|

市場調查報告書

商品編碼

2062483

微型電池:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Micro Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

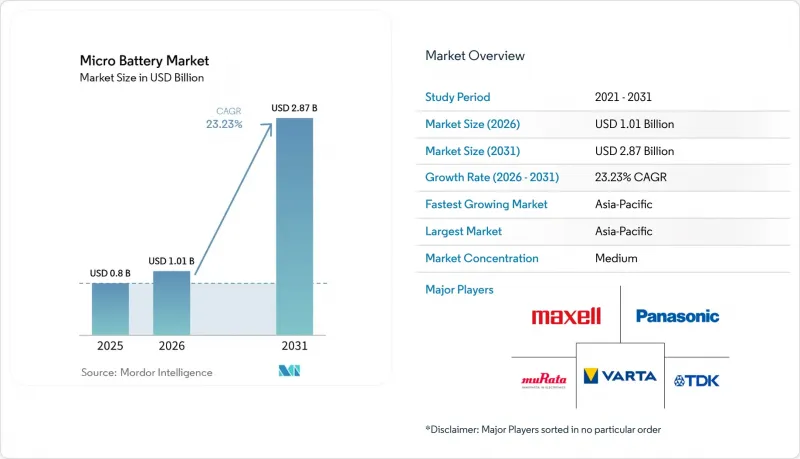

根據 Mordor Intelligence 預測,微型電池市場規模將從 2025 年的 8 億美元成長到 2026 年的 10.1 億美元,到 2031 年達到 28.7 億美元,2026 年至 2031 年的複合年成長率為 23.23%。

本報告按類型(薄膜、固體、印刷/軟性、紐扣型及其他)、應用(醫療設備、穿戴式裝置、智慧卡/RFID、感測器、配件及其他)、最終用戶(醫療保健、家用電子電器、工業、汽車、國防及其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球微型電池市場趨勢與洞察

穿戴式裝置的普及

智慧型手錶、戒指式設備和穿戴式音訊設備的出貨量持續推動著微型電池市場的需求。由於高密度電芯和自適應電源管理技術的整合,開放式耳機的運作時間已從2025年的5-6小時延長至2026年的8-12小時。 Ensurge公司於2024年發布的650-750 Wh/L固態電池設計正瞄準這些穿戴式音頻設備,因為它們無需使用易燃的液態電解質,這對於耳道內的佩戴者而言是一項關鍵的安全優勢。預計到2025年,軟性紙電池的市場規模將達到25億美元,它透過將電源直接嵌入紡織基板中,無需增加重量和體積的剛性外殼。全球音訊設備對IEC 62368-1標準的遵守,使得品牌越來越依賴經過認證的微型電池供應商來降低產品責任風險。

植入式醫療用電子設備的成長

微型心臟節律器、神經刺激設備和藥物輸送泵依靠微型電池來延長更換週期並降低手術風險。美國食品藥物管理局 (FDA) 的品管法規將於 2026 年 2 月生效,該法規要求電池供應商提供電芯層級的可追溯性,迫使規模較小的企業將合規工作外包或退出市場。 Ilika 於 2026 年 1 月向 Cirtec Medical 交付了首批 Stereax M300固態電池的大宗訂單,而其他 21 家設備製造商仍在進行臨床檢驗。利用心室運動回收能量的實驗原型表明,未來有望實現無電池植入,但長期生物相容性研究仍在進行中。 2025 年電池故障預警發布後,監管機構加強了審查,導致對 ISO 13485 認證供應商的需求增加。

固體微型電池製造成本高

真空沉澱、專用前驅體和低通量批量生產製程使得固態電池的成本比鋰離子電池高出3到5倍。 ProLogium公司位於敦克爾克的工廠設定了2029年實現4吉瓦時產能和低於每千瓦時150美元成本的目標,但其資本負擔巨大。乾電極生產線可將能耗降低47%,前景可觀,但尚未在微型電池規模上驗證。 Elevated Materials公司在2025年交付了超過100公里的鋰金屬薄膜,但需要在2026年之前將產量提高三倍,這凸顯了薄膜供應鏈的瓶頸。在成本降低之前,固態電池的應用可能主要集中在醫療、國防和高階穿戴式裝置領域。

細分市場分析

到2025年,薄膜電池將佔據微型電池市場35.4%的佔有率,其應用基礎主要集中在醫療植入和智慧卡領域,在這些領域,長期認證至關重要。固態電池預計將以26.2%的複合年成長率成長,這主要得益於ProLogium的860 Wh/L平台和Ilika的大規模生產擴張。這些電池系統對監管嚴格的醫療設備和國防設備極具吸引力,因為它們滿足了設計人員對亞毫米級厚度的要求,並且無需使用易燃的液態電解質。印刷電池和軟性電池已佔據一次性感測器和智慧包裝市場,在這些市場中,超低成本和形狀柔軟性比最大容量更為重要。紐扣電池在汽車鑰匙和手錶中仍然必不可少,因為現有的生產線能夠以每單位幾美分的價格提供久經考驗的可靠性。

製造地的現狀反映了產量和利潤率的不同趨勢。 ProLogium位於桃園的工廠預計到2025年將出貨超過60萬顆電池,證明了卷軸式薄膜製造流程的擴充性。同時,Zinergy和Flint分別新增了數千平方公尺的紙基電池生產空間,用於生產一次性應用。對結合微型電池和能量收集器的混合化學技術的研究投入不斷增加,正推動微型電池市場向多電源架構發展,從而在不增加外形規格下延長其使用壽命。

區域分析

預計到2025年,亞太地區將佔據41.8%的銷售佔有率。這主要得益於中國在電池製造領域的領先地位,以及日本對固態電池研發提供的6.6億美元補助。寧德時代(CATL)在前驅體採購方面的規模經濟正在降低整個全部區域供應鏈的成本結構。韓國製造商雖然被垂直整合的中國競爭對手搶佔了部分市場佔有率,但他們正在重新投資固態電池生產線以恢復利潤率。 ProLogium公司位於敦克爾克的4GWh專案計畫於2029年運作,屆時將為歐洲原始設備製造商(OEM)提供在地採購的選擇,有助於降低地緣政治風險。

在北美,由於國防法規禁止使用中國製造的零件,供應鏈網路正在重組。美國陸軍的標準化戰術通用電池(STUB)標準要求供應商必須事先獲得國內認證,並將供應商的選擇範圍限制在符合標準的製造商。 NEO電池材料公司位於韓國的基地為美國無人機專案提供零件,這些專案需要符合第4872條的規定。

在歐洲,歐盟國防基金的津貼正被用於開發兩用可同時為民用穿戴設備和士兵系統供電的微型電池。 HARVEST計畫就是一個典型的例子,該計畫將於2026年至2027年獲得資助,它既滿足北約的互通性要求,也符合歐盟電池監管可追溯性規則。南美洲以及中東和非洲地區仍然依賴進口,由於外匯波動和當地生產能力有限,短期內推廣應用受到限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 穿戴式裝置的普及

- 植入式醫療用電子設備的成長

- 擴展物聯網邊緣—感測器網路

- 小型穿戴式音訊設備對電源的需求日益成長

- 自主型印刷電子產品的生態系統正在興起。

- 國防領域智慧塵埃感測器節點的應用

- 市場限制因素

- 固體微型電池製造成本高

- 與傳統紐扣電池相比,能量密度較低

- 薄膜沉積材料供應鏈中的限制因素

- 微型電池缺乏標準化測試規程

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 薄膜電池

- 固體電池

- 印刷/軟性電池

- 紐扣式微型電池

- 其他

- 透過使用

- 醫療器材

- 穿戴式電子產品

- 智慧卡和射頻識別

- 無線感測器節點

- 家用電子電器配件

- 其他

- 最終用戶

- 衛生保健

- 家用電子電器

- 工業自動化

- 汽車與出行

- 國防/航太

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Murata Manufacturing Co., Ltd.

- Maxell Holdings Ltd.

- Panasonic Corporation

- TDK Corporation

- VARTA AG

- Renata SA

- Cymbet Corporation

- Samsung SDI Co., Ltd.

- STMicroelectronics

- NEC Energy Solutions

- Ultralife Corporation

- EnerSys

- BrightVolt Inc.

- Blue Spark Technologies

- ProLogium Technology

- Ilika plc

- SolidEnergy Systems

- EVE Energy Co., Ltd.

- Imprint Energy

- BYD Company Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the micro battery market size is expected to increase from USD 0.8 billion in 2025 to USD 1.01 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 23.23% over 2026-2031.

This report is Segmented by Type (Thin-Film, Solid-State, Printed/Flexible, Button-Cell, Others), Application (Medical Devices, Wearables, Smart Cards/RFID, Sensors, Accessories, Others), End-User (Healthcare, Consumer-Electronics, Industrial, Automotive, Defense, Others), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

Global Micro Battery Market Trends and Insights

Proliferation of Wearable Devices

Shipments of smartwatches, rings, and hearables continue to lift micro battery market demand. Open-ear earbuds moved runtime from 5-6 hours in 2025 to 8-12 hours in 2026 after integrating higher-density cells and adaptive power management. Ensurge's 650-750 Wh/L solid-state design, released in 2024, targets these hearables because it removes flammable liquid electrolytes, a critical safety benefit inside the ear canal. Flexible paper batteries worth USD 2.5 billion in 2025 are embedding power directly into textile substrates, eliminating rigid housings that add weight and bulk. Global compliance with IEC 62368-1 for audio devices is steering brands toward certified micro-battery suppliers that can mitigate product-liability exposure.

Growth in Implantable Medical Electronics

Miniaturized pacemakers, neurostimulators, and drug-delivery pumps rely on micro batteries that extend replacement intervals and lower surgical risk. The FDA's February 2026 Quality Management System Regulation forces battery vendors to implement granular cell-level genealogy, pushing smaller firms to outsource compliance or exit the market. Ilika shipped its first revenue order of Stereax M300 solid-state cells to Cirtec Medical in January 2026, while 21 additional device makers remain in clinical validation. Research prototypes harvesting ventricular motion hint at future battery-free implants, yet long-term biocompatibility studies are still underway. Heightened regulatory scrutiny since a 2025 warning letter on battery failures is amplifying demand for suppliers with ISO 13485 accreditation .

High Manufacturing Cost of Solid-State Micro Batteries

Vacuum deposition, specialty precursors, and low-throughput batch processing leave solid-state cells at a 3-5 X cost premium over lithium-ion. ProLogium's Dunkirk site aims for 4 GWh by 2029 and a sub-USD 150 kWh cost target, but the capital burden is significant. Dry-electrode lines that cut energy use 47% are promising yet unproven at the micro-battery scale. Elevated Materials shipped over 100 km of lithium metal film in 2025 and must triple output in 2026, underscoring thin-film supply-chain bottlenecks . Until costs fall, adoption concentrates in medical, defense, and premium wearables.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of IoT Edge-Sensor Networks

- Rising Demand for Compact Hearable Power Sources

- Limited Energy Density vs. Conventional Coin Cells

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thin-film batteries held a 35.4% micro battery market share in 2025, anchored in medical implants and smart cards that value long qualification histories. Solid-state variants will grow at a 26.2% CAGR, powered by ProLogium's 860 Wh/L platform and Ilika's commercial ramp. These chemistries satisfy designer demands for sub-millimeter profiles and eliminate flammable liquid electrolytes, compelling in regulated healthcare and defense devices. Printed and flexible batteries captured disposable sensors and smart packaging, where ultralow cost and form flexibility matter more than maximum capacity. Button-cell formats remain essential in automotive key fobs and watches because incumbent production lines deliver proven reliability at cents-per-unit prices.

Manufacturing footprints reflect divergent volume and margin profiles. ProLogium's Taoyuan plant shipped over 600,000 cells in 2025, demonstrating roll-to-roll thin-film scalability, while Zinergy and Flint each added thousands of square meters of paper-battery floor space for single-use applications. Hybrid chemistries coupling micro batteries with energy harvesters are gaining research funding, positioning the micro battery market for multipower architectures that extend deployment lifetimes without enlarging form factors.

Geography Analysis

Asia-Pacific held 41.8% revenue share in 2025, supported by China's supremacy in battery manufacturing and Japan's USD 660 million subsidy for solid-state R&D. CATL's scale in precursor procurement lowers cost structures throughout the regional supply chain. Korean producers lost share to vertically integrated Chinese rivals, yet are reinvesting in all-solid-state lines to reclaim margin. ProLogium's 4 GWh Dunkirk project, scheduled for 2029, offers European OEMs a localized supply alternative that sidesteps geopolitical risk.

North America is reshaping supply networks under defense regulations that block Chinese content. The U.S. Army's standardized tactical universal battery (STUB) sizes force domestic pre-qualification, narrowing the vendor pool to compliant manufacturers. NEO Battery Materials' South Korean site serves U.S. drone programs seeking Section 4872 conformity.

Europe is channeling EU Defence Fund grants toward dual-use micro batteries that power both civilian wearables and soldier systems. HARVEST, funded in 2026-2027, exemplifies projects aligning with NATO interoperability needs while meeting EU battery regulation traceability rules. South America and MEA remain import-dependent, and currency volatility plus limited local manufacturing capacity restrain near-term uptake.

- Murata Manufacturing Co., Ltd.

- Maxell Holdings Ltd.

- Panasonic Corporation

- TDK Corporation

- VARTA AG

- Renata SA

- Cymbet Corporation

- Samsung SDI Co., Ltd.

- STMicroelectronics

- NEC Energy Solutions

- Ultralife Corporation

- EnerSys

- BrightVolt Inc.

- Blue Spark Technologies

- ProLogium Technology

- Ilika plc

- SolidEnergy Systems

- EVE Energy Co., Ltd.

- Imprint Energy

- BYD Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of wearable devices

- 4.2.2 Growth in implantable medical electronics

- 4.2.3 Expansion of IoT edge - sensor networks

- 4.2.4 Rising demand for compact hearable power sources

- 4.2.5 Self-powered printed-electronics ecosystem emerging

- 4.2.6 Defense adoption of smart-dust sensor nodes

- 4.3 Market Restraints

- 4.3.1 High manufacturing cost of solid-state micro batteries

- 4.3.2 Limited energy density v s. conventional coin cells

- 4.3.3 Supply-chain constraints for thin-film deposition materials

- 4.3.4 Lack of standardized micro-battery test protocols

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Thin-Film Batteries

- 5.1.2 Solid-State Micro Batteries

- 5.1.3 Printed/Flexible Batteries

- 5.1.4 Button-Cell Micro Batteries

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Medical Devices

- 5.2.2 Wearable Electronics

- 5.2.3 Smart Cards and RFID

- 5.2.4 Wireless Sensor Nodes

- 5.2.5 Consumer-Electronics Accessories

- 5.2.6 Others

- 5.3 By End-user

- 5.3.1 Healthcare

- 5.3.2 Consumer-Electronics

- 5.3.3 Industrial and Automation

- 5.3.4 Automotive and Mobility

- 5.3.5 Defense and Aerospace

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 Maxell Holdings Ltd.

- 6.4.3 Panasonic Corporation

- 6.4.4 TDK Corporation

- 6.4.5 VARTA AG

- 6.4.6 Renata SA

- 6.4.7 Cymbet Corporation

- 6.4.8 Samsung SDI Co., Ltd.

- 6.4.9 STMicroelectronics

- 6.4.10 NEC Energy Solutions

- 6.4.11 Ultralife Corporation

- 6.4.12 EnerSys

- 6.4.13 BrightVolt Inc.

- 6.4.14 Blue Spark Technologies

- 6.4.15 ProLogium Technology

- 6.4.16 Ilika plc

- 6.4.17 SolidEnergy Systems

- 6.4.18 EVE Energy Co., Ltd.

- 6.4.19 Imprint Energy

- 6.4.20 BYD Company Limited

7 Market Opportunities & Future Outlook

- 7.1 Emerging Technologies & Innovations

- 7.2 Expansion into Untapped Applications

- 7.3 Government Incentives & Funding

- 7.4 Long-term Growth Prospects

微型電池市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、電池類型、最終用戶、地區和競爭格局分類,2021-2031年

微型電池市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、電池類型、最終用戶、地區和競爭格局分類,2021-2031年 微型電池市場規模、佔有率和趨勢分析報告:按材料、類型、容量、電池類型、地區和細分市場分類(2026-2033 年)

微型電池市場規模、佔有率和趨勢分析報告:按材料、類型、容量、電池類型、地區和細分市場分類(2026-2033 年) 微型電池市場:按技術、外形尺寸、可充電/不可充電、容量範圍和應用分類-2026-2032年全球市場預測

微型電池市場:按技術、外形尺寸、可充電/不可充電、容量範圍和應用分類-2026-2032年全球市場預測 微型電池市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、裝置、最終用戶、功能及安裝配置分類

微型電池市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、裝置、最終用戶、功能及安裝配置分類 微型電池市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球微型電池市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球固體微型電池市場規模、佔有率、趨勢和成長分析報告(2026-2034)

微型電池市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球微型電池市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球固體微型電池市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球微型電池市場報告SMD全固態電池市場按電解液材料、電池類型、容量範圍和應用分類,全球預測(2026-2032)手錶用微型電池市場:按產品類型、化學成分、應用、通路和最終用戶分類-2026年至2032年全球預測

2026年全球微型電池市場報告SMD全固態電池市場按電解液材料、電池類型、容量範圍和應用分類,全球預測(2026-2032)手錶用微型電池市場:按產品類型、化學成分、應用、通路和最終用戶分類-2026年至2032年全球預測