|

市場調查報告書

商品編碼

2062447

電池感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Battery Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

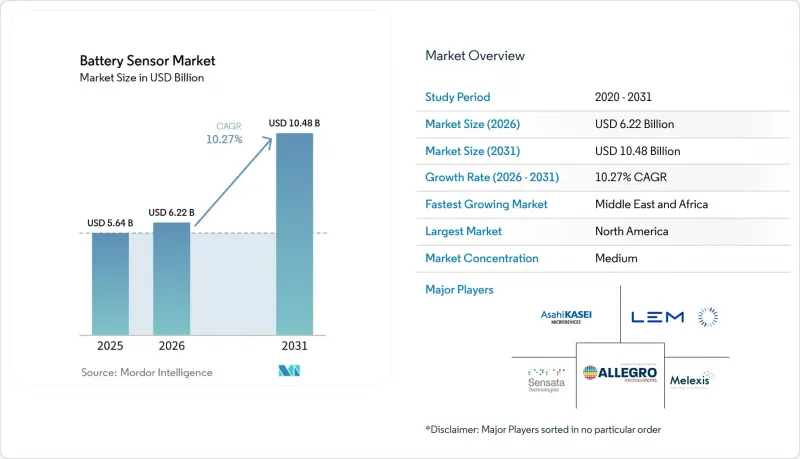

根據 Mordor Intelligence 預測,電池感測器市場規模預計將從 2025 年的 56.4 億美元和 2026 年的 62.2 億美元成長到 2031 年的 104.8 億美元,2026 年至 2031 年的複合年成長率為 10.27%。

本報告按感測器類型(例如,霍爾效應電流感測器)、技術(例如,封閉回路型感測器、開放回路型感測器)、應用(例如,電動乘用車、電動商用車)、終端用戶產業(例如,汽車、能源和公共產業)以及地區(例如,北美、歐洲、亞太地區)進行細分。市場預測以美元計價。

全球電池感測器市場趨勢及洞察

電動車產量激增和xEV電池安全法規日益嚴格

中國GB38031-2025標準規定乘用車和車隊必須在五分鐘內檢測到熱失控,這要求從簡單的熱敏電阻器串轉向多感測器融合技術,該技術結合了霍爾效應電流、光纖溫度和MEMS壓力通道。將於2024年核准的ISO 21498介面在電池管理系統和車輛控制單元之間增加了一條雙向資料通路,從而能夠即時限制輸出以抑制過放電事件。 ZOE Energy Storage將於2025年推出一款四參數檢測堆棧,其熱失控檢測速度比傳統電池組快20倍,顯示監管壓力正在重塑設計規則。

公用事業規模儲能設施的快速擴張

Alliant Energy位於威斯康辛州的200兆瓦/400兆瓦時儲能設施於2026年3月投入運作,該設施依靠50個貨櫃內安裝的12,000個受監控單元,凸顯了現代電網中感測器部署的規模。 SSE的100兆瓦渡橋系統利用電阻技術來偵測內阻波動,延長了其使用壽命。喬治亞電力公司的65兆瓦儲能設施透過採用無線監視器,省去了兩公里長的銅線束,節省了12萬美元的安裝成本。這些案例表明,感測器驅動的預測性維護如何有助於降低儲能的平準化度電成本(LCOE)。

低成本分流解決方案中存在廣泛的溫度漂移和偏移誤差。

由於汽車溫度循環的影響,裸露的分流器會產生 50µV/ 度C的偏移漂移,導致車輛使用壽命期間測量範圍預測誤差達到 3%。這需要一個共模抑制比為 120 dB 的外部運算放大器,這將使元件成本增加 1.20 美元,抵消分流器本身的成本優勢。此外,800V 逆變器的電磁干擾會導致總誤差超過 0.5%,超出 ISO 21498 標準的精度限制。

細分市場分析

到2025年,霍爾效應元件將佔據電池感測器市場43.2%的佔有率。這主要歸功於其非接觸式雙向測量能力,而這對於再生煞車至關重要。受固態電池先導計畫(需要與陶瓷相容的色散溫度測量)的推動,光纖感測器預計到2031年將以11.9%的複合年成長率成長。雖然分流器在±1%精度即可滿足需求的消費性電子產品中仍發揮重要作用,但ISO 21498標準要求汽車平台的精度與霍爾感測器相當。德克薩斯(TI)的18通道電壓IC自2025年8月起開始出貨,能夠偵測低至1mV的電壓差,從而進一步推動了整合監控的藍圖。

光纖布拉格光柵(FBG)串在公用事業規模系統中日益普及,因為它們能夠抵抗高壓逆變熱敏電阻器普遍存在的電磁干擾。 MEMS壓力晶片,例如Honeywell的0.25% FS BPS系列,能夠在熱量積聚加劇之前很久就檢測到低至2 kPa的氣體積聚。成長放緩的原因在於缺乏能夠承受3000次插拔循環和-40 度C至125 度C溫度循環的汽車級光纖連接器,但康寧和Prismian正在透過開發穩健的LC連接器來應對這一挑戰。

預計到2025年,閉合迴路隔離設計將佔銷售額的40.5%。這主要得益於市場對800V平台中1000A無漂移感測技術的需求不斷成長,而這些技術對於高性能電動車和工業應用至關重要。無線節點預計將以11.7%的複合年成長率成長,尤其有利於商用車隊營運商。例如,Dukosi的C-SynQ技術已將組裝重量減少了15%,組裝時間縮短了40%。 NXP的超寬頻平台提供10公分級精度的3D單元定位能力,能夠快速辨識並定位故障單元,從而簡化故障排查工作。這對於最大限度地減少停機時間和營運效率低下至關重要。

採用 CAN FD 和 I2C 協定的數位輸出感測器正在迅速普及。例如,英飛凌的 XDM700-1 感測器能夠以 5Mbps 的速率傳輸18 個通道的數據,滿足了現代電池管理系統對高速資料通訊日益成長的需求。另一方面,由於功能上的限制,模擬感測器的應用往往局限於傳統的工業 UPS 應用。瑞薩電子的 DA14533 感測器是一款低功耗藍牙感測器,使用紐扣電池即可實現長達 10 年的使用壽命,使其成為電動滑板車和其他小型行動裝置的理想解決方案。然而,CAN-藍牙閘道的雙重認證流程是一個瓶頸,將產品上市時間延長約 9 個月,這對希望快速回應市場需求的製造商來說是一個挑戰。

區域分析

預計到2025年,亞太地區將佔電池感測器市場收入的33.3%,並預計在2031年之前以11.1%的複合年成長率成長,這主要得益於GB38031-2025標準強制要求的熱失控檢測。以日本廠商為例,例如計畫於2026年4月發布的B-and-Plus無線監測器,這些廠商正在自動導引運輸車(AGV)中消除線束並提高更換速度。在韓國,350kW充電強制要求使用電阻譜技術,而恩智浦半導體(NXP)的BMA7418晶片組支援此技術。在印度,超過50MW的可再生能源專案強制要求配備電池能源儲存系統,這推動了對成本最佳化型感測器的需求。

在北美和歐洲,符合 ISO 26262 ASIL D 標準的雙通道電流偵測技術是首選。在德國,無鐵芯霍爾感測器已成為主流,英飛凌透過取消鐵氧體磁芯,實現了每台感測器 0.80 歐元(0.85 美元)的成本降低。在英國費裡布里奇電站,電阻譜技術預計將使儲能成本降低 8%。美國威斯康辛州和喬治亞的電力公司已經證明了無線監測器的成本優勢,它可以節省數千美元的銅線成本。

在中東和非洲,電池儲能正被應用於沙烏地阿拉伯的NEOM等大型企劃中,該專案強制要求進行氫氣檢測以應對高溫環境。在南非的可再生能源專案中,採用的分流解決方案在1%精度即可滿足要求的情況下,可降低40%的成本。南美洲的部署主要集中在巴西,該國的NOM-194-SCFI-2015標準與基於CAN FD的數位監控器相容。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車產量激增以及電動車電池的嚴格安全法規

- 大型儲能設施的快速擴張

- 霍爾效應電流感測器的成本更低、精度更高

- ISO 21498 電池監控介面標準化

- 將電池級光纖感測技術整合到固態電池試點計畫中

- 在微型移動出行電池組中採用 Wake-on-CAN 超低功耗感測技術。

- 市場限制因素

- 低成本分流解決方案中存在廣泛的溫度漂移和偏移誤差。

- 鐵氧體或坡莫合金磁芯的價格波動和供應狀況

- 1 MHz 隔離電流感測器調變中 EMC 合規性的挑戰

- 無線電池感測器協定缺乏認證機構

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 依感測器類型

- 霍爾效應電流感測器

- 分流式電流感測器

- 電壓監控積體電路

- 溫度(NTC/PTC)感測器

- 光纖電池感測器

- MEMS壓力感測器(單元級)

- 透過技術

- 封閉回路型(隔離式)感測器

- 開放回路感應器

- 數位(I2C/CAN/SENT)輸出

- 類比輸出

- 無線電池感測器

- 透過使用

- 電動乘用車

- 電動商用車

- 混合動力汽車和插電式混合動力汽車

- 固定式能源儲存系統

- 家用電子產品

- 工業級UPS和備用電源

- 按最終用戶行業分類

- 車

- 能源公用事業

- 家用電子產品

- 工業和製造業

- 電訊

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Allegro MicroSystems, Inc.

- Asahi Kasei Microdevices Corporation

- Melexis NV

- LEM Holding SA

- Sensata Technologies Holding plc

- Texas Instruments Incorporated

- Infineon Technologies AG

- TDK Corporation

- Honeywell International Inc.

- TE Connectivity Ltd.

- Analog Devices, Inc.

- NXP Semiconductors NV

- Murata Manufacturing Co., Ltd.

- HIOKI EE Corporation

- Littelfuse, Inc.

- Renesas Electronics Corporation

- Alpha and Omega Semiconductor Limited

- Silicon Laboratories Inc.

- Eaton Corporation plc

- ROHM Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the battery sensor market size is expected to increase from USD 5.64 billion in 2025 and USD 6.22 billion in 2026 to reach USD 10.48 billion by 2031, growing at a CAGR of 10.27% over 2026-2031.

This report is Segmented by Sensor Type (Hall-Effect Current Sensors, and More), Technology (Closed-Loop Sensors, Open-Loop Sensors, and More), Application (Electric Passenger Vehicles, Electric Commercial Vehicles, and More), End-User Industry (Automotive, Energy and Utilities, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Battery Sensor Market Trends and Insights

EV Production Surge And Stringent xEV Battery-Safety Mandates

China's GB38031-2025 standard obliges passenger cars and fleets to detect thermal runaway within five minutes, forcing a shift from simple thermistor strings to multi-sensor fusion that couples Hall-effect current, fiber-optic temperature, and MEMS pressure channels. The ISO 21498 interface, ratified in 2024, adds bidirectional data paths between battery management systems and vehicle control units, enabling real-time power limitation that curbs over-discharge events. ZOE Energy Storage fielded a four-parameter detection stack in 2025 that identifies runaway 20 times earlier than legacy packs, illustrating how regulatory pressure is reshaping design rules.

Rapid Growth Of Utility-Scale Energy-Storage Installations

Alliant Energy's 200 MW-400 MWh site in Wisconsin, commissioned in March 2026, relies on 12,000 monitored cells across 50 containers, highlighting the scale of sensor deployment in modern grids. SSE's 100 MW Ferrybridge system uses impedance spectroscopy to flag internal resistance drift and lengthen service life. Wireless monitors at Georgia Power's 65 MW facility removed two kilometers of copper harness, cutting installation outlay by USD 120,000. These installations show how sensor-enabled predictive maintenance underpins lower levelized cost of storage.

Wide Temperature-Drift And Offset Errors In Low-Cost Shunt Solutions

Automotive temperature cycles induce 50 µV °C-1 offset drift in bare shunts, translating into 3% range-prediction error over vehicle life. External op-amps with 120 dB common-mode rejection are required, adding USD 1.20 in components and offsetting shunts' perceived savings. EMI from 800 V inverters further pushes total error beyond 0.5%, breaching ISO 21498 accuracy limits.

Other drivers and restraints analyzed in the detailed report include:

- Falling Cost And Accuracy Gains In Hall-Effect Current Sensors

- Standardization Of ISO 21498 Battery Monitoring Interfaces

- Volatile Pricing And Supply Of Ferrite Or Permalloy Magnetic Cores

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect devices owned 43.2% Battery sensor market share in 2025, thanks to contactless bidirectional measurement vital for regenerative braking. Fiber-optic sensors are on an 11.9% CAGR path to 2031, propelled by solid-state battery pilots that require ceramic-safe, distributed temperature reading. Shunts stay relevant in consumer gadgets where +-1% suffices, yet ISO 21498 pushes automotive platforms toward Hall accuracies. Texas Instruments' 18-channel voltage IC, shipping since August 2025, resolves 1 mV differentials, reinforcing integrated monitoring roadmaps.

Fiber Bragg grating strings are gaining in utility-scale systems, resisting electromagnetic interference that plagues thermistors near high-voltage inverters. MEMS pressure chips, such as Honeywell's 0.25%-FS BPS line, detect 2 kPa gas buildup well before exothermic escalation. Growth is tempered by the lack of automotive-rated fiber connectors that survive 3,000 matings and -40 °C to 125 °C cycles, a gap both Corning and Prysmian address with rugged LC variants.

Closed-loop isolated designs delivered 40.5% revenue in 2025, driven by the increasing demand for drift-free 1,000 A sensing in 800 V platforms, which are critical for high-performance electric vehicles and industrial applications. Wireless nodes are forecast to grow at an 11.7% CAGR, as Dukosi's C-SynQ technology demonstrated a 15% reduction in pack mass and a 40% decrease in assembly time, particularly benefiting commercial fleet operators. NXP's ultra-wideband platform offers precise 10 cm 3-D cell location capabilities, simplifying warranty forensics by enabling quick identification and mapping of faulty units, which is crucial for minimizing downtime and operational inefficiencies.

Digital output sensors utilizing CAN FD and I2C protocols are expanding rapidly, with Infineon's XDM700-1 sensor transferring 18-channel data at 5 Mbps, catering to the growing need for high-speed data communication in modern battery management systems. Meanwhile, analog variants are increasingly relegated to legacy industrial UPS roles due to their limited capabilities. Renesas' DA14533 sensor supports a 10-year coin-cell lifetime for Bluetooth Low Energy sensors, making it an ideal solution for e-scooters and other compact mobility devices. However, the dual certification process for CAN-to-Bluetooth gateways has been identified as a bottleneck, extending product launch timelines by approximately 9 months, posing challenges for manufacturers aiming to meet market demand swiftly.

Geography Analysis

Asia-Pacific generated 33.3% of the battery sensor market revenue in 2025 and is set for an 11.1% CAGR to 2031 as GB38031-2025 makes thermal-runaway detection compulsory. Japanese vendors, exemplified by B-and-Plus's April 2026 wireless monitor, scrap harnesses in automated guided vehicles, improving swap speed. South Korea specifies impedance spectroscopy for 350 kW charging, satisfied by NXP's BMA7418 chipset. India's above 50 MW renewable projects mandate battery energy-storage add-ons, spurring demand for cost-optimized sensors.

North America and Europe prioritize ISO 26262 ASIL D dual-channel current sensing. Germany champions coreless Hall sensors, with Infineon trimming EUR 0.80 (USD 0.85) per unit by deleting ferrite cores. The United Kingdom's Ferrybridge site projects an 8% lower levelized storage cost via impedance spectroscopy. U.S. utilities in Wisconsin and Georgia illustrate the cost case for wireless monitors that wipe out thousands of dollars in copper.

The Middle East and Africa adopt battery storage in megaprojects such as Saudi Arabia's NEOM, specifying hydrogen gas detection to tackle high-ambient heat. South Africa's renewables program turns to shunt solutions at 40% lower cost where 1% accuracy suffices. South American adoption is concentrated in Brazil, where NOM-194-SCFI-2015 aligns with digital monitors built on CAN FD.

- Allegro MicroSystems, Inc.

- Asahi Kasei Microdevices Corporation

- Melexis NV

- LEM Holding SA

- Sensata Technologies Holding plc

- Texas Instruments Incorporated

- Infineon Technologies AG

- TDK Corporation

- Honeywell International Inc.

- TE Connectivity Ltd.

- Analog Devices, Inc.

- NXP Semiconductors N.V.

- Murata Manufacturing Co., Ltd.

- HIOKI E.E. Corporation

- Littelfuse, Inc.

- Renesas Electronics Corporation

- Alpha and Omega Semiconductor Limited

- Silicon Laboratories Inc.

- Eaton Corporation plc

- ROHM Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Production Surge and Stringent xEV Battery-Safety Mandates

- 4.2.2 Rapid Growth of Utility-Scale Energy-Storage Installations

- 4.2.3 Falling Cost and Accuracy Gains in Hall-Effect Current Sensors

- 4.2.4 Standardization of ISO 21498 Battery Monitoring Interfaces

- 4.2.5 Integration of Cell-Level Fiber-Optic Sensing in Solid-State Battery Pilots

- 4.2.6 Adoption of Wake-on-CAN Ultra-Low-Power Sensing for Micro-Mobility Packs

- 4.3 Market Restraints

- 4.3.1 Wide Temperature-Drift and Offset Errors in Low-Cost Shunt Solutions

- 4.3.2 Volatile Pricing and Supply of Ferrite or Permalloy Magnetic Cores

- 4.3.3 EMC Compliance Hurdles for 1 MHz Isolated Current-Sensor Modulation

- 4.3.4 Scarcity of Certification Labs for Wireless Battery-Sensor Protocols

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Hall-Effect Current Sensors

- 5.1.2 Shunt-Based Current Sensors

- 5.1.3 Voltage Monitoring ICs

- 5.1.4 Temperature (NTC / PTC) Sensors

- 5.1.5 Fiber-Optic Battery Sensors

- 5.1.6 MEMS Pressure Sensors (Cell-Level)

- 5.2 By Technology

- 5.2.1 Closed-Loop (Isolated) Sensors

- 5.2.2 Open-Loop Sensors

- 5.2.3 Digital (I2C / CAN / SENT) Output

- 5.2.4 Analog Output

- 5.2.5 Wireless Battery Sensors

- 5.3 By Application

- 5.3.1 Electric Passenger Vehicles

- 5.3.2 Electric Commercial Vehicles

- 5.3.3 Hybrid and Plug-in Hybrid Vehicles

- 5.3.4 Stationary Energy-Storage Systems

- 5.3.5 Consumer Electronics

- 5.3.6 Industrial UPS and Backup

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Energy and Utilities

- 5.4.3 Consumer Electronics

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Telecommunications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Allegro MicroSystems, Inc.

- 6.4.2 Asahi Kasei Microdevices Corporation

- 6.4.3 Melexis NV

- 6.4.4 LEM Holding SA

- 6.4.5 Sensata Technologies Holding plc

- 6.4.6 Texas Instruments Incorporated

- 6.4.7 Infineon Technologies AG

- 6.4.8 TDK Corporation

- 6.4.9 Honeywell International Inc.

- 6.4.10 TE Connectivity Ltd.

- 6.4.11 Analog Devices, Inc.

- 6.4.12 NXP Semiconductors N.V.

- 6.4.13 Murata Manufacturing Co., Ltd.

- 6.4.14 HIOKI E.E. Corporation

- 6.4.15 Littelfuse, Inc.

- 6.4.16 Renesas Electronics Corporation

- 6.4.17 Alpha and Omega Semiconductor Limited

- 6.4.18 Silicon Laboratories Inc.

- 6.4.19 Eaton Corporation plc

- 6.4.20 ROHM Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽車智慧電池感測器市場:按車輛類型、感測器類型、運輸方式、應用和銷售管道分類-2026-2032年全球市場預測

汽車智慧電池感測器市場:按車輛類型、感測器類型、運輸方式、應用和銷售管道分類-2026-2032年全球市場預測 2026年全球汽車智慧電池感測器市場報告汽車電池感測器市場:按感測器類型、電池化學成分、車輛類型和分銷管道分類-2026-2032年全球預測

2026年全球汽車智慧電池感測器市場報告汽車電池感測器市場:按感測器類型、電池化學成分、車輛類型和分銷管道分類-2026-2032年全球預測 2026-2034年全球汽車智慧電池感測器市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車智慧電池感測器市場規模、佔有率、趨勢和成長分析報告 汽車智慧電池感測器市場規模、佔有率和成長分析(按類型/通訊協定、感測器類型、應用、車輛類型、最終用途和地區分類)—產業預測(2026-2033 年)

汽車智慧電池感測器市場規模、佔有率和成長分析(按類型/通訊協定、感測器類型、應用、車輛類型、最終用途和地區分類)—產業預測(2026-2033 年) 全球車輛智慧電池感測器市場

全球車輛智慧電池感測器市場 智慧電池感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測全球智慧電池感測器市場

智慧電池感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測全球智慧電池感測器市場 2030 年智慧電池感測器市場預測:按感測器類型、技術、應用、最終用戶和地區進行的全球分析到 2030 年電池感測器市場預測:按感測器類型、電壓類型、車輛類型、技術、應用、分銷管道和地區進行的全球分析

2030 年智慧電池感測器市場預測:按感測器類型、技術、應用、最終用戶和地區進行的全球分析到 2030 年電池感測器市場預測:按感測器類型、電壓類型、車輛類型、技術、應用、分銷管道和地區進行的全球分析