|

市場調查報告書

商品編碼

2062484

石油和天然氣基礎設施:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Oil and Gas Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

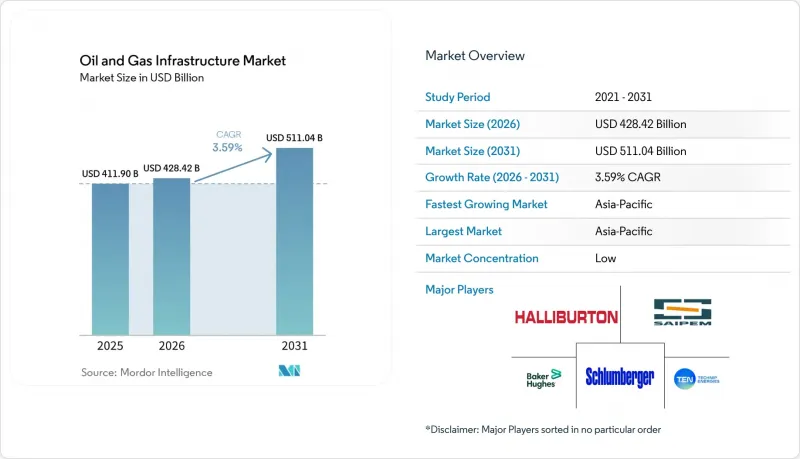

根據 Mordor Intelligence 預測,石油和天然氣基礎設施市場規模將在 2025 年達到 4,119 億美元,2026 年達到 4,284.2 億美元,2031 年達到 5,110.4 億美元,2026 年至 2031 年的複合年成長率為 3.59%。

本報告按類型(管道、倉儲設施、加工和精煉設備、鑽探平臺、液化天然氣進出口終端、壓縮機和泵站)、應用(探勘和生產、運輸及其他)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球油氣基礎設施市場趨勢與洞察

老舊管線的更新周期

2025年,北美業者新增天然氣管線輸送量達每日63億立方英尺,但其中大部分只是替換了上世紀六、七十年代安裝的腐蝕管路。同年,華盛頓向19個州撥款1.96億美元聯邦津貼,用於防腐蝕和鋼管升級改造。在大西洋彼岸的歐洲,約40%的高壓管道網路建於1980年之前,監管機構正敦促根據ISO 16708標準縮短檢查週期。此舉推高了對高品質鋼材和自動化焊接設備的短期需求。俄羅斯天然氣工業股份公司(Gazprom)計劃在2028年前退役8,000公里幹線管道,並將資金用於建造一條新的北極管道。這表明,適應貿易格局變化的項目被優先考慮,而對老舊資產的投資則被擱置。雖然鋼材價格上漲有時會延遲訂單,但總體而言,這波升級改造浪潮為管道製造商和防腐蝕供應商提供了持續的利多。

全球液化天然氣貿易擴張

預計到2025年,液化天然氣貿易量將達4.12億噸,年增4.8%。這反映了歐洲需要彌補俄羅斯管道天然氣供應減少1550億立方公尺的缺口,以及亞洲持續從煤炭轉向天然氣的趨勢。美國三個液化天然氣出口終端-卡爾卡修通道2號、黃金通道和普拉克明斯-預計2025年獲得最終批准,到2020年代末,總合將新增每年3,960萬噸的額定處理能力。在歐洲,2022年至2025年間運作了850億立方公尺的再氣化能力。其中三分之一是透過浮體式儲存再氣化裝置(FSRU)實現的,這實現了快速部署並降低了初始成本。卡達計劃在2025年保持其在全球出口中20%的佔有率,但2026年3月霍爾木茲海峽的封鎖迫使其宣布部分貨物運輸受不可抗力影響,這暴露了該海峽狹窄航道的集中風險。雖然基礎設施擴建可以增強系統韌性,但如果長期天然氣需求受到抑制,可再生能源的普及也會加劇人們對擱淺資產的擔憂。

原油價格劇烈波動

2026年初,全球原油供應過剩140萬至250萬桶/日,布蘭特原油均價為每桶62至65美元。 2026年3月霍爾木茲海峽危機導致油價飆升至每桶78美元,但隨著戰略儲備的釋放和好望角航線的改道,油價在10天內恢復正常。營運商通常要求油價達到或超過每桶70美元才會批准建造長週期平台和跨境管道。因此,油價若長期低於每桶70美元,將會延後最終的投資決策。 2026年初,美國頁岩油鑽探公司削減了8%的預算,優先考慮股東回報而非增產,這導致相關收集系統的擴建工程停滯。拉丁美洲的國營企業也面臨類似的壓力。巴西石油公司(Petrobras)推遲了原定於2025年投入使用的兩艘浮體式生產船,而YPF公司也推遲了其在瓦卡穆埃爾塔地區投資25億美元的干線管道擴建計劃。

細分市場分析

在所有資產類別中,LNG接收站的擴張速度最快,預計2031年將維持7.0%的年成長率。然而,到2025年,管道仍將佔油氣基礎設施市場佔有率的42.8%。 2022年至2025年間,光是歐洲就將新增850億立方公尺的再氣化能力,主要依賴可在一年內錨碇的浮體式儲存再氣化裝置(FSRU)。儲存基礎設施也不斷增加,因為布魯塞爾方面規定每年11月1日前庫存目標必須達到90%,這刺激了洞穴倉儲設施的改造和新的鹽丘浸出作業。煉油加工設施的發展趨勢則是喜憂參半。預計到2025年,全球名目產能將達到每日1.02億桶,但隨著電動車的日益普及,經合組織國家的運轉率徘徊在82%左右,這顯示成熟市場存在產能合理化的潛力。

同時,鑽探平臺和海底系統正受益於深海開發的復甦。巴西石油公司(Petrobras)於2025年訂購了四艘浮體式生產儲卸油船(FPSO),總價值達140億美元。預計每艘船的日處理能力為18萬桶。壓縮站正在進行電氣化維修。 2025年,Cenovas公司在福斯特溪(Foster Creek)安裝了25台總合裝置容量為16兆瓦的馬達組,將燃料氣燃燒量減少了18%。 2026年,德希尼布能源公司(Technip Energy)獲得了卡達北部西液化天然氣(LNG)擴建計畫價值12億美元的EPC合約。該專案採用模組化工廠,與傳統的現場組裝大型企劃相比,現場安裝時間縮短了18個月。因此,預計未來十年與LNG接收站相關的石油和天然氣基礎設施市場規模將超過新建長途管道的市場規模,從而重組整個價值鏈的資本投資分配結構。

區域分析

2025年,北美地區的支出佔全球總支出的34.7%。這主要得益於能源傳輸公司(Energy Transfer)在中游領域的50億至55億美元的資本投資,以及三座大型液化天然氣出口終端的建設獲批,這些終端將鞏固美國作為全球最大液化天然氣出口國的地位,預計到2030年這一地位將得到鞏固。加拿大TC能源公司運作價值60億美元的資產,並批准另外36.3億美元的項目,同時也將完成沿太平洋海岸的Coast Gaslink天然氣管道項目,為加拿大液化天然氣公司(LNG Canada)供應天然氣。在墨西哥東南部工業區,管道輸送能力仍無法滿足需求,導致該地區繼續依賴昂貴的現貨液化天然氣,這也凸顯了跨境擴張方面尚未開發的機會。

預計到2031年,亞太地區將成為成長最快的地區,年複合成長率將達到6.3%,這主要得益於印度數百億美元的基礎設施發展計畫以及印尼批准建設Tankro和Mako等海上樞紐計畫。馬來西亞的BIGST天然氣叢集預計將於2025年做出最終投資決定(FID),並於2029年開始供氣。馬來西亞國家石油公司(Petronas)的Rosmali Marjoram專案計畫日供氣8億立方英尺。日本和韓國更嚴格的液化天然氣(LNG)庫存要求(90天用量)進一步推高了對地下倉儲設施租賃的需求,進口終端的累積訂單依然強勁。

在歐洲,隨著來自俄羅斯的1,550億立方公尺管線天然氣供應逐步減少,大量資金正持續投入擴建再氣化終端和倉儲設施。截至2025年10月1日,庫存水準將達到83%,距離歐盟11月份設定的90%的目標僅差一個月,儘管來自俄羅斯的供應有所減少,但在寒潮期間,天然氣提取速度仍然受到限制。憑藉GASCADE公司的氫氣管道和Fluxys公司20億歐元的維修計劃,該地區在混合天然氣運輸技術領域處於領先地位。南美的投資主要集中在巴西,巴西石油公司(Petrobras)訂購了一個價值12億美元的海底建設項目,計劃於2025年完工,並增加了浮體式生產船的訂單,而阿根廷的瓦卡穆埃爾塔油田仍然受到管道瓶頸的困擾。中東和非洲既擁有龐大的低成本蘊藏量,也面臨地緣政治風險。儘管2026年3月運輸中斷,卡達仍維持了2025年全球液化天然氣出口20%的佔有率。阿拉伯聯合大公國正在將其富查伊拉倉儲設施擴建4,200萬桶,而莫三比克的珊瑚北計畫則表明,浮體式液化天然氣可以在不進行陸上大型企劃的情況下促進深海油田的開發。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 老舊管線的更新周期

- 全球液化天然氣貿易擴張

- 增加對深海和超深海油田的資本投資

- 國家能源安全計劃

- 管道氫氣污染維修

- 利用數位雙胞胎進行預測性維護和營運管理

- 市場限制因素

- 原油價格劇烈波動

- 淨零排放和ESG驅動的資本配置轉變

- 模組化浮體式液化天然氣系統的競爭

- 網路安全問題導致專案延期

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 管道

- 儲存設施

- 加工和精煉單元

- 鑽探平臺

- 液化天然氣進出口終端

- 壓縮機和抽水站

- 透過使用

- 探勘與生產

- 運輸

- 加工/提煉

- 倉儲/配送

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Schlumberger

- Halliburton

- Baker Hughes

- Technip Energies

- Saipem

- Wood PLC

- Fluor Corporation

- Worley

- Petrofac

- National Oilwell Varco

- McDermott International

- CPECC

- KBR Inc.

- Bechtel Corporation

- Subsea 7

- Aker Solutions

- JGC Corporation

- Larsen & Toubro

- Samsung Engineering

- TC Energy

- Kinder Morgan

- Enbridge

第7章 市場機會與未來展望

According to Mordor Intelligence, the oil and gas infrastructure market size was USD 411.90 billion in 2025 and is expected to reach USD 428.42 billion in 2026 and reach USD 511.04 billion by 2031, growing at a CAGR of 3.59% over 2026-2031.

This report is Segmented by Type (Pipelines, Storage Facilities, Processing and Refining Units, Drilling Platforms, LNG Import/Export Terminals, Compressor and Pumping Stations), Application (Exploration and Production, Transportation, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Oil and Gas Infrastructure Market Trends and Insights

Ageing Pipeline Replacement Cycle

North American operators added 6.3 billion cubic feet per day of new gas-line capacity in 2025, yet most construction simply swapped out corroded segments installed in the 1960s and 1970s . Washington disbursed USD 196 million of federal grants to 19 states for corrosion control and steel-line upgrades that same year . Across the Atlantic, about 40% of Europe's high-pressure grid predates 1980, encouraging regulators to tighten inspection intervals under ISO 16708, a move that is driving short-cycle demand for high-grade steel and automated welding equipment. Gazprom intends to retire 8,000 kilometers of trunk lines by 2028 and redirect funds toward newer Arctic routes, illustrating how aging assets are being de-prioritized in favor of projects that match shifting trade patterns. Collectively, the replacement wave is a durable catalyst for pipe mills and corrosion-protection vendors even though steel-price spikes occasionally delay orders.

Rising Global LNG Trade

LNG trade climbed to 412 million tons in 2025, a 4.8% year-over-year rise that reflected Europe's need to offset the loss of 155 billion cubic meters of Russian pipeline volumes and Asia's ongoing coal-to-gas switch . Three U.S. export terminals, Calcasieu Pass 2, Golden Pass, and Plaquemines, gained final approval in 2025 and will collectively add 39.6 million tons per annum of nameplate capacity by decade-end. Europe commissioned an additional 85 billion cubic meters of regasification space between 2022 and 2025, one-third of which was realized via floating storage and regasification units, enabling rapid deployment and lowering upfront costs . Qatar retained a 20% global export share in 2025 but was forced to declare force majeure on specific cargoes during the March 2026 Strait of Hormuz disruption, exposing concentration risk in the Strait's narrow shipping lane. Although the build-out strengthens system resilience, it also amplifies stranded-asset concerns should renewable penetration curb long-term gas demand.

Extreme Oil-Price Volatility

Brent averaged USD 62 to USD 65 per barrel in early 2026 amid a 1.4 million- to 2.5 million-barrel-per-day global surplus. The March 2026 Strait of Hormuz scare briefly lifted prices to USD 78, but values normalized within ten days following strategic-reserve releases and route diversions around the Cape of Good Hope. Operators typically need a USD 70-plus threshold to green-light long-cycle platforms and cross-border pipelines; therefore, prolonged sub-USD 70 pricing defers final investment decisions. U.S. shale drillers cut budgets by 8% in early 2026, prioritizing shareholder returns over volume growth, which then suspends related gathering-system expansions. Latin American national companies felt similar pressure: Petrobras postponed two floating production vessels in 2025, and YPF deferred a USD 2.5 billion trunk-line expansion serving Vaca Muerta.

Other drivers and restraints analyzed in the detailed report include:

- Deep- & Ultra-Deep-Water CAPEX Upswing

- National Energy-Security Programs

- Net-Zero & ESG Capital-Allocation Shifts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LNG terminals are expanding the fastest among asset classes, clocking a 7.0% annual growth rate through 2031, even though pipelines still held 42.8% of the oil and gas infrastructure market share in 2025. Europe alone added 85 billion cubic meters of regasification capacity between 2022 and 2025, leaning heavily on floating storage and regasification units that can be moored in under a year. Storage infrastructure is rising in tandem because Brussels mandates a 90% inventory target each November 1, encouraging cavern conversions and new salt-dome leaching. Refining and processing units face mixed fortunes: global nameplate capacity touched 102 million barrels per day in 2025, but OECD utilization hovered near 82% amid rising electric-vehicle penetration, signaling potential rationalization in mature markets.

Drilling platforms and subsea systems, however, are benefiting from a deep-water renaissance. Petrobras placed orders for four floating production, storage, and offloading vessels in 2025, cumulatively worth USD 14 billion, each slated for 180,000-barrel-per-day throughput. Compressor stations are undergoing electrification retrofits; Cenovus installed 25 electric units totaling 16 megawatts at Foster Creek in 2025, lowering fuel-gas burn by 18%. Technip Energies captured a USD 1.2 billion EPC contract for Qatar's North Field West LNG expansion in 2026, a project embracing modular trains that cut field-erection times by 18 months compared with stick-built megaprojects. The oil & gas infrastructure market size for LNG terminals is therefore poised to surpass that of new long-haul pipelines in the next decade, reshaping capex allocation across the value chain.

Geography Analysis

North America captured 34.7% of 2025 spending, driven by USD 5 billion to USD 5.5 billion of midstream capex from Energy Transfer and the sanctioning of three major LNG export terminals that will consolidate the United States' position as the world's largest LNG shipper by 2030. Canada's TC Energy commissioned USD 6 billion of assets in 2025 and green-lit another USD 3.63 billion, while completing Coastal GasLink to feed LNG Canada on the Pacific Coast. Mexico's industrial southeast still relies on expensive spot LNG cargoes because pipeline capacity lags demand, underlining an untapped opportunity for cross-border expansions.

Asia-Pacific is the fastest-growing zone at a 6.3% CAGR to 2031, propelled by India's multi-hundred-billion-dollar infrastructure drive and Indonesia's approval of offshore hubs such as Tangkulo and Mako. Malaysia's BIGST cluster reached final investment decision in 2025, with first gas expected in 2029, and Petronas' Rosmari-Marjoram project aims to deliver 800 million cubic feet per day. Japan and South Korea's stricter 90-day LNG reserves mandate is spurring additional cavern leasing, keeping import-terminal EPC order books healthy.

Europe continues to funnel capital into regasification terminals and storage expansions as it phases out 155 billion cubic meters of Russian pipeline supply. Inventory reached 83% by October 1, 2025, only one month shy of the bloc's 90% November target despite lower Russian volumes, yet draw-down rates remain constrained during cold snaps. GASCADE's hydrogen-ready line and Fluxys' EUR 2 billion retrofit plan place the region at the forefront of mixed-gas transmission technology. South America's capex is concentrated in Brazil, where Petrobras awarded USD 1.2 billion of subsea work in 2025 and is ramping up floating production vessel orders, though Argentina's Vaca Muerta remains hampered by pipeline bottlenecks. The Middle East and Africa combine vast low-cost reserves with geopolitical risk: Qatar maintained a 20% share of global LNG exports in 2025 despite the March 2026 shipping disruption. The UAE boosted Fujairah storage by 42 million barrels, and Mozambique's Coral Norte is proving that floating LNG can unlock deep-water fields without onshore megaprojects.

- Schlumberger

- Halliburton

- Baker Hughes

- Technip Energies

- Saipem

- Wood PLC

- Fluor Corporation

- Worley

- Petrofac

- National Oilwell Varco

- McDermott International

- CPECC

- KBR Inc.

- Bechtel Corporation

- Subsea 7

- Aker Solutions

- JGC Corporation

- Larsen & Toubro

- Samsung Engineering

- TC Energy

- Kinder Morgan

- Enbridge

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing Pipeline Replacement Cycle

- 4.2.2 Rising Global LNG Trade

- 4.2.3 Deep- & Ultra-Deep-water CAPEX Upswing

- 4.2.4 National Energy-Security Programs

- 4.2.5 Pipeline Hydrogen-Blending Retrofits

- 4.2.6 Digital-Twin-based Predictive O&M

- 4.3 Market Restraints

- 4.3.1 Extreme Oil-Price Volatility

- 4.3.2 Net-Zero & ESG Capital-Allocation Shifts

- 4.3.3 Modular Floating-LNG Competition

- 4.3.4 Cyber-security Driven Project Delays

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Pipelines

- 5.1.2 Storage Facilities

- 5.1.3 Processing and Refining Units

- 5.1.4 Drilling Platforms

- 5.1.5 LNG Import/Export Terminals

- 5.1.6 Compressor and Pumping Stations

- 5.2 By Application

- 5.2.1 Exploration and Production

- 5.2.2 Transportation

- 5.2.3 Processing and Refining

- 5.2.4 Storage and Distribution

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 Technip Energies

- 6.4.5 Saipem

- 6.4.6 Wood PLC

- 6.4.7 Fluor Corporation

- 6.4.8 Worley

- 6.4.9 Petrofac

- 6.4.10 National Oilwell Varco

- 6.4.11 McDermott International

- 6.4.12 CPECC

- 6.4.13 KBR Inc.

- 6.4.14 Bechtel Corporation

- 6.4.15 Subsea 7

- 6.4.16 Aker Solutions

- 6.4.17 JGC Corporation

- 6.4.18 Larsen & Toubro

- 6.4.19 Samsung Engineering

- 6.4.20 TC Energy

- 6.4.21 Kinder Morgan

- 6.4.22 Enbridge

7 Market Opportunities & Future Outlook

- 7.1 Emerging Markets & Investment Hotspots

- 7.2 Green Infrastructure & Sustainability Trends

- 7.3 Digital Transformation & Smart Infrastructure

- 7.4 Public Private Partnerships & Policy Support

石油和天然氣產業資本投資市場-2026-2032年全球預測石油與天然氣工程服務市場-2026-2032年全球市場預測

石油和天然氣產業資本投資市場-2026-2032年全球預測石油與天然氣工程服務市場-2026-2032年全球市場預測 石油和天然氣測量儀器市場規模、佔有率和成長分析:按類型、技術、產品、應用、最終用戶和地區分類 - 產業預測,2026-2033年油氣中游設備市場:依設備類型、材料類型、應用、最終用途及通路分類-2026-2032年全球市場預測

石油和天然氣測量儀器市場規模、佔有率和成長分析:按類型、技術、產品、應用、最終用戶和地區分類 - 產業預測,2026-2033年油氣中游設備市場:依設備類型、材料類型、應用、最終用途及通路分類-2026-2032年全球市場預測 中型油氣設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年油氣上游活動市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、鑽井類型、最終用戶、地區和競爭格局分類,2021-2031年

中型油氣設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年油氣上游活動市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、鑽井類型、最終用戶、地區和競爭格局分類,2021-2031年 石油和天然氣化學品市場:按應用和地區分類

石油和天然氣化學品市場:按應用和地區分類 公共交通遠端資訊處理市場預測—按解決方案類型、應用、最終用戶和地區分類的全球分析—2034年

公共交通遠端資訊處理市場預測—按解決方案類型、應用、最終用戶和地區分類的全球分析—2034年 2026年全球電池儲能EPC(工程、採購和施工)市場報告潛艦切割解決方案市場:依切割技術、服務類型、部署方式、動力來源、應用與最終用途分類-2026-2032年全球預測

2026年全球電池儲能EPC(工程、採購和施工)市場報告潛艦切割解決方案市場:依切割技術、服務類型、部署方式、動力來源、應用與最終用途分類-2026-2032年全球預測