|

市場調查報告書

商品編碼

2062429

噴墨編碼器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Inkjet Coders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

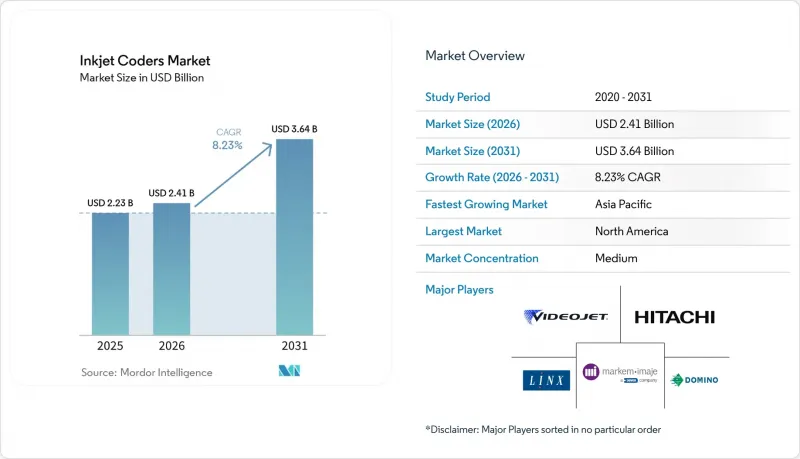

根據 Mordor Intelligence 預測,噴墨編碼器市場將從 2025 年的 22.3 億美元成長到 2026 年的 24.1 億美元,到 2031 年達到 36.4 億美元,2026 年至 2031 年的複合年成長率預計為 8.23%。

本報告按技術(連續噴墨等)、終端用戶產業(食品飲料、醫藥保健等)、墨水類型(溶劑型染料墨水、UV固化墨水和LED墨水等)、基材(塑膠、紙張和紙板等)以及地區(北美、亞太等)進行細分。市場預測以美元計價。

全球噴墨編碼器市場趨勢及洞察

嚴格的序列化和可追溯性規定

美國和歐盟的藥品供應鏈法規規定,所有處方藥包裝必須包含符合 ISO/IEC 15415 1.5 級或更高標準的2D條碼,這迫使製造商改造或更換編碼器,以實現符合法規要求的高解析度列印。中國國家藥品監督管理局和印度的 iVEDA 出口計畫已將類似要求擴展到亞洲生產商,而沙烏地阿拉伯將於 2025 年 10 月生效的雙語條碼要求,則在採購清單中增加了多字元集功能。食品可追溯性也不斷推進,美國《食品安全現代化法案》(FSMA) 第 204 條規則和 GS1 的「Sunrise 2027」舉措均要求高風險食品包含零售可讀的序列化2D條碼。這些政策共同縮短了決策的寬限期,使得引入符合標準的噴墨編碼器作為市場解決方案成為資本投資計畫的核心。

高速快速消費品生產線的普及

在飲料、乳製品和休閒食品工廠,這些印表機目前以每分鐘 1200 個單位的速度運作,將列印時間縮短至幾分之一秒。 Markem-Imaje 的 9750 熱噴墨印表機在 2024 年的試點項目中實現了每小時 12 萬罐的處理速度,與傳統的連續噴墨列印小寫字母條碼的方法相比,展現出卓越的處理能力。 Domino 的 Gx 系列印表機在軟性薄膜上也能達到類似的列印速度,確保在枕式包裝袋上達到清晰、高對比度的列印效果。亞太地區的飲料工廠正在逐步部署這些設備,北美地區的乳製品生產商也在維修其 HDPE 塑膠罐生產線。連接到剔除站的攝影機會即時檢驗所有條碼,從而避免產品召回和罰款。

與排放相關的法規限制了溶劑型油墨的使用。

由於加州空氣資源委員會 (CARB) 設定的排放上限以及歐盟 REACH 法規對丁酮、甲苯和二甲苯的限制,加工商被迫以紫外光固化油墨或水性油墨取代溶劑型油墨。雖然溶劑型油墨對高密度聚乙烯 (HDPE) 和聚丙烯 (PP) 仍具有優異的附著力,但新的揮發性有機化合物 (VOC) 排放閾值正在加速紫外光固化 (UV-LED) 技術的應用,該技術不僅消除了空氣污染物,而且符合有關其向食品接觸材料轉移的法規。

細分市場分析

熱噴墨生產線滿足了飲料和乳製品市場日益成長的需求,推動該細分市場的複合年成長率達到9.9%,儘管到2025年,連續噴墨仍將佔銷售額的43.2%。連續噴墨印表機市場規模持續成長,這得益於其非接觸式列印的通用性,以及與包括塑膠、薄膜和瓦楞紙板在內的多種材料的兼容性。高解析度壓電式按需噴墨平台在藥品序列化領域市佔率不斷擴大,能夠列印傳統系統無法實現的ISO/IEC標準級資料矩陣碼。閥噴式系統在建築材料和農藥包裝領域仍保持強勁勢頭,因為在這些領域,字元高度比圖形細節更為重要。高黏度壓電噴頭的研究和開發正在取得進展,例如京瓷的 1,584 噴嘴型號,能夠以 80 mPa·s 的速度噴射液體,這將使噴墨技術擴展到裝飾塗料和 3D 模具應用領域。

關於規模化生產的經驗教訓各不相同。熱敏噴頭在生產線速度超過每分鐘 1000 個單元的情況下表現出色,但噴嘴壽命和墨盒成本仍然是主要問題。另一方面,連續噴墨供應商透過提供噴頭診斷功能(例如自清潔)和降低單碼耗材成本,在軟包裝領域保持主導地位。因此,混合技術的採用十分普遍,使工廠能夠在不犧牲運作的前提下,為合適的承印物選擇合適的噴頭。

預計到2025年,食品飲料產業將佔總銷售額的40.5%。這主要得益於龐大的SKU數量以及零售商對2D條碼的需求。由於2D條碼在各類產品類型中的廣泛應用,該產業將繼續保持其主導地位。然而,受全球序列化舉措的推動,醫藥和醫療保健產業正經歷最快的成長,複合年成長率高達9.7%。主要由食品公司驅動的噴墨編碼器市場預計將保持其強勁勢頭。同時,注射用生物製藥、預填充式注射器和醫療設備套裝對高解析度編碼的需求不斷成長,為高利潤率的銷售創造了機會。此外,電子產品製造商正在採用紫外線固化和雷射混合技術來滿足IPC可追溯性標準,而汽車和航太行業則正在為引擎缸體和複合材料面板引入閥門噴射編碼器。

為了滿足不斷變化的需求,特別是關於永久性批號的法規要求,化妝品品牌也正在轉向使用UV-LED油墨。這些油墨經過特殊設計,能夠無縫粘附在觸感柔軟的層壓材料上,而不會對其造成損壞,從而在保持產品美觀的同時確保符合法規要求。整個產業對可追溯性和法規遵循的日益重視,正在推動編碼和識別技術的創新。因此,製造商正在加大對先進解決方案的投資,以滿足這些需求並提高營運效率。這一趨勢凸顯了編碼技術在滿足特定產業需求以及應對嚴格法規和消費者期望帶來的挑戰方面所發揮的關鍵作用。

區域分析

在《藥品供應鏈安全法案》(DSCSA) 和《食品安全現代化法案》(FSMA) 第 204 條的推動下,預計到 2025 年,北美地區的銷售額將佔全球總銷售額的 33.3%,這將加速 2D 列印機在製藥和高風險食品加工廠的廣泛應用。生產商正在將編碼器與製造執行系統 (MES) 和企業資源計劃 (ERP) 系統整合,以實現可變資料的自動化處理和遠端診斷,從而減少人為錯誤和人事費用。雖然加州更嚴格的揮發性有機化合物 (VOC) 法規正在加速向紫外線 LED 的過渡,但高昂的初始投資成本阻礙了中小型加工商採用該技術。

亞太地區以9.1%的複合年成長率領跑,主要受中國肉毒桿菌毒素序列化、印度強制使用GS1QR碼以及沙烏地阿拉伯雙語條碼法規等因素的影響,這些法規對該地區出口商造成了衝擊。值得關注的投資包括SATO在泰國投資1,130萬美元興建的標籤工廠,該工廠年產700萬平方公尺,主要面向東南亞市場。成都凱利爾等本土供應商透過提供比歐美品牌低30-40%的模組化編碼器,正在中小企業中搶佔市場佔有率。

在歐洲,根據第二階段反仿冒藥品指令和2024年包裝廢棄物法規,可重複使用的容器和不含揮發性有機化合物(VOC)的油墨已被強制使用,市場需求依然旺盛。高階品牌正在升級到紫外線LED噴墨印表機,而注重成本的企業則將噴墨印表機更換為環保溶劑型油墨。德國、英國和法國在工業4.0框架下主導編碼器整合,而東歐國家則在合規要求和預算限制之間尋求平衡。此外,中東和非洲符合歐盟標準的序列化法律,以及已在南美洲全面實施的巴西數位藥品護照,也都在推動市場發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 嚴格的序列化和可追溯性規定

- 高速快速消費品生產線的普及

- 快速過渡到永續、可清洗和可回收包裝

- 將CIJ/TIJ噴頭整合到工業4.0 MES系統中

- 採用紫外線固化油墨防止仿冒。

- 用於列印頭的AI驅動預測性維護演算法

- 市場限制因素

- 限制溶劑型油墨的VOC相關排放法規

- 凍結易受景氣衰退影響產業的資本投資

- 與雷射編碼器在高對比包裝領域的競爭日益激烈。

- 壓電印字頭組件供應鏈瓶頸

- 產業價值/價值鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 連續噴墨(CIJ)

- 熱噴墨(TIJ)

- 壓電按需滴落

- 閥門噴射式/大字

- 產業最終用途

- 食品/飲料

- 藥品和醫療保健

- 電子與電機工程

- 汽車和航太

- 化妝品和個人護理

- 化學/工業製造

- 按墨水類型

- 溶劑型染料墨水

- UV固化和LED油墨

- 水性油墨

- 食品級和可食用油墨

- 顏料墨水和特殊墨水

- 按基板

- 塑膠(HDPE、PET、PP)

- 紙張和紙板

- 玻璃

- 金屬(鋁、鐵)

- 軟性薄膜和層壓

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Videojet Technologies, Inc.

- Markem-Imaje SAS

- Domino Printing Sciences plc

- Hitachi Industrial Equipment Systems Co., Ltd.

- Linx Printing Technologies Ltd.

- Control Print Limited

- REA Elektronik GmbH

- Matthews International Corporation(Matthews Marking Systems)

- Needham Ink Technologies Ltd.

- FoxJet LLC

- InkJet, Inc.

- KEYENCE Corporation

- Koenig and Bauer Coding GmbH(KBA-Metronic)

- KGK Jet India Pvt. Ltd.

- RN Mark Inc.

- Squid Ink Manufacturing Inc.

- Weber Marking Systems GmbH

- Zanasi Srl

- HSA Systems A/S

- Leibinger GmbH

- EBS Ink-Jet Systeme GmbH

- ATD Ltd.(ALE)

- Guangzhou EC-JET Electronic Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the inkjet coders market size is expected to increase from USD 2.23 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.64 billion by 2031, growing at a CAGR of 8.23% over 2026-2031.

This report is Segmented by Technology (Continuous Inkjet, and More), End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, and More), Ink Type (Solvent-Based Dye Inks, UV-Curable and LED Inks, and More), Substrate Material (Plastics, Paper and Paperboard, and More), and Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Inkjet Coders Market Trends and Insights

Stringent Serialization and Traceability Regulations

Drug-supply-chain laws in the United States and the European Union now obligate every prescription pack to carry Data Matrix barcodes that pass ISO/IEC 15415 grade 1.5 or higher, pushing manufacturers to retrofit or replace coders for compliant high-resolution printing. China's National Medical Products Administration and India's iVEDA export program extended the same requirement to Asian producers, while Saudi Arabia's dual-language mandate, effective October 2025, added multi-character-set capability to procurement checklists. Food traceability is moving in parallel, as the U.S. FSMA Rule 204 and the GS1 Sunrise 2027 initiative force high-risk foods to carry serialized 2D codes readable at retail. Collectively, these policies compress decision windows, making compliance-ready inkjet coders market solutions central to capital plans.

Proliferation of High-Speed FMCG Production Lines

Beverage, dairy, and snack plants now run at 1,200 units per minute, narrowing the print window to fractions of a second. Markem-Imaje's 9750 thermal inkjet achieved 120,000 cans per hour in 2024 trials, highlighting throughput advantages over legacy continuous inkjet on small-character codes. Domino's Gx-Series meets similar speeds on flexible films, ensuring crisp, high-contrast marks on flow-wrap pouches. Asia-Pacific beverage hubs lead installations, while North American dairies retrofit HDPE jug lines. Cameras wired into reject stations verify every code in real time, safeguarding against recalls and penalties.

VOC-Related Emissions Rules Limiting Solvent-Based Inks

California Air Resources Board caps and EU REACH limits on methyl ethyl ketone, toluene, and xylene force converters to replace solvent inks with UV-curable or water-based formulations. Although solvent inks still offer superior adhesion on HDPE and PP, new VOC thresholds accelerate UV-LED adoption that eliminates airborne pollutants and aligns with food-contact migration rules.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Sustainable, Washable and Returnable Packaging

- Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks

- Capital-Expenditure Freezes in Recession-Exposed Sectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal inkjet lines captured expanding beverage and dairy demand, pushing the segment toward a 9.9% CAGR, while continuous inkjet still held 43.2% of 2025 revenue. The inkjet coders market size for continuous inkjet remains buoyed by its non-contact versatility across plastics, films and corrugate. High-resolution piezo drop-on-demand platforms gained share in pharmaceutical serialization, printing Data Matrix codes at ISO/IEC grades that legacy systems cannot match. Adoption of valve-jet units stayed strong in construction and agro-chemical packaging where character height outweighs graphic fidelity. Ongoing R&D in high-viscosity piezo heads, exemplified by Kyocera's 1,584-nozzle model able to jet 80 mPa*s fluids, will extend inkjet into decorative coatings and 3D molds.

Scaling lessons differ. Thermal heads excel where line speeds exceed 1,000 units per minute, yet nozzle lifespan and cartridge cost remain scrutinized. Continuous inkjet vendors counter with self-cleaning printhead diagnostics and lower per-code consumables, defending dominance in flexible packaging. Mixed-technology footprints are therefore common, allowing plants to allocate the right head to the right substrate without sacrificing uptime.

Food and beverage lines accounted for 40.5% of the revenue in 2025, driven by extensive SKU counts and retailer requirements for 2D barcodes. This segment remains dominant due to its broad application across various product categories. However, the pharmaceutical and healthcare sectors are experiencing the fastest growth, with a compound annual growth rate (CAGR) of 9.7%, fueled by global serialization initiatives. The inkjet coders market, primarily led by food companies, is expected to maintain its stronghold. At the same time, the increasing demand for high-resolution coding in injectable biologics, pre-filled syringes, and medical-device kits is creating opportunities for higher-margin unit volumes. Additionally, electronics manufacturers are adopting UV-curable and laser hybrid technologies to meet IPC traceability standards, while automotive and aerospace industries are integrating valve-jet coders for engine blocks and composite panels.

Cosmetics brands are also adapting to evolving requirements, particularly indelible batch-code regulations, by transitioning to UV-LED inks. These inks are specifically designed to bond seamlessly to soft-touch laminates without causing blemishes, ensuring compliance and maintaining product aesthetics. The growing emphasis on traceability and regulatory compliance across industries is driving innovation in coding and marking technologies. As a result, manufacturers are increasingly investing in advanced solutions to meet these demands while enhancing operational efficiency. This trend highlights the critical role of coding technologies in supporting industry-specific needs and addressing the challenges posed by stringent regulations and consumer expectations.

Geography Analysis

North America contributed 33.3% of 2025 revenue on the back of DSCSA and FSMA Rule 204, spurring wide deployment of 2D-capable printers in pharmaceutical and high-risk food plants. Producers integrate coders with MES and ERP suites to automate variable data and remote diagnostics, reducing manual errors and labor overhead. California's tougher VOC caps accelerate UV-LED conversions, although high capital cost tempers rollout among smaller processors.

Asia-Pacific registers the fastest 9.1% CAGR, fueled by China's botulinum-toxin serialization, India's GS1 QR mandates, and Saudi Arabia's dual-language barcode rule that impacts exporters across the region. Investments include SATO's USD 11.3 million Thai label plant that produces 7 million m2 annually to service Southeast Asia. Local vendors such as Chengdu Kelier scale modular coders priced 30-40% below Western brands, capturing share in small-to-medium enterprises.

Europe sustains sizeable demand under the Falsified Medicines Directive Phase 2 and the 2024 Packaging Waste Regulation, which require reusable containers and VOC-free inks. Premium brands upgrade to UV-LED while cost-sensitive firms retrofit CIJ with eco-solvent blends. Germany, the U.K. and France spearhead Industry 4.0 coder integration, whereas Eastern Europe balances compliance needs against budget constraints. Additional momentum stems from Middle East and African serialization laws aligned with EU standards and Brazil's digital drug passport now active across South America.

- Videojet Technologies, Inc.

- Markem-Imaje SAS

- Domino Printing Sciences plc

- Hitachi Industrial Equipment Systems Co., Ltd.

- Linx Printing Technologies Ltd.

- Control Print Limited

- REA Elektronik GmbH

- Matthews International Corporation (Matthews Marking Systems)

- Needham Ink Technologies Ltd.

- FoxJet LLC

- InkJet, Inc.

- KEYENCE Corporation

- Koenig and Bauer Coding GmbH (KBA-Metronic)

- KGK Jet India Pvt. Ltd.

- RN Mark Inc.

- Squid Ink Manufacturing Inc.

- Weber Marking Systems GmbH

- Zanasi S.r.l.

- HSA Systems A/S

- Leibinger GmbH

- EBS Ink-Jet Systeme GmbH

- ATD Ltd. (ALE)

- Guangzhou EC-JET Electronic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Serialization and Traceability Regulations

- 4.2.2 Proliferation of High-Speed FMCG Production Lines

- 4.2.3 Rapid Shift to Sustainable, Washable and Returnable Packaging

- 4.2.4 Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks

- 4.2.5 Adoption of UV-Curable Inks for Counterfeit Mitigation

- 4.2.6 AI-Enabled Predictive-Maintenance Algorithms for Print-Heads

- 4.3 Market Restraints

- 4.3.1 VOC-Related Emissions Rules Limiting Solvent-Based Inks

- 4.3.2 Capital-Expenditure Freezes in Recession-Exposed Sectors

- 4.3.3 Rising Competition from Laser Coders on High-Contrast Packs

- 4.3.4 Supply-Chain Bottlenecks for Piezo Print-Head Components

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Continuous Inkjet (CIJ)

- 5.1.2 Thermal Inkjet (TIJ)

- 5.1.3 Piezo Drop-on-Demand

- 5.1.4 Valve-Jet / Large-Character

- 5.2 By End-Use Industry

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceuticals and Healthcare

- 5.2.3 Electronics and Electrical

- 5.2.4 Automotive and Aerospace

- 5.2.5 Cosmetics and Personal Care

- 5.2.6 Chemicals and Industrial Manufacturing

- 5.3 By Ink Type

- 5.3.1 Solvent-Based Dye Inks

- 5.3.2 UV-Curable and LED Inks

- 5.3.3 Water-Based Inks

- 5.3.4 Food-Grade and Edible Inks

- 5.3.5 Pigmented and Specialty Inks

- 5.4 By Substrate Material

- 5.4.1 Plastics (HDPE, PET, PP)

- 5.4.2 Paper and Paperboard

- 5.4.3 Glass

- 5.4.4 Metals (Aluminum, Steel)

- 5.4.5 Flexible Films and Laminates

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Videojet Technologies, Inc.

- 6.4.2 Markem-Imaje SAS

- 6.4.3 Domino Printing Sciences plc

- 6.4.4 Hitachi Industrial Equipment Systems Co., Ltd.

- 6.4.5 Linx Printing Technologies Ltd.

- 6.4.6 Control Print Limited

- 6.4.7 REA Elektronik GmbH

- 6.4.8 Matthews International Corporation (Matthews Marking Systems)

- 6.4.9 Needham Ink Technologies Ltd.

- 6.4.10 FoxJet LLC

- 6.4.11 InkJet, Inc.

- 6.4.12 KEYENCE Corporation

- 6.4.13 Koenig and Bauer Coding GmbH (KBA-Metronic)

- 6.4.14 KGK Jet India Pvt. Ltd.

- 6.4.15 RN Mark Inc.

- 6.4.16 Squid Ink Manufacturing Inc.

- 6.4.17 Weber Marking Systems GmbH

- 6.4.18 Zanasi S.r.l.

- 6.4.19 HSA Systems A/S

- 6.4.20 Leibinger GmbH

- 6.4.21 EBS Ink-Jet Systeme GmbH

- 6.4.22 ATD Ltd. (ALE)

- 6.4.23 Guangzhou EC-JET Electronic Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球噴墨編碼器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球噴墨編碼器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 噴墨編碼器市場:依技術類型、墨水類型、安裝類型、列印速度、企業規模、最終用戶產業和分銷管道分類-2026-2032年全球市場預測

噴墨編碼器市場:依技術類型、墨水類型、安裝類型、列印速度、企業規模、最終用戶產業和分銷管道分類-2026-2032年全球市場預測 噴墨編碼器市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終用戶、材質、設備及功能分類

噴墨編碼器市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終用戶、材質、設備及功能分類 噴墨印表機市場規模、佔有率及成長分析(按類型、墨水類型、應用、最終用途和地區分類)-2026-2033年產業預測全球噴墨打碼機市場:2025 年至 2030 年預測全球噴墨打碼機市場規模(按類型、最終用戶、地區、範圍和預測)

噴墨印表機市場規模、佔有率及成長分析(按類型、墨水類型、應用、最終用途和地區分類)-2026-2033年產業預測全球噴墨打碼機市場:2025 年至 2030 年預測全球噴墨打碼機市場規模(按類型、最終用戶、地區、範圍和預測) 噴墨打碼機市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

噴墨打碼機市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測