|

市場調查報告書

商品編碼

2062469

鹼性燃料電池:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Alkaline Fuel Cells - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

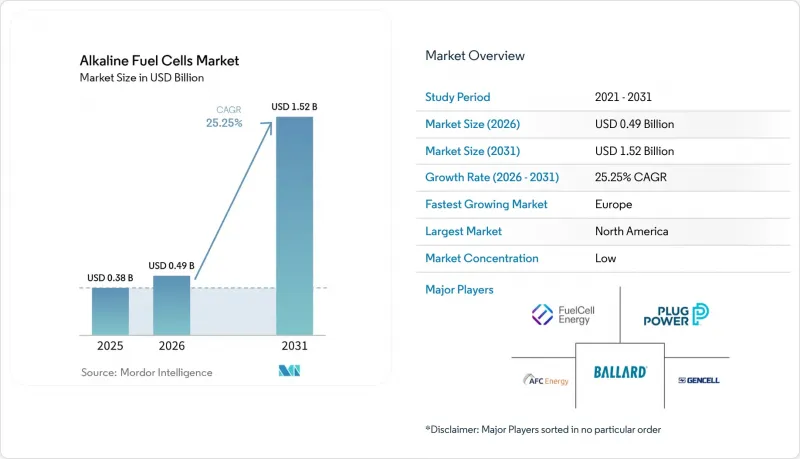

據 Mordor Intelligence 稱,2025 年鹼性燃料電池市值為 3.8 億美元,預計到 2031 年將達到 15.2 億美元,而 2026 年為 4.9 億美元,預測期(2026-2031 年)的複合年成長率為 25.25%。

本報告按類型(固定式鹼性燃料電池和行動/可攜式鹼性燃料電池)、功率輸出(5kW以下、5-50kW、50kW以上)、應用領域(軍事和國防、太空船和發射系統、備用和遠端電源等)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元(USD)計價。

全球鹼性燃料電池市場趨勢與洞察

電解槽成本的降低提高了商業性可行性。

大規模生產已將20兆瓦以下鹼性電解槽的資本投資降低至每千瓦389.50美元,而大規模容量的裝置則進一步降低至每千瓦82.80美元,從而縮小了氫能與石化燃料之間的成本差距。鎳基電極不使用鉑族金屬,降低了組件成本風險,並將電堆壽命延長至8萬小時以上。有針對性的研發支持,例如美國能源局向Avium公司提供的津貼,持續提升催化劑的效率和耐久性。歐盟的類似措施正在資助下一代鹼性技術,加速推進到2030年實現40吉瓦可再生氫電解槽的部署。這些進展提高了短期資金籌措潛力,並支撐了鹼性燃料電池市場的積極成長。

軍方對靜音電源系統的需求日益成長

國防機構正在加快採購,以安靜、高能量密度的氫能解決方案取代噪音大的柴油發電機。美國陸軍在白沙飛彈靶場部署的首個氫能奈米電網,已證明其能夠為全天候離網監控供電,並為更廣泛的基地部署奠定了基礎。士兵使用的攜帶式電源需要在0.1-3千瓦的功率範圍內達到超過1000瓦時/公斤的能量密度,而使用不含貴金屬的鎳基鹼性燃料電池堆可以輕鬆實現這一目標。歐洲各國軍隊也遵循類似的趨勢,德國聯邦國防軍訂購離網裝置就是一個例證。由此產生的短期需求將顯著擴大鹼性燃料電池市場規模,並降低製造商大規模生產計畫的風險。

電解的二氧化碳毒性限制了實施的柔軟性。

氫氧化鉀電解會與大氣中的二氧化碳反應生成碳酸鹽,隨著時間的推移,碳酸鹽會降低離子電導率和電解效率。高純氫氣和洗滌設備會增加成本和複雜性,阻礙其在二氧化碳濃度較高的工業環境中的應用。雖然膜技術創新提供了一個有前景的解決方案,但目前仍處於早期階段,短期內市場規模有限。

細分市場分析

2025年,固定式氫氣罐佔總銷售量的63.7%,主要得益於通訊、微電網和工業用戶對低度成本和數天自主運作的優先考量。 Verizon的行動電話基地台計畫表明,擺脫柴油燃料的趨勢正在持續推動對氫氣罐和維修備件的需求。可攜式和移動式氫氣罐雖然規模較小,但其年複合成長率高達27.3%,主要得益於軍方對5kW以下靜音電源的採購。美國特種作戰司令部在2025年訂購的500套氫氣罐凸顯了戰術性應用的日益普及。

輕質複合複合材料容器使氫氣重量減輕了一半,整合泵則縮小了周邊設備的面積,使得1-3千瓦的燃料電池組重量低於20公斤,運作可達48-72小時。商業用戶、電影攝製組和緊急應變人員都非常重視低噪音和快速加氫。儘管固定式裝置預計在2031年之前仍將主導鹼性燃料電池市場,因為大規模備用電源應用的需求超過了可攜式應用,但行動領域的成長表明,燃料電池的應用範圍正在向基礎設施以外的領域拓展。

區域分析

北美地區在每公斤氫氣3美元的稅額扣抵抵免和國防部合約的支持下,預計到2025年將佔全球氫氣銷售額的37.4% 。墨西哥灣沿岸的樞紐正在利用改造後的天然氣管道,而加拿大偏遠地區的礦場也正在逐步淘汰柴油燃料,以利用每公升2美元的氫氣價格差。墨西哥目前發展落後,但隨著美國氫氣產量的擴大,它有可能搭上跨境氫氣貿易的順風車。

預計到2031年,歐洲將成為成長最快的地區,複合年成長率將達到26.6%,主要得益於歐盟可再生能源計畫(REPowerEU)、德國90億歐元的氫能預算以及港口物流樞紐的氨裂解技術。再生能源指令III透過設定具有約束力的再生能源配額,確保鹼性燃料電池市場的長期發展,從而穩定了該市場。北歐水電以具有競爭力的成本提供低碳氫化合物,推動了資料中心和渡輪船隊的早期應用。

亞太地區的成長情況因地而異。日本和韓國正在補貼住宅燃料電池,而鹼性燃料電池仍主要應用於備用電源領域。澳洲和智利正在效仿加拿大的礦業微電網模式,中東港口正在考慮部署與氨出口和太陽能發電相結合的鹼性燃料電池輔助裝置。智利在南美洲的藍圖目標是2030年部署25吉瓦的電解槽,這意味著需要平衡下游燃料電池的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 降低電解槽成本

- 軍方對「靜音電源」的需求日益成長

- 對綠色氨燃料庫的需求日益成長

- 偏遠礦山中獨立可再生能源的整合

- 市場限制因素

- 二氧化碳引起的電解質中毒

- 短堆疊壽命與PEMFC的比較

- 鎳價波動對電極成本的影響

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 固定式鹼性燃料電池

- 移動式/可攜式鹼性燃料電池

- 依輸出類型

- 5千瓦或以下

- 5~50 kW

- 超過50千瓦

- 透過使用

- 軍事/國防

- 太空船和發射系統

- 備用/遠端電源

- 攜帶式電子設備

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- AFC Energy plc

- GenCell Ltd.

- Elcogen AS

- FuelCell Energy Inc.

- Plug Power Inc.

- Ballard Power Systems

- Ceres Power Holdings

- PHMatter LLC

- Apollo Energy Systems

- Next Hydrogen Solutions

- EvolOH Inc.

- Zhangjiagang Horizon Fuel Cell

- Nedstack Fuel Cell Technology

- Intelligent Energy Ltd.

- AlkaMem Ltd.

- Doosan Fuel Cell

- Siemens Energy AG

- Toshiba Energy Systems

- SFC Energy AG

- Johnson Matthey plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the alkaline fuel cells market size was valued at USD 0.38 billion in 2025 and is estimated to grow from USD 0.49 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 25.25% during the forecast period (2026-2031).

This report is Segmented by Type (Static Alkaline Fuel Cells and Mobile/Portable Alkaline Fuel Cells), Power Output (Up To 5 KW, 5 To 50 KW, and More), Application (Military and Defense, Spacecraft and Launch Systems, Backup and Remote Power, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Alkaline Fuel Cells Market Trends and Insights

Declining Electrolyzer Costs Drive Commercial Viability

Widespread scale-up brings alkaline electrolyzer capex to USD 389.5 per kW for sub-20 MW plants and USD 82.8 per kW for larger units, narrowing hydrogen's cost gap with fossil fuels. Nickel-based electrodes avoid platinum group metals, trimming bill-of-materials risk and pushing stack life beyond 80,000 h. Targeted R&D support, such as the U.S. Department of Energy's USD 5 million grant to Avium, continues to improve catalyst efficiency and longevity. Similar EU initiatives funnel funding toward next-generation alkaline technology, hastening the rollout of 40 GW of renewable hydrogen electrolyzers by 2030. These developments amplify near-term bankability and underpin the alkaline fuel cells market's aggressive growth path.

Growing Military Demand for Silent Power Systems

Defense establishments are accelerating procurement to replace noisy diesel generators with silent, high-energy-density hydrogen solutions. The U.S. Army's first hydrogen nanogrid at White Sands Missile Range validates 24/7 off-grid surveillance power and establishes a blueprint for broader base deployment. Soldier-portable targets call for over 1,000 Wh/kg energy densities at 0.1-3 kW, readily achievable with nickel-based alkaline stacks dispensing with precious metals. European forces mirror this trend, evidenced by Bundeswehr orders for off-grid units. Resultant near-term demand adds meaningful volume to the alkaline fuel cells market and de-risks manufacturers' scale-up plans.

CO2-Induced Electrolyte Poisoning Limits Deployment Flexibility

Potassium hydroxide electrolytes react with atmospheric CO2 to form carbonate salts, lowering ionic conductivity and cutting efficiency over time. High-purity hydrogen and scrubbing hardware add cost and complexity, discouraging deployment in CO2-rich industrial settings. Mitigation through membrane innovations is promising yet remains nascent, constraining near-term addressable volume.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Green Ammonia Bunkering Needs

- Stranded-Renewable Integration at Remote Mines

- Short Stack Life Compared with PEM Technology

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Static units captured 63.7% of 2025 revenue as telecom, microgrid, and industrial users valued low cost per kilowatt and multi-day autonomy. Verizon's national cell-tower program illustrates how diesel displacement creates recurring demand for hydrogen cartridges and service spares. Portable and mobile systems, although smaller, are advancing at 27.3% CAGR as militaries procure silent power below 5 kW. A 2025 U.S. Special Operations Command order for 500 units highlights rising tactical adoption.

Lighter composite vessels halve hydrogen weight, and integrated pumps shrink balance-of-plant footprints, enabling 1-3 kW packs under 20 kg that deliver 48-72 h runtime. Commercial users, film crews, and emergency responders value low noise and rapid refueling. Static installations will still command the bulk of the alkaline fuel cells market through 2031 because large-scale backup outspends portable volumes, yet mobile growth signals diversification beyond infrastructure.

Geography Analysis

North America generated 37.4% of 2025 revenue, buoyed by USD 3 kg-1 hydrogen production credits and Department of Defense contracts. Gulf Coast hubs leverage repurposed gas pipelines, while Canada's remote mines substitute diesel at USD 2 L-1 parity. Mexico lags but may piggyback on cross-border hydrogen trade as U.S. production scales.

Europe is the fastest-growing region at 26.6% CAGR to 2031, powered by REPowerEU, the EUR 9 billion German hydrogen budget, and port-side ammonia cracking for logistics hubs. The Renewable Energy Directive III sets binding RFNBO quotas that secure long-term offtake, stabilizing the alkaline fuel cells market. Nordic hydropower offers low-carbon hydrogen at competitive cost, driving early adoption in datacenters and ferry fleets.

Asia-Pacific growth is uneven. Japan and South Korea subsidize residential fuel cells, yet alkaline chemistries stay focused on backup duty. Australia and Chile replicate Canadian mine microgrids, while Middle East ports explore AFC auxiliary units tied to solar-linked ammonia exports. South America's Chilean roadmap targets 25 GW of electrolyzers by 2030, implying downstream fuel-cell balancing demand.

- AFC Energy plc

- GenCell Ltd.

- Elcogen AS

- FuelCell Energy Inc.

- Plug Power Inc.

- Ballard Power Systems

- Ceres Power Holdings

- PHMatter LLC

- Apollo Energy Systems

- Next Hydrogen Solutions

- EvolOH Inc.

- Zhangjiagang Horizon Fuel Cell

- Nedstack Fuel Cell Technology

- Intelligent Energy Ltd.

- AlkaMem Ltd.

- Doosan Fuel Cell

- Siemens Energy AG

- Toshiba Energy Systems

- SFC Energy AG

- Johnson Matthey plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Declining electrolyzer costs

- 4.1.2 Growing military demand for silent power

- 4.1.3 Rise of green ammonia bunkering needs

- 4.1.4 Stranded-renewable integration at remote mines

- 4.2 Market Restraints

- 4.2.1 CO2-induced electrolyte poisoning

- 4.2.2 Short stack life vs PEMFC

- 4.2.3 Nickel price volatility impact on electrode costs

- 4.3 Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Static Alkaline Fuel Cells

- 5.1.2 Mobile/Portable Alkaline Fuel Cells

- 5.2 By Power Output

- 5.2.1 Up to 5 kW

- 5.2.2 5 to 50 kW

- 5.2.3 Above 50 kW

- 5.3 By Application

- 5.3.1 Military and Defense

- 5.3.2 Spacecraft and Launch Systems

- 5.3.3 Backup and Remote Power

- 5.3.4 Portable Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AFC Energy plc

- 6.4.2 GenCell Ltd.

- 6.4.3 Elcogen AS

- 6.4.4 FuelCell Energy Inc.

- 6.4.5 Plug Power Inc.

- 6.4.6 Ballard Power Systems

- 6.4.7 Ceres Power Holdings

- 6.4.8 PHMatter LLC

- 6.4.9 Apollo Energy Systems

- 6.4.10 Next Hydrogen Solutions

- 6.4.11 EvolOH Inc.

- 6.4.12 Zhangjiagang Horizon Fuel Cell

- 6.4.13 Nedstack Fuel Cell Technology

- 6.4.14 Intelligent Energy Ltd.

- 6.4.15 AlkaMem Ltd.

- 6.4.16 Doosan Fuel Cell

- 6.4.17 Siemens Energy AG

- 6.4.18 Toshiba Energy Systems

- 6.4.19 SFC Energy AG

- 6.4.20 Johnson Matthey plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment