|

市場調查報告書

商品編碼

2062424

迷你LED顯示器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Mini-LED Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

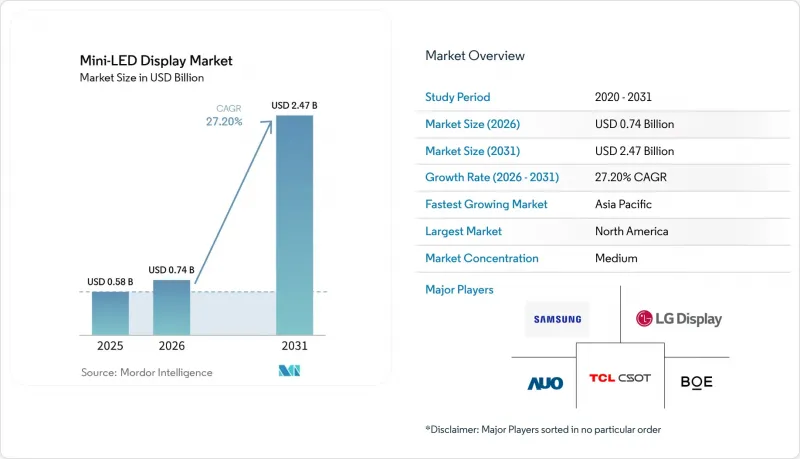

根據 Mordor Intelligence 預測,mini-LED 顯示器市場規模將從 2025 年的 5.8 億美元和 2026 年的 7.4 億美元成長到 2031 年的 24.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 27.20%。

本報告按應用領域(電視、IT顯示器和筆記型電腦、智慧型手機和平板電腦、車載顯示器、穿戴式裝置和AR/VR)、技術(mini-LED背光模組、直下式mini-LED)、背板整合(PCB被動矩陣、玻璃主動矩陣、軟性混合基板)和地區進行細分。市場預測以美元(USD)為單位。

全球Mini-LED顯示器市場趨勢與洞察

微型LED背板成本的下降正在推動市場擴張。

背板製造效率的提升將使TCL背板背板的成本在2025年前每年降低15%至20%,從而消除55至65吋電視與OLED電視的價格差距。共用LCD基礎設施將使TCL能夠攤銷其在玻璃薄膜電晶體(TFT)背板方面的資本投資,使其在2025年上半年實現Mini-LED電視出貨量成長176%。這凸顯了成本與需求之間的彈性。從金屬凸塊到導電光阻劑凸塊的轉變將進一步簡化大規模轉移流程,提高良率,並為2031年前持續降低成本奠定技術基礎。

2025年下半年,電視製造商的產能將逐漸從OLED轉向其他產品。

為因應來自中國品牌日益激烈的競爭(中國品牌在Mini-LED電視出貨量方面佔據主導地位),三星電子和LG電子於2025年下半年將其生產線從OLED轉向RGB Mini-LED技術。這項策略調整使兩家公司能夠縮短前置作業時間,擴展產品線,並透過在2026年國際消費性電子展(CES 2026)上發布的高階機型推出新產品。此舉凸顯了兩家公司對利用先進的LCD背光技術作為競爭優勢的信心,確保它們能夠在不斷發展的顯示技術領域中保持領先地位和競爭力。

在小於 55 吋的顯示器中,組件的成本優勢優於 OLED。

2025年,由於Mini-LED面板的LED陣列密度更高且需要額外的驅動IC,55吋以下的Mini-LED面板價格仍高成本OLED面板。這種成本差距限制了Mini-LED技術在價格敏感型市場(尤其是那些以性價比為關鍵因素的市場)的普及。然而,隨著片上量子點(QD)整合技術的進步,與磷光體相關的成本已開始降低,Mini-LED和OLED之間的成本差距正在逐步縮小。儘管如此,預計到2028年及以後,Mini-LED在中型顯示器領域的應用仍將受到限制。製造商正致力於最佳化生產流程,以提升Mini-LED技術在未來幾年的競爭力。

細分市場分析

至2025年,電視機將佔Mini-LED顯示器市場佔有率的38.23%。這主要得益於高階機型以更低的價格提供比OLED更高的亮度。中國產能的快速成長和補貼政策也推動了這個細分市場的發展。隨著電動車(EV)中10吋以上駕駛座螢幕的普及,預計到2031年,汽車顯示器市場將以27.55%的複合年成長率成長。這些更大的螢幕需要更佳的戶外可視性,以增強駕駛員的視野並支援高級功能。高級駕駛輔助系統(ADAS)和資訊娛樂功能的整合進一步推動了對高性能顯示器的需求。此外,對節能耐用顯示技術的需求不斷成長,預計也將在整個預測期內推動該細分市場的成長。

由於亮度超過1000尼特,且符合DCI-P3 100% HDR認證標準,Mini-LED顯示器在專業顯示器和筆記型電腦中的應用對內容創作者極具吸引力。這些認證保證了卓越的色彩準確度和亮度,這對於影片編輯和圖形設計等專業應用至關重要。雖然Mini-LED在智慧型手機和平板電腦的應用仍然有限,但蘋果的iPad Pro尤其採用了Mini-LED來提升顯示器效能。然而,由於散熱問題和技術高成本,Mini-LED在穿戴式裝置領域仍屬於小眾應用。儘管面臨這些挑戰,但Mini-LED技術的進步可望逐步擴大其在各類設備中的應用。

區域分析

預計到2025年,亞太地區將佔據54.74%的市場。這主要得益於中國垂直整合的生態系統,京東方、TCL、華星光電和天馬等公司整合了LED晶片和麵板的生產,從而提高了生產速度並降低了成本。政府補貼也使國內Mini-LED電視的市佔率接近10%。同時,韓國的三星顯示器和LG顯示已將其產能從OLED轉向Mini-LED,以維持其市場佔有率。此外,該地區受益於強大的供應鏈和政府支持,進一步加速了Mini-LED的普及。消費性電子和汽車應用領域對高性能顯示器的需求不斷成長,也推動了該地區的領先地位。亞太地區將持續保持Mini-LED顯示器市場創新和生產中心的地位。

在北美和歐洲,高階電視和遊戲顯示器廣受歡迎,兩地的汽車製造商都在電動車(EV)駕駛座中採用Mini-LED顯示螢幕,以提升顯示品質和功能。歐盟生態設計法規將於2028年生效,該法規對背光燈的能源效率提出了更高的要求,推動了高密度Mini-LED設計的應用,以提高每瓦亮度。為了滿足日益成長的節能高解析度顯示器需求,這些地區也在增加對顯示器技術的投資。北美和歐洲注重永續性和創新,已成為Mini-LED市場的重要貢獻者。此外,遊戲和家庭娛樂系統的日益普及也推動了對高階顯示解決方案的需求。

預計到2031年,中東地區將以27.81%的複合年成長率(CAGR)成為所有地區中成長最快的地區,這主要得益於商業地產和交通樞紐大規模數位電子看板的普及應用。該地區對基礎設施現代化和先進技術應用的重視,正在推動對Mini-LED顯示器的需求。此外,政府主導的智慧城市建設和公共空間改造計畫也進一步促進了市場發展。雖然南美洲和非洲對市場的貢獻仍然較小,但Mini-LED電視牆已開始在一些備受矚目的城市專案中部署。在這些地區,Mini-LED技術正逐步應用於廣告、娛樂和公共資訊系統等領域,預示著未來巨大的成長潛力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 降低Mini-LED背板的成本

- 電視製造商的產能將在 2025 年下半年從 OLED 轉向其他產品。

- 汽車駕駛座正朝著亮度超過 2000 尼特的顯示器發展。

- Micro-LED的良率問題延長了Mini-LED的市場機會。

- 將於2026年到期的量子點晶片相關專利

- 2025-2027 年客艙娛樂維修

- 市場限制因素

- 55吋以下OLED螢幕的組件成本溢價

- 關於遊戲顯示器HDR光暈現象的申訴

- 2028 年:歐盟生態設計法規禁止使用功率超過 5W 的背光燈。

- 稀土元素磷光體價格波動

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過使用

- 電視機

- IT顯示器和筆記型電腦

- 智慧型手機和平板電腦

- 汽車顯示器

- 穿戴式裝置和增強/虛擬實境

- 透過技術

- 迷你LED背光模組(BLU)

- 直射式迷你LED

- 透過背板整合

- PCB被動矩陣

- 玻璃活性基質

- 軟性混合基板

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- Apple Inc.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- TCL China Star Optoelectronics Technology Co., Ltd.

- Sony Group Corporation

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Osram GmbH

- Epistar Corporation

- Seoul Semiconductor Co., Ltd.

- Cree LED(Smart Global Holdings, Inc.)

- Nationstar Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Konka Group Co., Ltd.

- Hisense Visual Technology Co., Ltd.

- Unilumin Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the mini-LED display market size is projected to expand from USD 0.58 billion in 2025 and USD 0.74 billion in 2026 to USD 2.47 billion by 2031, registering a CAGR of 27.20% between 2026 and 2031.

This report is Segmented by Application (Televisions, IT Monitors and Laptops, Smartphones and Tablets, Automotive Displays, and Wearables and AR/VR), Technology (Mini-LED Backlight Unit, and Direct-Emissive Mini-LED), Backplane Integration (PCB Passive Matrix, Glass Active Matrix, and Flexible Hybrid Substrate), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mini-LED Display Market Trends and Insights

Falling Mini-LED Back-Plane Costs Drive Market Expansion

Back-plane manufacturing efficiencies drove a 15-20% year-over-year cost decline in 2025, closing the price gap with OLED in 55-65 inch televisions. Shared LCD infrastructure allowed glass thin-film transistor back-planes to amortize capital expenditures and enabled TCL to lift Mini-LED TV shipments by 176% in H1 2025, underscoring the elasticity between cost and demand. Shift from metal bumps to conductive photoresist bumps further simplified the mass-transfer workflow, boosting yields and positioning the technology for continued cost compression through 2031.

TV Makers Capacity Switches From OLED in 2H 2025

Samsung Electronics and LG Electronics reallocated production lines from OLED to RGB Mini-LED technology in late 2025 to address the growing competition from Chinese brands, which dominated the Mini-LED TV market in terms of volume. This strategic shift allowed the companies to reduce lead times, broaden their product offerings, and introduce new models through premium tiers showcased at CES 2026. The move highlighted their confidence in leveraging refined LCD back-lighting technology as a competitive advantage, ensuring they remain relevant and competitive in the evolving display technology landscape.

Bill of Materials Premium Over OLED Below 55 Inch

In 2025, Mini-LED panels below 55 inches remained costlier than OLED panels due to the higher LED-array density and the need for additional driver ICs. This cost disparity limited the penetration of Mini-LED technology in price-sensitive market segments, where affordability is a key factor. However, advancements in QD on-chip integration have started to reduce phosphor-related expenses, gradually narrowing the cost gap between Mini-LED and OLED. Despite these improvements, the adoption of Mini-LED in mid-size displays is expected to remain limited until after 2028. Manufacturers are focusing on optimizing production processes to make Mini-LED technology more competitive in the coming years.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Cockpits Shift to >= 2,000-Nit Displays

- Micro-LED Yield Issues Prolonging Mini-LED Window

- HDR Halo Complaints in Gaming Monitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Televisions accounted for 38.23% of the Mini-LED Display market in 2025, supported by premium models that offered higher brightness than OLED at lower prices. The segment benefited from rapid capacity shifts and subsidies in China. Automotive displays are projected to grow at a 27.55% CAGR through 2031 as electric vehicles increasingly adopt cockpit screens larger than 10 inches. These larger screens require superior sunlight readability to enhance driver visibility and support advanced functionalities. The demand for high-performance displays is further driven by the integration of advanced driver assistance systems (ADAS) and infotainment features. Additionally, the push for energy-efficient, durable display technologies is expected to drive growth in this segment over the forecast period.

Adoption of Mini-LED in professional monitors and laptops has strengthened since it met HDR certifications exceeding 1,000 nits and 100% DCI-P3, making it highly attractive to content creators. These certifications ensure superior color accuracy and brightness, critical for professional applications such as video editing and graphic design. Smartphones and tablets saw limited adoption, particularly with Apple's iPad Pro, which used Mini-LED for enhanced display performance. However, wearables remained a niche application due to thermal constraints and the high cost of Mini-LED technology. Despite these challenges, advancements in Mini-LED technology are expected to gradually expand its adoption across various device categories.

Geography Analysis

Asia-Pacific captured 54.74% market share in 2025, driven by China's vertically integrated ecosystem, where BOE, TCL, CSOT, and Tianma aligned LED chip and panel production for speed and cost savings. Subsidies lifted Mini-LED television share toward 10% domestically, while South Korea's Samsung Display and LG Display redirected capacity from OLED to Mini-LED to defend their market share. Additionally, the region benefited from a strong supply chain and government support, which further accelerated adoption. The increasing demand for high-performance displays in consumer electronics and automotive applications also contributed to the region's dominance. Asia-Pacific remains a key hub for innovation and production in the mini-LED display market.

North America and Europe favored premium televisions and gaming monitors, with automakers in both regions specifying Mini-LED cockpits for electric vehicles to enhance display quality and functionality. The European Union's Ecodesign rules, effective in 2028, place efficiency pressure on back-light power, inadvertently encouraging the adoption of high-zone Mini-LED designs that improve luminance per watt.These regions also witnessed growing investments in display technologies to meet e increasing demand for energy-efficient, high-resolution displays. The focus on sustainability and innovation has positioned North America and Europe as significant contributors to the Mini-LED market. Furthermore, the rising popularity of gaming and home entertainment systems has driven demand for premium display solutions.

The Middle East is projected to record the fastest regional CAGR at 27.81% through 2031, propelled by large-format digital signage in commercial real estate and transportation hubs. The region's focus on modernizing infrastructure and adopting advanced technologies has fueled the demand for Mini-LED displays. Additionally, government initiatives to develop smart cities and enhance public spaces have further boosted the market. South America and Africa remain smaller contributors but are starting to deploy Mini-LED video walls in high-visibility urban projects. These regions are gradually embracing Mini-LED technology for applications in advertising, entertainment, and public information systems, showcasing their potential for future growth.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- TCL China Star Optoelectronics Technology Co., Ltd.

- Sony Group Corporation

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Osram GmbH

- Epistar Corporation

- Seoul Semiconductor Co., Ltd.

- Cree LED (Smart Global Holdings, Inc.)

- Nationstar Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Konka Group Co., Ltd.

- Hisense Visual Technology Co., Ltd.

- Unilumin Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Falling Mini-LED Back-Plane Costs

- 4.2.2 TV Makers Capacity Switches From OLED in 2H 2025

- 4.2.3 Automotive Cockpits Shift to >= 2,000-Nit Displays

- 4.2.4 Micro-LED Yield Issues Prolonging Mini-LED Window

- 4.2.5 Quantum-Dot On-Chip Patents Expiring 2026

- 4.2.6 In-Flight Entertainment Retrofits 2025-2027

- 4.3 Market Restraints

- 4.3.1 Bill of Materials Premium Over OLED Below 55 Inch

- 4.3.2 HDR Halo Complaints in Gaming Monitors

- 4.3.3 EU Ecodesign Ban on > 5 W Back-Lights 2028

- 4.3.4 Rare-Earth Phosphor Price Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 TVs

- 5.1.2 IT Monitors and Laptops

- 5.1.3 Smartphones and Tablets

- 5.1.4 Automotive Displays

- 5.1.5 Wearables and AR/VR

- 5.2 By Technology

- 5.2.1 Mini-LED Backlight Unit (BLU)

- 5.2.2 Direct-Emissive Mini-LED

- 5.3 By Backplane Integration

- 5.3.1 PCB Passive Matrix

- 5.3.2 Glass Active Matrix

- 5.3.3 Flexible Hybrid Substrate

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Singapore

- 5.4.4.7 Malaysia

- 5.4.4.8 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Apple Inc.

- 6.4.3 LG Display Co., Ltd.

- 6.4.4 BOE Technology Group Co., Ltd.

- 6.4.5 AU Optronics Corp.

- 6.4.6 Innolux Corporation

- 6.4.7 TCL China Star Optoelectronics Technology Co., Ltd.

- 6.4.8 Sony Group Corporation

- 6.4.9 Nichia Corporation

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Osram GmbH

- 6.4.12 Epistar Corporation

- 6.4.13 Seoul Semiconductor Co., Ltd.

- 6.4.14 Cree LED (Smart Global Holdings, Inc.)

- 6.4.15 Nationstar Optoelectronics Co., Ltd.

- 6.4.16 San'an Optoelectronics Co., Ltd.

- 6.4.17 Tianma Micro-electronics Co., Ltd.

- 6.4.18 Konka Group Co., Ltd.

- 6.4.19 Hisense Visual Technology Co., Ltd.

- 6.4.20 Unilumin Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

櫃檯LED市場規模、佔有率和成長分析:按產品組成、發射頻譜、最終用途、銷售管道、分銷通路和地區分類-2026-2033年產業預測

櫃檯LED市場規模、佔有率和成長分析:按產品組成、發射頻譜、最終用途、銷售管道、分銷通路和地區分類-2026-2033年產業預測 LED模組化顯示器市場預測至2034年-全球分析(按類型、彩色顯示器、像素間距、控制系統、安裝方式、技術、應用、最終用戶和地區分類)

LED模組化顯示器市場預測至2034年-全球分析(按類型、彩色顯示器、像素間距、控制系統、安裝方式、技術、應用、最終用戶和地區分類) 小像素間距LED顯示器市場:2026-2032年全球市場預測(依產品類型、像素間距、技術、安裝方式、應用領域及最終用戶分類)數位看板市場:按格式、安裝位置、交付方式、產業、最終用途和應用分類-2026-2032年全球市場預測

小像素間距LED顯示器市場:2026-2032年全球市場預測(依產品類型、像素間距、技術、安裝方式、應用領域及最終用戶分類)數位看板市場:按格式、安裝位置、交付方式、產業、最終用途和應用分類-2026-2032年全球市場預測 全球LED顯示器市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球LED顯示器市場規模、佔有率、趨勢及成長分析報告(2026-2034年) LED電影螢幕市場規模、佔有率和成長分析(按產品類型、技術、螢幕尺寸、最終用戶、銷售管道和地區分類)-2026-2033年產業預測

LED電影螢幕市場規模、佔有率和成長分析(按產品類型、技術、螢幕尺寸、最終用戶、銷售管道和地區分類)-2026-2033年產業預測 LED模組化顯示器市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和安裝類型分類迷你LED顯示器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能及安裝類型分類

LED模組化顯示器市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和安裝類型分類迷你LED顯示器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能及安裝類型分類 日本LED顯示器市場規模、佔有率、趨勢及預測(依技術、顏色、應用、最終用途及地區分類),2026-2034年

日本LED顯示器市場規模、佔有率、趨勢及預測(依技術、顏色、應用、最終用途及地區分類),2026-2034年 2026年智慧裝卸區發光二極體(LED)顯示器全球市場報告

2026年智慧裝卸區發光二極體(LED)顯示器全球市場報告