|

市場調查報告書

商品編碼

2062451

無線接取網分析與監測:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)RAN Analytics And Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

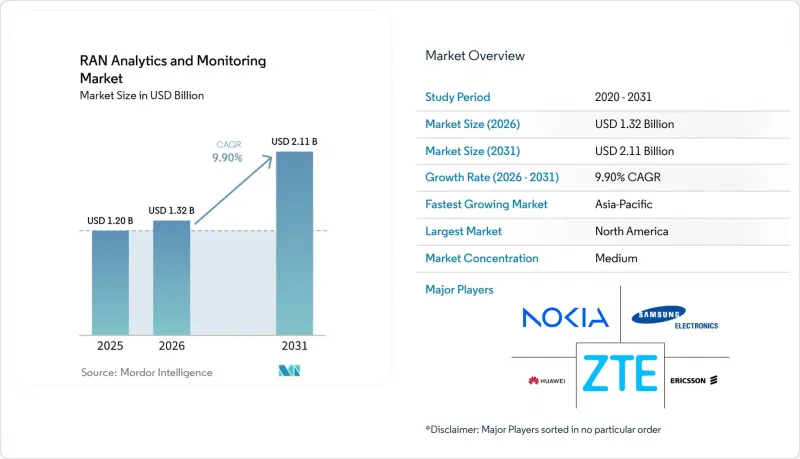

根據 Mordor Intelligence 預測,無線存取網 (RAN) 分析和監控市場規模將從 2025 年的 12 億美元和 2026 年的 13.2 億美元成長到 2031 年的 21.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.9%。

本報告按元件(平台/軟體、服務)、部署模式(本地部署、雲端部署)、網路技術(4G/LTE 及其他)、應用程式(效能管理、故障和事件管理及其他)、最終用戶(一級行動網路營運商、行動虛擬網路營運商及其他)和地區進行細分。市場預測以美元計價。

全球無線接取網路(RAN)分析與監測市場趨勢及洞察

利用人工智慧驅動的預測性維護來提高5G密度

隨著通訊業者為滿足中等頻寬容量需求而增設數千個小型基地台,預測性維護變得至關重要。這種轉變透過在服務品質下降之前自動偵測干擾、休眠基地台或波束劣化等問題,減少了人工維護時間。華為和中國移動的40萬個基地台專案等部署案例表明,運營商級自主代理系統擴充性。目前,供應商正競相提供無需高階資料科學技能即可啟動的預訓練模型和封閉回路型工作流程,從而加快價值實現速度。在越來越多的商業成功案例中,預算正從傳統的關鍵績效指標 (KPI) 儀錶板轉向自動化修復平台。總體而言,2026 年以後簽署的大部分新契約將基於能夠預測和預防故障的軟體。

雲端原生 RAN 解耦加速資料視覺化。

透過將無線存取網路 (RAN) 分類為集中式、分散式和無線單元,可以獲得更多遙測點,從而實現即時雲端原生分析。諾基亞的自主網路架構 (Autonomous Network Fabric) 和 Infovista 的無人值守現場驗證等解決方案,能夠以每秒Gigabit向可擴展的 API 優先後端提供資料流。通訊業者可以跨多個供應商獲得精細化的可見性,減少供應商鎖定,並在無需進行大規模系統升級的情況下推出新的分析功能。這種架構彈性帶來的代價是,在舊有系統逐步淘汰之前,必須先執行雙重保障協定堆疊。但大多數一級業者認為,柔軟性和速度帶來的優勢遠大於過渡過程中的複雜性。

多廠商無線接取網路中資料標準的碎片化

異質日誌格式阻礙了統一模型的訓練,並迫使通訊業者維護自訂解析器,從而推高了整合成本。 NETSCOUT 2024 年 AIOps 調查指出,不一致的模式是機器學習普及的最大障礙,其影響甚至超過了運算資源稀缺和授權費用。正在試行多廠商開放式無線接取網路 (Open RAN) 的印度通訊業者指出,依賴第三方系統整合商進行資料標準化會顯著增加成本,通常會使專案週期延長一倍。儘管 O-RAN 聯盟倡導通用資訊模型,但廠商為了保持競爭優勢,仍在不斷發佈各自的計數器,這進一步延長了規範化工作。

細分市場分析

儘管平台軟體在2025年仍佔據了大部分收入,但隨著多廠商環境日益複雜,服務業務的成長速度正在加快。通訊業者意識到,持續的模型重訓練和跨域關聯分析超出了傳統網路營運中心的能力範圍,因此他們開始以基於結果的合約方式採購部署、客製化和生命週期管理服務。因此,由託管服務驅動的無線接取網(RAN)分析和監控市場正以兩位數的速度成長,而供應商則透過預先建置的使用案例庫和服務等級保證來凸顯自身優勢。

此外,服務的成長也反映出人工智慧工程和開放式無線存取網編配的人才短缺。Capgemini SA和HCL科技等系統整合商正在建立全天候卓越中心,供應商則將持續升級納入訂閱模式,將資本投資轉化為可預測的營運成本。由於大多數二級營運商和企業專用網路所有者缺乏專業團隊,即使大型通訊業者繼續投資於自身的軟體堆棧,服務主導的交付模式也可能在2031年之前保持主導地位。

由於其可擴展性、基於成長的收費模式以及與超大規模人工智慧工具鏈的原生整合,雲端部署已佔據了絕大多數應用。相較於固定的本地叢集,橫向自動擴展能夠更好地處理來自數萬個基地台的串流遙測資料。因此,當資料量因流量高峰、韌體升級或新增頻段而增加時,雲端平台通常能夠提供最低的總體擁有成本 (TCO)。

對於延遲敏感型和主權受限的工作負載,本地部署和混合模式仍然很受歡迎。例如,歐洲通訊業者為了遵守《一般資料保護規則》(GDPR),會在私有雲端中處理包含大量個人資料的分析,同時將匿名化的訓練集匯出到公共雲端,以實現經濟高效的模型迭代。在整個預測期內,無線接取網路 (RAN) 分析和監控市場將繼續向「雲端優先」模式轉變,但能夠將邊緣、私有和公有資源整合到單一策略框架下的供應商將獲得最廣泛的應用。

區域分析

北美地區佔據了最大的支出佔有率,這主要得益於Verizon、AT&T和T-Mobile等公司積極部署中波頻段,以及向開放式無線接入網(RAN)測試平台的廣泛轉變。對多廠商RAN智慧控制器的早期測試增強了人們對基於標準的遙測技術的信心,並使廠商獨立監控套件的預算編製成為可能。此外,基地台密度的增加也帶動了鐵塔公司的資本投資,從而鞏固了通訊業者和基礎設施所有者對分析技術的需求。

在歐洲,監管機構對開放介面的支持,加上嚴格的能源效率指令,正在推動對功率分析模組和網路安全增強型解耦架構的投資。德國電信和沃達豐等通訊業者正在建立內部數位雙胞胎,用於供應商評估和符合NIS2要求,從而確保跨供應商關聯引擎的穩定供應。德國在汽車製造業採用專用網路方面處於領先地位,而英國和法國則優先考慮碳排放追蹤儀錶板,以實現國家永續性目標。

隨著印度待開發區5G網路、中國部署自主代理以及東南亞開展虛擬化無線接入網試點計畫同步推進,亞太地區正以最高的複合年成長率成長。例如,中國移動部署40萬個站點的智慧代理,展現了營運商級人工智慧營運能力,並鼓勵其他區域夥伴採用類似框架。日本在軟體定義無線接取網路(SDR RAN)的努力以及澳洲在遍遠地區發展通訊網路的重點,進一步豐富了這一高度多元化的格局。然而,所有子區域正在形成一種通用的策略,即強調雲端可擴展性、能源效率和開放介面的柔軟性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧驅動的5G網路擁塞預測性維護

- 雲端原生 RAN 解耦加速資料視覺化。

- 工業4.0工廠中專用5G網路激增

- 自動化開放式無線接取網路/擴充xApps-rApps生態系統

- 能源效率法規正在推動無線接取網功耗分析。

- 通訊業者為實現零接觸營運 (ZTO) 所做的努力

- 市場限制因素

- 多廠商無線接取網路中資料標準的碎片化

- 通訊服務供應商在人工智慧/機器學習模型工程方面的技能差距

- 擴大虛擬化無線接取網路中的網路攻擊面

- 現有4G網路現代化改造的投資報酬率不確定性

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 平台/軟體

- 服務

- 部署模式

- 現場

- 基於雲端的

- 網路科技

- 2G/3G

- 4G/LTE

- 5G NR

- Open RAN/vRAN

- 透過使用

- 績效管理

- 事件和事故管理

- 最佳化行動性和交接

- 能源和容量最佳化

- 最終用戶

- 一級行動網路營運商

- 行動虛擬網路營運商

- 企業專用網路

- 中立主機/塔樓公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Samsung Electronics Co., Ltd.(Network Business)

- NEC Corporation

- Mavenir Systems, Inc.

- Viavi Solutions Inc.

- MYCOM OSI Limited

- Infovista SAS

- TEOCO Corporation

- EXFO Inc.

- NETSCOUT Systems, Inc.

- Cellwize Wireless Technologies Pte Ltd.

- AirHop Communications, Inc.

- Parallel Wireless, Inc.

- Tupl, Inc.

- Rakuten Symphony Inc.

- Capgemini SE(Engineering and RAN Analytics)

- HCL Technologies Limited

- Amdocs Limited

- VMware, Inc.(Service Management and Analytics)

第7章 市場機會與未來展望

According to Mordor Intelligence, the rAN analytics and monitoring market size is projected to expand from USD 1.20 billion in 2025 and USD 1.32 billion in 2026 to USD 2.11 billion by 2031, registering a CAGR of 9.9% between 2026 to 2031.

This report is Segmented by Component (Platform/Software, and Services), Deployment Mode (On-Premises, and Cloud-Based), Network Technology (4G/LTE, and More), Application (Performance Management, Fault and Event Management, and More), End User (Tier-1 Mobile Network Operators, Mobile Virtual Network Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global RAN Analytics And Monitoring Market Trends and Insights

AI-Driven Predictive Maintenance For 5G Densification

Predictive maintenance is becoming essential as operators add thousands of small cells to satisfy mid-band capacity requirements. The shift cuts manual engineering hours by automatically detecting interference, sleeping cells, or degraded beams before service quality dips. Deployments such as Huawei and China Mobile's 400,000-site project have proven the scalability of autonomous agents at carrier-grade. Vendors now compete on providing pre-trained models and closed-loop workflows that can be activated without deep data-science skills, shortening time to value. Commercial success stories are accelerating budget reallocation from legacy key performance indicator dashboards to automated remediation platforms. The prevailing expectation is that software able to predict and prevent outages will underpin most new contracts signed after 2026.

Cloud-Native RAN Disaggregation Accelerates Data Visibility

Breaking the RAN into centralized, distributed, and radio units opens additional telemetry points that cloud-native analytics harness in real time. Solutions such as Nokia's Autonomous Network Fabric and Infovista's driverless field validation stream gigabit-per-second data streams into elastic, API-first backends. Operators gain fine-grained visibility across multiple vendors, reduce lock-in, and can spin up new analytic functions without forklift upgrades. This architectural freedom is offset by the need to run dual assurance stacks while legacy systems are retired, yet most tier-1 carriers judge the benefits of flexibility and speed to outweigh transitional complexity.

Fragmented data standards across multi-vendor RAN

Heterogeneous log formats impede the training of unified models, forcing operators to maintain custom parsers that raise integration costs. NETSCOUT's 2024 AIOps survey lists inconsistent schemas as the top inhibitor of machine-learning rollouts, ahead of compute shortages and licensing fees. Indian carriers piloting multi-vendor Open RAN cite the need for third-party system integrators to normalize data as a major expense spike, often doubling project timelines. The O-RAN Alliance promotes common information models, but equipment makers still release proprietary counters for competitive edge, prolonging normalization efforts.

Other drivers and restraints analyzed in the detailed report include:

- Surge Of Private 5G Networks In Industry 4.0 Plants

- Open RAN Automation And xApps-rApps Ecosystem Expansion

- Skills gap in AI/ML model engineering for CSPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software accounted for the bulk of 2025 revenue, yet rising multi-vendor complexity means services are climbing faster. Operators recognize that continuous model retraining and cross-domain correlation exceed routine network operations center competencies, so they purchase deployment, customization, and lifecycle management as outcome-based engagements. The RAN analytics and monitoring market size attributed to managed services is therefore expanding at a double-digit pace, while suppliers differentiate through libraries of pre-built use cases and service-level guarantees.

Services growth also reflects skills shortages in AI engineering and open-RAN orchestration. System integrators such as Capgemini and HCL Technologies are building 24/7 centers of excellence, and vendors bundle evergreen upgrades into subscriptions that convert capital outlays into predictable operating expenses. Because most tier-2 carriers and enterprise private-network owners lack specialist teams, service-led delivery will remain the preferred model through 2031, even as larger operators keep investing in proprietary software stacks.

Cloud-based implementations already hold a majority of deployments thanks to elasticity, pay-as-you-grow economics, and native integration with hyperscale AI toolchains. Streaming telemetry from tens of thousands of cell sites is better handled by horizontal auto-scaling than by fixed on-premises clusters. As a result, cloud platforms frequently demonstrate the lowest total cost of ownership when traffic spikes, firmware upgrades, or new spectrum bands multiply data volumes.

On-premises and hybrid models persist for latency-sensitive or sovereignty-constrained workloads. European carriers, for example, process personal-data-heavy analytics in private clouds to comply with the General Data Protection Regulation, while exporting non-identifiable training sets to public clouds for cheaper model iteration. Over the forecast horizon, the RAN analytics and monitoring market will continue shifting toward a cloud-first stance, but vendors able to unify edge, private, and public resources under a single policy framework will enjoy the widest adoption.

Geography Analysis

North America drives the largest share of spending thanks to aggressive mid-band spectrum roll-outs by Verizon, AT&T, and T-Mobile, and a pervasive move toward open RAN test beds. Early trials of multi-vendor RAN intelligent controllers have boosted confidence in standards-based telemetry, unlocking budgets for vendor-agnostic monitoring suites. Densification has also spilled into tower-company capital expenditure, cementing analytics demand across both carriers and infrastructure owners.

Europe combines regulatory support for open interfaces with stringent energy-efficiency directives, channeling investment into power analytics modules and cyber-secure, disaggregated architectures. Operators such as Deutsche Telekom and Vodafone are building internal digital twins to benchmark suppliers and comply with NIS2 requirements, ensuring steady procurement of cross-vendor correlation engines. Germany leads private-network uptake in automotive manufacturing, while the United Kingdom and France prioritize carbon-tracking dashboards to meet national sustainability targets.

Asia-Pacific posts the fastest CAGR as India's greenfield 5G, China's autonomous-agent deployments, and Southeast Asia's virtualized RAN pilots scale concurrently. Projects such as China Mobile's 400,000-site intelligent-agent deployment validate carrier-grade AI operations, encouraging regional peers to adopt similar frameworks. Japan's push into software-defined RAN and Australia's focus on rural coverage round out a highly diverse patchwork, yet all sub-regions converge on a playbook that values cloud elasticity, energy savings, and open-interface flexibility.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Samsung Electronics Co., Ltd. (Network Business)

- NEC Corporation

- Mavenir Systems, Inc.

- Viavi Solutions Inc.

- MYCOM OSI Limited

- Infovista SAS

- TEOCO Corporation

- EXFO Inc.

- NETSCOUT Systems, Inc.

- Cellwize Wireless Technologies Pte Ltd.

- AirHop Communications, Inc.

- Parallel Wireless, Inc.

- Tupl, Inc.

- Rakuten Symphony Inc.

- Capgemini SE (Engineering and RAN Analytics)

- HCL Technologies Limited

- Amdocs Limited

- VMware, Inc. (Service Management and Analytics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven Predictive Maintenance for 5G Densification

- 4.2.2 Cloud-native RAN Disaggregation Accelerates Data Visibility

- 4.2.3 Surge of Private 5G Networks in Industry 4.0 Plants

- 4.2.4 Open RAN Automation/xApps-rApps Ecosystem Expansion

- 4.2.5 Energy-efficiency Mandates Driving RAN Power Analytics

- 4.2.6 Telco Push Toward Zero-touch Operations (ZTO)

- 4.3 Market Restraints

- 4.3.1 Fragmented Data Standards Across Multi-vendor RAN

- 4.3.2 Skills Gap in AI/ML Model Engineering for CSPs

- 4.3.3 Rising Cyber-attack Surface on Virtualised RAN

- 4.3.4 ROI Uncertainty in Brown-field 4G Modernisations

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform / Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.3 By Network Technology

- 5.3.1 2G / 3G

- 5.3.2 4G / LTE

- 5.3.3 5G NR

- 5.3.4 Open RAN / vRAN

- 5.4 By Application

- 5.4.1 Performance Management

- 5.4.2 Fault and Event Management

- 5.4.3 Mobility and Handover Optimisation

- 5.4.4 Energy and Capacity Optimisation

- 5.5 By End User

- 5.5.1 Tier-1 Mobile Network Operators

- 5.5.2 Mobile Virtual Network Operators

- 5.5.3 Private Enterprise Networks

- 5.5.4 Neutral-Host / TowerCos

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Nokia Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 ZTE Corporation

- 6.4.5 Samsung Electronics Co., Ltd. (Network Business)

- 6.4.6 NEC Corporation

- 6.4.7 Mavenir Systems, Inc.

- 6.4.8 Viavi Solutions Inc.

- 6.4.9 MYCOM OSI Limited

- 6.4.10 Infovista SAS

- 6.4.11 TEOCO Corporation

- 6.4.12 EXFO Inc.

- 6.4.13 NETSCOUT Systems, Inc.

- 6.4.14 Cellwize Wireless Technologies Pte Ltd.

- 6.4.15 AirHop Communications, Inc.

- 6.4.16 Parallel Wireless, Inc.

- 6.4.17 Tupl, Inc.

- 6.4.18 Rakuten Symphony Inc.

- 6.4.19 Capgemini SE (Engineering and RAN Analytics)

- 6.4.20 HCL Technologies Limited

- 6.4.21 Amdocs Limited

- 6.4.22 VMware, Inc. (Service Management and Analytics)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

無線接取網路市場-2026-2032年全球市場預測

無線接取網路市場-2026-2032年全球市場預測 無線接取網路:2025-2031年全球市場預測

無線接取網路:2025-2031年全球市場預測 無線接取網路市場預測至2034年-全球架構、組件、技術、頻段、最終用戶和區域分析vRAN解決方案市場預測至2034年:按組件、部署類型、網路類型、架構、應用、最終用戶和地區分類的全球分析

無線接取網路市場預測至2034年-全球架構、組件、技術、頻段、最終用戶和區域分析vRAN解決方案市場預測至2034年:按組件、部署類型、網路類型、架構、應用、最終用戶和地區分類的全球分析 無線接取網路市場分析及至2035年預測:依類型、服務、技術、部署、產品、硬體及最終用戶分類

無線接取網路市場分析及至2035年預測:依類型、服務、技術、部署、產品、硬體及最終用戶分類 2026年全球無線接取網路市場報告2026年全球無線接取網路(RAN)智慧控制器市場報告2026年無線接取網路(RAN)邊緣可觀測性全球市場報告PMP網路基地台市場按產品類型、最終用戶產業、分銷管道、經營模式和應用分類-全球預測,2026-2032年

2026年全球無線接取網路市場報告2026年全球無線接取網路(RAN)智慧控制器市場報告2026年無線接取網路(RAN)邊緣可觀測性全球市場報告PMP網路基地台市場按產品類型、最終用戶產業、分銷管道、經營模式和應用分類-全球預測,2026-2032年 全球無線接取網分析與監控市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球無線接取網分析與監控市場規模、佔有率、趨勢及成長分析報告(2026-2034)