|

市場調查報告書

商品編碼

2062425

量子網路:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Quantum Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

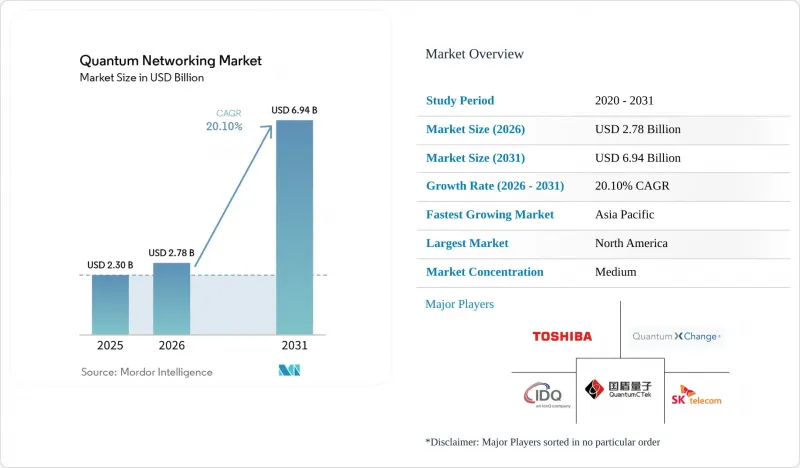

根據 Mordor Intelligence 預測,量子網路市場將從 2026 年的 27.8 億美元成長到 2031 年的 69.4 億美元,2026 年至 2031 年的複合年成長率為 20.1%。

本報告按組件(硬體、軟體、服務)、應用(量子金鑰傳輸、安全雲端通訊等)、最終用戶(政府和國防、大型企業、通訊和IT、金融服務等)、網路類型(地面光纖網路、自由空間光鏈路等)和地區進行細分。市場預測以價值(美元)表示。

全球量子網路市場趨勢與洞察

由於對手利用量子技術,網路安全威脅日益加劇。

國家支持的攻擊者正在快取加密流量,以應對容錯量子電腦的出現,從而加速「先收集後解密」式攻擊。隨著傳統公開金鑰加密的脆弱性日益凸顯,量子金鑰分發(QKD)提供可驗證的安全金鑰,有效抵禦暴力破解破解。美國已最終確定2024年後量子時代的演算法,但維修現有系統需要數年時間,這為QKD提供了即時緩解風險的機會。中國已將量子骨幹網路擴展至約翰尼斯堡,並計劃於2025年完成,凸顯了安全金鑰交換的地緣政治重要性。摩根大通等大型銀行已開始使用QKD連接其交易平台,並指出與純軟體方案相比,延遲降低了18%。

增加政府撥款和國家計劃

公共資金可以降低私人投資的風險。美國能源局已撥款6.25億美元,用於在2025年建成全國性的量子網路原型。歐洲量子通訊基礎設施(EuroQCI)正在投資7.3億歐元(約8.23億美元)建造一條長達1兆公里的跨國網路。印度耗資7.5億美元的「國家量子任務」正在建造一條2000公里的骨幹網,而日本連接東京和大阪的600公里鏈路已於2024年實現了超過1Mbps的關鍵速率。這些協調一致的項目加速了標準的製定,並重振了供應商生態系統。

對量子中繼器和衛星有效載荷的高額資本投入

若要將量子金鑰分發(QKD)的傳輸距離擴展到100公里以上且沒有可靠的節點,則需要部署量子中繼器,每個中繼器的成本約為200萬至500萬美元。例如,一條500公里的城域環路大約需要10個中繼器,成本將顯著增加,尤其是在預算有限的發展中地區。此外,用於QKD部署的衛星有效載荷每次發射的成本也高達5000萬至1.5億美元。根據spacenews.com報導,地面站光學設備的成本可能超過2,000萬美元,這進一步加劇了成本問題。這些高昂的成本構成了大規模部署的主要障礙,使得量子通訊技術的應用主要局限於經濟實力雄厚的國家或那些戰略性地優先投資先進量子通訊技術的國家。

細分市場分析

截至2025年,硬體在量子網路市場中佔60.18%。量子隨機數產生器、單光子源和崩光二極體構成了安全通訊鏈路的基礎。隨著通訊業者部署基於這些資產的託管服務,以服務為導向的量子網路市場規模預計將以20.68%的複合年成長率快速成長。英飛凌的低溫檢測器在通訊波長下實現了85%的效率,從而延長了光纖的有效傳輸距離。包括Quantum Computing Inc.的薄膜鈮酸鋰產品線在內的晶圓代工廠的並行擴產計劃,旨在到2027年實現每季度1萬個光子電路的出貨量。

通訊業者的業務收益正在整合,他們可以透過數千條企業線路分攤高額的重複客戶成本。 Orange Business Services 的「Quantum Defender」以訂閱模式提供量子金鑰分發 (QKD) 服務,將資本投資轉化為營運成本。這種模式無需大量前期投資,使更多企業能夠輕鬆使用量子金鑰傳輸。此外,軟體供應商正在透過在 QKD 系統之上整合金鑰管理編配來增強其產品,從而實現與現有IT基礎設施的無縫整合。這些解決方案還整合了後量子演算法,以確保與舊有系統的向後相容性,並解決未來相容性問題。隨著硬體日益商品化,競爭的焦點正在轉向軟體自動化、服務品質以及提供全面且可擴展的解決方案的能力,以滿足企業客戶不斷變化的需求。

截至2025年,量子金鑰傳輸)佔據了量子網路市場62.28%的佔有率,但分散式量子運算成長最快,預計到2031年複合年成長率(CAGR)將達到20.97%。透過量子糾纏連接多個處理器,可以突破單一站點的限制,擴展邏輯量子位元的數量。 IBM展示了這項能力,他們利用一個三節點網路,將其變分特徵值求解器的處理速度提高了40%。目前,超大規模超大規模資料中心業者正在試行混合架構,將QKD和後量子密碼技術結合,以確保資料中心間連線速度高達100 Gbps。

歐洲的NIS2指令強制要求關鍵基礎設施營運商實施抗量子加密措施,此後,安全雲端通訊受到了廣泛關注。該指令迫使各組織優先考慮安全資料傳輸,以確保符合嚴格的法規要求。雖然量子感測器網路目前仍處於小眾應用領域,但其在高精度時間同步和重力異常檢測方面的潛力正吸引國防領域的關注。這些網路可望在提升國防能力方面發揮關鍵作用。此外,隨著分散式運算的不斷發展,預計網路流量將越來越依賴基於量子糾纏的骨幹網路。這種轉變將進一步增加對低延遲量子金鑰傳輸(QKD)鏈路的需求,而低延遲QKD鏈路對於在先進運算環境中維持安全高效的通訊至關重要。

區域分析

預計到2025年,北美將佔全球收入的50.49%,這主要得益於大量的創業投資資金投資、嚴格的銀行監管以及美國能源局開發的17節點量子網路原型。加拿大預計在2025年投資3.6億加元(約2.67億美元)用於保障能源和通訊資產安全,而墨西哥正在啟動由大學主導的量子金鑰分發(QKD)鏈路先導計畫。該地區主導的市場地位歸功於其強大的生態系統,該生態系統由集中在矽谷、波士頓和多倫多的超大規模資料中心業者中心、國防相關企業和光電新創公司組成。

預計到2031年,亞太地區的複合年成長率將達到20.88%。中國正透過營運一條由1萬公里和145個節點組成的國家骨幹網,展現對技術進步的重視。日本、韓國和新加坡正在擴展都市區量子金鑰分發(QKD)叢集,印度已撥款7.5億美元,計畫在2028年前建成一條2,000公里的量子骨幹網路。澳洲正在資助量子記憶體研究,以延長中繼器狀態的保持時間。儘管該地區的標準仍然分散,但政府的大力支持正在加速全部區域的擴充性。

歐洲受益於歐洲量子糾纏互聯計畫 (EuroQCI) 提供的 7.3 億歐元(8.499 億美元)資金以及統一的法規結構。德國電信的 30 公里量子糾纏隱形傳態技術已成功展示了都市區部署,而 NIS2 的要求正在推動企業採用該技術。英國、德國、法國、義大利和西班牙正在建造國家骨幹網,預計將於 2027 年在 EuroQCI 框架下實現互聯。小規模的經濟體也正在效仿,但通訊市場的碎片化正在減緩統一部署的進程。中東、非洲和南美洲雖然發展落後,但也展現出專注的進步。沙烏地阿拉伯正在利用量子金鑰分發 (QKD) 技術保護海上能源資產,阿拉伯聯合大公國正在試行建立主權資料鏈路。南非已加入中國的北京-約翰尼斯堡量子鏈路,以規避國內資本投資的限制。巴西正在聯合開發衛星地面站,智利正在資助用於採礦應用的量子感測技術。然而,由於預算限制,這些地區的大規模部署受到限制。在新興市場,人們正在考慮採用中心輻射式衛星模式來克服光纖基礎設施的限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用量子技術的對手對網路安全的威脅日益加劇

- 增加政府撥款和國家計劃

- 光纖和衛星量子金鑰分發現場測試進展迅速。

- 與 6G 行動核心網路整合的前景

- 透過擴大光子晶片代工廠規模來降低組件成本。

- 推動與超大規模資料中心業者雲端供應商的混合量子安全雲端互連

- 市場限制因素

- 對量子中繼器和衛星有效載荷的高額資本投入

- 缺乏全球互通性標準

- 當可靠節點無法使用時,光纖PMD的傳輸距離會受到限制。

- 新興國家缺乏低溫基礎設施

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 透過使用

- 量子金鑰傳輸(QKD)

- 安全雲端通訊

- 分散式量子計算

- 量子感測器網路

- 其他用途

- 最終用戶

- 政府/國防

- 大公司

- 通訊/IT

- 金融服務

- 醫療保健和生命科學

- 能源公用事業

- 研究與學術

- 依網路類型

- 地面光纖網路

- 自由空間光鏈路

- 衛星通訊鏈路

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Alibaba Group Holding Limited(Alibaba Quantum Laboratory)

- Alphabet Inc.(Google Quantum AI)

- Amazon Web Services, Inc.

- Anellos Photonics Inc.

- Atos SE

- Baidu, Inc.

- BT Group plc

- China Aerospace Science and Industry Corporation Limited

- D-Wave Quantum Inc.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- ID Quantique SA

- Infineon Technologies AG

- IonQ, Inc.

- Nokia Corporation

- Quantum Xchange, Inc.

- QuTech(Stichting Veldhoven Institute)

- Rigetti and Co, LLC

- SK Telecom Co., Ltd.

- Toshiba Digital Solutions Corporation

- Verizon Communications Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the quantum networking market size is projected to expand from USD 2.78 billion in 2026 to USD 6.94 billion by 2031, registering a CAGR of 20.1% over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Application (Quantum Key Distribution, Secure Cloud Communications, and More), End-User (Government and Defense, Large Enterprises, Telecom and IT, Financial Services, and More), Network Type (Terrestrial Fiber Networks, Free-Space Optical Links, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Quantum Networking Market Trends and Insights

Escalating Cybersecurity Threat from Quantum-Capable Adversaries

Harvest-now-decrypt-later campaigns are accelerating as nation-state actors cache encrypted traffic in anticipation of fault-tolerant quantum computers. With classical public-key cryptography vulnerable, QKD delivers provably secure keys that nullify brute-force decryption. The United States finalized post-quantum algorithms in 2024, yet retrofit efforts will take years, creating a window where QKD provides immediate risk mitigation.China extended its quantum backbone to Johannesburg in 2025, underscoring the geopolitical stakes of secure key exchange. Major banks such as JPMorgan Chase have already linked their trading desks via QKD, citing a 18% reduction in latency compared to software-only alternatives.

Rising Government Funding and National Programs

Public financing de-risks private investment. The U.S. Department of Energy allocated USD 625 million in 2025 for a nationwide quantum-internet prototype.Europe's EuroQCI funnels EUR 730 million (USD 823 million) into a 10,000-kilometer cross-border network. India's USD 750 million National Quantum Mission is constructing a 2,000-kilometer backbone, while Japan's 600-kilometer Tokyo-Osaka link exceeded 1 Mbps key rates in 2024.These coordinated programs accelerate alignment with standards and catalyze vendor ecosystems.

High CAPEX for Quantum Repeaters and Satellite Payloads

Extending QKD beyond 100 kilometers without trusted nodes requires deploying quantum repeaters, which cost approximately USD 2-5 million each. For instance, a 500-kilometer metro loop may require installing around 10 repeaters, significantly increasing costs, particularly in developing regions where budgets are constrained. Additionally, satellite payloads for QKD implementation add substantial expenses, ranging from USD 50-150 million per launch. This is further compounded by the cost of ground-station optics, which can exceed USD 20 million, as reported by spacenews.com. These high costs create significant barriers to large-scale rollouts, limiting adoption primarily to nations with substantial financial resources or those driven by strategic mandates to invest in advanced quantum communication technologies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Progress in Fiber and Satellite QKD Field-Trials

- Integration Prospects with 6G Mobile Core Networks

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 60.18% quantum networking market share in 2025. Quantum random-number generators, single-photon sources, and avalanche photodiodes form the bedrock of secure links. The quantum networking market size attributable to services is projected to grow sharply, with a 20.68% CAGR, as operators wrap managed offerings around these assets. Infineon's cryogenic-ready detector reached 85% efficiency at telecom wavelengths, lengthening viable fiber spans. Parallel foundry scale-ups, such as Quantum Computing Inc.'s thin-film lithium-niobate line, aim to ship 10,000 photonic circuits per quarter by 2027.

Service revenue is consolidating among carriers that can amortize the cost of costly repeaters across thousands of enterprise circuits. Orange Business Services' Quantum Defender prices QKD as a subscription, converting capital outlays into operating expenses. This model allows enterprises to adopt quantum key distribution without significant upfront investments, making it more accessible to a broader range of businesses. Additionally, software vendors are enhancing their offerings by layering key-management orchestration on top of QKD systems, enabling seamless integration with existing IT infrastructures. These solutions are also incorporating post-quantum algorithms to ensure backward compatibility with legacy systems, addressing concerns about future-proofing. As hardware becomes increasingly commoditized, the focus of competition is shifting toward software automation, service quality, and the ability to deliver comprehensive, scalable solutions that meet the evolving needs of enterprise customers.

Quantum key distribution accounted for 62.28% of the quantum networking market in 2025, yet distributed quantum computing is the fastest riser, with a 20.97% CAGR through 2031. Linking multiple processors via entanglement scales logical qubits beyond single-site ceilings, a capability IBM proved by accelerating a variational eigensolver 40% using a three-node network. Hyperscalers now pilot hybrid architectures that blend QKD with post-quantum cryptography to secure data-center interconnects at up to 100 Gbps.

Secure cloud communications are gaining significant traction as the European NIS2 directive mandates that critical infrastructure operators implement quantum-safe encryption measures. This directive has driven organizations to prioritize secure data transmission to ensure compliance with stringent regulations. Quantum sensor networks, while still a niche application, are drawing increasing interest from the defense sector due to their potential in precision timing and gravitational anomaly detection. These networks are expected to play a pivotal role in enhancing defense capabilities. Furthermore, as distributed computing continues to evolve, traffic patterns are anticipated to increasingly rely on entanglement-enabled backbones. This shift will further amplify demand for low-latency QKD (Quantum Key Distribution) links, which are essential for maintaining secure, efficient communication in advanced computing environments.

Geography Analysis

North America captured 50.49% revenue in 2025, driven by significant venture funding, stringent banking regulations, and the U.S. Department of Energy's 17-node quantum internet prototype. Canada invested CAD 360 million (USD 267 million) in 2025 to secure energy and telecom assets, while Mexico initiated pilot projects for university-run QKD links. The region's market leadership is attributed to a strong ecosystem of hyperscalers, defense contractors, and photonics startups concentrated in Silicon Valley, Boston, and Toronto.

Asia-Pacific is projected to grow at a CAGR of 20.88% through 2031. China operates a 10,000-kilometer, 145-node national backbone, highlighting its focus on sovereign technological advancements. Japan, South Korea, and Singapore are expanding metropolitan QKD clusters, while India has allocated USD 750 million for a 2,000-kilometer quantum spine by 2028. Australia is funding quantum memory research to extend the storage time of repeater states. Although regional standards remain fragmented, strong government support is accelerating scalability across the region.

Europe benefits from EUR 730 million (USD 849.9 million) in EuroQCI funding and cohesive regulatory frameworks. Deutsche Telekom's 30-kilometer entanglement teleportation has validated urban deployments, while NIS2 mandates are driving enterprise adoption. The United Kingdom, Germany, France, Italy, and Spain are developing national backbones that are expected to interconnect under EuroQCI by 2027. Smaller economies are following suit, although fragmented telecom markets are slowing uniform adoption. The Middle East and Africa, along with South America, are trailing but showing targeted progress. Saudi Arabia is securing offshore energy assets using QKD, and the UAE is piloting sovereign data links. South Africa has joined China's Beijing-Johannesburg quantum route, bypassing domestic capital expenditure constraints. Brazil is collaborating on satellite ground stations, and Chile is funding quantum sensing for mining applications. However, limited budgets in these regions are tempering large-scale deployments. Across emerging markets, hub-and-spoke satellite models are being explored to overcome limitations in the fiber infrastructure.

- Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- Alphabet Inc. (Google Quantum AI)

- Amazon Web Services, Inc.

- Anellos Photonics Inc.

- Atos SE

- Baidu, Inc.

- BT Group plc

- China Aerospace Science and Industry Corporation Limited

- D-Wave Quantum Inc.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- ID Quantique SA

- Infineon Technologies AG

- IonQ, Inc.

- Nokia Corporation

- Quantum Xchange, Inc.

- QuTech (Stichting Veldhoven Institute)

- Rigetti and Co, LLC

- SK Telecom Co., Ltd.

- Toshiba Digital Solutions Corporation

- Verizon Communications Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Cybersecurity Threat from Quantum-Capable Adversaries

- 4.2.2 Rising Government Funding and National Programs

- 4.2.3 Rapid Progress in Fiber and Satellite QKD Field-Trials

- 4.2.4 Integration Prospects with 6G Mobile Core Networks

- 4.2.5 Photonic Chip Foundry Scale-Ups Lowering Component Costs

- 4.2.6 Hyperscaler Push for Hybrid Quantum-Secure Cloud Interconnect

- 4.3 Market Restraints

- 4.3.1 High CAPEX for Quantum Repeaters and Satellite Payloads

- 4.3.2 Lack of Global Interoperability Standards

- 4.3.3 Fiber PMD Limits Reach without Trusted Nodes

- 4.3.4 Shortage of Cryogenic Infrastructure in Emerging Economies

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Quantum Key Distribution (QKD)

- 5.2.2 Secure Cloud Communications

- 5.2.3 Distributed Quantum Computing

- 5.2.4 Quantum Sensor Networks

- 5.2.5 Other Applications

- 5.3 By End-User

- 5.3.1 Government and Defense

- 5.3.2 Large Enterprises

- 5.3.3 Telecom and IT

- 5.3.4 Financial Services

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Energy and Utilities

- 5.3.7 Research and Academia

- 5.4 By Network Type

- 5.4.1 Terrestrial Fiber Networks

- 5.4.2 Free-Space Optical Links

- 5.4.3 Satellite-Based Links

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- 6.4.2 Alphabet Inc. (Google Quantum AI)

- 6.4.3 Amazon Web Services, Inc.

- 6.4.4 Anellos Photonics Inc.

- 6.4.5 Atos SE

- 6.4.6 Baidu, Inc.

- 6.4.7 BT Group plc

- 6.4.8 China Aerospace Science and Industry Corporation Limited

- 6.4.9 D-Wave Quantum Inc.

- 6.4.10 Fujitsu Limited

- 6.4.11 Huawei Technologies Co., Ltd.

- 6.4.12 ID Quantique SA

- 6.4.13 Infineon Technologies AG

- 6.4.14 IonQ, Inc.

- 6.4.15 Nokia Corporation

- 6.4.16 Quantum Xchange, Inc.

- 6.4.17 QuTech (Stichting Veldhoven Institute)

- 6.4.18 Rigetti and Co, LLC

- 6.4.19 SK Telecom Co., Ltd.

- 6.4.20 Toshiba Digital Solutions Corporation

- 6.4.21 Verizon Communications Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment