|

市場調查報告書

商品編碼

2062475

節能維修:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Energy Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

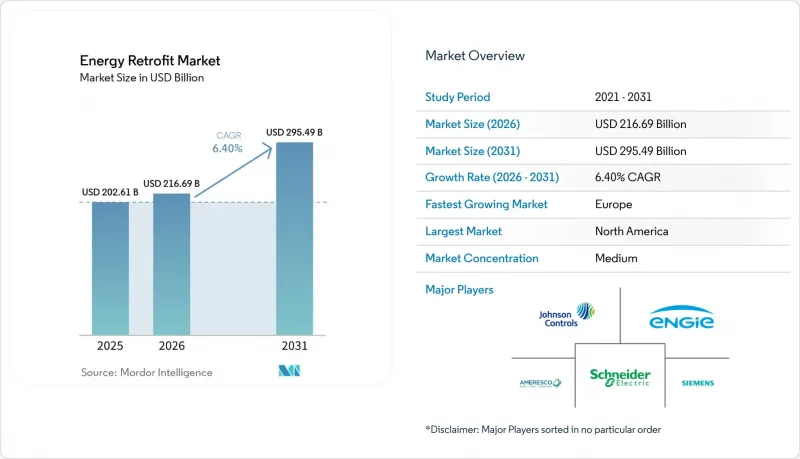

根據 Mordor Intelligence 預測,能源維修市場規模將從 2025 年的 2,026.1 億美元成長到 2026 年的 2,166.9 億美元,到 2031 年達到 2,954.9 億美元,2026 年至 2031 年的複合年成長率為 6.40%。

本報告按維修規模(大型節能維修、小規模/微維修)、技術(暖通空調系統、照明系統、建築圍護結構等)、應用(住宅、商業建築等)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球能源維修市場趨勢及洞察

政府關於能源效率的強制性規定和獎勵

修訂後的歐盟建築能源性能指令將於2024年納入成員國國內法,屆時將確立法定維修要求,將自願維修轉變為法律義務。德國在2024年透過其「建築節能改造計畫」(BEG)投入135億歐元進行節能維修。法國的「MaPrimeRenov」計畫為熱泵安裝提供了26億歐元的津貼。在美國,《通貨膨脹控制法》第179D條規定,對於節能50%的項目,每平方英尺可獲得5美元的稅額扣抵。同時,《兩黨基礎設施法案》透過節能和能源效率專案津貼注入了35億美元。在日本,修訂後的《建築節能法》將於2025年4月生效,該法將強制所有新建非住宅建築達到能源效率標準,從而引發一波積極的維修。在韓國,零能耗建築(ZEB)的強制性要求將於2025年6月擴大到所有面積超過500平方公尺的公共建築。此外,首爾還建立了一項補貼制度,最高可補貼50%的維修費用。

企業淨零排放 ESG 承諾正在加速對維修的需求。

大型企業正將維修成本直接納入其基於科學的排放藍圖。宜家計劃在2030年實現所有門市淨零能耗,並計劃在2024年底在400個地點安裝總合1.7吉瓦的屋頂太陽能發電系統。李維斯承諾在2027年維修其90%的設施,並將能源強度降低40%。舊金山聯邦儲備銀行2024年的一項研究表明,公佈基於科學的目標的公司在節能項目上的投資比同行高出23%。同時,資金籌措方式也在不斷發展。 2024年,匯豐銀行為歐洲房地產投資信託基金(REITs)設計了一筆5億美元的永續發展掛鉤貸款,使它們能夠隨著其已檢驗投資組合的能源強度降低而降低借貸成本。

儘管技術成本下降,但初始資本支出(CAPEX)仍然很高。

綜合維修專案通常將建築外圍維修、暖通空調系統升級和控制系統整合整合到一個專案中,導致典型支出高達六位數甚至七位數。 2024 年對不列顛哥倫比亞省的一項Meta分析顯示,大型維修的中位數成本為每平方英尺 150 至 250 加元(110 至 185 美元),即使有補貼,簡單的投資回收期也超過 15 年,遠遠超過許多投資者的持有期。歐盟委員會估計,到 2030 年,為實現維修目標,每年將面臨 950 億歐元的資金缺口。類似的資金缺口在印度也令人擔憂,68% 的受訪業主表示,初始成本是他們採取行動的主要障礙。綠色銀行和在建融資等新方法前景可期,但目前仍僅限於美國部分州和歐盟國家。

細分市場分析

到2025年,「淺層維修」將佔節能維修市場規模的64.4%,這反映出業主傾向於選擇那些投資回報快、干擾小且能節省15-25%能源的措施,例如更換LED照明、安裝智慧溫控器和增加低成本隔熱材料材料。雖然大規模維修屬於資本密集項目,但由於淨零排放法規要求建築群的能源強度降低50%以上,其年複合成長率仍高達8.6%。美國「更佳建築計劃」(Better Building Initiative)計畫中38%的節能中位數凸顯了節能改造的潛在效益,並為採用能源效率掛鉤融資的長期折舊計畫提供了依據。

該產業的價值鏈正呈現兩極化。電氣承包商主導大型和小規模項目,而大型維修項目則吸引了專業工程公司的參與,這些公司能夠根據績效合約整合建築外圍護結構改造、機械設備升級和可再生能源裝置。被動式房屋認證正逐漸成為可靠性的指標,預計到2024年,全球將有1840個維修項目獲得認證,比2022年成長64%。歐洲投資銀行向波蘭和羅馬尼亞的多用戶住宅大型維修項目提供的2億歐元貸款表明,投資者對以節能效益為支撐的債務結構的興趣日益濃厚。

區域分析

由於美國聯邦政府的慷慨稅收優惠和各州綠色銀行貸款計劃,預計北美地區到2025年將佔能源維修市場收入的38.9%。隨著加州2026年新建商業建築的太陽能和儲能要求擴展到維修項目,預計該地區的監管將進一步收緊。

歐洲預計將以9.0%的複合年成長率成長,受益於《建築能源性能指令》(EPBD)嚴格的合規期限以及數十億歐元的補貼計劃,例如德國的《能源效率法案》(BEG)和英國的公共部門脫碳津貼。然而,歐盟委員會警告稱,每年將出現950億歐元的資金缺口,這促使人們開發創新金融產品,例如用於維修的房屋抵押貸款組合和歐盟支持的擔保計畫。

亞太地區的趨勢各不相同。中國的「十四五」規劃目標是到2025年實現3.5億平方公尺的維修,但各省的實施情況差異很大。在日本,更嚴格的建築節能標準將於2025年4月生效,這引發了中心商業區的維修熱潮。同時,在韓國,積極的零能耗建築政策推動了公共設施的維修,並提供50%的補貼。在拉丁美洲、中東和非洲,巴西的PROCEL和阿拉伯聯合大公國的Estidama等大型計畫正在為未來擴大規模的法規奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府關於節能的強制規定和獎勵

- 企業為實現淨零排放和ESG(環境、社會和治理)目標所做的努力,正在加速維修的需求。

- 經合組織國家中需要維修的破舊建築存量

- 電力和天然氣價格的波動促使人們進行維修,優先考慮投資回收。

- 利用人工智慧驅動的建築孿生分析挖掘隱藏的成本降低潛力

- 擴大基於績效和基於ESG的貸款的採用。

- 市場限制因素

- 儘管技術成本下降,但初始資本投資仍相對較高。

- 房東和房客之間獎勵不匹配的困境。

- 大型維修缺乏技術純熟勞工和專案經理

- 績效風險的識別與衡量不確定性

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 投資和資金籌措趨勢

第5章 市場規模與成長預測

- 按維修規模

- 大規模能源維修

- 小規模、小型節能維修

- 透過技術

- 暖通空調系統

- 照明系統

- 建築圍護結構(隔熱材料和玻璃)

- 可再生能源(光伏發電、太陽熱能發電)的併網

- 智慧建築控制和物聯網

- 熱水供應和管道

- 透過使用

- 住宅大樓

- 商業建築

- 工業設施

- 公共及公共設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Johnson Controls

- Ameresco

- Siemens AG

- Schneider Electric

- ENGIE

- Honeywell International

- ABB

- Daikin Industries

- Trane Technologies

- Carrier Global

- Bouygues Energies & Services

- Veolia Energy

- Enel X

- Rockwool Group

- Kingspan Group

- NORESCO

- Cenergistic

- Eaton Corporation

- Comfort Systems USA

- EMCOR Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the energy retrofit market size is expected to increase from USD 202.61 billion in 2025 to USD 216.69 billion in 2026 and reach USD 295.49 billion by 2031, growing at a CAGR of 6.40% over 2026-2031.

This report is Segmented by Retrofit Depth (Deep Energy Retrofits, Shallow/Light Energy Retrofits), Technology (HVAC Systems, Lighting Systems, Building Envelope, and More), Application (Residential Buildings, Commercial Buildings, and More), and Geography Geography (North America, Europe, Asia-Pacific, South America and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Energy Retrofit Market Trends and Insights

Government Energy-Efficiency Mandates & Incentives

The European Union's recast Energy Performance of Buildings Directive, transposed by member states in 2024, sets statutory renovation requirements that convert optional upgrades into legal obligations. Germany disbursed EUR 13.5 billion for efficiency upgrades under its BEG program during 2024, and France's MaPrimeRenov' added EUR 2.6 billion to subsidize heat-pump installations. In the United States, Section 179D of the Inflation Reduction Act now offers a USD 5 per-square-foot deduction for projects achieving 50% energy cuts, while the Bipartisan Infrastructure Law funneled USD 3.5 billion through Energy Efficiency and Conservation Block Grants. Japan's revised Building Energy Conservation Law, effective April 2025, imposed mandatory savings standards on all new non-residential properties, prompting a wave of pre-emptive retrofits. South Korea's Zero Energy Building mandate was extended to all public buildings above 500 square meters in June 2025, complemented by a Seoul subsidy that covers up to 50% of retrofit costs.

Corporate Net-Zero/ESG Commitments Accelerating Retrofit Demand

Large enterprises are writing retrofit spending directly into science-based emission-reduction roadmaps. IKEA aims to upgrade every owned store to net-zero energy by 2030, installing 1.7 GW of rooftop solar across 400 sites by end-2024. Levi Strauss has committed to retrofit 90% of its facilities by 2027 to slash energy intensity 40%. The Federal Reserve Bank of San Francisco's 2024 study showed that firms with public science-based targets devote 23% more capital to efficiency projects compared with peers. Financing tools are evolving in tandem: HSBC arranged a USD 500 million sustainability-linked loan for a European REIT in 2024, reducing borrowing costs as verified portfolio energy intensity falls.

High Upfront CAPEX Despite Falling Tech Costs

Comprehensive retrofits often group envelope upgrades, HVAC replacements, and controls integration into one project, pushing typical spends into six- or seven-figure territory. A 2024 British Columbia meta-analysis found median deep-retrofit costs of CAD 150-250 per square foot (USD 110-185), with simple payback exceeding 15 years even after subsidies, far longer than many investors' hold periods. The European Commission pegs the annual funding gap for its 2030 renovation target at EUR 95 billion. Similar gaps loom in India, where 68% of surveyed owners cited upfront cost as the primary deterrent to action. Emerging tools such as green banks and on-bill financing are promising but remain limited to select U.S. states and a handful of EU nations.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Building Stock in OECD Economies Requiring Upgrades

- Volatile Electricity & Gas Prices Prompting Payback-Driven Retrofits

- Landlord-Tenant Split-Incentive Dilemma

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shallow retrofits captured 64.4% of the 2025 Energy Retrofit Market size, reflecting owners' preference for quick-payback measures such as LED relamping, smart thermostats, and low-cost insulation top-ups that deliver 15%-25% savings with minimal disruption. Deep retrofits, though capital-intensive, are expanding at an 8.6% CAGR as net-zero mandates push portfolios toward more than 50% cuts in energy intensity. Median savings of 38% in U.S. Better Buildings Initiative projects underscore the upside, justifying long amortization schedules under efficiency-linked financing.

Industry value chains are bifurcating. Electrical contractors dominate high-volume shallow works, while deep projects attract specialist engineering firms that can integrate envelope redesign, mechanical upgrades, and renewable installations under outcome-based contracts. Passive House certification is emerging as a credibility marker, with 1,840 certified retrofit projects worldwide in 2024, up 64% from 2022. The European Investment Bank's EUR 200 million facility for multifamily deep retrofits in Poland and Romania demonstrates growing investor appetite for savings-backed debt structures.

Geography Analysis

North America captured 38.9% of the 2025 Energy Retrofit Market revenue, buoyed by generous U.S. federal tax incentives and state-level green-bank financing programs. The region's regulatory push will intensify as California's 2026 solar-plus-storage mandate for new commercial buildings spills over into retrofit scopes.

Europe, forecast to grow at 9.0% CAGR, benefits from the EPBD's hard compliance deadlines and multi-billion-euro subsidy pools such as Germany's BEG and the U.K.'s Public Sector Decarbonisation grants. Yet the European Commission warns of a EUR 95 billion annual financing gap, spurring creative instruments like renovation mortgage portfolios and EU-backed guarantee schemes.

Asia-Pacific trends are heterogeneous. China's 14th Five-Year Plan targets 350 million m2 of retrofits by 2025, but enforcement differs widely by province. Japan's April 2025 building-energy code stiffening is triggering a wave of upgrades in the commercial core, while South Korea's aggressive zero-energy mandate is catalyzing half-subsidized retrofits in public stock. Latin America and the Middle East-Africa, though flagship programs, Brazil's PROCEL and the UAE's Estidama, are laying regulatory foundations for future scale.

- Johnson Controls

- Ameresco

- Siemens AG

- Schneider Electric

- ENGIE

- Honeywell International

- ABB

- Daikin Industries

- Trane Technologies

- Carrier Global

- Bouygues Energies & Services

- Veolia Energy

- Enel X

- Rockwool Group

- Kingspan Group

- NORESCO

- Cenergistic

- Eaton Corporation

- Comfort Systems USA

- EMCOR Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government energy-efficiency mandates & incentives

- 4.2.2 Corporate net-zero/ESG commitments accelerating retrofit demand

- 4.2.3 Ageing building stock in OECD economies requiring upgrades

- 4.2.4 Volatile electricity & gas prices prompting payback-driven retrofits

- 4.2.5 AI-enabled building-twin analytics uncovering hidden savings

- 4.2.6 Growing adoption of outcome-based financing & ESG-linked loans

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX despite falling tech costs

- 4.3.2 Landlord-tenant split-incentive dilemma

- 4.3.3 Shortage of deep-retrofit skilled labor & project managers

- 4.3.4 Performance-risk perception & measurement uncertainty

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment & Funding Trends

5 Market Size & Growth Forecasts

- 5.1 By Retrofit Depth

- 5.1.1 Deep Energy Retrofits

- 5.1.2 Shallow/Light Energy Retrofits

- 5.2 By Technology

- 5.2.1 HVAC Systems

- 5.2.2 Lighting Systems

- 5.2.3 Building Envelope (Insulation and Glazing)

- 5.2.4 Renewable Integration (Solar PV, Solar Thermal)

- 5.2.5 Smart Building Controls and IoT

- 5.2.6 Water Heating and Plumbing

- 5.3 By Application

- 5.3.1 Residential Buildings

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial Facilities

- 5.3.4 Public and Institutional Buildings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Johnson Controls

- 6.4.2 Ameresco

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric

- 6.4.5 ENGIE

- 6.4.6 Honeywell International

- 6.4.7 ABB

- 6.4.8 Daikin Industries

- 6.4.9 Trane Technologies

- 6.4.10 Carrier Global

- 6.4.11 Bouygues Energies & Services

- 6.4.12 Veolia Energy

- 6.4.13 Enel X

- 6.4.14 Rockwool Group

- 6.4.15 Kingspan Group

- 6.4.16 NORESCO

- 6.4.17 Cenergistic

- 6.4.18 Eaton Corporation

- 6.4.19 Comfort Systems USA

- 6.4.20 EMCOR Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

能源維修系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、應用、地區和競爭格局分類,2021-2031年

能源維修系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、應用、地區和競爭格局分類,2021-2031年 能源效率評估市場預測至2034年-按審計類型、審計範圍、服務類型、建築類型、應用、最終用戶和地區分類的全球分析能源效率審計市場預測至2034年-按審計類型、審計範圍、服務類型、建築類型、應用、最終用戶和地區分類的全球分析

能源效率評估市場預測至2034年-按審計類型、審計範圍、服務類型、建築類型、應用、最終用戶和地區分類的全球分析能源效率審計市場預測至2034年-按審計類型、審計範圍、服務類型、建築類型、應用、最終用戶和地區分類的全球分析 能源維修市場:按產品、應用和地區分類

能源維修市場:按產品、應用和地區分類 能源維修系統市場:依產品類型、技術、維修等級及最終用戶分類-2026-2032年全球預測

能源維修系統市場:依產品類型、技術、維修等級及最終用戶分類-2026-2032年全球預測 維修服務市場規模、佔有率和成長分析:按服務類別、建築類型、目標組件、服務模式和地區分類-2026-2033年產業預測

維修服務市場規模、佔有率和成長分析:按服務類別、建築類型、目標組件、服務模式和地區分類-2026-2033年產業預測 能源維修系統市場規模、佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。

能源維修系統市場規模、佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。 2026年全球能源維修系統市場報告全球冷媒改裝服務市場(按設備類型、服務類型、容量和最終用戶分類)預測(2026-2032年)能源市場校準服務(按服務模式、計量表類型、最終用戶產業和校準頻率分類)全球預測(2026-2032 年)

2026年全球能源維修系統市場報告全球冷媒改裝服務市場(按設備類型、服務類型、容量和最終用戶分類)預測(2026-2032年)能源市場校準服務(按服務模式、計量表類型、最終用戶產業和校準頻率分類)全球預測(2026-2032 年)