油和天然氣鑽探

- 礦業

- 化工/石油化工

- 塑膠

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Derrick Equipment Company

- NOV-BRANDT

- Halliburton

- Schlumberger

- GN Solids Control

- Baker Hughes

- Elgin Separation Solutions

- KEMTRON Technologies

- MI SWACO

- Aipu Solids Control

- Tri-Flo International

- TR Solids Control

- H-Screening Separation

- Shale Tech Solutions

- Kem-Terra

- DC Solid Control

- ShengJia Machinery

- Derrick Fine Mesh

- KOSUN Machinery

- DFE

- Southwest Petroleum University Tech

第7章 市場機會與未來展望

According to Mordor Intelligence, the shale shakers market size is projected to be USD 2.19 billion in 2025, USD 2.32 billion in 2026, and reach USD 3.01 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031.

This report is Segmented by Product Type (Linear Motion, and More), Technology (Single Deck, Double Deck, Triple Deck), Drive System (Electrically Driven, Belt Driven), Installation (Newly Installed, Retrofitted), Application (Coal Cleaning, and More), and Geography (North America, Europe, Asia Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Shale Shakers Market Trends and Insights

Surging Horizontal and Directional Shale Drilling Activity

Haynesville gas-directed drilling touched 64 rigs in February 2026 as LNG export expansions and data-center power demand boosted gas targets by 1.2 billion cubic feet per day for 2026 and 1.6 billion cubic feet per day for 2027 . Each horizontal well generates up to 2,000 barrels of drilling fluid that must pass across shale shakers before reuse. Longer laterals averaging 10,000-12,000 feet raise solids loading by 40%, forcing operators to shift from single-deck to triple-deck equipment to maintain 800 gallons-per-minute circulation. U.S. pad-drilling expertise is migrating to Argentina's Vaca Muerta and Saudi Arabia's Jafurah, where portable high-throughput decks process 28 liters per second at 7.5 G-force. Autonomous g-force control that modulates vibration amplitude based on downhole telemetry is reducing screen blinding by 20% and extending mesh life to 55 hours, lowering consumable cost by USD 8,000 per well. The confluence of higher well counts, longer laterals, and automation adds 1.5 % to the CAGR.

Rising Offshore Ultra-Deepwater Wells With High-G Mud Programs

Chevron's Anchor project came on-stream in 2024 at 20,000 psi wellhead pressure, relying on synthetic-based muds that impose 6.5 G loads on decks . Conventional linear-motion units struggle to remove sub-10-micron barite without losing fluid, prompting uptake of balanced elliptical shakers that safeguard 200-mesh screens while achieving 80% solids removal. ADNOC Drilling ordered two jack-up rigs and three island rigs in 2025, all specified with AI-enabled triple-deck shakers designed for 18-pound-per-gallon mud. Arabian Drilling reactivated three rigs the same year, each fitted with triple-deck units to handle high-pressure reservoirs. Growing deepwater campaigns in Brazil and West Africa will translate this practice globally, contributing 0.8 % to long-term growth.

Crude-Price Volatility Curbing New Rig CAPEX

West Texas Intermediate averaged USD 62 per barrel in early 2026, prompting North American independents to trim drilling budgets and rely on 40% productivity gains to meet output targets. Fewer greenfield rigs translate to lower demand for newly installed shakers, even though retrofit work partially offsets the dip. Operators defer purchases until sustained prices climb above USD 70, creating a 0.9 percentage-point drag on CAGR through 2028.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Cuttings-Discharge Regulations

- Rig Digital-Twin Adoption Enabling Predictive Shaker Maintenance

- High Ownership Cost Versus Shaker-Less Vacuum Filtration Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Linear-motion designs generated 68.6% of 2025 revenue and will grow at 5.6% annually through 2031. The segment benefits from aggressive unidirectional vibration of 0.25 inches at up to 4 G that propels sticky Haynesville gumbo across the screen. Field trials showed that NOV's Brandt Alpha line delivered 37% waste reduction and saved USD 45,000 per pad in the Midland Basin. Balanced elliptical motion is favored offshore to protect fine screens against 6.5 G mud programs. Circular designs persist in coal cleaning where simplicity matters.

The shale shakers market for linear-motion units is projected to grow steadily through 2031, driven by their extensive use in conventional drilling and high-volume solids control operations. The introduction of autonomous G-force control systems is increasing screen life from approximately 40 hours to around 55 hours, enabling operators to lower consumable costs by nearly USD 8,000 per well. Adherence to API RP 13C standards at D100 cut points of 75-150 microns continues to enhance procurement preferences in Middle Eastern drilling projects, solidifying the segment's strong role in overall shale shaker demand.

Single-deck units remained most numerous in 2025, with 54.2% installs due to low upfront cost. Triple-deck platforms, however, post the fastest 6.3% CAGR because they integrate coarse, intermediate, and fine screening inside one frame, erasing the need for separate desanders and desilters.Brightway's design trims footprint by 40% and halves rig-up time.

Triple-deck shale shaker systems are projected to experience significant growth through 2031, driven by operators' focus on adhering to stringent North Sea zero-discharge regulations, which mandate residual oil content below 1%. The integration of digital-twin sensors across multiple decks enhances operational data collection, facilitating machine-learning-based predictions of bearing wear and improving overall equipment uptime. While single-deck units remain prevalent in coal and mining applications, triple-deck configurations are increasingly favored for high-specification drilling rigs in North America.

Geography Analysis

North America controlled 40.1% of the shale shakers market revenue in 2025 and is projected to grow at 6.2% annually to 2031. Haynesville rig counts rose to 64 by February 2026, and Permian totals held near 255 even during price softness. Comstock Resources plans 43 Haynesville wells in 2026, each specifying high-throughput triple-deck units. Tightening Colorado and Alberta noise codes are driving VFD retrofits that align with digital-twin uptime programs at Precision Drilling, reducing downtime by 30%.

The Middle East shows the strongest spending momentum. ADNOC placed more than USD 1.9 billion in rig orders during 2025 that mandate AI-enabled solids control, while Saudi operators keep capacity at 13 million barrels per day. Triple-deck shakers with PMAC motors and API RP 13C mesh are now standard in new Saudi and UAE fleets. Europe's North Sea, constrained by OSPAR zero-discharge rules, adopts closed-loop systems with vacuum dewatering; residual oil levels under 1% are now routine on Norwegian Continental Shelf wells.

Asia-Pacific's growth is steadier. Chinese coal washing maintains demand for cost-focused shakers from GN Solids Control, yet national renewable targets temper long-term volumes. India's deeper Krishna-Godavari wells require higher throughput, but overall rig counts keep the region at one-third the North American size. South America, led by Brazil's pre-salt and Argentina's shale, is adopting North American pad-drilling methods that rely on portable equipment rated 28 liters per second at 7.5 G, although currency risks delay some orders.

- Derrick Equipment Company

- NOV-BRANDT

- Halliburton

- Schlumberger

- GN Solids Control

- Baker Hughes

- Elgin Separation Solutions

- KEMTRON Technologies

- M-I SWACO

- Aipu Solids Control

- Tri-Flo International

- TR Solids Control

- H-Screening Separation

- Shale Tech Solutions

- Kem-Terra

- DC Solid Control

- ShengJia Machinery

- Derrick Fine Mesh

- KOSUN Machinery

- DFE

- Southwest Petroleum University Tech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging horizontal & directional shale drilling activity

- 4.2.2 Rising offshore ultra-deepwater wells with high-G mud programs

- 4.2.3 Stringent cuttings-discharge regulations (e.g., North Sea OSPAR)

- 4.2.4 Rig digital-twin adoption enabling predictive shaker maintenance

- 4.2.5 Adoption of autonomous g-force control to optimise ROP

- 4.2.6 Lithium-rich geothermal wells requiring ultra-fine cuttings control

- 4.3 Market Restraints

- 4.3.1 Crude-price volatility curbing new rig CAPEX

- 4.3.2 High ownership cost vs. shaker-less vacuum filtration alternatives

- 4.3.3 API compliant mesh supply bottlenecks due to rare-earth alloys

- 4.3.4 ESG scrutiny on vibration-induced deck noise at well sites

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Linear Motion Shale Shakers

- 5.1.2 Balanced Elliptical Motion Shale Shakers

- 5.1.3 Circular Motion Shale Shakers

- 5.2 By Technology

- 5.2.1 Single Deck

- 5.2.2 Double Deck

- 5.2.3 Triple Deck

- 5.3 By Drive System

- 5.3.1 Electrically Driven

- 5.3.2 Belt Driven

- 5.4 By Installation

- 5.4.1 Newly Installed

- 5.4.2 Retrofitted

- 5.5 By Application

- 5.5.1 Coal Cleaning

- 5.5.2 Oil and Gas Drilling

- 5.5.3 Mining

- 5.5.4 Chemical and Petrochemical

- 5.5.5 Plastics

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Derrick Equipment Company

- 6.4.2 NOV-BRANDT

- 6.4.3 Halliburton

- 6.4.4 Schlumberger

- 6.4.5 GN Solids Control

- 6.4.6 Baker Hughes

- 6.4.7 Elgin Separation Solutions

- 6.4.8 KEMTRON Technologies

- 6.4.9 M-I SWACO

- 6.4.10 Aipu Solids Control

- 6.4.11 Tri-Flo International

- 6.4.12 TR Solids Control

- 6.4.13 H-Screening Separation

- 6.4.14 Shale Tech Solutions

- 6.4.15 Kem-Terra

- 6.4.16 DC Solid Control

- 6.4.17 ShengJia Machinery

- 6.4.18 Derrick Fine Mesh

- 6.4.19 KOSUN Machinery

- 6.4.20 DFE

- 6.4.21 Southwest Petroleum University Tech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

油氣膨脹封隔器市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地點、地區和競爭格局分類,2021-2031年

油氣膨脹封隔器市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地點、地區和競爭格局分類,2021-2031年 2026-2030年全球旋轉轉向系統市場

2026-2030年全球旋轉轉向系統市場 旋轉導向系統市場:2026-2032年全球市場預測(按系統類型、井型、鑽井深度、應用和最終用戶分類)電動挖土機市場:按類型、額定功率、鏟鬥容量、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測粉筆壓井歧管市場:按類型、井類型、壓力等級、材質和應用分類-2026年至2032年全球預測

旋轉導向系統市場:2026-2032年全球市場預測(按系統類型、井型、鑽井深度、應用和最終用戶分類)電動挖土機市場:按類型、額定功率、鏟鬥容量、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測粉筆壓井歧管市場:按類型、井類型、壓力等級、材質和應用分類-2026年至2032年全球預測 2026年全球膨脹式封堵器市場報告膨脹式封堵器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、膨脹類型、應用、地區和競爭格局分類,2021-2031年)頁岩振動篩市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、運作類型、安裝方式、驅動系統、應用、地區和競爭格局分類,2021-2031年旋轉導向工具市場按類型、操作方式、井深、應用和最終用途分類-全球預測,2026-2032年礦用挖掘車輛市場按推進類型、產品類型、挖掘能力、應用和最終用戶分類,全球預測(2026-2032)

2026年全球膨脹式封堵器市場報告膨脹式封堵器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、膨脹類型、應用、地區和競爭格局分類,2021-2031年)頁岩振動篩市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、運作類型、安裝方式、驅動系統、應用、地區和競爭格局分類,2021-2031年旋轉導向工具市場按類型、操作方式、井深、應用和最終用途分類-全球預測,2026-2032年礦用挖掘車輛市場按推進類型、產品類型、挖掘能力、應用和最終用戶分類,全球預測(2026-2032)