|

市場調查報告書

商品編碼

2062453

金屬空氣電池:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Metal-Air Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

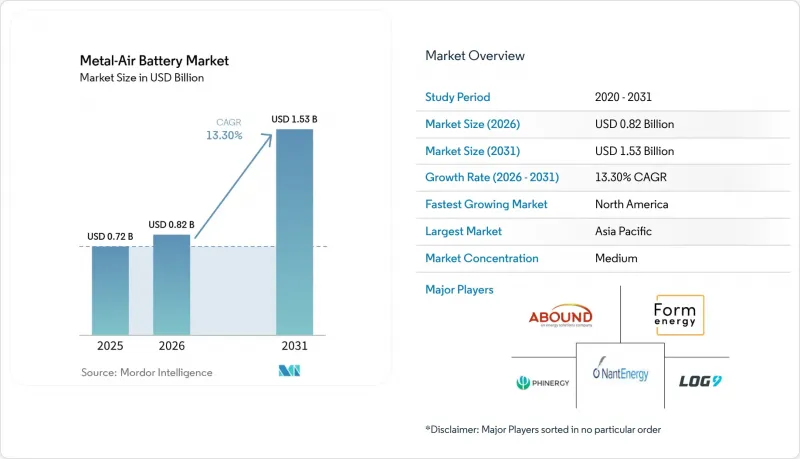

根據 Mordor Intelligence 預測,金屬空氣電池市場將從 2026 年的 8.2 億美元成長到 2031 年的 15.3 億美元,2026 年至 2031 年的複合年成長率為 13.3%。

本報告按金屬類型(鋅空氣電池、鋁空氣電池、鋰空氣電池、鐵空氣電池及其他金屬電池)、電池類型(一次電池、二次電池)、電壓(低壓、中壓、高壓)、應用領域(電動車、固定式儲能、軍工電子產品、消費性電子產品、醫療用電子設備及其他應用領域)和地區進行細分。市場預測以美元計價。

全球金屬空氣電池市場趨勢與洞察

可充電鋅空氣電池和鋰空氣電池化學技術的進步

2025年和2026年報告的突破性雙功能催化劑將鋅空氣電池的循環壽命延長至10000小時以上,並降低了充放電電壓差。這些改進減輕了溫度控管負擔,並為成本可與固定式儲能鋰離子電池相媲美的二次鋅空氣電池組鋪平了道路。研究團隊也致力於研發具有保護性鋰負極的固體電解質,為鋰空氣電池的商業化提供了清晰的路徑。這些進展共同增強了電力公司和資料中心營運商對多日放電解決方案能夠滿足保固要求的信心,從而促進了採購訂單的成長。

電動車的快速普及對超高能量密度電池組提出了更高的要求。

預計到2024年,全球電動車銷量將超過1,400萬輛,並持續成長。汽車製造商正在探索化學技術,力求在不增加電池組重量的情況下,實現單次充電500公里的續航里程。金屬空氣電池的理論比能量有望比鋰離子電池高出三到五倍。 Phinergy、Hindalco和Indian Oil簽署的合作備忘錄旨在研發一種鋁空氣電池組,其鋁板可在數分鐘內更換,從而徹底改變電力供應物流。增程器模組正在中國和印度的試點車隊中進行測試,而旨在實現零排放的監管獎勵正在加速商業平台的實用化。

與成熟的鋰離子電池相比,循環壽命有限

雖然實驗室中鐵空氣電池系統已記錄到長達 1696 小時的運作時間,而可充電鋅空氣電池在最佳情況下也能超過 10000 小時,但兩者都遠不及鋰離子電池標準的 3000-5000 次循環壽命。因此,鋰離子電池在涉及日常循環的應用領域,例如頻率調節和乘用車,仍然佔據主導地位。 Form Energy 將鐵空氣電池定位為適用於每週或每月放電 100 小時的應用,從而避免了最嚴苛的運作條件。持續改進電解二氧化碳生成抑制和枝晶控制仍然是其更廣泛應用的先決條件。

細分市場分析

預計到2025年,鋅空氣電池將維持金屬空氣電池市場55.47%的佔有率。這主要是由於其在助聽器和醫療用電子設備中的持續應用,在這些應用中,可靠的性能作為一次電池至關重要。鐵空氣電池領域,在Form Energy眾多在建工程的推動下,預計將佔據更大的金屬空氣電池市場。受各種應用領域日益成長的需求驅動,預計該領域在2026年至2031年的預測期內將以13.86%的最高複合年成長率成長。

併網系統和資料中心備用電源運作中對多日放電合約的需求日益成長,凸顯了鐵空氣電池的經濟可行性。這類電池尤其適用於那些可以接受循環壽命和往返效率之間權衡,以換取更低每千瓦時成本的應用場景。同時,鋁空氣電池開發商正利用豐富的鋁原料和金屬極板的快速更換特性。這種方法解決了許多重要問題,尤其是在商用車營運中,例如續航里程限制和因加油造成的停機時間。另一方面,儘管鋰空氣電池技術在固態電池原型開發方面取得了進展,但由於該技術仍處於早期階段,且商業化仍面臨諸多挑戰,預計在目前的預測期內不會廣泛應用。

截至2025年,一次電池佔金屬空氣電池市場的60.19%。這主要得益於其在助聽器等醫療設備和家用電子電器等領域的成熟應用。由於其可靠性和成本效益,這些電池在需要穩定性能的應用中繼續佔據市場主導地位。同時,雙功能催化劑的進步顯著延長了二次鋅空氣電池的使用壽命,使其能夠運作約10,000小時。這項進展為固定式能源儲存系統和行動應用開闢了新的應用機遇,預計在預測期內,可充電鋅空氣電池的複合年成長率將達到13.92%。

金霸王(Duracell)、Panasonic)和GP Batteries等老牌企業憑藉其廣泛的分銷網路和品牌知名度,在紐扣電池領域保持著強勁的地位。然而,像EnZinc和Zinc8這樣的新興企業正在穩步推進模組化鋅空氣電池組的規模化生產,以應用於區域微電網和商業建築等領域。隨著美國和歐洲等地區鋅空氣電池的年產能提升至吉瓦時級別,金屬空氣電池市場向二次電池配置的轉型預計將加速,從而進一步推動該領域的創新和應用。

區域分析

預計到2025年,亞太地區將佔據金屬空氣電池市場53.79%的佔有率。這主要得益於中國強大的製造能力、印度在鋁空氣電池領域的戰略合作以及日本在催化劑科學方面的進步。中國正透過寧德時代(CATL)的「Choco-Swap」生態系統推動電池更換基礎建設。該計畫於2024年12月啟動,計畫在2025年部署1,000座換電站,中期目標為1萬座,旨在為適用於鋁空氣電池和鋅空氣電池的金屬漿料供電系統打造典範。亞太地區受益於促進本地供應鏈發展的政策以及雄心勃勃的交通運輸電氣化目標,為市場成長創造了有利環境。此外,主要廠商的佈局和持續的研發投入也進一步鞏固了亞太市場的領先地位。

預計2026年至2031年間,北美將以14.08%的複合年成長率(CAGR)領先全球。這一成長得益於各州對長期儲能的強制性政策、能源部的資助舉措以及Form Energy在西維吉尼亞建立的生產基地。這些因素共同推動了北美本土生態系統的蓬勃發展,涵蓋了從基礎研究到大規模部署的各個環節。此外,加拿大透過ELYSIS計畫致力於低碳鋁生產,提升了該地區原料的永續性,並進一步促進了市場擴張。

歐洲持續致力於在「地平線歐洲」計畫下促進產學研合作,並撥款1,500萬歐元(約1,620萬美元)用於鋅空氣電池的商業化。德國和英國等國的電網營運商正擴大將多日儲能解決方案納入其容量競標中。這項策略重點旨在因應未來需求的顯著成長,前提是關鍵示範里程碑的實現。該地區對創新和監管支援的重視,持續推動金屬空氣電池技術的進步。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 可充電鋅鋰空氣電池技術的進步

- 電動車的快速普及需要超高能量密度的電池組。

- 鋅鋁價格下跌以及鋰鈷價格走勢

- 政府為長期儲能試點計畫提供資金

- 適用於商用電動車隊的可更換金屬漿液加註站

- 為提升國防部門中靜音輕型士兵的能力所做的努力

- 市場限制因素

- 與成熟的鋰離子電池技術相比,循環壽命較短。

- 空氣陰極中的二氧化碳中毒和催化劑劣化

- 不成熟的大規模製造供應鏈

- 對脫碳、高純度鋁原料的競爭

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按金屬類型

- 鋅空氣

- 鋁 - 空氣

- 鋰空氣

- 鐵 - 空氣

- 其他金屬類型

- 依電池類型

- 一次電池(不可充電)

- 備用電池(可充電)

- 透過電壓

- 低電壓(低於12伏特)

- 中壓(12-36伏特)

- 高電壓(超過 36 伏特)

- 透過使用

- 電動車

- 固定式儲能

- 軍用/國防電子設備

- 消費性電子設備和醫療用電子設備

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Arotech Corporation

- Duracell Inc.

- E-Stone Batteries BV

- Electric Fuel Battery Corporation

- EnZinc Inc.

- e-Zinc Corporation

- Fuji Pigment Co., Ltd.

- GP Batteries International Limited

- Log9 Materials Scientific Private Limited

- Maxell Holdings, Ltd.

- NantEnergy Inc.

- Panasonic Holdings Corporation

- Phinergy Ltd.

- PolyPlus Battery Company

- Renata SA

- Sunergy Battery Co., Ltd.

- ZAF Energy Systems Inc.

- Zhuhai Zhi Li Battery Co., Ltd.(ZeniPower)

- Zinc8 Energy Solutions Inc.

- Form Energy, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the metal-air battery market size is expected to increase from USD 0.82 billion in 2026 to USD 1.53 billion by 2031, growing at a CAGR of 13.3% over 2026-2031.

This report is Segmented by Metal Type (Zinc-Air, Aluminum-Air, Lithium-Air, Iron-Air, and Other Metal Type), Battery Type (Primary, and Secondary), Voltage (Low, Medium, and High), Application (Electric Vehicles, Stationary Energy Storage, Military and Defence Electronics, Consumer and Medical Electronics, and Other Application), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Metal-Air Battery Market Trends and Insights

Advances in Rechargeable Zinc-Air and Lithium-Air Chemistries

Breakthrough bifunctional catalysts reported during 2025 and 2026 increased zinc-air cycle life above 10,000 hours and narrowed the voltage gap between charge and discharge. These improvements reduce thermal management loads and pave the way for secondary zinc-air packs that can rival lithium-ion on total cost in stationary storage. Research groups are also converging on solid-state electrolytes with protected lithium anodes, placing lithium-air on a credible path toward commercialization. The combined progress strengthens confidence among utilities and data-center operators that multi-day discharge solutions can meet warranty requirements, stimulating procurement pipelines.

Rapid Electric-Vehicle Adoption Requiring Ultra-High Energy Density Packs

Global electric-vehicle sales surpassed 14 million units in 2024 and continue to climb. Automakers seek chemistries delivering 500 km per charge without heavier packs. Metal-air batteries promise three-to-five-fold higher theoretical specific energy compared with lithium-ion. Memoranda of understanding between Phinergy, Hindalco, and Indian Oil target aluminum-air packs that swap aluminum plates in minutes, reshaping refueling logistics. Pilot fleets in China and India are testing range-extender modules, and regulatory incentives for zero-tailpipe emissions accelerate the timeline for commercial platforms.

Limited Cycle Life Compared with Mature Lithium-Ion Chemistries

Laboratory iron-air systems have logged up to 1,696 hours, and rechargeable zinc-air cells now exceed 10,000 hours in the best cases, yet both remain below lithium-ion norms of 3,000-5,000 cycles. Daily-cycling applications, such as frequency regulation or passenger vehicles, therefore still default to lithium-ion. Form Energy positions iron-air for 100-hour discharge at weekly or monthly cycling intervals, sidestepping the heaviest duty profiles. Continued advances in electrolyte carbonation suppression and dendrite control remain prerequisites for broader deployment.

Other drivers and restraints analyzed in the detailed report include:

- Declining Zinc and Aluminum Prices Versus Lithium and Cobalt

- Government Funding for Long-Duration Storage Pilots

- Air-Cathode Carbon Dioxide Poisoning and Catalyst Degradation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc-air batteries are projected to retain a 55.47% share of the metal-air battery market in 2025, primarily due to their continued use in hearing aids and medical electronics, which rely on these batteries for their dependable performance as primary cells. The iron-air segment, supported by Form Energy's extensive multiproject pipeline, is expected to gain a larger share of the metal-air battery market. This segment is expected to register the highest compound annual growth rate (CAGR) of 13.86% during the forecast period of 2026-2031, driven by increasing adoption in various applications.

The growing number of multi-day discharge contracts in grid balancing and data center backup operations underscores the economic viability of iron-air batteries. These batteries are particularly suited for applications where trade-offs between cycle life and round-trip efficiency are acceptable in exchange for a lower cost per stored kilowatt-hour. Concurrently, aluminum-air battery developers are capitalizing on the abundance of aluminum feedstock and the ability to quickly swap metal plates. This approach addresses critical concerns such as range anxiety and refueling downtime, especially in commercial fleet operations. On the other hand, while lithium-air battery technology has shown progress in solid-state prototype development, its mainstream adoption remains outside the current forecast window due to its early-stage nature and ongoing challenges in commercialization.

Primary cells accounted for 60.19% of the metal-air battery market in 2025, driven by their established use in healthcare devices, such as hearing aids, and consumer electronics. These cells continue to dominate due to their reliability and cost-effectiveness in applications requiring consistent performance. Meanwhile, advancements in bifunctional catalysts have significantly extended the lifespan of secondary zinc-air batteries, enabling them to operate for nearly 10,000 hours. This development has opened up new opportunities for their use in stationary energy storage systems and mobility applications, contributing to a projected 13.92% compound annual growth rate (CAGR) for rechargeable zinc-air batteries during the forecast period.

Established players like Duracell, Panasonic, and GP Batteries maintain their stronghold in the button-cell segment, leveraging their extensive distribution networks and brand recognition. However, emerging companies such as EnZinc and Zinc8 are making strides toward scaling modular zinc-air battery packs for applications including community microgrids and commercial buildings. The shift in the metal-air battery market toward secondary configurations is expected to accelerate as manufacturing capacities in regions like the United States and Europe expand to gigawatt-hour annual output levels, further driving innovation and adoption in this segment.

Geography Analysis

Asia-Pacific accounted for 53.79% of the 2025 metal-air battery market, driven by China's extensive manufacturing capabilities, India's strategic aluminum-air collaborations, and Japan's advancements in catalyst science. China is advancing battery-swapping infrastructure through CATL's Choco-Swap ecosystem, which launched in December 2024 with plans to reach 1,000 stations by 2025 and a mid-term target of 10,000 stations, creating a template for metal-slurry refueling systems applicable to aluminum-air and zinc-air batteries. The region benefits from policies that promote local supply chain development and ambitious transportation electrification goals, creating a conducive environment for market growth. Additionally, the presence of key players and ongoing investments in research and development further solidify Asia-Pacific's dominance in the market.

North America is projected to exhibit the highest 14.08% forecast CAGR for 2026-2031. This growth is supported by state-level mandates for long-duration energy storage, funding initiatives from the Department of Energy, and the establishment of Form Energy's manufacturing facility in West Virginia. These factors contribute to a robust domestic ecosystem that spans from foundational research to large-scale field deployment. Furthermore, Canada's focus on low-carbon aluminum production through the ELYSIS venture enhances the region's feedstock sustainability, providing additional support for market expansion.

Europe remains committed to fostering academic-industry collaborations under the Horizon Europe program, allocating EUR 15 million (approximately USD 16.2 million) toward the commercialization of zinc-air batteries. National grid operators in countries like Germany and the United Kingdom are increasingly incorporating multi-day storage solutions into capacity auctions. This strategic focus positions Europe for a significant surge in demand in the future, contingent on achieving key demonstration milestones. The region's emphasis on innovation and regulatory support continues to drive advancements in metal-air battery technologies.

- Arotech Corporation

- Duracell Inc.

- E-Stone Batteries B.V.

- Electric Fuel Battery Corporation

- EnZinc Inc.

- e-Zinc Corporation

- Fuji Pigment Co., Ltd.

- GP Batteries International Limited

- Log9 Materials Scientific Private Limited

- Maxell Holdings, Ltd.

- NantEnergy Inc.

- Panasonic Holdings Corporation

- Phinergy Ltd.

- PolyPlus Battery Company

- Renata SA

- Sunergy Battery Co., Ltd.

- ZAF Energy Systems Inc.

- Zhuhai Zhi Li Battery Co., Ltd. (ZeniPower)

- Zinc8 Energy Solutions Inc.

- Form Energy, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in Rechargeable Zinc- and Lithium-Air Chemistries

- 4.2.2 Rapid EV Adoption Requiring Ultra-High Energy Density Packs

- 4.2.3 Declining Zinc and Aluminum Prices Versus Lithium and Cobalt

- 4.2.4 Government Funding for Long-Duration Storage Pilots

- 4.2.5 Swappable Metal-Slurry Refuel Stations for Commercial EV Fleets

- 4.2.6 National Defense Push for Silent, Lightweight Soldier Power

- 4.3 Market Restraints

- 4.3.1 Limited Cycle Life Compared with Mature Li-ion Chemistries

- 4.3.2 Air-Cathode CO2 Poisoning and Catalyst Degradation

- 4.3.3 Immature Large-Scale Manufacturing Supply Chain

- 4.3.4 Competition for Decarbonised High-Purity Aluminium Feedstock

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Metal Type

- 5.1.1 Zinc-air

- 5.1.2 Aluminum-air

- 5.1.3 Lithium-air

- 5.1.4 Iron-air

- 5.1.5 Other Metal Type

- 5.2 By Battery Type

- 5.2.1 Primary (Non-rechargeable)

- 5.2.2 Secondary (Rechargeable)

- 5.3 By Voltage

- 5.3.1 Low (less than 12 V)

- 5.3.2 Medium (12-36 V)

- 5.3.3 High (greater than 36 V)

- 5.4 By Application

- 5.4.1 Electric Vehicles

- 5.4.2 Stationary Energy Storage

- 5.4.3 Military and Defence Electronics

- 5.4.4 Consumer and Medical Electronics

- 5.4.5 Other Application

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arotech Corporation

- 6.4.2 Duracell Inc.

- 6.4.3 E-Stone Batteries B.V.

- 6.4.4 Electric Fuel Battery Corporation

- 6.4.5 EnZinc Inc.

- 6.4.6 e-Zinc Corporation

- 6.4.7 Fuji Pigment Co., Ltd.

- 6.4.8 GP Batteries International Limited

- 6.4.9 Log9 Materials Scientific Private Limited

- 6.4.10 Maxell Holdings, Ltd.

- 6.4.11 NantEnergy Inc.

- 6.4.12 Panasonic Holdings Corporation

- 6.4.13 Phinergy Ltd.

- 6.4.14 PolyPlus Battery Company

- 6.4.15 Renata SA

- 6.4.16 Sunergy Battery Co., Ltd.

- 6.4.17 ZAF Energy Systems Inc.

- 6.4.18 Zhuhai Zhi Li Battery Co., Ltd. (ZeniPower)

- 6.4.19 Zinc8 Energy Solutions Inc.

- 6.4.20 Form Energy, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

鋁空氣電池市場:按組件、類型、應用、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

鋁空氣電池市場:按組件、類型、應用、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 IronAir電池市場預測—按系統類型、電池組件、應用、最終用戶和地區分類的全球分析—2034年金屬空氣電池市場預測—按金屬類型、電池組件、應用、最終用戶和地區分類的全球分析—2034年金屬空氣電池市場:依金屬類型、電池類型、應用、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

IronAir電池市場預測—按系統類型、電池組件、應用、最終用戶和地區分類的全球分析—2034年金屬空氣電池市場預測—按金屬類型、電池組件、應用、最終用戶和地區分類的全球分析—2034年金屬空氣電池市場:依金屬類型、電池類型、應用、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 金屬空氣電池市場:2026-2032年全球市場預測(依活性金屬、電池類型、應用、終端用戶產業及通路分類)

金屬空氣電池市場:2026-2032年全球市場預測(依活性金屬、電池類型、應用、終端用戶產業及通路分類) 全球鐵空氣電池市場:市場規模、佔有率和趨勢分析(按類型、應用和地區分類),細分市場預測(2026-2033 年)

全球鐵空氣電池市場:市場規模、佔有率和趨勢分析(按類型、應用和地區分類),細分市場預測(2026-2033 年) 全球金屬空氣電池市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球鋰空氣電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球金屬空氣電池市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球鋰空氣電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 鋰空氣電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

鋰空氣電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 金屬空氣電池市場規模、佔有率和成長分析(按金屬、電壓、類型、應用和地區分類)-2026-2033年產業預測

金屬空氣電池市場規模、佔有率和成長分析(按金屬、電壓、類型、應用和地區分類)-2026-2033年產業預測