|

市場調查報告書

商品編碼

2062459

高頻交易伺服器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)High Frequency Trading Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

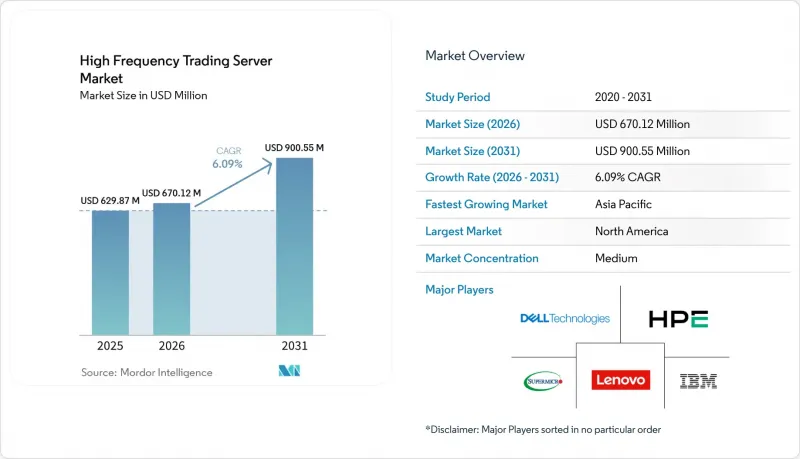

據 Mordor Intelligence 稱,2025 年高頻交易伺服器市值為 6.2987 億美元,預計到 2031 年將達到 9.0055 億美元,而 2026 年為 6.7012 億美元,預測期(2026-2031 年)的複合年成長率為 6.09%。

本報告按處理器架構(基於 x86 的伺服器、基於 ARM 的伺服器等)、外形尺寸(機架式伺服器、刀片式伺服器等)、應用領域(股票交易、外匯外匯等)、最終用戶(自營交易公司和市場創造者、投資銀行和證券公司等)以及地區進行細分。市場預測以美元計價。

全球高頻交易伺服器市場趨勢及洞察

演算法和人工智慧主導的交易量激增。

在發達的交易市場中,演算法交易佔股票訂單流的70%以上,強化學習代理現已直接整合到FPGA架構中,將交易週期縮短至奈秒級。歐洲證券及市場管理局(ESMA)於2026年2月發布的指導意見要求進行微秒級的交易前檢查,並優先考慮本地運算而非雲端終端。管理超過100億美元資產的量化基金正在交易所引擎附近部署具備推理能力的伺服器,將微秒級的縮短轉化為數百萬美元的滑點減少。隨著記憶體頻寬需求的不斷成長,諸如NVIDIA Grace等可提供每秒Terabyte連貫頻寬的ARM架構設計正在加速普及。因此,各大資料中心的異質伺服器出貨量正在結構性地成長。

對超低延遲基礎設施的需求

交易所近場主機正從 10Gigabit升級到 400Gigabit以太網,將往返時間縮短至不到 1 微秒,並為網卡設定了新的最低規格。 Kraken 於 2026 年 4 月在 Equinix LD5 開設了倫敦交易大廳,實現了亞毫秒級的歐洲交易所接入,並吸引了需要確定性交易流的加密貨幣市場創造者。 CME Aurora 與 Google Cloud 合作,新增了 42.8 萬平方英尺的架空地板空間,提供 17 千瓦的機櫃,用於支援雙路刀片伺服器節點和 FPGA 加速器。 DPDK 和 RDMA 等核心旁路協定堆疊如今已成為交易網卡的必備功能,進一步深化了伺服器設計與網路拓撲之間的協作。

託管機房和專用冷卻系統進行大量資本投入。

一級交換器鄰近機櫃每月租金為 6,000 至 9,600 美元,配備 10Gigabit網路連線;而高級機籠每月租金高達 15,000 美元,加上交叉連線費用,每個機架的年總支出超過 150,000 美元。升級到液冷系統需要 50,000 至 100,000 美元的初始成本,這迫使中型避險基金在預算限制下權衡延遲改善帶來的收益。沒有冷水循環系統的舊機房無法維修以容納高密度刀片伺服器,這促使企業遷移到新設施,並延長投資回收期。一些公司選擇虛擬專用伺服器 (VPN),以 20 微秒的延遲為代價,將每月成本降低到 2,000 美元以下,進一步分散了對尖端硬體的需求。

細分市場分析

隨著企業將能源效率和記憶體頻寬置於優先地位,基於 ARM 架構的伺服器預計將在 2026 年至 2031 年間保持最高成長率,複合年成長率 (CAGR) 預計達到 8.43%。 NVIDIA Grace CPU 擁有 72 個 Arm Neoverse V2 核心和每秒 1 Terabyte的頻寬,將於 2025 年開始出貨,從而實現先前需要雙路 x86 系統才能完成的即時風險模擬。 x86 系統憑藉數十年來針對 Intel 和 AMD 微程式碼最佳化的編譯交易邏輯,仍將保持其主導地位,預計到 2025 年將佔據高頻交易伺服器市場 74.32% 的佔有率。

ARM 的功率密度優勢通常可達 30-40%,這對於尋求每千瓦收益的託管服務提供者而言是一項顯著優勢。儘管重新編譯的障礙和有限的 ARM 原生 FPGA 工具正在減緩中小企業的轉型步伐,但像富士通、Arrcus 和 1Finity 於 2026 年 3 月達成的合作,表明各方對 ARM 設計在下一代機櫃中的應用越來越有信心。

預計到2031年,刀鋒伺服器將以7.84%的複合年成長率成長,並且在新部署中預計將超越機架式伺服器。思科的UCS XE9305底盤採用10U機殼,配備16個雙路節點,消除了機架頂部交換器的延遲,同時最大限度地提高了單位面積的運算能力。到2025年,機架式伺服器仍將佔據高頻交易伺服器市場63.47%的佔有率,這反映了它們在站點維修為低功耗環境方面的柔軟性。

水冷刀片底盤無需大規模維修即可維持 17 千瓦的機櫃,這在交換主機不斷提高密度限制的情況下是一項顯著優勢。 Supermicro 於 2026 年 3 月發布的 40 節點 MicroBlade 伺服器,將每個節點的面積減少了 50%,凸顯了占地面積面臨的經濟壓力。儘管維修限制將使機架式伺服器繼續保持其受歡迎程度,但刀鋒伺服器將日益成為新部署的標準配置。

區域分析

到2025年,北美將佔據高頻交易伺服器市場36.51%的佔有率,這主要得益於芝加哥商品交易所(CME)的Aurora伺服器、紐約證券交易所(NYSE)的Mahwah伺服器以及納斯達克(Nasdaq)的Carteret伺服器。 CME與Google雲端的合作將新增42.8萬平方英尺的架空地板空間,從而能夠部署適用於混合刀鋒伺服器和FPGA配置的17千瓦機櫃。 2026年1月,洲際交易所(ICE)的Mahwah伺服器將實現Tier 4級冗餘,擁有28兆瓦的電力供應能力和亞微秒級的時間協議精度,樹立了其他伺服器難以企及的標竿。

預計亞太地區2026年至2031年的複合年成長率將達到7.58%,成為成長最快的地區。計劃於2026年開幕的Equinix HK6將使香港成為連接中國當地交易所的跨境套利中心。日本交易所集團和韓國交易所已推出配備100Gigabit乙太網路介面的交易籠,以吸引本地自營交易公司。新加坡交易所繼續提供確定性交易,而印度國家證券交易所則引入隨機延遲機制,以抑制高頻獎勵。

歐洲、中東和非洲的趨勢各不相同。法蘭克福期貨交易所 (Eurex Frankfurt) 和阿姆斯特丹泛歐交易所 (Euronext Amsterdam) 的需求仍然強勁,其中法蘭克福期貨交易所每個機櫃每月收費 6,000 至 9,600 歐元(約 6,780 至 10,848 美元)。泛歐交易所於 2024 年 7 月建成的微波網路已將倫敦和貝加莫之間的延遲降低到 4 毫秒以下,這與利用光纖旁路進行伺服器部署的策略相符。中東主權財富基金正在為新興的數位資產交易所提供資金,而南美洲的採用仍處於早期階段,目前僅限於 B3 聖保羅的託管服務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 演算法交易和人工智慧主導的交易量激增。

- 對超低延遲基礎設施的需求

- 加密貨幣和數位資產交易所的擴張

- x86多核心與FPGA加速處理器的演進

- 用於微波和自由空間光鏈路的協同最佳化伺服器

- 新興金融中心的邊緣資料中心託管

- 市場限制因素

- 加強監管和阻礙成長的措施

- 託管機房和專用冷卻系統進行大量資本投入。

- NIC/FPGA組件的供應鏈限制

- 碳排放強度報告對超高密度空洞施加了限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 依處理器架構

- 基於 x86 的伺服器

- 基於 ARM 的伺服器

- 其他處理器架構

- 按外形規格

- 機架式伺服器

- 刀鋒伺服器

- 塔式伺服器

- 微型伺服器

- 透過使用

- 股票交易

- 外匯(Forex)

- 商品交易

- 衍生性商品和加密資產

- 最終用戶

- 自營交易公司和市場創造者

- 投資銀行和證券公司

- 避險基金和資產管理公司

- 股票和衍生性商品交易所

- 相關系統(CRM、財務、人力資源)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer, Inc.

- Lenovo Group Limited

- International Business Machines Corporation

- Cisco Systems, Inc.

- Fujitsu Limited

- NEC Corporation

- Inspur Group Co., Ltd.

- Gigabyte Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Quanta Computer Inc.

- Wistron Corporation

- MiTAC Holdings Corporation

- Penguin Computing, Inc.

- LDA Technologies Ltd.

- Silicom Ltd.

- XENON Pty Ltd.

- Broadberry Data Systems Limited

- Arista Networks, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the high frequency trading server market size was valued at USD 629.87 million in 2025 and estimated to grow from USD 670.12 million in 2026 to reach USD 900.55 million by 2031, at a CAGR of 6.09% during the forecast period (2026-2031).

This report is Segmented by Processor Architecture (x86-Based Servers, ARM-Based Servers, and More), Form Factor (Rack Servers, Blade Servers, and More), Application (Equity Trading, Foreign Exchange, and More), End-User (Proprietary Trading Firms and Market Makers, Investment Banks and Brokerage Houses, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global High Frequency Trading Server Market Trends and Insights

Surge in Algorithmic and AI-Driven Trading Volumes

Algorithmic execution accounts for more than 70% of equity order flow in developed venues, and reinforcement-learning agents are now being embedded directly into FPGA fabric to shave nanoseconds off tick-to-trade cycles. The European Securities and Markets Authority guidance issued in February 2026 requires microsecond-level pre-trade checks that favor on-premises compute over cloud endpoints. Quantitative funds managing more than USD 10 billion in assets deploy inference-capable servers next to exchange engines, converting microsecond gains into multi-million-dollar slippage savings. Memory-bandwidth demands widen, accelerating the adoption of ARM designs such as NVIDIA Grace that deliver 1 terabyte per second of coherent bandwidth. The result is a structural lift in unit shipments of heterogeneous servers across major colocation hubs.

Demand for Ultra-Low-Latency Infrastructure

Exchange proximity hosts are upgrading from 10-gigabit to 400-gigabit Ethernet, compressing round-trip times to sub-microsecond territory and setting new floor specifications for network interface cards. Kraken opened a London cage at Equinix LD5 in April 2026 that delivers sub-millisecond access to European venues, drawing crypto market makers that require deterministic flows. CME Aurora added 428,000 square feet of raised floor in partnership with Google Cloud, providing 17-kilowatt cabinets that accommodate dual-socket blade nodes and FPGA accelerators. Kernel-bypass stacks such as DPDK and RDMA are now mandatory features on trading NICs, further intertwining server design with network topology.

High CAPEX for Colocation and Specialized Cooling

Tier-1 exchange-adjacent cabinets range from USD 6,000 to USD 9,600 per month for 10-gigabit connectivity, and premium cages attract USD 15,000 monthly, pushing annual spend beyond USD 150,000 per rack after cross-connects. Liquid-cooling upgrades add USD 50,000-100,000 upfront, forcing mid-tier hedge funds to weigh latency gains against budget limits. Legacy halls lacking chilled-water loops cannot retrofit high-density blades, driving migrations to new builds and elongating payback periods. Some firms downshift to virtual private servers, trading 20 microseconds of latency for monthly bills under USD 2,000, fragmenting demand for cutting-edge hardware.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cryptocurrency and Digital-Asset Exchanges

- Evolution of x86 Multi-core and FPGA-accelerated Processors

- Rising Regulatory Scrutiny and Speed-Bump Initiatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ARM-based servers logged the fastest 8.43% CAGR forecast for 2026-2031 as firms prioritize energy efficiency and memory bandwidth. NVIDIA Grace CPUs with 72 Arm Neoverse V2 cores and 1 terabyte per second of bandwidth shipped in 2025, enabling real-time risk simulations that once demanded dual-socket x86 rigs. x86 systems still dominated with 74.32% of high frequency trading server market share in 2025, underpinned by decades of compiled trading logic optimized for Intel and AMD microcode.

The power-density edge for ARM is frequently 30-40%, a benefit that aligns with colocation operators chasing revenue per kilowatt. Recompilation hurdles and limited ARM-native FPGA tooling slow migration for smaller firms, yet partnerships such as Fujitsu-Arrcus-1Finity in March 2026 reveal growing confidence in ARM designs for next-generation cages.

Blade servers are projected to expand at 7.84% CAGR to 2031, eclipsing rack systems in new builds. Cisco's UCS XE9305 chassis hosts 16 dual-socket nodes in 10U, eliminating top-of-rack switch latency and maximizing compute per square foot. Rack servers maintained 63.47% share of the high-frequency trading server market in 2025, reflecting their flexibility in retrofitting sites with lower power envelopes.

Liquid-cooling-ready blade chassis sustain 17-kilowatt cabinets without disruptive retrofits, an advantage as exchange hosts lift density ceilings. Supermicro's March 2026 40-node MicroBlade reduced per-node footprint by 50%, underscoring the economic pressure on square footage. Retrofit constraints will preserve rack prevalence, but greenfield deployments increasingly default to blade.

Geography Analysis

North America anchored 36.51% of the high frequency trading server market in 2025, supported by CME Aurora, NYSE Mahwah, and Nasdaq Carteret. CME's partnership with Google Cloud delivered 428,000 square feet of additional raised floor, enabling 17-kilowatt cabinets that favor blade and FPGA hybrids. ICE Mahwah reached Tier 4 redundancy with 28 megawatts and sub-1 microsecond precision time protocol in January 2026, cementing a benchmark others emulate.

Asia-Pacific is projected to log a 7.58% CAGR over 2026-2031, the fastest regional climb. Equinix HK6, opening in 2026, positions Hong Kong as a cross-border arbitrage hub linking mainland exchanges. Japan Exchange Group and Korea Exchange rolled out 100-gigabit Ethernet cages, drawing regional proprietary firms. Singapore Exchange continues to offer deterministic access, yet India's National Stock Exchange introduced randomized delays that temper high-frequency incentives.

Europe, the Middle East, and Africa show divergent trends. Eurex Frankfurt and Euronext Amsterdam sustain steady demand, with Eurex charging EUR 6,000-9,600 (USD 6,780-10,848) per cabinet each month. Euronext's July 2024 microwave network lowered London-Bergamo latency below 4 milliseconds, aligning with server placements that exploit fiber bypass. Middle Eastern sovereign wealth funds fund nascent digital-asset exchanges, while South America remains in early adoption, limited to B3 Sao Paulo colocation offerings.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer, Inc.

- Lenovo Group Limited

- International Business Machines Corporation

- Cisco Systems, Inc.

- Fujitsu Limited

- NEC Corporation

- Inspur Group Co., Ltd.

- Gigabyte Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Quanta Computer Inc.

- Wistron Corporation

- MiTAC Holdings Corporation

- Penguin Computing, Inc.

- LDA Technologies Ltd.

- Silicom Ltd.

- XENON Pty Ltd.

- Broadberry Data Systems Limited

- Arista Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Algorithmic and AI-Driven Trading Volumes

- 4.2.2 Demand for Ultra-Low-Latency Infrastructure

- 4.2.3 Expansion of Cryptocurrency and Digital-Asset Exchanges

- 4.2.4 Evolution of x86 Multi-Core and FPGA-Accelerated Processors

- 4.2.5 Microwave and Free-Space Optical Links Co-Optimizing Servers

- 4.2.6 Edge Colocation in Emerging Financial Hubs

- 4.3 Market Restraints

- 4.3.1 Rising Regulatory Scrutiny and Speed-Bump Initiatives

- 4.3.2 High CAPEX for Colocation and Specialized Cooling

- 4.3.3 Supply-Chain Constraints for NIC / FPGA Components

- 4.3.4 Carbon-Intensity Reporting Limiting Ultra-Dense Halls

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processor Architecture

- 5.1.1 x86-based Servers

- 5.1.2 ARM-based Servers

- 5.1.3 Other Processor Architectures

- 5.2 By Form Factor

- 5.2.1 Rack Servers

- 5.2.2 Blade Servers

- 5.2.3 Tower Servers

- 5.2.4 Micro Servers

- 5.3 By Application

- 5.3.1 Equity Trading

- 5.3.2 Foreign Exchange (Forex)

- 5.3.3 Commodity Trading

- 5.3.4 Derivatives and Cryptoassets

- 5.4 By End-User

- 5.4.1 Proprietary Trading Firms and Market Makers

- 5.4.2 Investment Banks and Brokerage Houses

- 5.4.3 Hedge Funds and Asset Managers

- 5.4.4 Stock and Derivatives Exchanges

- 5.4.5 Ancillary Systems (CRM, Treasury, HR)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 Super Micro Computer, Inc.

- 6.4.4 Lenovo Group Limited

- 6.4.5 International Business Machines Corporation

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Fujitsu Limited

- 6.4.8 NEC Corporation

- 6.4.9 Inspur Group Co., Ltd.

- 6.4.10 Gigabyte Technology Co., Ltd.

- 6.4.11 ASUSTeK Computer Inc.

- 6.4.12 Quanta Computer Inc.

- 6.4.13 Wistron Corporation

- 6.4.14 MiTAC Holdings Corporation

- 6.4.15 Penguin Computing, Inc.

- 6.4.16 LDA Technologies Ltd.

- 6.4.17 Silicom Ltd.

- 6.4.18 XENON Pty Ltd.

- 6.4.19 Broadberry Data Systems Limited

- 6.4.20 Arista Networks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

高頻交易伺服器市場規模、佔有率和成長分析:按組件、部署類型、延遲類型、交易類型、最終用戶和地區分類-2026-2033年產業預測

高頻交易伺服器市場規模、佔有率和成長分析:按組件、部署類型、延遲類型、交易類型、最終用戶和地區分類-2026-2033年產業預測 2026年全球高頻交易(HFT)伺服器市場報告

2026年全球高頻交易(HFT)伺服器市場報告 高頻交易伺服器市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者、功能及解決方案分類

高頻交易伺服器市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者、功能及解決方案分類 高頻交易伺服器市場:產業趨勢及全球預測(至 2035 年)-按處理器類型、外形尺寸、應用領域、產業垂直領域、伺服器架構、公司規模和主要地區劃分2025年高頻交易全球市場報告

高頻交易伺服器市場:產業趨勢及全球預測(至 2035 年)-按處理器類型、外形尺寸、應用領域、產業垂直領域、伺服器架構、公司規模和主要地區劃分2025年高頻交易全球市場報告 全球高頻交易市場(按產品、執行策略、資產類別、部署方法和最終用戶):未來預測(2025-2030 年)

全球高頻交易市場(按產品、執行策略、資產類別、部署方法和最終用戶):未來預測(2025-2030 年) 高頻交易伺服器市場規模、佔有率、趨勢分析報告:按處理器、按外形規格、按應用、按地區、細分市場預測,2025-2030 年高頻交易市場規模、佔有率、趨勢分析報告:按產品、按部署、按最終用途、按地區、細分市場預測,2025-2030 年

高頻交易伺服器市場規模、佔有率、趨勢分析報告:按處理器、按外形規格、按應用、按地區、細分市場預測,2025-2030 年高頻交易市場規模、佔有率、趨勢分析報告:按產品、按部署、按最終用途、按地區、細分市場預測,2025-2030 年 高頻率交易伺服器的印度市場評估:各部署類型,處理器,各硬體設備類型,資產類別,各最終用途產業,各地區,機會,預測(2018年度~2032年度)高頻交易伺服器美國市場評估:依部署方法、依處理器、依硬體類型、依資產類別、依最終用途行業、依地區、機會、預測(2017-2031年)

高頻率交易伺服器的印度市場評估:各部署類型,處理器,各硬體設備類型,資產類別,各最終用途產業,各地區,機會,預測(2018年度~2032年度)高頻交易伺服器美國市場評估:依部署方法、依處理器、依硬體類型、依資產類別、依最終用途行業、依地區、機會、預測(2017-2031年)