|

市場調查報告書

商品編碼

2063236

袋式過濾器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Bag Filter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

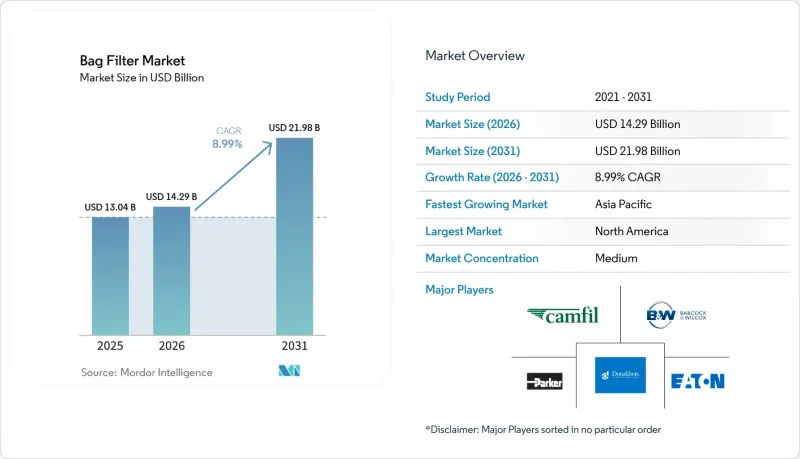

據 Mordor Intelligence 稱,2025 年袋式過濾器市值為 130.4 億美元,預計到 2031 年將達到 219.8 億美元,而 2026 年為 142.9 億美元,預測期(2026-2031 年)複合年成長率為 8.9%。

本報告按類型(脈衝噴氣、反吹式、振動式)、濾材(紡織品、不織布、玻璃纖維及其他)、應用(抑塵、空氣污染控制、產品回收、水處理及其他)、最終用戶(發電、水泥、化工及其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球袋式過濾器市場趨勢及洞察

更嚴格的工業排放法規

中國對新建燃煤發電廠的顆粒物排放限值設定為低於30毫克/立方米,印度則規定水泥窯的顆粒物排放限值低於50毫克/立方米,因此安裝布基過濾器對於遵守至關重要。歐盟工業排放指令的修訂降低了允許的粉塵閾值,金屬和垃圾焚化發電發電廠正在進行維修。伊利諾州將於2025年1月起禁止使用聚四氟乙烯(PTFE)纖維,美國環保署(EPA)也要求揭露全氟烷基和多氟烷基物質(PFAS)的使用情況,促使人們對等離子處理聚酯和奈米纖維氈展開調查。因此,供應商需要管理兩類產品系列——面向亞洲市場的PTFE產品和麵向歐美市場的無氟產品——以維持ISO 14001和區域空氣品質認證。能夠自主完成紗線擠出、膜流延和後處理的垂直整合型企業最能應對這種兩極化的情況。

新興亞洲地區煤炭和生質能發電能力的擴張

中國計劃在2025年運作78吉瓦的新燃煤電廠,併計劃同年再投產161吉瓦,同時291吉瓦的管道裝機容量將確保對袋式除塵器(除塵器)的持續需求。印度水泥製造商計劃在2026年至2028年間將其破碎產能提高1.6億至1.7億噸,是過去三年增速的三倍。同時,東協電力公司正在採用生質能混燒技術,由此產生的灰燼的化學特性要求配備冗餘的脈衝噴氣管線以確保可靠性。這些並行投資正在推動高溫、高容量袋式除塵器市場的成長,抵消了其他地區燃煤發電廠逐步淘汰的影響。

經合組織國家燃煤發電廠建設放緩

在美國和歐盟,關閉的燃煤發電廠電廠數量超過了新建電廠的數量,預計到2025年,煤炭在美國電力供應中的比例將低於20%。因此,這些地區對袋式過濾器的需求嚴重偏向維修和售後濾袋,這給設備銷售帶來了壓力,但也幫助多元化供應商在耗材方面保持了盈利能力。

細分市場分析

預計到2025年,脈衝噴氣除塵器將佔總銷售額的63.9%,並持續以9.5%的複合年成長率成長至2031年。這主要得益於中國數吉瓦燃煤發電廠對連續清潔和確保排放低於30毫克/立方米的迫切需求。脈衝噴氣採用差壓感知器最佳化電磁閥啟動時間,每年可節省高達15%的壓縮空氣。反吹式除塵系統應用於製藥和特種化學品行業中難以處理的粉末生產線,而振動篩除塵器則繼續應用於鋸木廠和穀倉等注重簡易性而非性能的場所。弗羅伊登貝格公司2026年推出的低壓損濾材進一步提升了脈衝噴氣除塵器的能源效率。 GEMCO木質顆粒指南建議的集中式脈衝噴氣集塵機連接多個粉塵源,可降低30%的安裝成本,這也凸顯了這種配置在袋式除塵器市場佔據主導地位的原因。

預計到2025年,不織布將佔據55.1%的市場。這主要擴充性的針刺生產流程,該工藝允許在表面塗覆聚四氟乙烯(PTFE)或等離子處理層,從而增強防水性能,同時成本比機織織物低25%。杭州恆科每月50萬張的產能充分展現了其在全球供應中的規模優勢。玻璃纖維用於支撐垃圾焚化發電發電廠的煙道結構,這些煙道的溫度超過260°C,但其脆性和易酸腐蝕性限制了其應用。熱塑性氈的自動化熱焊接過程消除了針孔,並將爆破強度提高了30%,使不織布成為無菌食品和藥品包裝袋的理想選擇。向不含全氟烷基和多氟烷基物質(PFAS)塗層的轉變正在加速對等離子室和奈米纖維生產線的投資,預計到2031年,不織布的複合年成長率將保持在9.4%。

區域分析

北美地區受益於煤炭向天然氣的轉型、PFAS法規的實施以及新澤西州和北卡羅來納州密集的製藥產業叢集,預計到2025年將佔全球銷售額的40.3%。伊利諾州對聚四氟乙烯(PTFE)的禁令以及美國環保署(EPA)的資訊揭露要求,迫使供應商對無氟毛氈進行認證,這使得擁有自主等離子技術的垂直整合型製造商更具優勢。唐納森公司斥資8.2億美元收購Facets公司,進一步鞏固了其在成熟設備市場中進軍耗材領域的策略。

預計到2031年,亞太地區的複合年成長率將達到11.6%,這主要得益於中國計劃到2025年新增78吉瓦燃煤發電廠裝機容量,以及印度計劃將水泥產量提高1.6億至1.7億噸。中國和印度窯爐嚴格的顆粒物排放標準(分別為30毫克/立方公尺和50毫克/立方公尺)進一步凸顯了對布袋除塵器的需求。東南亞國協生質能混燒產生的腐蝕性灰燼也推動了對耐化學腐蝕毛氈和冗餘布袋除塵器的需求。

在歐洲,修訂後的《工業排放指令》正在加強粉塵排放法規,PFAS(全氟烷基和多氟烷基物質)的禁用也在推進,這使得人們對不含PFAS的濾材和預測性維護感測器產生了濃厚的興趣。 LoRaWAN在英國工廠的部署,凸顯了該地區在數位化維護領域的主導地位。在俄羅斯、南美洲和中東,採礦、水泥和石化計畫數量不斷成長,中國OEM廠商正積極在資本成本方面競爭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強工業排放法規

- 新興亞洲地區煤炭和生質能發電產能擴張

- 加強水泥和採礦業的生產能力

- 從ESP系統升級並過渡到Bughouse系統

- 在布袋除塵器中引入預測性維護感測器

- 用於製藥胜肽生產線溶劑回收的袋式過濾器

- 市場限制因素

- 經合組織國家燃煤發電廠建設放緩

- 聚酯/PTFE濾材的價格波動

- 結合濾筒和靜電除塵器的混合解決方案正在蠶食袋式過濾器的市場佔有率。

- 人們對聚四氟乙烯塗層袋中 PFAS 的擔憂

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 脈衝噴氣袋式過濾器

- 反向氣囊過濾器

- 搖袋過濾器

- 濾材

- 紡織媒體

- 不織布介質

- 玻璃纖維介質

- 其他

- 透過使用

- 抑塵

- 空氣污染防治

- 產品召回

- 水處理

- 其他

- 最終用戶

- 發電

- 水泥生產

- 化工/石油化工產品

- 製藥和生物技術

- 食品/飲料加工

- 採礦和冶金

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Donaldson Company Inc.

- Parker-Hannifin Corp.

- Camfil AB

- Babcock & Wilcox Enterprises

- Eaton Corp. plc

- Thermax Ltd.

- Danaher(Pall Corp.)

- Mitsubishi Power

- WL Gore & Associates

- Nederman Holding AB

- Ahlstrom-Munksjo Oyj

- American Air Filter(AAF Flanders)

- Menardi Filters

- Sly Inc.

- Lenntech BV

- JK Fenner(India)Ltd.

- Filtra-Systems Co.

- Aircon Corporation

- Hangzhou Filter Technology(China)

- Lydall Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the bag filter market size was valued at USD 13.04 billion in 2025 and is estimated to grow from USD 14.29 billion in 2026 to reach USD 21.98 billion by 2031, at a CAGR of 8.99% during the forecast period (2026-2031).

This report is Segmented by Type (Pulse Jet, Reverse Air, Shaker), Filter Media (Woven, Non-Woven, Glass Fiber, Others), Application (Dust Control, Air Pollution Control, Product Recovery, Water Treatment, Others), End-User (Power Generation, Cement, Chemical, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Bag Filter Market Trends and Insights

Stricter Industrial Emission Regulations

China enforces sub-30 mg/Nm3 particulate limits for new coal plants, while India mandates sub-50 mg/Nm3 for cement kilns, making fabric filtration compulsory for compliance. The European Union's Industrial Emissions Directive revision reduces permitted dust thresholds, driving retrofits across metals and waste-to-energy sites. Illinois banned PTFE textiles effective January 2025, and the U.S. EPA now requires PFAS usage disclosure, pushing research into plasma-treated polyester and nanofiber felts. Suppliers must therefore manage dual portfolios, PTFE for Asia and fluorine-free for Western markets, to remain certified under ISO 14001 and regional air-quality codes. Vertically integrated companies that control yarn extrusion, membrane casting, and post-treatment are best placed to navigate this split.

Expansion of Coal and Biomass Capacity in Emerging Asia

China commissioned 78 GW of new coal units in 2025 and proposed another 161 GW during the same year, with a 291 GW pipeline ensuring sustained baghouse demand . India's cement producers plan 160-170 million ton of grinding additions in fiscal 2026-28, triple their prior three-year pace, while ASEAN utilities co-fire biomass, which creates ash chemistry that requires redundant pulse-jet lines for reliability. These parallel investments anchor high-temperature, high-volume bag filter market growth and offset coal retirements elsewhere.

Slowdown of Coal Power Build-Out in OECD

The United States and the European Union retire more coal units than they build, and coal generated less than 20% of U.S. electricity in 2025 . Bag filter demand in these regions, therefore, tilts toward retrofits and aftermarket bags, pressuring equipment sales but sustaining consumables revenue for diversified suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions in Cement and Mining Industries

- Retrofit Shift from ESP to Baghouse Systems

- Volatile Prices of Polyester and PTFE

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pulse-jet units captured 63.9% of 2025 revenue and are on track for a 9.5% CAGR through 2031, supported by multi-gigawatt coal plants in China that require continuous cleaning and sub-30 mg/Nm3 guarantees. Pulse-jet designs integrate differential-pressure sensors that optimize solenoid timing, saving up to 15% compressed air per year. Reverse-air systems serve fragile powder lines in pharmaceuticals and specialty chemicals, while shaker units persist in sawmills and grain elevators where simplicity trumps performance. Freudenberg's 2026 low-pressure-drop media further improve energy efficiency in pulse-jet installations. Centralized pulse-jet collectors that link several dust sources, as promoted in the GEMCO wood-pellet guide, cut installed cost by 30% and demonstrate why this configuration dominates the bag filter market.

Non-woven felts held 55.1% share in 2025, thanks to scalable needle-punch production that keeps cost 25% below woven fabrics while allowing PTFE or plasma top-layers for hydrophobicity. Hangzhou Hengke's 500,000-piece monthly capacity exemplifies the scale that underpins global supply. Glass fiber supports waste-to-energy stacks above 260 °C, though brittleness and acid attack limit volumes. Automated heat-welding of thermoplastic felts removes stitch holes, boosting burst strength by 30% and making non-woven designs attractive for sterile-grade food and pharma bags. The shift to PFAS-free coatings accelerates investments in plasma chambers and nanofiber lines, sustaining a 9.4% CAGR for non-woven media through 2031.

Geography Analysis

North America generated 40.3% of 2025 revenue, supported by coal-to-gas retrofits, PFAS legislation, and dense pharmaceutical clusters in New Jersey and North Carolina. Illinois' PTFE ban and EPA disclosure rules force suppliers to qualify fluorine-free felts, favoring vertically integrated producers with in-house plasma technology. Donaldson's USD 820 million Facet deal underscores the push for consumables exposure in a mature equipment market.

Asia-Pacific will post an 11.6% CAGR to 2031, led by China's 78 GW of 2025 coal additions and India's 160-170 million ton cement expansion pipeline. Tight particulate standards of 30 mg/Nm3 in China and 50 mg/Nm3 in Indian kilns cement the need for fabric filtration. ASEAN biomass co-firing introduces corrosive ash that drives demand for chemically resistant felts and redundant baghouses.

Europe tightens dust limits under the updated Industrial Emissions Directive and advances PFAS bans, favoring PFAS-free media and predictive sensors. LoRaWAN deployments across UK factories prove the region's leadership in digital maintenance. Russia, South America, and the Middle East add mining, cement, and petrochemical projects where Chinese OEMs compete aggressively on capital cost.

- Donaldson Company Inc.

- Parker-Hannifin Corp.

- Camfil AB

- Babcock & Wilcox Enterprises

- Eaton Corp. plc

- Thermax Ltd.

- Danaher (Pall Corp.)

- Mitsubishi Power

- WL Gore & Associates

- Nederman Holding AB

- Ahlstrom-Munksjo Oyj

- American Air Filter (AAF Flanders)

- Menardi Filters

- Sly Inc.

- Lenntech B.V.

- JK Fenner (India) Ltd.

- Filtra-Systems Co.

- Aircon Corporation

- Hangzhou Filter Technology (China)

- Lydall Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter industrial emission regulations

- 4.2.2 Expansion of coal- & biomass-fired capacity in emerging Asia

- 4.2.3 Capacity additions in cement & mining industries

- 4.2.4 Retrofit shift from ESP to baghouse systems

- 4.2.5 Predictive-maintenance sensor adoption in baghouses

- 4.2.6 Solvent-recovery bag filters in pharmaceutical peptide lines

- 4.3 Market Restraints

- 4.3.1 Slowdown of coal power build-out in OECD

- 4.3.2 Volatile prices of polyester/PTFE filter media

- 4.3.3 Hybrid cartridge-ESP solutions eroding bag filter share

- 4.3.4 PFAS concerns over PTFE-coated bags

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Pulse Jet Bag Filters

- 5.1.2 Reverse Air Bag Filters

- 5.1.3 Shaker Bag Filters

- 5.2 By Filter Media

- 5.2.1 Woven Media

- 5.2.2 Non-Woven Media

- 5.2.3 Glass Fiber Media

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Dust Control

- 5.3.2 Air Pollution Control

- 5.3.3 Product Recovery

- 5.3.4 Water Treatment

- 5.3.5 Others

- 5.4 By End-user

- 5.4.1 Power Generation

- 5.4.2 Cement Production

- 5.4.3 Chemical and Petrochemicals

- 5.4.4 Pharmaceutical and Biotech

- 5.4.5 Food and Beverage Processing

- 5.4.6 Mining and Metallurgy

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Donaldson Company Inc.

- 6.4.2 Parker-Hannifin Corp.

- 6.4.3 Camfil AB

- 6.4.4 Babcock & Wilcox Enterprises

- 6.4.5 Eaton Corp. plc

- 6.4.6 Thermax Ltd.

- 6.4.7 Danaher (Pall Corp.)

- 6.4.8 Mitsubishi Power

- 6.4.9 WL Gore & Associates

- 6.4.10 Nederman Holding AB

- 6.4.11 Ahlstrom-Munksjo Oyj

- 6.4.12 American Air Filter (AAF Flanders)

- 6.4.13 Menardi Filters

- 6.4.14 Sly Inc.

- 6.4.15 Lenntech B.V.

- 6.4.16 JK Fenner (India) Ltd.

- 6.4.17 Filtra-Systems Co.

- 6.4.18 Aircon Corporation

- 6.4.19 Hangzhou Filter Technology (China)

- 6.4.20 Lydall Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment